Chinese State Investors Do Not Seem to Profit From Higher U.S. Interest Rates

Given the size and composition of its external lending, China should be clearing far more interest income on its reserves and policy lending than SAFE reports.

China is a big external creditor. There isn’t any real debate about this.

It has $3.2 trillion in foreign exchange reserves.

Its deposit-taking state commercial banks have another $1 trillion or so in net foreign assets (and $1.2 trillion in gross foreign assets), including about $300 billion in foreign currency bonds.

China’s non deposit funded policy banks have roughly another $1 trillion in assets.

These holdings are at least partially funded by China’s State Administration of Foreign Exchange (SAFE), out of SAFE’s undisclosed non-reserve foreign currency assets as part of China’s policy of encouraging the “diversified use” of the state’s foreign exchange through co-participation funds.

The China Investment Corporation (CIC) and the national social security fund have some foreign bonds as well (there are $300 billion of bonds implied by the balance of payments that aren’t on the balance sheets of the state commercial banks).

Altogether, the portfolio adds up to at least $5.5 trillion in foreign assets, almost all denominated in a foreign currency and mostly in dollars (the policy banks don’t seem to have lent much in euros).

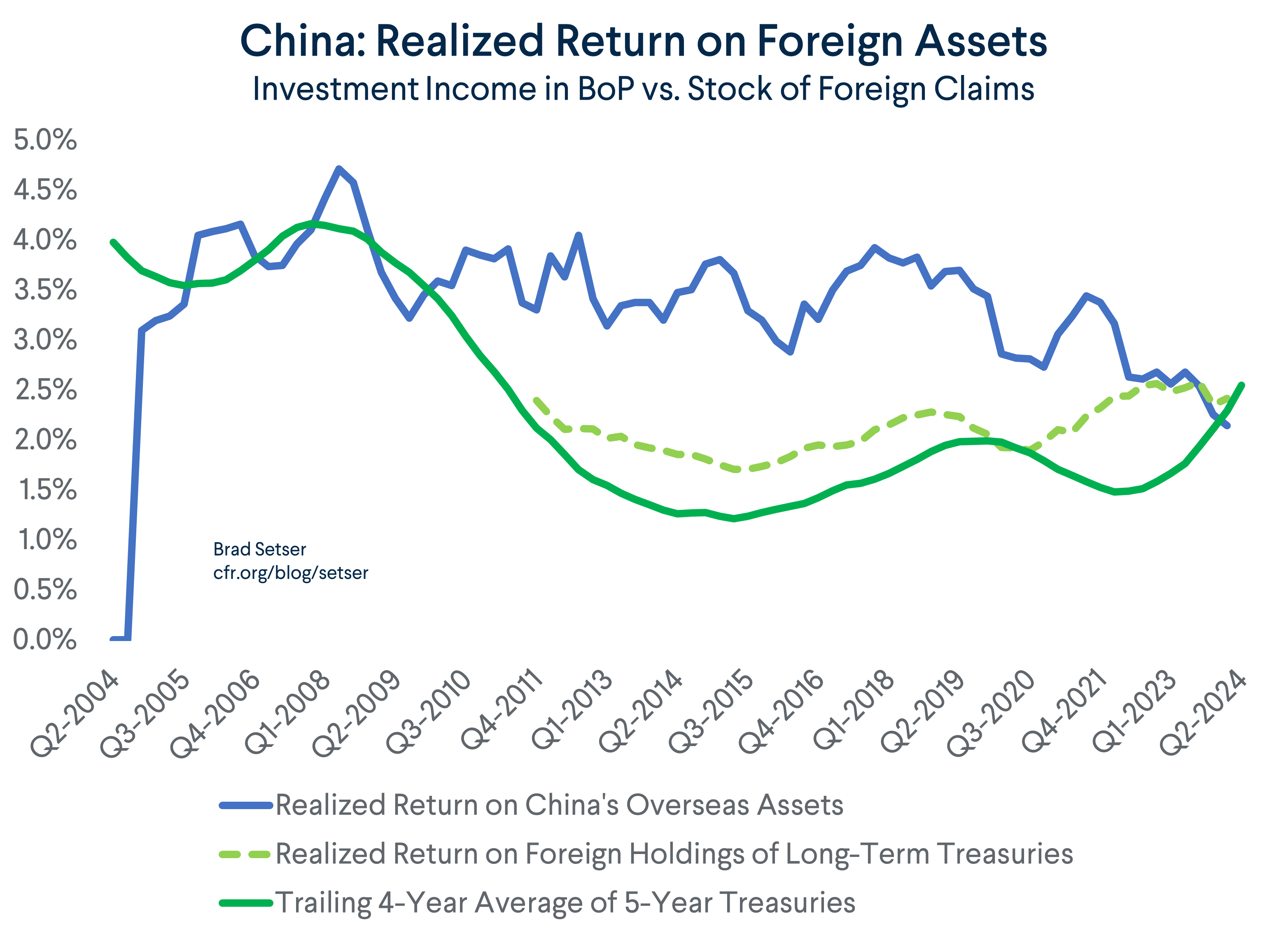

For most of the decade prior to the pandemic, that $5.5 trillion, invested in traditional safe reserve assets like short-term U.S. bills and the shorter end of the U.S. Treasury curve, would have yielded about $110 billion a year in income (a 2 percent average yield)

Over the last year, though, it should have been even more; this portfolio should have yielded something like $250 billion in income.

China, of course, has a fairly diverse reserve portfolio—its reserves are invested in a mix of longer-dated Treasuries (including some inflation linkers), U.S. Agency bonds, European government bonds and Japanese yen (at least partially on a hedged basis).

Its policy banks sometimes lend on concessional terms at a fixed rate, but also do a fair amount of lending at the shorter-term dollar rate and a 300-basis point (or more) spread. Half of Kenya’s $4 billion railway loan, for example, pays LIBOR plus over 300 basis points.

Its commercial banks presumably have a decent chunk of short-term assets (which are a better match for their liabilities) as well some global dollar credit.

The overall balance on investment income also depends on what a country pays on its external borrowing.

But the yield on (unhedged) foreign holdings of Chinese government bonds has collapsed.

Sum it all up, and there is no reason to think the investment income of “China, Inc.” hasn’t increased along with global interest rates over the last five years.

