Global Economics Monthly: May 2014

Russia Contagion: Local or Global?

- Robert KahnSteven A. Tananbaum Senior Fellow for International Economics

Bottom Line: Given Russia’s economic and financial links to world markets, sanction decisions need to consider the realistic possibility of contagion.

Conventional wisdom has it that sanctions will impose a cost on Russia, but that absent a major intensification of the conflict the effects will be concentrated in the region with limited global impact. To date, sanctions have been modest, targeting a limited number of individuals, their companies, and small banks. But a set of tougher industry-wide sanctions affecting finance, energy, and defense are reportedly under consideration.

In part, this belief in limited, regional contagion reflects a relatively sanguine view among investors about the prospects of an escalation of tensions, a position many in the foreign policy community do not share. If the probabilities and the implications are hard to measure, it is not surprising that many in the markets choose not to give much weight to severe downside scenarios. That optimism could prove untenable if the darker views of Russian president Vladimir Putin’s plans prove accurate.

In addition, it is often argued that Russia simply is not critical to the global markets. For example, Goldman Sachs Research argues that despite contributing 3 percent of global gross domestic product (GDP) and significant energy exports, Russia’s limited integration in global supply chains and international financial markets means “repercussions for the global economy of current tensions might be relatively small.” Their firm’s greater concern is that Russia may respond to sanctions by turning inward. From that perspective, the long-term isolation of the Russian economy is the primary legacy from sanctions.

These arguments are reflected in current market prices. Though Russian bonds are down 6.9 percent and equities are down 9.6 percent on the year, global equity markets are broadly unchanged and appear more likely to be moved by industrial country growth and rate developments rather than shifting information on sanctions. Emerging market spreads are near historically tight levels, further suggesting delinkage from Russia (and risk appetite from yield-hungry investors). One can either be comforted by the stability of global markets or concerned about the prospect of a sharp market correction if these assumptions are disproved.

What will matter for the contagion debate is that the Russian market is too interconnected with the world to ignore.

Last month I looked at the case for sanctions having a material effect on Russia. I argued that the answer was yes, primarily because of Russia’s complex, leveraged, and opaque financial linkages with the West. This month, I turn the focus to the channels for contagion within and outside Russia if the conflict intensifies and the West moves to extend sanctions to entire industries such as energy, finance, or high tech.1 Sanctions have never been imposed on a country as large and complex as Russia, making quantification difficult, but a preliminary assessment suggests effects that are far more sizeable than indicated by conventional wisdom. It is a mistake to focus on whether Russia is big enough to matter; what will matter for the contagion debate is that the Russian market is too interconnected with the world to ignore. However, policies can be put in place to limit the dislocations for the West.

Domestic Markets: Tight Macro Policies Magnify Sanctions

Russia’s economy already was weakening before the Ukraine crisis. Between 1999 and 2008, growth averaged 7 percent, but the Russian economic miracle was deflated by the financial crisis. Activity fell more than 10 percent from 2008 to 2009, and the subsequent recovery has been disappointing. Sanctions have tipped the Russian economy into recession, with some forecasts showing that intensified sanctions could result in a sudden stop in capital flows that would lead Russia’s economy to fall 4 percent or more this year.

Russia has limited scope to ease policies to offset a sanctions shock that cut off its access to global capital markets and restricted trade. The scope for fiscal expansion is limited by concerns about inflation and priority military spending, while monetary policy is constrained by the external weakness and concern that high inflation could undermine the government’s support with pensioners and the poor. In the face of large-scale capital outflows, the central bank has raised interest rates twice and allowed the exchange rate to depreciate. If such pressures continue, Russia does have large amounts of international reserves. Assuming that gold and three months of imports are untouchable, there is still around $125 billion remaining that could be spent defending the exchange rate. Nonetheless, with capital outflows of $60 billion to $70 billion in the first quarter alone, the scope for foreign exchange intervention is limited. Meanwhile, the central bank is funding state spending through a variety of instruments, such as infrastructure bonds and joint ventures, potentially crowding out new private sector lending. This suggests little scope for an easing of policy to offset a sanctions shock.

Channels of International Contagion

The effects of sectoral sanctions for Russian growth could be quite severe. However, whether that shock reverberates through the global economy depends less on the magnitude of the Russian recession and more on the economic and financial channels through which Russia is linked with the West. Though much of the public discussion has focused on critical trade ties, the prospect of contagion there may be limited, while the financial channels of contagion have the potential for outsized spillovers.

Global Trade: It’s About Commodities

Russian raw materials—energy, agriculture, metals and mining—represent the bulk of Russian exports. Sanctions can block trade in these goods, both directly and through restricting the financing of this trade, potentially causing disruptions in global production of raw material–intensive manufacturing. Beyond raw materials, however, the links are more limited. Russia exports few manufactured products to the West. Russian supply chains are dominated by the former Soviet Union and Russian exports are not critical inputs to Western manufacturing beyond its role as an energy supplier. Anecdotally, though, some large U.S. manufacturers fear a disruption of production if rare raw materials for which Russia is a major supplier are blocked.

