What Did the Greenspan Fed Do with Its “Considerable Time” Pledge in ’04?

By experts and staff

- Published

Experts

![]() By Benn SteilSenior Fellow and Director of International Economics

By Benn SteilSenior Fellow and Director of International Economics

By

- Dinah WalkerAnalyst, Geoeconomics

The big question for the December 16-17 FOMC meeting is whether to drop the pledge to keep rates at near-zero for a “considerable time.” Prior to the last meeting in October, two-thirds of primary dealers expected that language to be modified before the end of the year.

Can history be any guide?

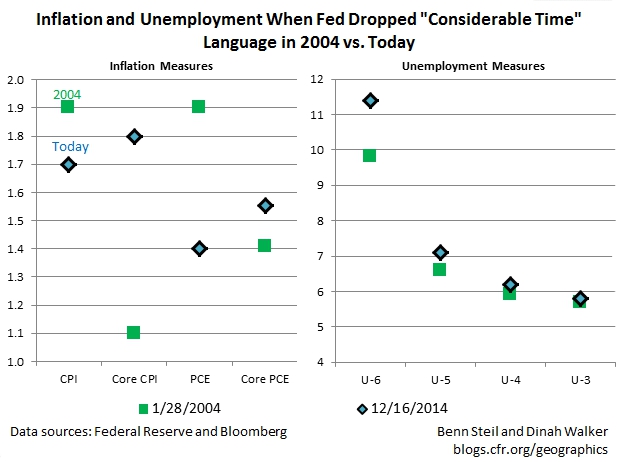

Eleven years ago, at the January 2004 meeting, the Greenspan Fed faced precisely the same question, with the markets watching intently. At that time it had been operating for 6 months under a pledge not to raise rates for a “considerable period.”

As the figure above shows, measures of core inflation, which the Fed favors, were lower back then. And unemployment at the time was almost precisely where it is now (except for U-6*, which was lower).

And what did the Greenspan Fed do? It dropped its “considerable period” pledge, saying instead that “the Committee believes that it can be patient in removing its policy accommodation.”

If history is a guide, then, the Yellen Fed will drop its “considerable time” pledge on Wednesday, paving the way for a possible rate hike in the middle of 2015.

* Total unemployed, plus all persons marginally attached to the labor force, plus total employed part time for economic reasons, as a percent of the civilian labor force plus all persons marginally attached to the labor force

Read about Benn’s latest award-winning book, The Battle of Bretton Woods: John Maynard Keynes, Harry Dexter White, and the Making of a New World Order, which the Financial Times has called “a triumph of economic and diplomatic history.”