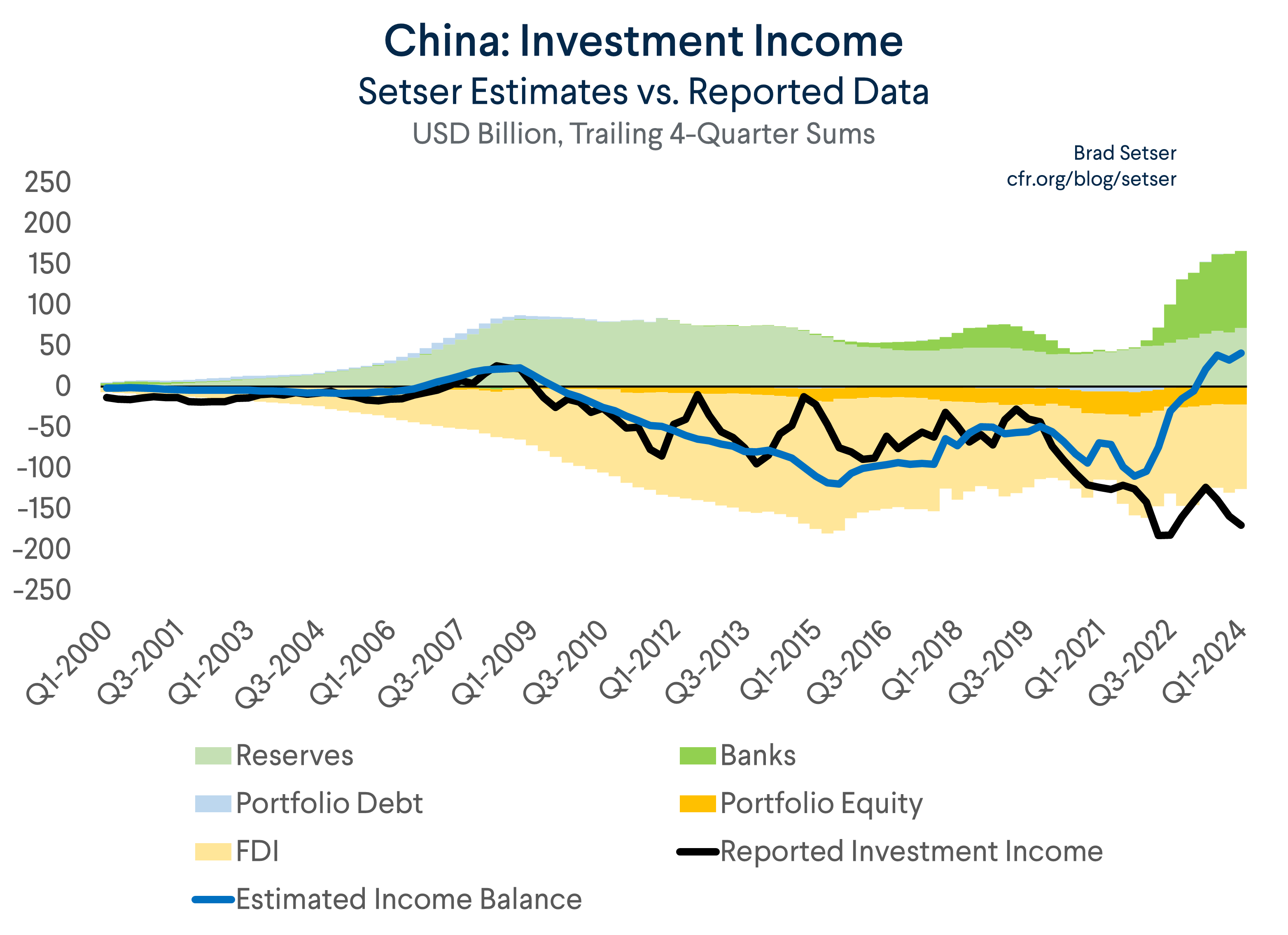

Yet that isn’t what China reports in its balance of payments data.

China doesn’t report any details of foreign income, so its interest income is blurred together with dividend income on foreign equity investments. However, total earnings on investment income have trended down even as global interest rates have trended up, and the bulk of China’s foreign assets should not just pay interest, but generate interest and returns linked to the U.S. dollar interest rate.

That’s strange.

