Geo-Graphics

A graphical take on geoeconomics, by Benn Steil, Senior Fellow and Director of International Economics.

Part of the Greenberg Center for Geoeconomic Studies

Latest Posts

Full Archive

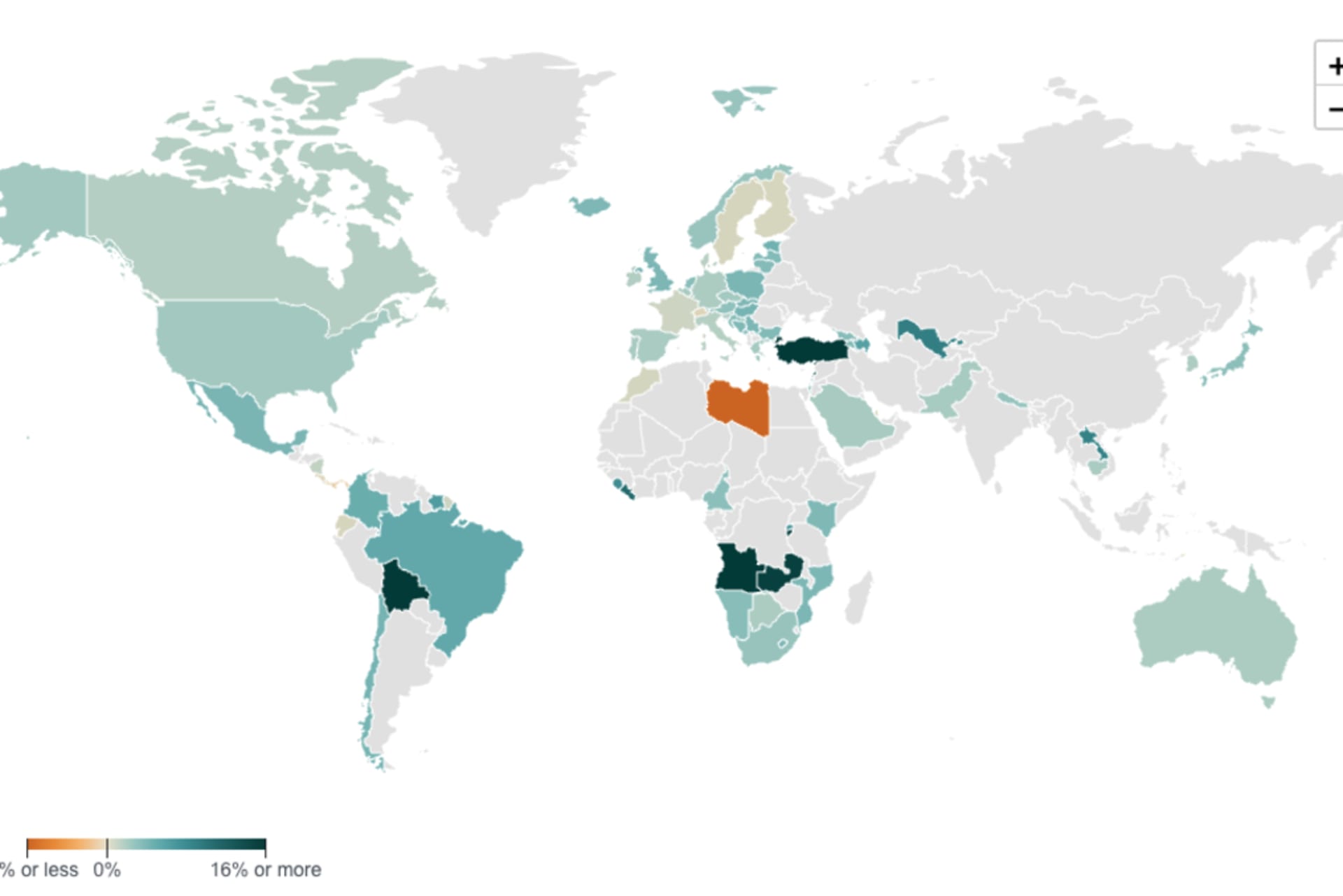

Global Inflation Tracker

By Benn Steil and Yuma Schuster

The CFR Global Inflation Tracker allows you to gauge trends in prices across the world over time. Inflation Data by Country The map below aids in gauging inflation trends in almost two hundred countries around the world—mainly those that report data to the International Monetary Fund (IMF). The inflation rate is defined as the rate of […]

