China’s Asymmetric Basket Peg

The implications of Brexit understandably have dominated the global economic policy debate. But there are issues other than Brexit that could also have a large global impact: most obviously China and its currency.

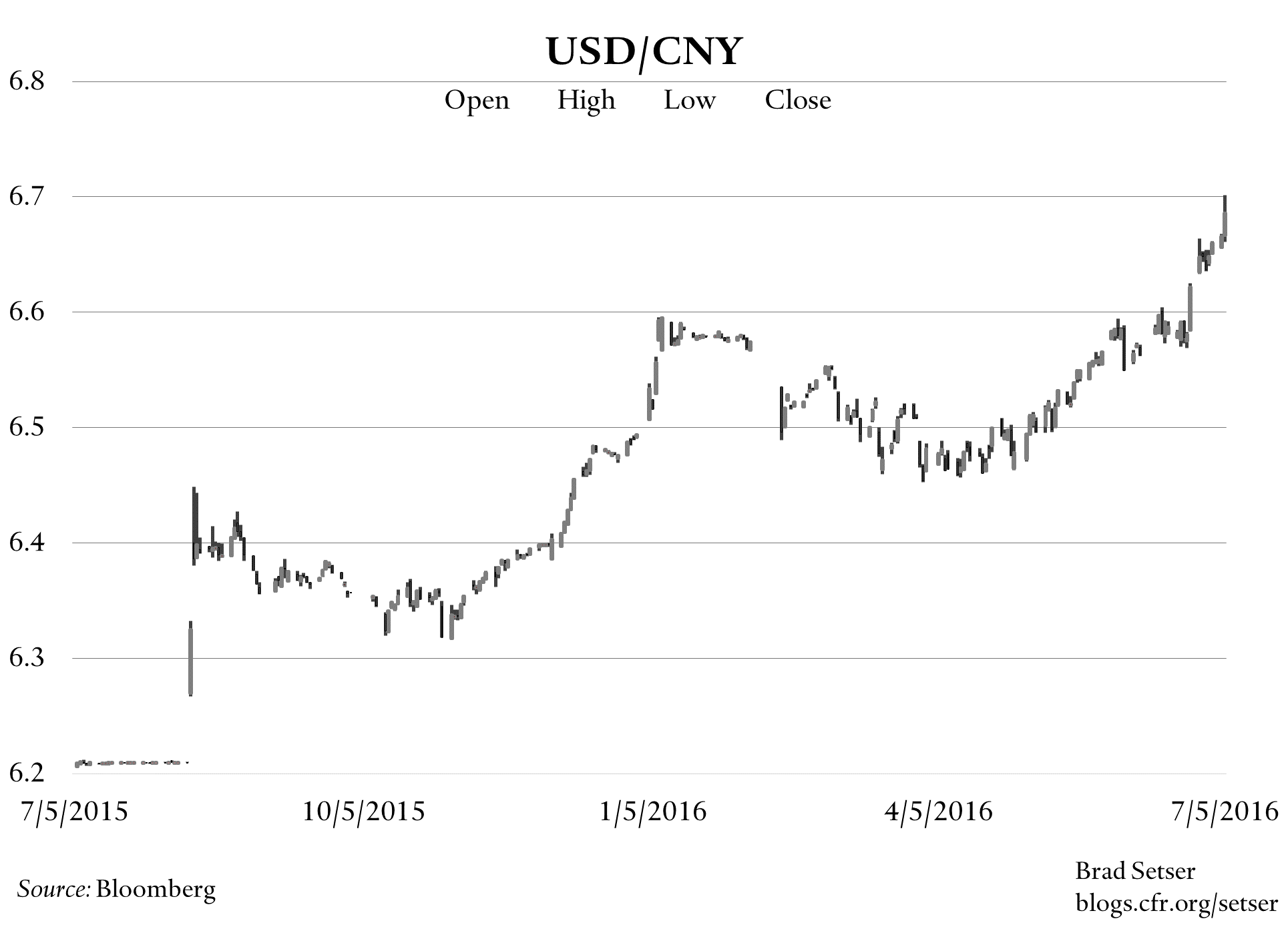

The yuan rather quietly hit multi-year lows against the dollar last week. And today the yuan-to-dollar exchange rate (as well as the offshore CNH rate) came close to 6.7, and is not too far away from the 6.8 level that was bandied about last week as the PBOC’s possible target for 2016.*

The dollar is—broadly speaking—close to unchanged from the time China announced that it would manage its currency with reference to a basket in the middle of December.*

So the yuan might be expected to be, very roughly, where it was last December 11. December 11 of course is the day that China released the China Foreign Exchange Trade System (CFETS) basket. Yet since December 11, the yuan is down around 1.5% against the dollar, down about 5 percent against the euro and down nearly 19 percent against the yen.

