No, Tax Breaks for U.S. Oil and Gas Companies Probably Don’t Materially Affect Climate Change

Last week, the journal Nature Energy published an article from scholars at the Stockholm Environment Institute arguing that the tax breaks given to oil companies by the U.S. government could lead to carbon emissions that eat up 1 percent of the world’s remaining “carbon budget.” (The carbon budget is scientists’ best guess of how much more carbon dioxide the world can emit while still having a chance of limiting global warming to 2°C.) This is an enormous figure—few other national policies reach that level of climate impact. So, if true, this analysis provides a powerful argument in favor of ending preferential tax treatment for U.S. oil and gas firms (see Vox’s piece for an accessible discussion).

But that conclusion flies in the face of the conclusion reached by a paper published here at the Council on Foreign Relations by energy economist Gilbert Metcalf. His paper concluded that tax breaks for oil companies modestly increase U.S. oil production, but, more importantly, global prices for and consumption of oil barely budge as a result, minimally affecting the climate. (The paper came to a similar conclusion about the climate impacts of tax breaks for U.S. natural gas production.) I was closely involved in the review and editing process for that paper, and I can attest that Professor Metcalf’s methodology was rigorously stress-tested.

So who’s right? In a nutshell, I stand by the CFR paper’s conclusion that federal tax breaks for oil and gas companies aren’t a major contributor to climate change. The biggest reason is that both the Nature Energy and CFR papers are in agreement that the tax breaks barely alter global oil prices, which implies insignificant changes in global consumption of, and emissions from, oil. In fact, the Nature Energy authors do not dispute this, and they only explicitly say that tax breaks cause emissions from burning U.S. oil to increase. But their omission that those tax breaks likely cause emissions from burning other countries’ oil to decrease can easily mislead a casual reader to assume that they mean global emissions will increase as much as emissions from burning U.S. oil will.

The two papers also have some other quantitative disagreements, and the Nature Energy paper might have more up-to-date industry data than the CFR paper. Nevertheless, I don’t think those other disagreements justify overturning the CFR paper’s overall conclusion about the limited climate effects of the tax breaks.

Finally, the two papers do agree on one thing: the tax breaks should go. The Nature Energy paper contends that ending the tax breaks would bring “substantial climate benefits.” Although the CFR paper concludes that emissions “would not change substantially,” the two papers agree that tax reform has symbolic value that would strengthen U.S. climate leadership; U.S. taxpayers would also benefit from a few billion dollars annually of recouped government revenue from oil companies.

Back to Basics

The two papers are in agreement that there are three major tax breaks that oil companies get from the federal government that promote more U.S. oil production. The first allows firms to immediately expense “intangible drilling costs” (IDCs), which account for the majority of drilling costs, rather than deducting them from their taxable income over several years. The second tax break, percentage depletion, allows some oil companies to deduct a fixed percentage of their taxable income as costs rather than deducting the value of their reserves as they are depleted. And the third tax break allows oil companies to write off a percentage of their income through the domestic manufacturing deduction. Together, these three tax breaks amount to around $4 billion in foregone government revenue annually. (The Nature Energy paper considers several other tax breaks but concludes that these three are the important ones.)

Both papers then set out to quantify how much more oil U.S. firms produce as a result of the tax breaks. In general, the two papers go about this in a similar way. The Nature Energy paper uses real industry data on U.S. shale oil fields to calculate which fields are profitable to produce oil from with the tax breaks but aren’t worth drilling without those breaks. And the CFR paper uses a new theoretical tool along with empirical statistics to find the percentage of wells that tax breaks make profitable to drill.