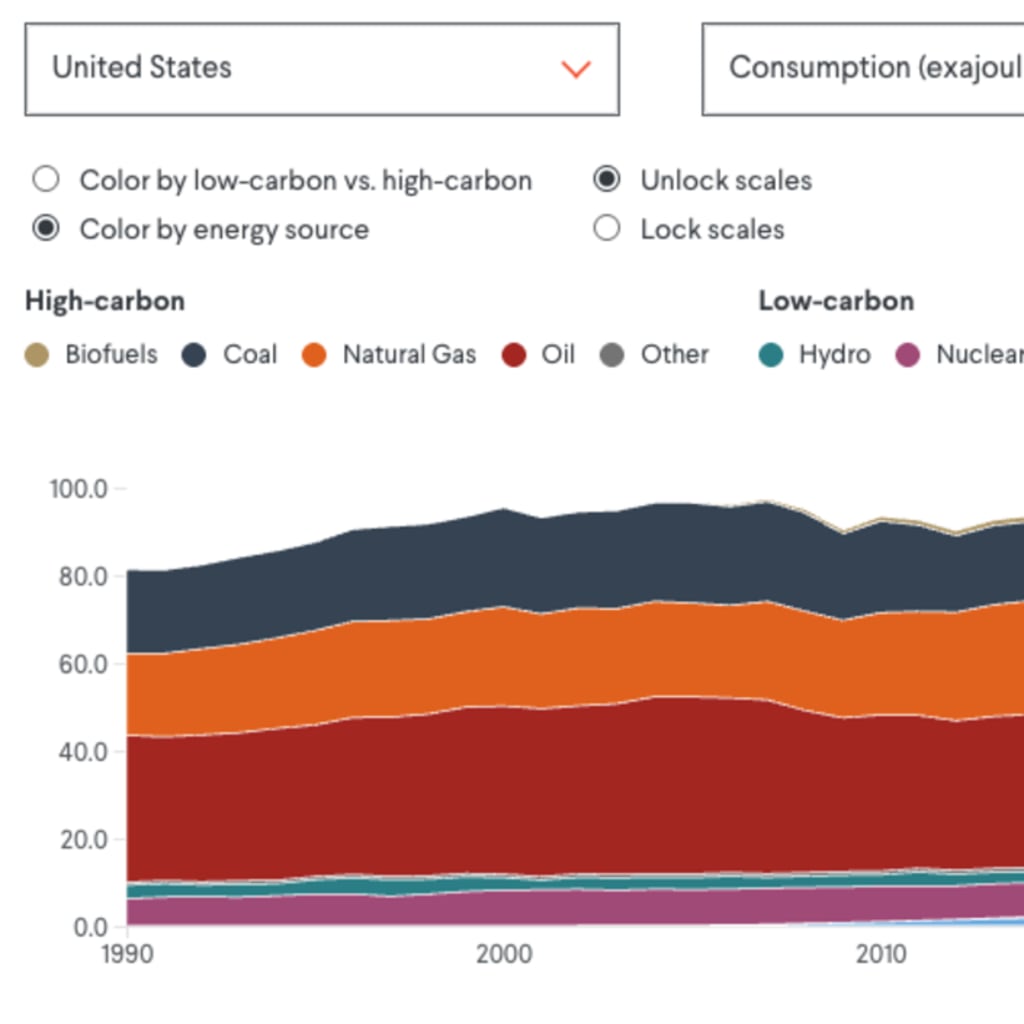

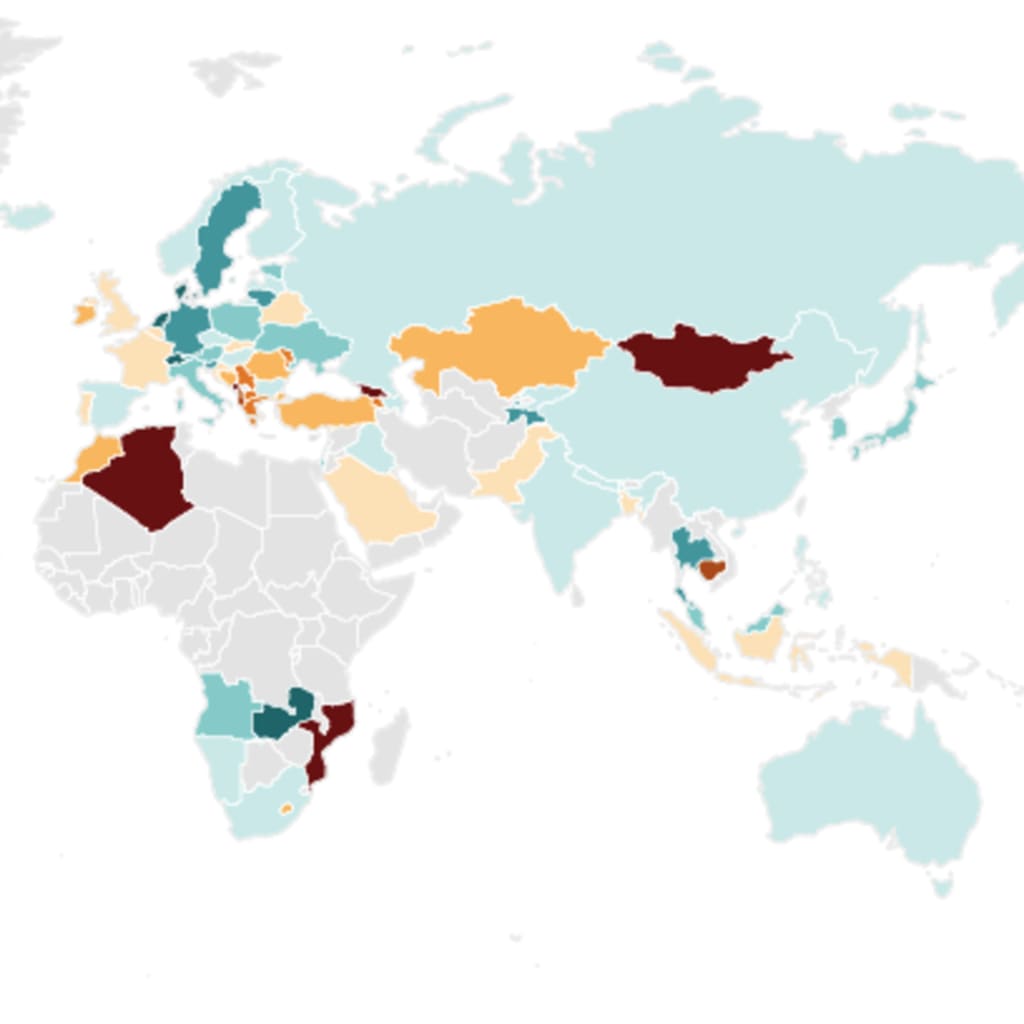

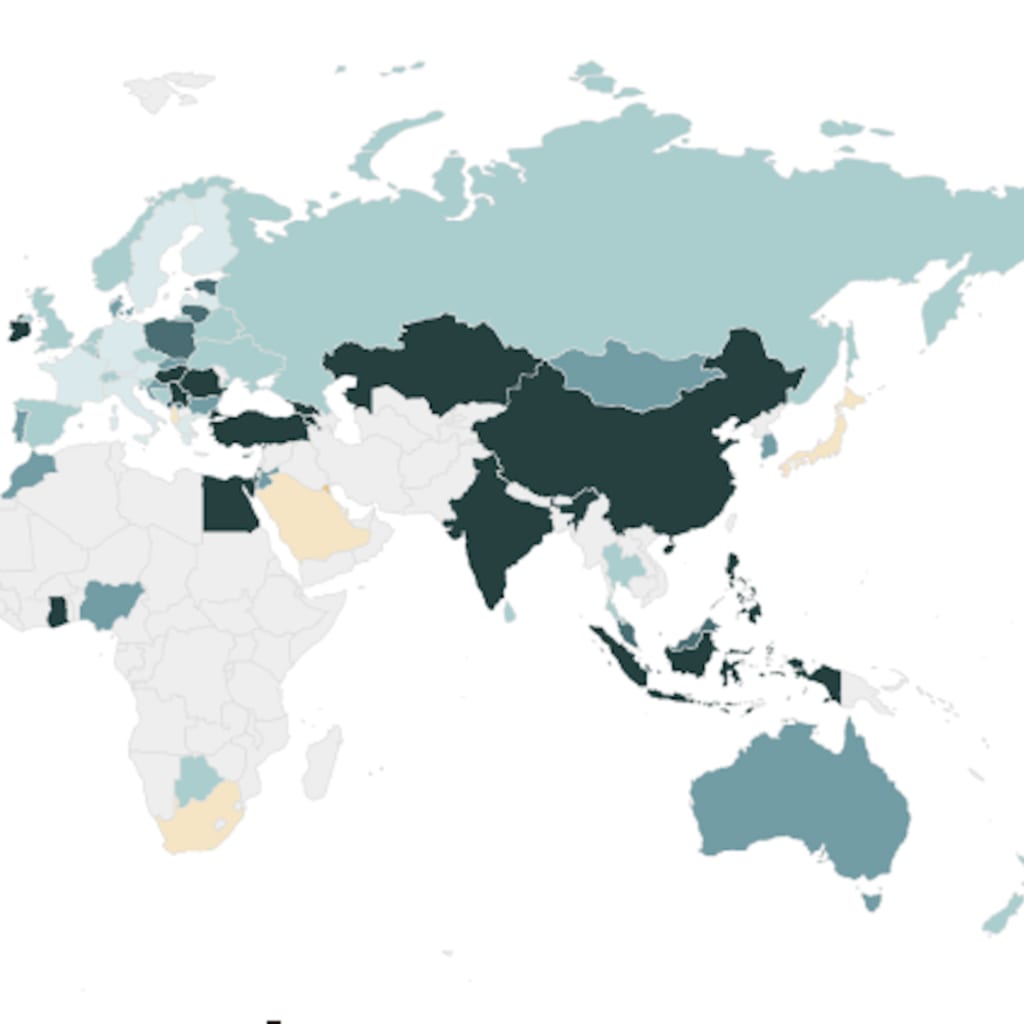

Global Energy Tracker

By Benn Steil and Yuma Schuster