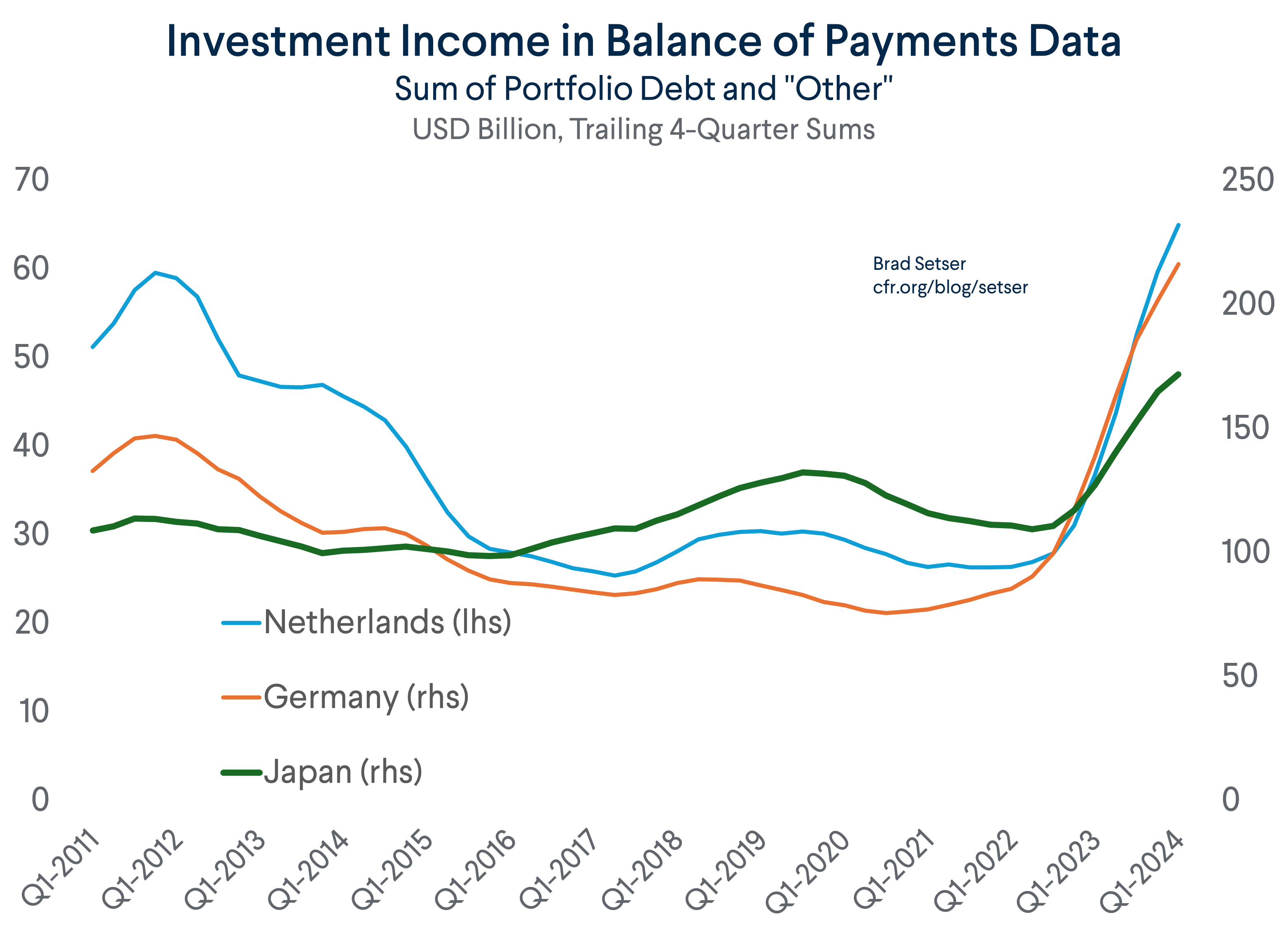

It is even stranger because the interest income of other big creditor countries has done just that—increased alongside dollar interest rates.