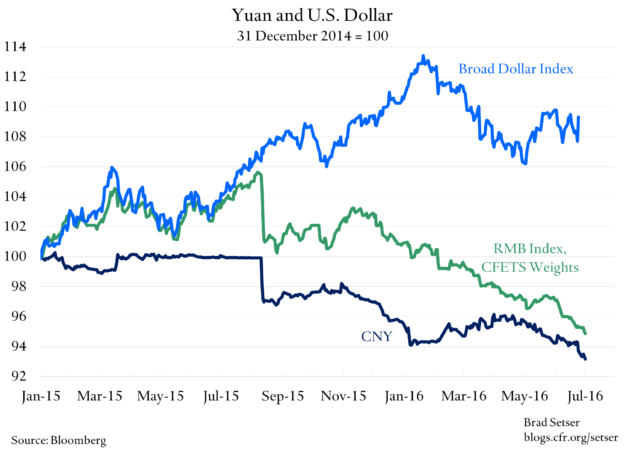

The reason why the renminbi is down against all the major currencies, obviously, is that managing the renminbi “with reference to a basket” hasn’t meant targeting stability against a basket. As the chart above illustrates, over the last seven months the renminbi has slowly depreciated against the CFETS basket. The renminbi has now depreciated by about 5 percent against the CFETS basket since last December, and by about 10 percent since last summer.

How? No doubt there are many tricks up the PBOC’s sleeve. But one is straightforward. When the dollar goes down, China hasn’t appreciated its currency by all that much against the dollar. And when the dollar goes up, China has depreciated against the dollar in a way that is consistent with management “with reference to a basket.”

That takes advantage of the fact that the yuan’s value against the dollar is what matters inside China, while the broader basket matters more for trade. And it takes advantage of the fact that politically the yuan-to-dollar exchange rate matters more than the yuan-to-euro exchange rate.

So even if the yuan was a bit overvalued last summer, it isn’t obviously overvalued now.

China’s manufacturing export surplus remains quite large. And export volume growth—which was falling last summer—has now turned around. It is not realistic for Chinese export volumes to outperform global trade by all that much any more; China is simply too big a player in global trade. China will have to adjust to a new normal here.

My hope is that China will pocket the depreciation achieved over the last several months, and will now start managing its currency more symmetrically or even be somewhat more willing to allow a stronger dollar to flow through to a stronger yuan.