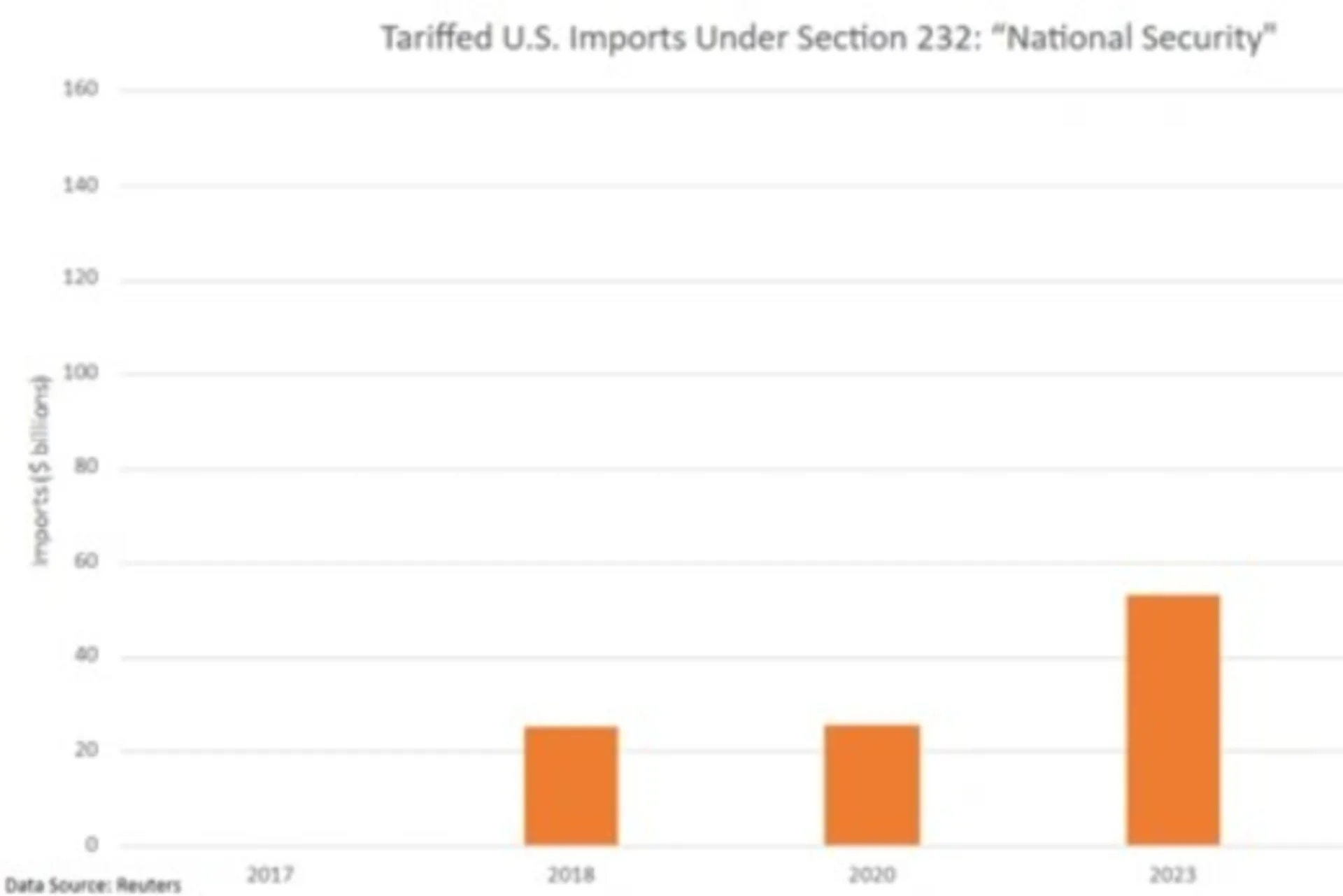

Global Trade Tracker

By Benn Steil and Yuma Schuster

Global Growth Tracker

By Benn Steil and Yuma Schuster

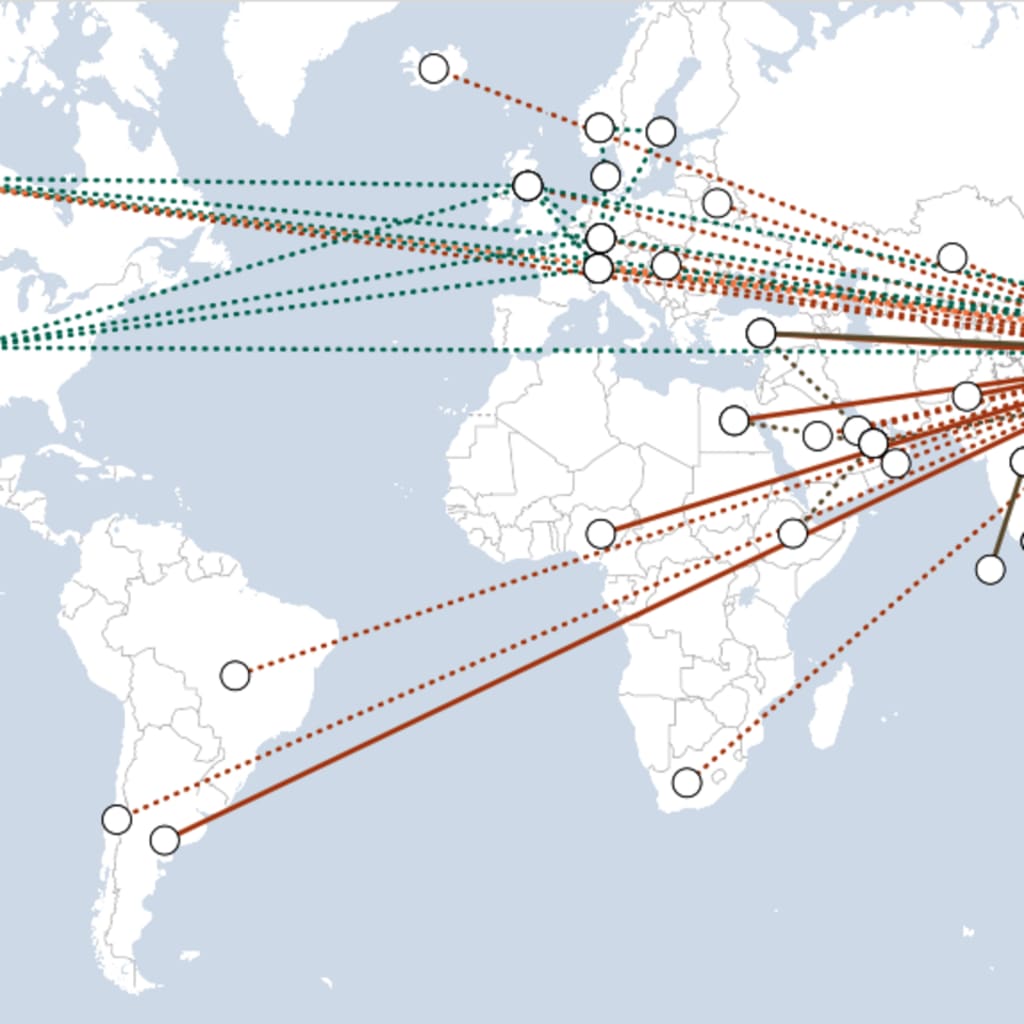