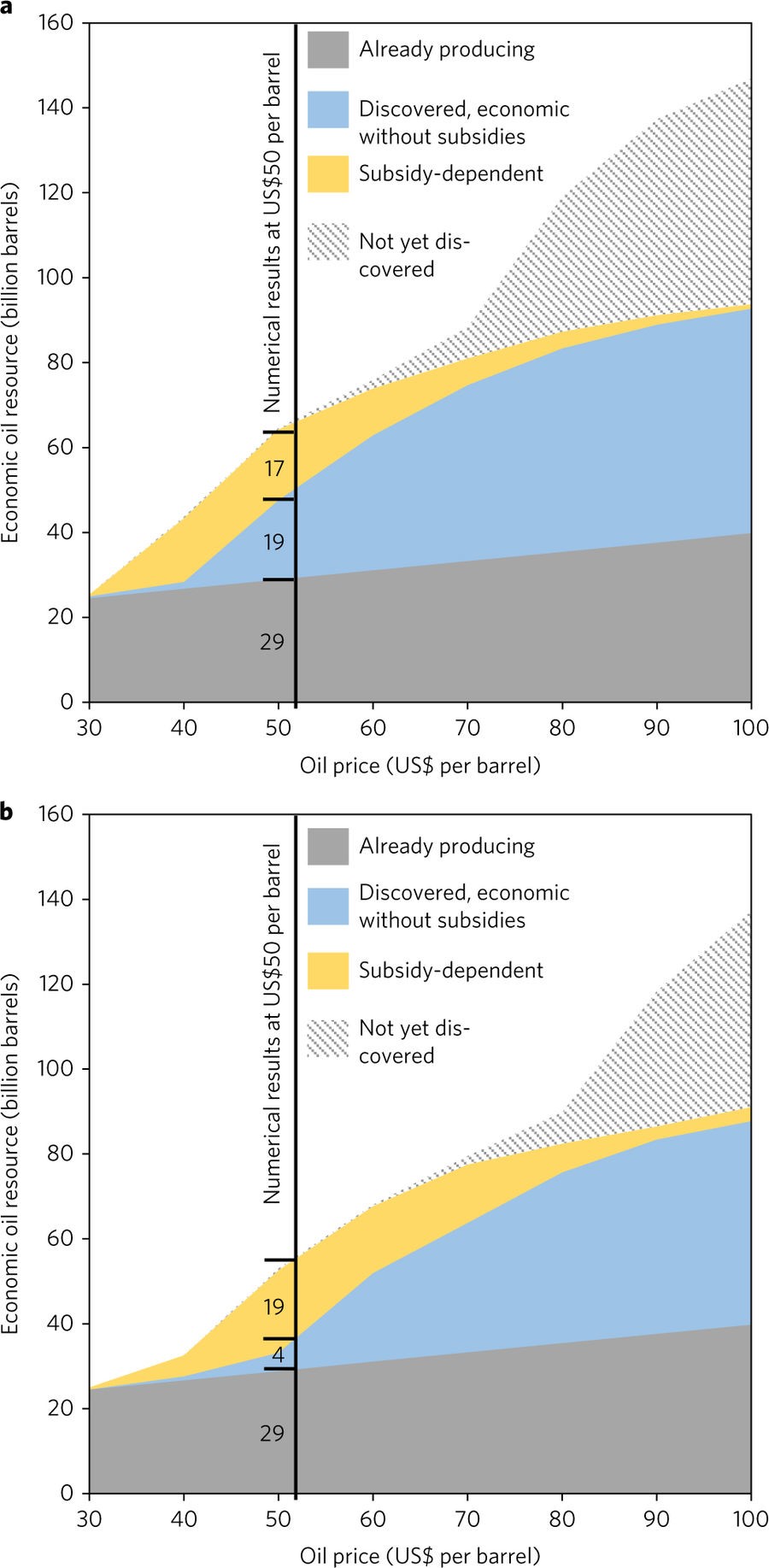

But the two papers differ in their bottom-line conclusions. The Nature Energy paper rings the alarm bells by concluding that the total amount of oil in the fields that tax breaks turn from unprofitable to profitable is between 13 and 37 percent of the total amount of profitable oil (depending on where oil prices are between $75 and $50 per barrel; higher prices mean that less oil becomes economic to produce as a result of tax breaks—see figure 1). As a result, the authors conclude, if all of the oil in the fields turned profitable by tax breaks were produced by 2050 (and burned), the world would emit 6–7 gigatons of carbon dioxide, roughly 1 percent of the remaining carbon budget.

Figure 1: Nature Energy paper summary figure: “The impact of subsidies is highly sensitive to oil price. These charts shows how much oil is economic at price levels between US$30 and US$100 per barrel according to whether it is already producing; discovered and economic without subsidies; discovered and economic only because of subsidies (‘subsidy-dependent’); or not yet discovered. a, Results at the base, 10% discount rate. b, Results at an alternative discount rate of 15%. The subsidy-dependence of the not-yet-discovered fields was not assessed, as these quantities are speculative, based on Rystad Energy’s assessment. Still, should they prove as subsidy-dependent as the fields we do assess, the impact of subsidies at higher prices would be larger than we currently estimate.”

