The end of the United States exorbitant privilege?

There is a lot of angst right now about the dollar, and specifically about the dollar’s ability to remain the leading global reserve currency. Look at the FT leader at the end of 2007, or Daniel Gross in Newsweek’s end of the year spectacular.

Most of that angst is keyed off the (small) recent slides in the dollar’s share of global reserves. Never mind that the big slide in the dollar’s share of global reserves occurred in 2002 and 2003 - not now. And never mind that the world’s central banks have never held more dollars than they do now.

Indeed, the only thing growing faster than angst about the dollar’s status as a reserve currency is central bank holdings of dollars.

The press (even the Financial Times) as well as some currency analysts tends to report the (easily calculated) changes in dollar share of total reserves rather than changes in actual dollar and euro holdings. Almost no one tries to report the (far harder to calculate) increase in dollar and euro holdings net of valuation changes.

Yet I would challenge anyone who has looked at the actual IMF data to argue that the defining feature of today’s global economy is anything other than the unprecedented pace of reserve growth in the emerging world - and the unprecedented accumulation of dollar reserves by emerging market central banks.

The big issue facing the world isn’t the end of the dollar as a reserve currency so much as the overuse of the dollar as a reserve currency - the resulting accumulation of dollar reserves by countries that really have no need for reserves of any kind.

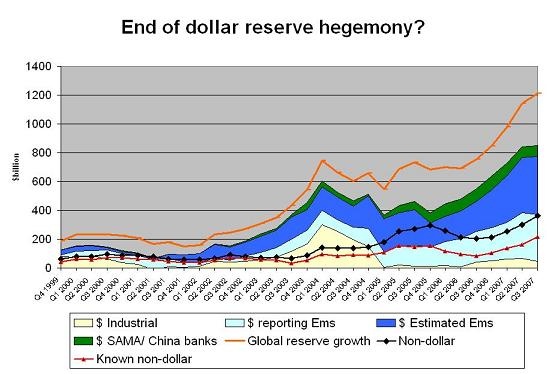

Take a look at a graph* showing the estimated increase -- on a rolling four quarter basis -- in dollar reserves relative to the over growth in the world’s reserves after adjusting for valuation changes.

There isn’t much evidence of a shortage of dollar asset accumulation. Central banks almost certainly added more dollars to their portfolio over the last four quarters than in other four quarter period.

* The preceding graph breaks out the dollar holdings of the industrial countries (mostly Japan), dollar holdings of reporting emerging economies (a group that likely includes Russia, Brazil and India), estimated dollar holdings on non-reporting emerging economies (a group that certainly includes China and likely also includes Taiwan and the Gulf economies) and estimated dollar holdings of Chinese banks and the Saudi Monetary Agency. The underlying data generally comes from the IMF, supplemented by the data SAMA releases on the size of its non-reserve assets and the PBoC’s data on the foreign currency balance of China’s banks (I’ll discuss this data in more detail in a subsequent post).

Yes, a lot of dollar and euro purchases come from countries that don’t report detailed data about their reserves to the IMF - so there is a reasonable margin of error. But the countries that do not report - China, some Gulf central banks - tend to manage their currencies against the dollar, and almost certainly still have most of their reserves in dollars. And if you prefer hard data to my estimates, just compare the red line --which shows non-dollar reserve growth of countries that report detailed data to the IMF relative to the dollar reserve growth from reported industrial economies and reporting emerging economies (the sum of the tan and light blue shaded area).

And yes, estimated central bank purchases of euro and pounds (look at the black line; it is dominated by euro and pound purchases) are certainly rising. Central banks are certainly buying more euros and pounds now than back in late 2003/ early 2004 for example. Even so, estimated 2007 euro and pound purchases are only about ½ estimated dollar purchases. They were nearly equal to dollar purchases in 2001 and, for that matter, in much of 2005.

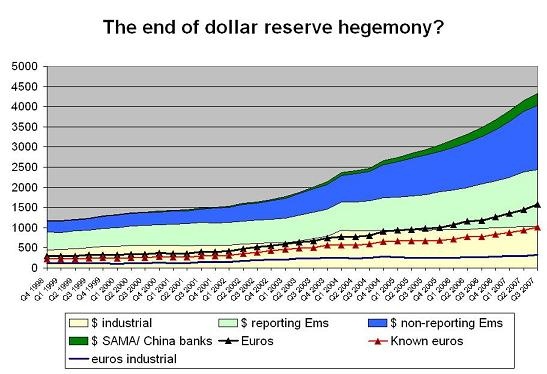

What of total dollar holdings? They - not surprisingly - still quite large, both absolutely and relative to the world’s euro holdings. Best I can tell, the world still holds nearly 3 times as many dollars as euros as reserves.