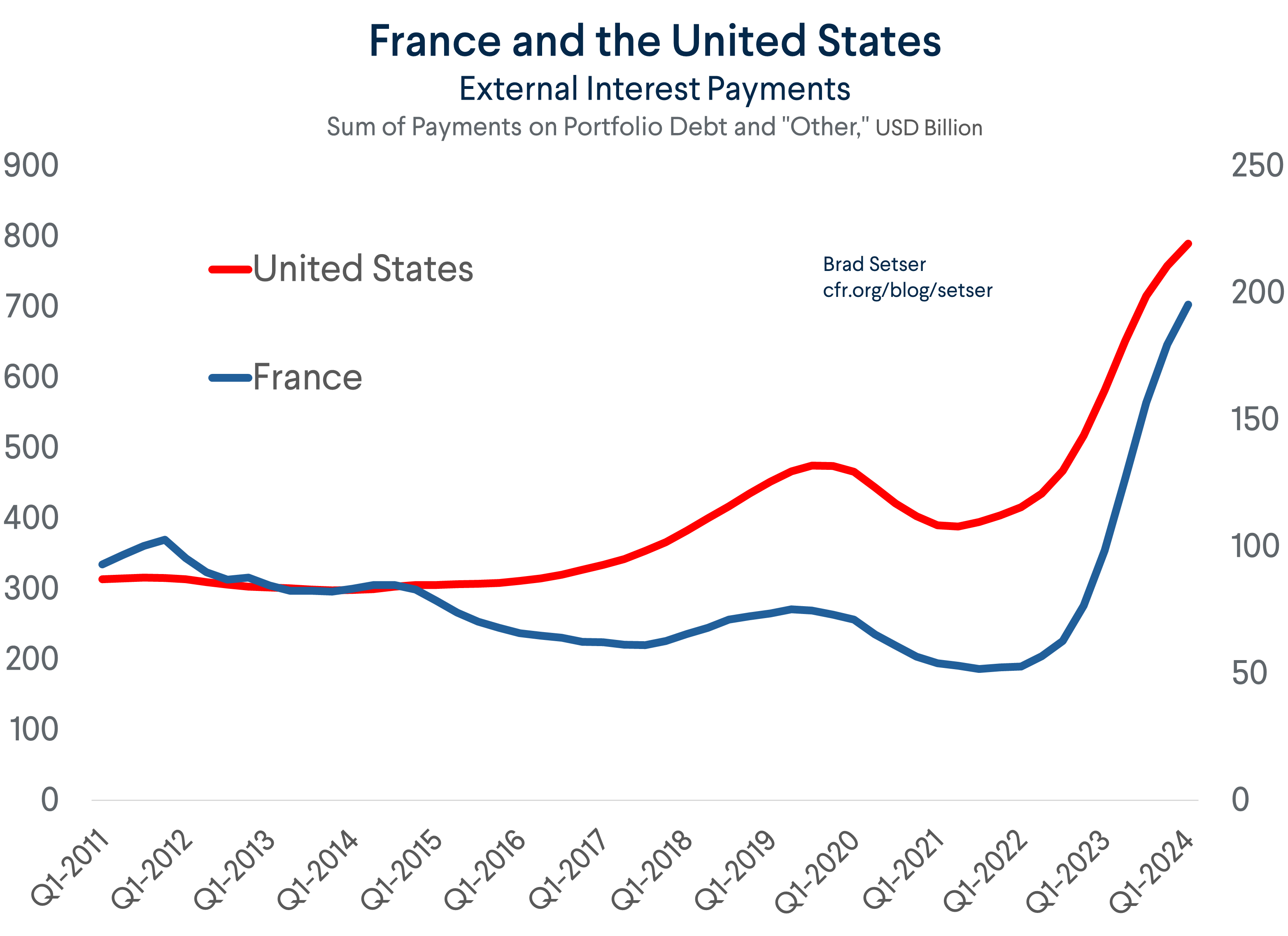

The interest paid by big external borrowers—most prominently the U.S.—has also ticked up.

Bottom line: either the Chinese data is accurate and China’s reserve managers and state banks are simply incredibly bad investors, or China is somehow fiddling with the data. It is quite difficult indeed to understand how investment income could move down when global interest rates are moving up.

Absent any detail from China—and in the face of overwhelming evidence from other creditor countries (and for that matter, data on the payments made by the big debtor countries)—I personally would discount the reported Chinese data.

There are just too many things that don’t add up, or line up, when they should.