My base assumption would be little or no change in oil prices after a short period of adjustment.

Much of the discussion in the press has focused on the effects on the energy industry, given the importance of Russian exports to Europe. A cutoff in natural gas exports certainly would create bottlenecks in supply and a spike in natural gas prices. By some estimates, the increase in gas prices could be 20 to 40 percent. What would happen to oil prices? Arguably, the effects would be much smaller, as non-Russian sources fill the European gap and Russia sells to Asia. Indeed, given the global nature of oil markets, the end result may be more a reallocation of oil supplies than a substantial shift in supply. Some economists have argued that oil prices may even fall if non-Russian producers react to the disruption in supplies by releasing oil from reserves and pumping more, but it would be unusual to see a sustained and globally coordinated policy that more than offsets any global shortfall. My base assumption would be little or no change in oil prices after a few months for markets to adjust. Finally, the dependence of Russia on oil and gas revenue (65 percent of exports and 35 percent of revenue) leads optimists to suggest that Russia might look elsewhere to retaliate, particularly if ongoing capital flight continues to pressure international reserves and the currency.

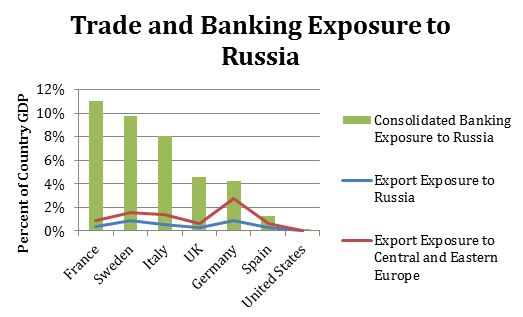

Financial Linkages: Bigger Than They Seem

I have argued elsewhere that the costs of sanctions will be greatest in the financial arena, given the high degree of leverage and opacity in Russian financial linkages to the West (Figure 1). First, sanctions and retaliation could force a rapid deleveraging of Russian financial institutions. This sceario could cause sizeable losses for Russian and international investors, which would be compounded by the reduction in global risk appetite. Second, a flight to safe havens might lead Group of Seven (G-7) treasury securities to rally, but risky assets could be hit globally. Third, financial market sanctions could have dramatic effects not only on Russian financial institutions but also on the markets in which they operate. For example, Russian banks hold significant derivative positions and sanctions on those companies could damage liquidity and market trust.

The high level of uncertainty gives rise to a defacto tax on financial intermediation, which is another feature exacerbating the contagion from financial sanctions. It is evident from the sanctions to date that the major effects on Russia stem from concerns that financial ties with Russian companies could lead to future problems. The high costs of unwinding financial relations acts as a break on making deals today.

The prospect of financial distress is hard to measure, but the experience with past emerging market crisis underscores the vulnerability that comes from high levels of debt. Russia has large external debts (over $700 billion, or 34 percent of GDP), of which two-thirds is public debt. State-owned enterprises are highly leveraged and dependent on the central bank for liquidity to fund external asset purchases. Financial sanctions could, by freezing assets, expose investors to losses on gross rather than net positions. Foreign exposure to Russian equity is more limited, suggesting that losses in those markets will not have independent and significant effects on global markets.

Finally, any disruption to payments systems could have cascading consequences. Those of us of a certain age recall the Christmas tree–light problem. If one of the lights malfunctioned, the entire chain would not work, and it was painful trying to figure out which light was causing the outage. Similarly, if any U.S. entity is involved in any link of a chain of transactions, the potential exists for the entire transaction to fail. That is the interconnectedness problem at the core of sanctions in the complex financial markets we have today.

Figure 1: Costs of Sanctions in the Financial Arena

Summing up

It is too sanguine to assume that the effects of sanctions, should they intensify to include whole sectors of the Russian economy, will be limited to the region. In the end, it is a global market, and delinking Russia from it will have important implications for all parties. At the same time, these costs must be weighed against the costs of doing nothing and the risk of protracted instability. At a time when Russia is testing the existing rules of the international order, preserving the integrity of the Ukrainian state and supporting its economic and political reform may tip the balance toward action.

Looking Ahead: Kahn’s take on the news on the horizon

Japanese Quantitative Easing

Faltering growth and inflation prospects will increase pressure on the Bank of Japan to double down on quantitative easing.

Emerging Market Growth

Evidence grows that the emerging market slowdown will persist. How will markets adjust to emerging markets growing more slowly than industrial countries?

Federal Reserve Meetings

The May meeting could be the first with new members Stanley Fischer and Lael Brainard, and markets may be extra sensitive to hints of future policy directions.t

Report

Report Report

Report Report

Report Report

Report Report

Report Report

Report