The dollar isn’t disappearing as a reserve currency. Sure, the world’s holdings of euros are rising rapidly (especially if they are reported in dollars ... ) but so are the world’s holdings of dollars.

The really big change is that close to half ½ of all dollar holdings (and about 1/3 of all euro holdings) are now coming from countries that do not report detailed data to the IMF.

So why the angst?

Well, the euro is a viable alternative to the dollar in some deep sense.

The euro already has effectively displaced the dollar as the key reserve currency of Europe. Eastern European countries, the Nordic countries and Switzerland hold most of their reserves in euros. Russia is moving that way as well. The central banks of countries that are members of the euro increasingly (I suspect) hedge their dollar holdings. And Europe is enjoying a fair amount of exorbitant privilege of its own. The rise in emerging market holdings of euro reserves is now financing European direct investment in the emerging world -- much as the growth in European and Japanese dollar reserves in the 1960s financed US direct investment in Europe and Japan.

But so far the euro is basically a regional reserve currency - not a global reserve currency. The oil exporters in the gulf and the manufacturing powerhouses of Asia still manage their currencies primarily against the dollar, not against the euro. As a result they likely still add far more dollars than euros to their portfolio.

The economic logic of such an arrangement though is eroding in a less Amero-centric world economy, creating an underlying sense that the dollar’s global role is at greater risk.

The Gulf increasingly exports its oil to Asia rather than the US. It certainly buys its imports from Asia and Europe rather than the US. The East Asian manufacturing powerhouses also now increasingly trade with Europe and the commodity exporters rather than the US. Financial flows no longer map all that well to real trade flows. There is a quite plausible case that the world is now overweight dollars - both relative to the euro, and relative to Asian or oil currencies. Indeed, the real asymmetry in today’s global monetary architecture is the absence of any Asian reserve currency.

Finally,

There also is -- perhaps -- a growing sense the enormous increase in central bank dollar holdings may reflect political decisions that make little economic or financial sense rather than the dollar’s intrinsic appeal as a financial asset. The dollar hasn’t held its value against the euro - or held its value relative to oil. And it isn’t likely to hold its value v. most emerging market currencies. The United States supposed comparative advantage at financial engineering isn’t worth as much now as it seemed to be worth a a year ago. Broker sam cannot sell his CDOs ... (more poetry here)

Finally, yhe fact that the US now depends so heavily on central bank financing also makes the US all the more sensitive to any change in the dollar’s status.

The US now relies on exorbitant privilege not so much to live well as to sustain the otherwise unsustainable - notably large private capital outflows from a country with a large current account deficit that isn’t attracting large private inflows. Without a lifeline from the world’s central banks, the US wouldn’t be able to finance its external deficit by selling under-performing financial assets. And if the US ever had to finance its deficit by selling financial assets that outperformed comparable assets, watch out. The US external position would deteriorate rapidly.

That leaves the United States in a position of intrinsic vulnerability.

The real risk though isn’t that the dollar will suddenly lose out to the euro. The real risk is that a bunch of already over-reserved emerging economies will conclude that it isn’t in their interest to hold even more dollars and euros - dollars and euros that they no longer really need - in their portfolio, and that this change will come before the US has weaned itself off its need for subsidized central bank financing.

The current wave of new sovereign wealth funds is effectively an implicit admission that most emerging economies are already over-reserved.

There is, though, another risk - namely that China and a host of others won’t change, the continued availability of such financing will allow the US to sustain large deficits without producing assets that private investors want to hold, and the overhang of unneeded and in some sense unwanted dollar reserves will grow. The result: the United States’ dependence on the political good will of its creditors will only deepen.

The United States’ heavy reliance on its “extraordinary privilege” to finance its deficit consequently is cause for concern - even if there isn’t yet any sign that the emerging world has started to withdraw the “extraordinary privilege” now granted to both the dollar and the euro.