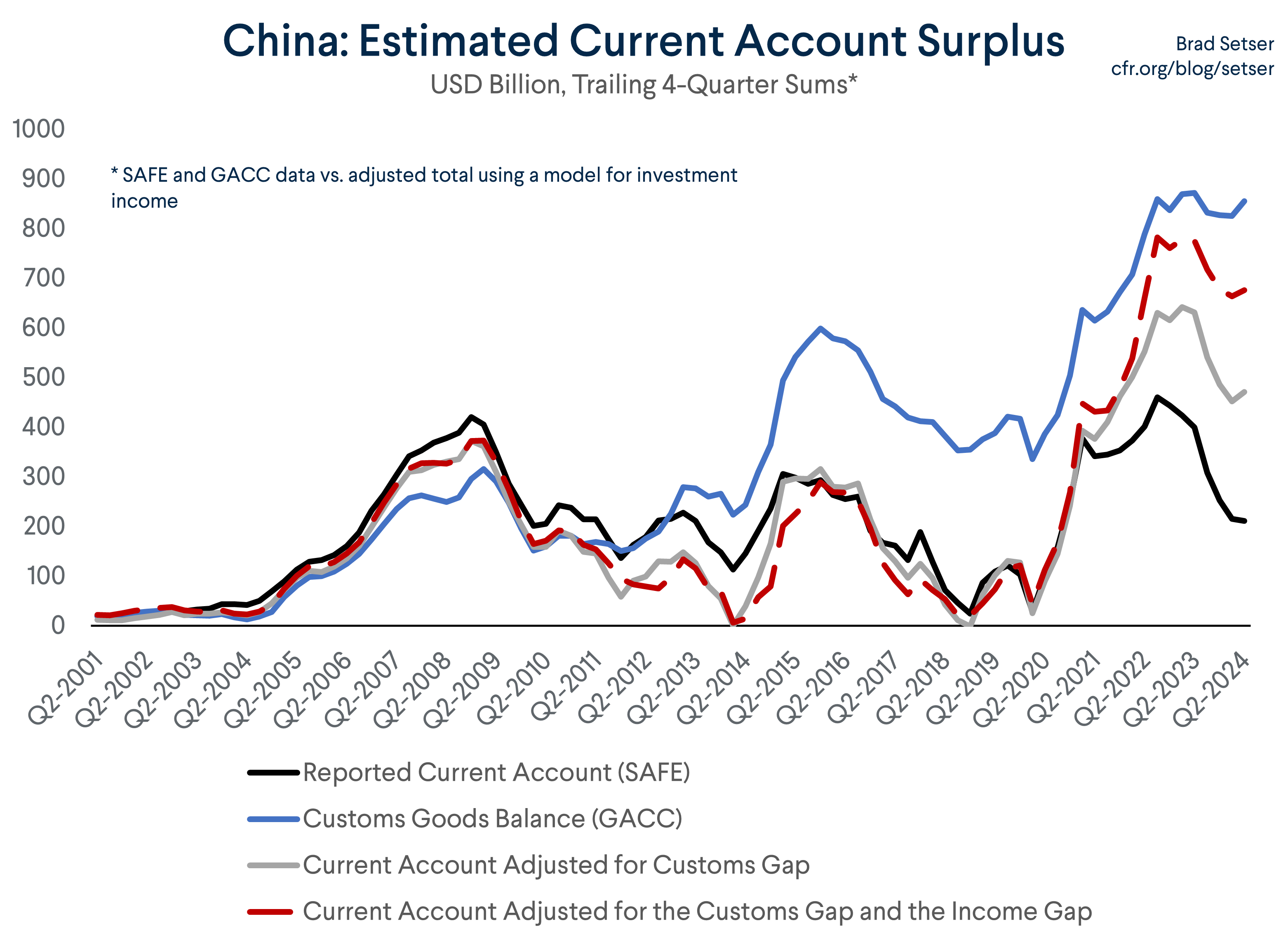

My mark-to-model estimate of China’s investment income balance would generate an overall income surplus—and add about $200 billion to the reported current account.

That is a significant sum, particularly in the context of the major global economies.

The fact that China’s reported investment income balance is still in deficit is one of the main reasons why China’s external balance has evolved in an unusual manner over the last few years.

The use of internal survey/transactions data rather than the customs data to calculate the goods balance, a topic which I cover in a previous blog, is the other main reason why the reported fall in China’s external surplus simply makes no economic sense (it is inconsistent with all other global data sets that I have examined).

For now, my best guess is that China’s external surplus is closer to $700 billion (a bit under 4 percent of GDP) than $200 billion.

If China wants to prove me wrong, SAFE needs to:

1. Provide detail on its investment income calculations—going forward, but also in the back data.

2. Explain why its adjustment to the goods data doesn’t imply offsetting adjustments to other parts of the balance of payments data, given that what should normally be the onshore profits of foreign firms operating in China are getting swept into the trade numbers.