Central Bank Currency Swaps Tracker

By Benn Steil, Yuma Schuster and Samuel Zucker

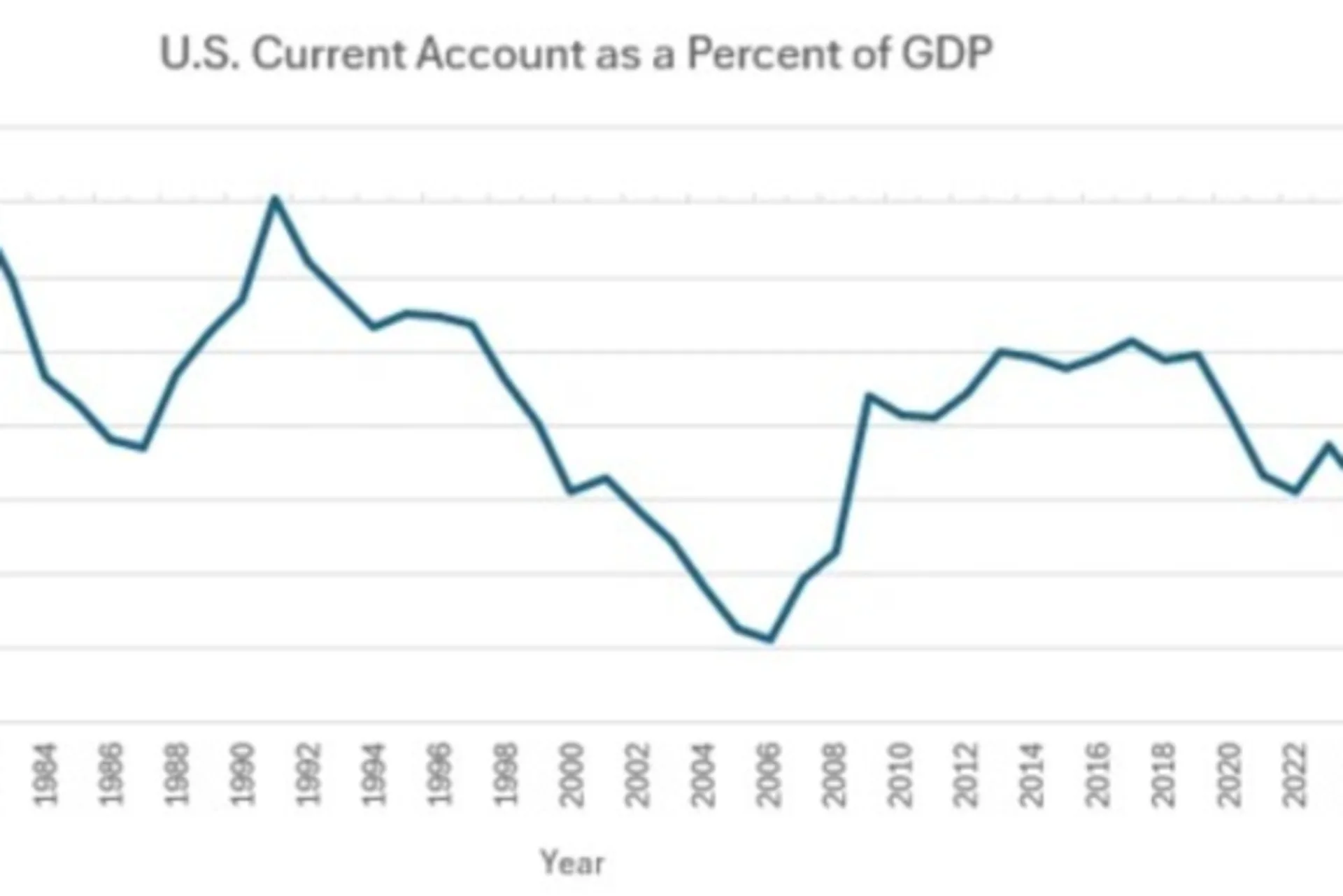

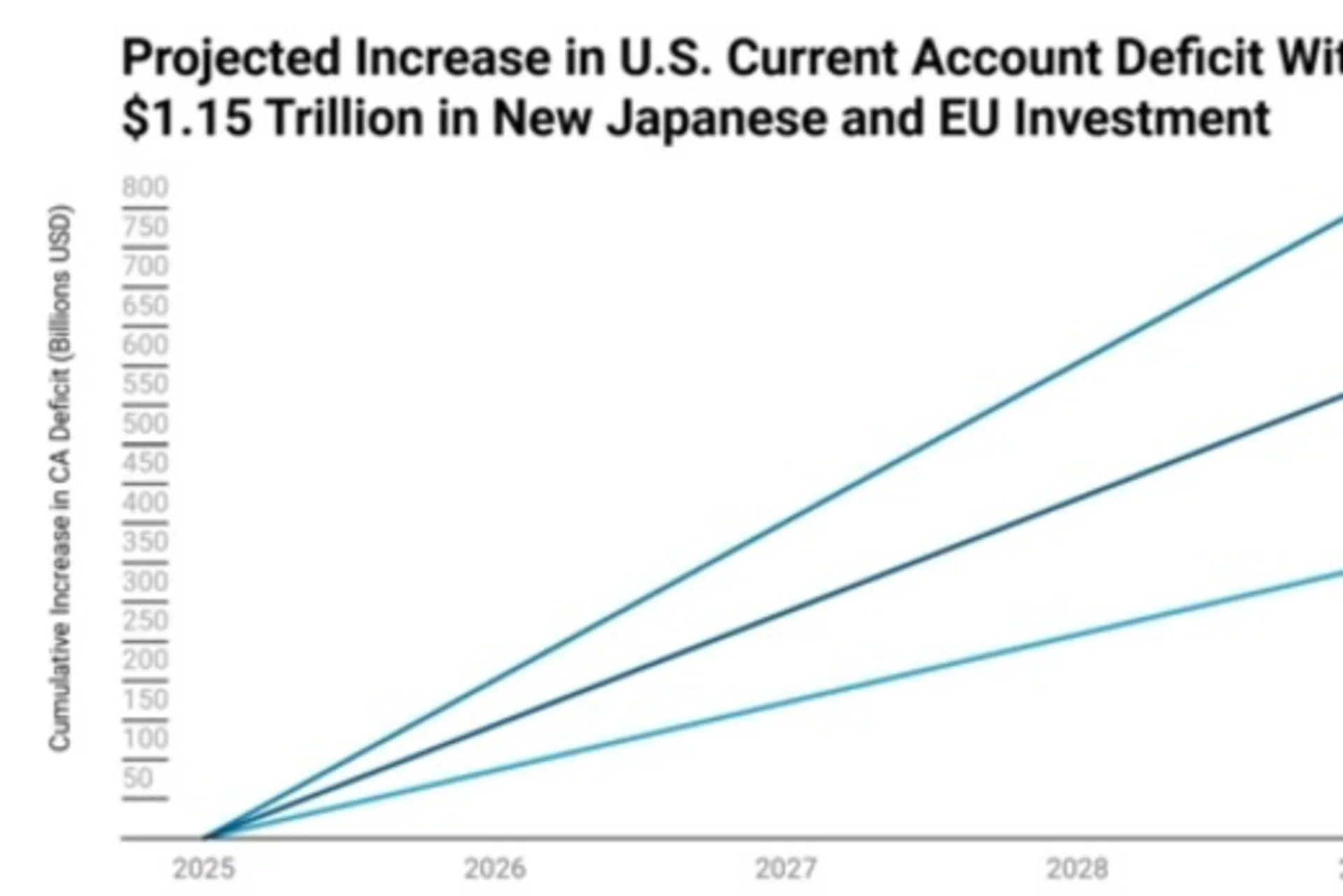

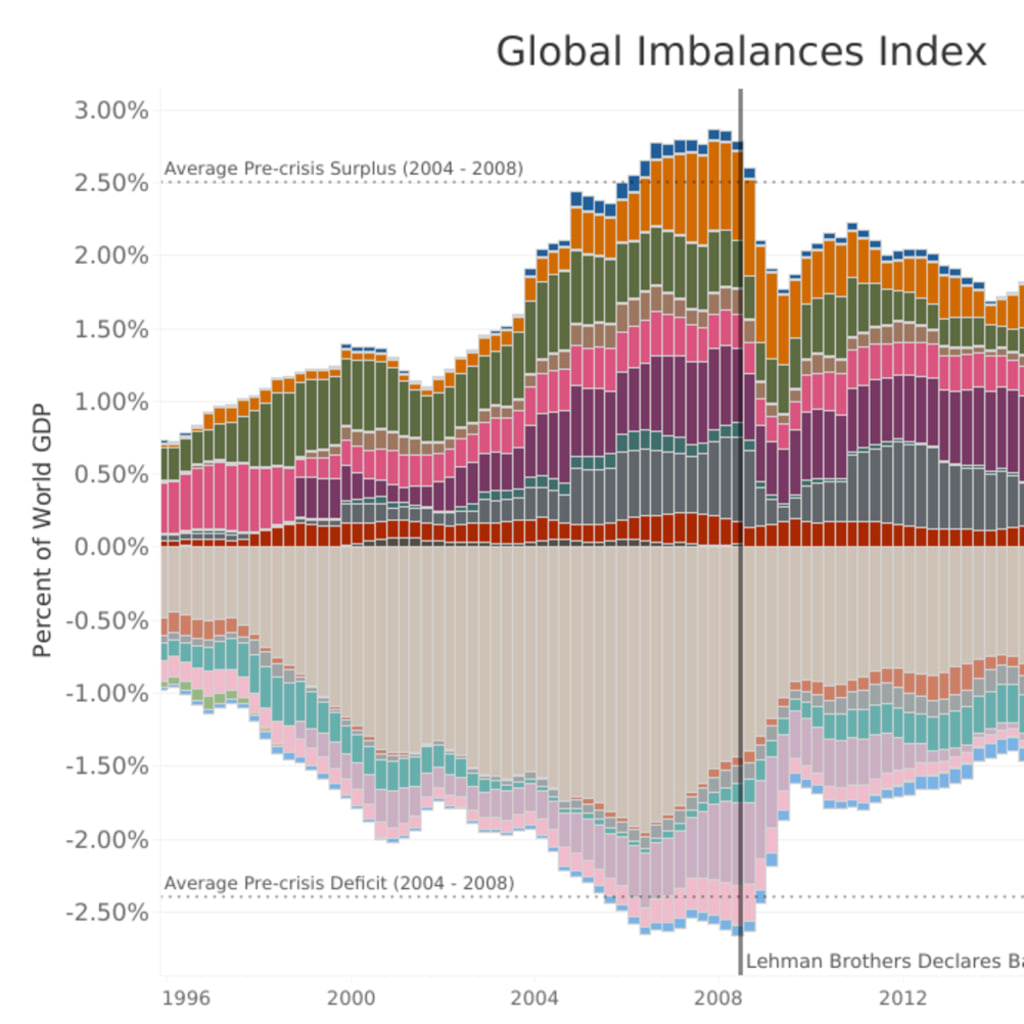

