Global Economics Monthly: March 2014

The Fed’s Guidance Dilemma

- Robert KahnSteven A. Tananbaum Senior Fellow for International Economics

Bottom Line: Economists are sharply divided on the question of how much slack exists in U.S. labor markets. The answer matters a great deal. It informs how the Federal Reserve should act and what Fed officials should announce to markets.

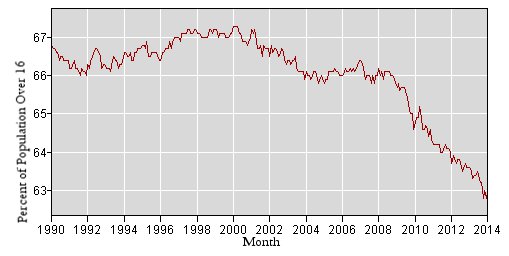

The sharp decline in the U.S. unemployment rate since the recession has become a Rorschach test for economists. At the core of the question is how to interpret the steep and continuing decline in the labor force participation rate. The rate peaked in 2000 and began to drop dramatically following the onset of the recession. (See Chart 1.) For some, the rate reflects inadequate policies that are driving discouraged workers out of the labor force. For others, it is symptomatic of a rapidly tightening labor market and a Fed engaged in a reckless policy of monetary expansion that risks new bubbles and future inflation.

Figure 1. Labor Force Participation

Several recent papers have addressed this question and provided evidence supporting the view that the majority of the decline in labor force participation and the increase in long-term unemployment can be explained by structural shifts, which in this case means a number of things. Demographic changes—notably an aging population of baby boomers choosing early retirement—could be the cause. Changing patterns of labor force participation by students (staying longer in school) and women could also be a factor. In addition, a phenomenon known as hysteresis may contribute to this decline, as people drop out of the labor force due to the recession and then subsequently lose skills and connectedness, making reentry extraordinarily difficult. As of now, we can’t know whether these shifts will reverse as the economy strengthens, but the weight of this recent evidence suggests that much of the move will be longer lasting.

There is a growing body of evidence that inflation responds more to short-term unemployment than long-term unemployment.

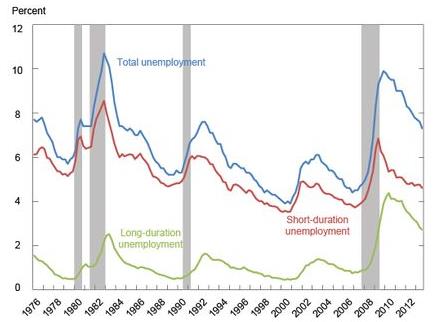

These findings challenge the view that there is significant slack remaining in labor markets, and suggest that monetary policy’s main effect is to draw back into the job market those who have been unemployed only a short period of time. This suggests that inflation and inflationary expectations will be driven by developments in short-term unemployment (defined as being unemployed for twenty-six weeks or fewer), as these are the workers competing for jobs. In this regard, a recent paper by New York Fed staff adds to a growing body of evidence both for Europe and the United States (and both inside and outside the Fed) that inflation responds more to short-term unemployment than long-term unemployment. With short-term unemployment near cyclical lows, this view suggests that there may be less slack in labor markets and less time before inflation begins to rise. (See Chart 2.)

Figure 2. Unemployment Gaps by Duration

What does the Fed believe?

The Fed has always been emphasized that 6.5 percent is a threshold, not a trigger.

Uncertainty over how labor markets will respond to Fed policy comes at a challenging time for the Fed as it tries to fine-tune its forward guidance to markets. At the end of January, the unemployment rate was 6.6 percent, near the 6.5 percent unemployment rate threshold the Fed previously identified Fed as the point at which it would consider hiking rates. (This idea is known as the Evans Rule, named after Charles Evans of the Boston Fed who first proposed it.) The Fed has always emphasized that this number is a threshold after which rate hikes become a possibility, not a trigger. But markets nonetheless linked their expectations of liftoff in rates to developments in the unemployment rate.

As unemployment fell toward 6.5 percent over the last several months, the Fed sought to shift the focus away from the unemployment rate to other indicators. The December Fed statement signaled that economic conditions would warrant keeping the Fed funds rate near zero “well past the time” unemployment crossed 6.5 percent. Janet Yellen, in her congressional testimony to become Federal Reserve chief, emphasized that slack still remains and that the Fed is looking at a range of indicators in assessing conditions. From a market perspective, Yellen had jettisoned the Evans rule, signaling that the headline threshold of 6.5 percent unemployment is no longer the dominant factor in setting monetary policy. The large number of long-term unemployed means that the labor market is weaker than it appears. Other measures will assume more importance.

If the Evans rule is abandoned, what should replace it in the Fed’s guidance? One alternative is simply to adopt a lower unemployment rate threshold, for example 6 percent. But it makes little sense to pick another number that has a tenuous relationship to inflation. Another alternative is to stress a wider range of indicators that will guide the Fed’s decision about when to begin hiking interest rates. Yellen’s comments point in this direction, and go a step further by shifting the focus to longer-term unemployment and other indicators suggesting significant additional slack. There are two risks here. The first is that by highlighting several variables, the message could be muddied. The second problem is the assumption that wage pressure will remain weak even as short-term unemployment falls, because the long-term unemployed will be pulled back into the market. What if this view is wrong? To the extent that inflation depends on short rates, the risk exists that inflationary pressures could emerge, forcing the Fed to make a policy U-turn. In sum, the shift in the Fed’s guidance could make markets more vulnerable to any inflationary shock.

A third alternative would be to shift the focus away from when the first rate hike will take place and instead provide guidance about where rates would likely head over the longer term. The Fed’s forecasts assume that interest rates will rise slowly, and remain at historically low levels for a significant period after they start to increase. To the extent markets believe this forecast, long-term interest rates should remain low. In this regard, the Bank of England may point the way. In the United Kingdom, unemployment is nearing the 7 percent threshold that had earlier been cited as part of the Bank of England’s forward guidance. There, too, Bank of England head Mark Carney is trying to reorient the discussion away from the listed unemployment rate and refocus on a slow, gradual pace of rate hikes that will follow. Carney, who perhaps has been more transparent in this regard, last month referred to “stage two” of forward guidance in which other indicators mattered more than unemployment.

Inflation data will matter more in the discussion of when rates will lift off.

At a time when questions are being raised about the impact of asset purchases (quantitative easing) on activity, forward guidance is now the most powerful tool in the central banker’s toolbox. But that also creates the risk of sharp adjustments when guidance is proven wrong or changes. If the long-term unemployed and those who have dropped out of the labor market exert downward pressure on wages, rates could remain at zero for some time before lifting off. However, if short-term unemployment is at a level where price pressures could soon emerge, Janet Yellen’s job could become more difficult. Given uncertainty about the degree of slack in the labor market, inflation data will matter more in the discussion of when rates will lift off, and markets may be more sensitive to inflationary news.

Looking Ahead: Kahn’s take on the news on the horizon

Growth Investments

Group of Twenty (G20) finance ministers pledged $2 trillion to support growth. It’s unlikely to happen, but can the effort to put flesh on the bones lead to some useful infrastructure initiatives?

Financing for Ukraine

Ukraine needs financing and cannot wait until after elections for a full International Monetary Fund program. A bridge loan package needs to be arranged.

European Qualitative Easing

Good economic news has quieted talk of a European Central Bank (ECB) rate cut, but pressures will reemerge soon.t

Report

Report Report

Report Report

Report Report

Report Report

Report Report

Report