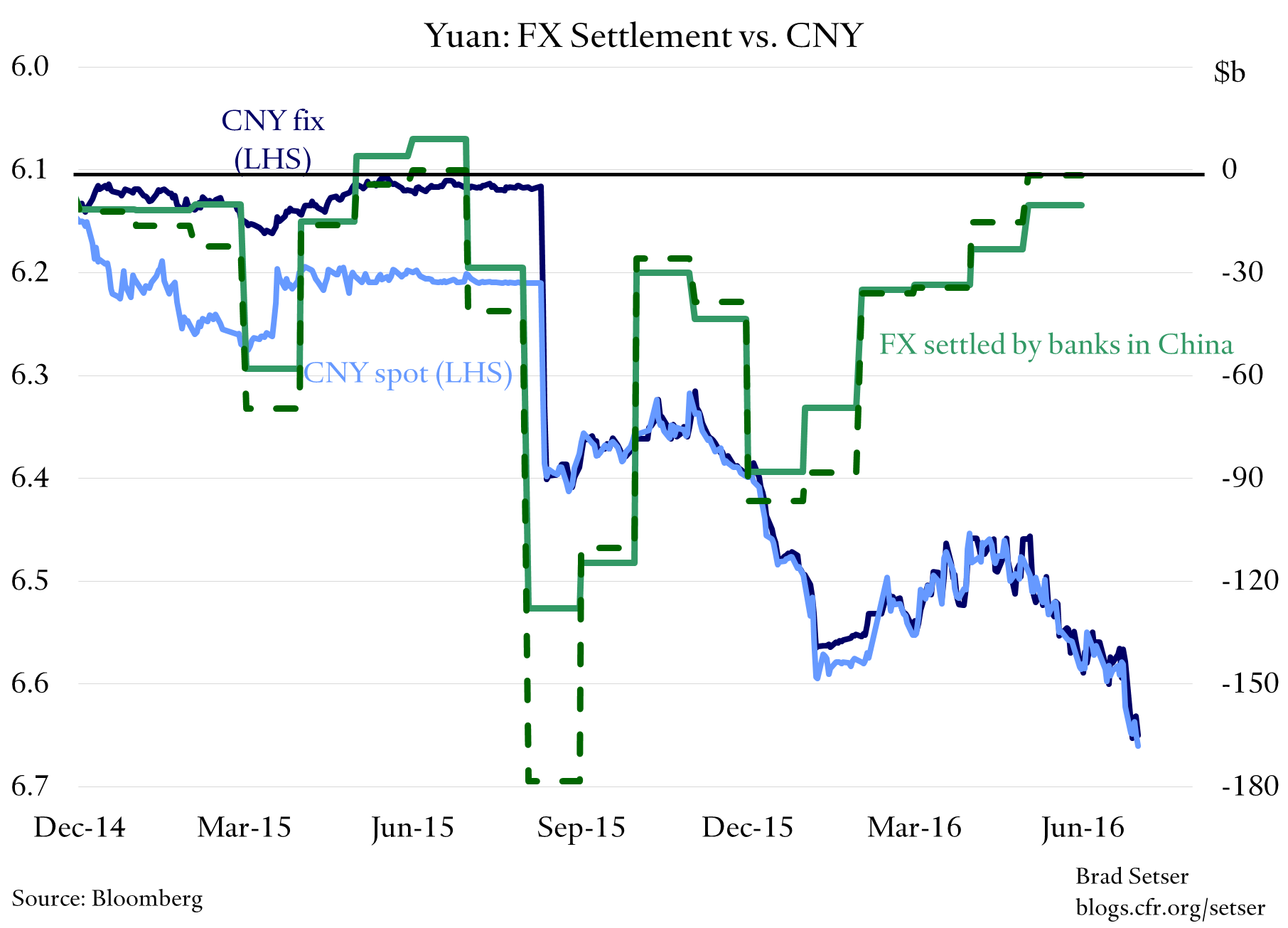

Since January, the expectation of stability (more or less) against the dollar together with the repayment of (unhedged) external debt, a tightening of controls and the threat of intervention in the offshore market seem to have reduced outflow pressures. The fairly steady depreciation against the basket has coincided with smaller reserve sales.*** But there is a risk that speculative pressure could return if the market concludes that China thinks it can now depreciate against a basket thanks to tighter controls and less external debt.

And, obviously, if depreciation against the basket can only be achieved through depreciation against the dollar, it is hard to see how the yuan doesn’t become even more of a domestic political issue in the United States. 6.8 against the dollar brings the renminbi back to its level of eight years ago, more or less.

* Reuters: “China’s central bank would tolerate a fall in the yuan to as low as 6.8 per dollar in 2016 to support the economy, which would mean the currency matching last year’s record decline of 4.5 percent, policy sources said.” The PBOC indirectly pushed back against the story, and has reiterated that it is committed to a “basically stable” renminbi. The Reuters story can also be read two ways: as a signal that China wants a steady depreciation against the dollar, or a signal that there is a limit on how far China is willing to allow the yuan to depreciate against the dollar even if the dollar starts to appreciate against the majors.

** China’s basket doesn’t mirror the U.S. basket. Japan for example, has a 15 percent weight in China’s basket versus a 6-7 percent weight in the Federal Reserve’s broad index, and Canada and Mexico figure more prominently in the U.S. index. The pound, incidentally, has a 4 percent weight in the CFETS basket. Still, the dollar index provides a rough guide to how China would move if it pegged to the dollar.

*** Goldman’s Asia team has suggested that Chinese firms have been settling imports with renminbi in 2016, and this flow likely reflects an orchestrated attempt to limit pressure on the currency that should be counted as a form of hidden intervention. I will take that argument up at a later time. But even with the Goldman adjustment, the pace of reserve sales (using the settlement data) has fallen from $100-150 billion a month in January to $25 billion or so in April and May.