Global Imbalances Tracker

By Benn Steil and Yuma Schuster

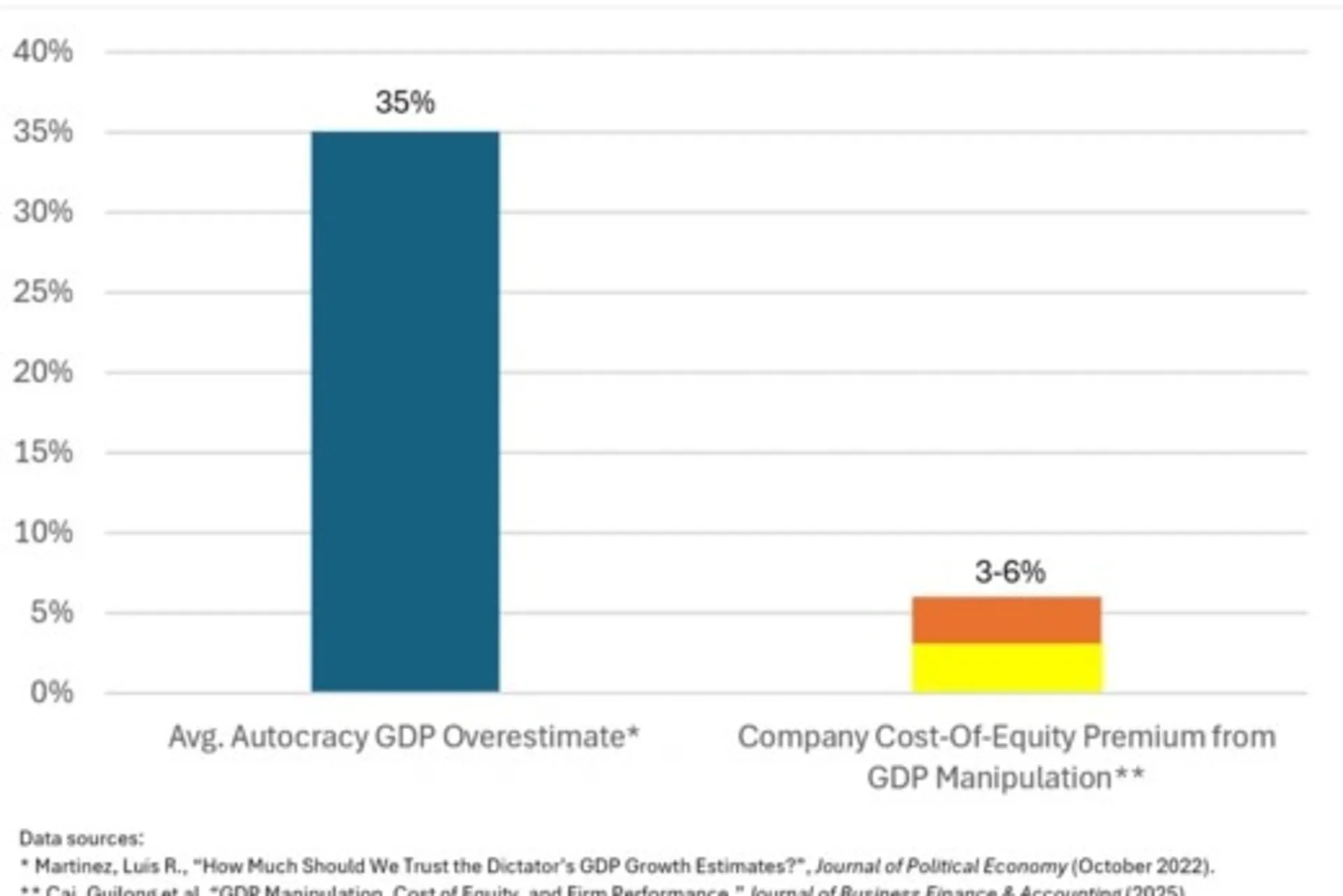

CFR Sovereign Risk Tracker

By Benn Steil and Yuma Schuster

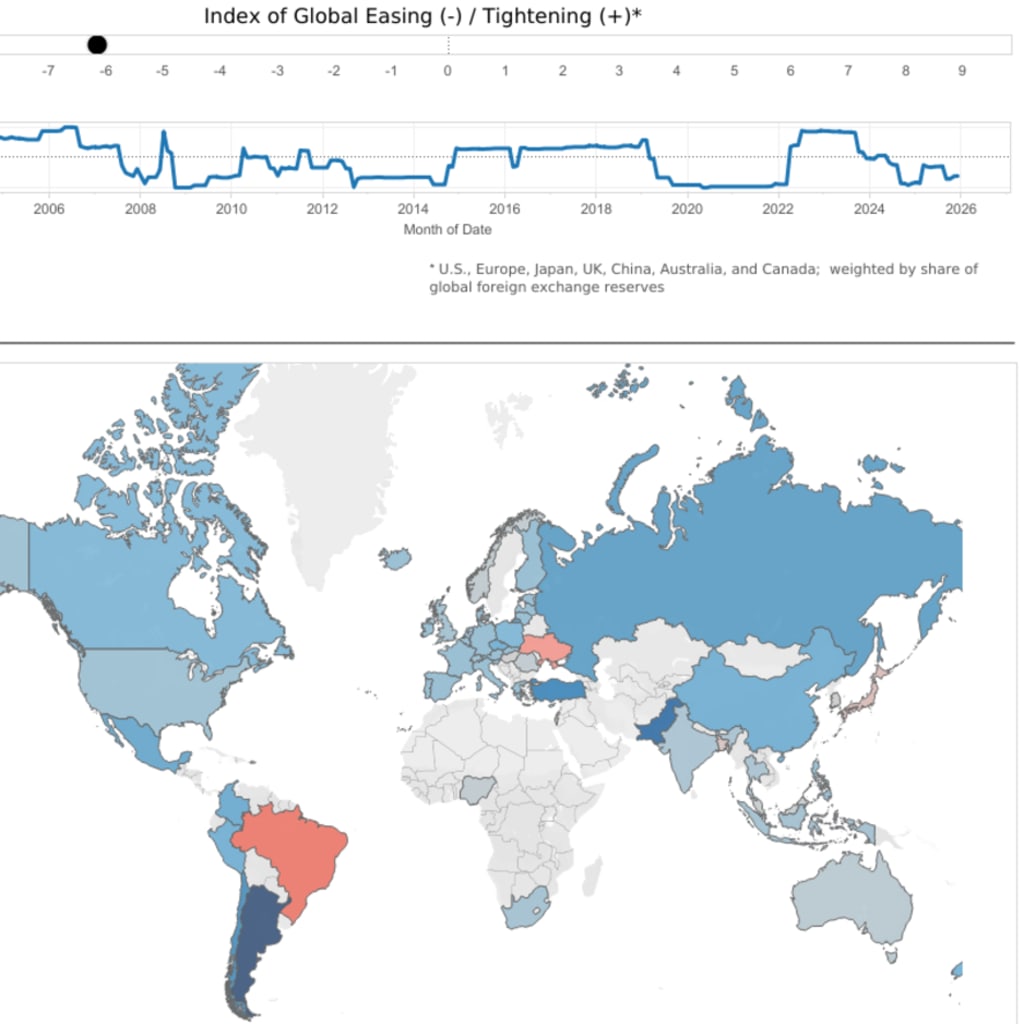

Global Monetary Policy Tracker

By Benn Steil and Yuma Schuster

Benn Steil is senior fellow and director of international economics at the Council on Foreign Relations in New York. He is the lead writer of the Council’s Geo-Graphics economics blog, and the creator of nine web-based interactives tracking Global Monetary Policy, Global Inflation, Global Imbalances, Global Growth, Global Trade, Global Energy, Sovereign Risk, China’s Belt and Road, and Central Bank Currency Swaps.

Benn Steil

Senior Fellow and Director of International Economics