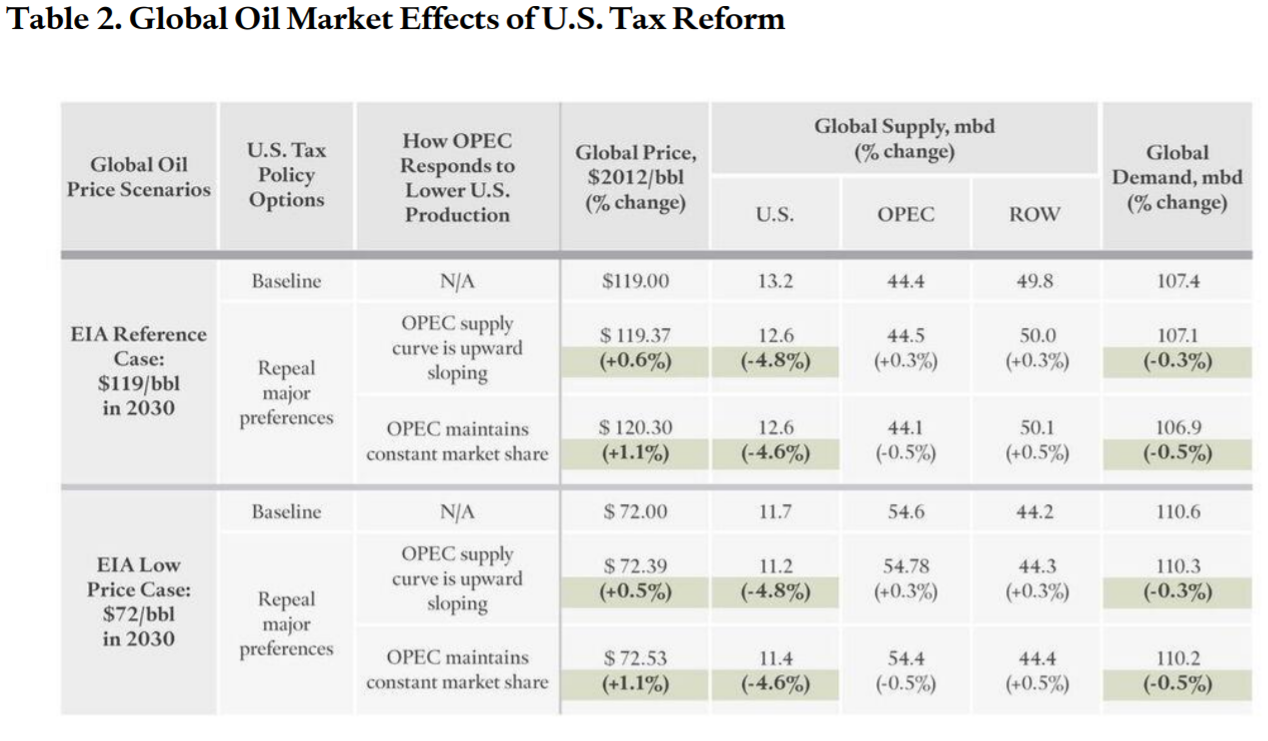

The CFR paper finds that 9 percent of the wells that oil companies drill each year are induced by tax breaks. But most of the additional oil that the U.S. produces will be offset by reduced production elsewhere in the world. After using a simple model of global oil supply and demand, the paper concludes that increased U.S. production translates only to at most a 1 percent decrease in global oil prices, and a measly half a percent increase in global consumption of oil (see table 2, which projects the oil market impacts of taking away tax breaks). Such a small uptick is washed out by the ordinary volatility of oil prices and resulting changes in consumption. So the CFR paper concludes that the nearly-undetectable change in global oil consumption means that the climate effects of U.S. tax breaks are negligible.

Table 2: CFR paper summary table: “Table 2 presents the modeled equilibrium values of global oil price, supply, and demand in 2030. The first column lays out four ways that the global market could develop: two future oil price possibilities considered by the Energy Information Agency (EIA), and within each of those cases, the two scenarios for OPEC to be price-responsive or exhibit cartel behavior to maintain its market share. Within each of these four alternatives for how global markets might behave, the second column presents two options for domestic policy: the United States can maintain existing tax preferences (baseline), or it can repeal the three major preferences. The tax reform is assumed to shift the domestic oil supply curve by 5 percent. The remaining columns in table 2 report the equilibrium Brent oil price—the benchmark for most of the world’s oil—in 2012 dollars; supply, in million barrels of oil per day (mbd) from the United States, OPEC, and the rest of the world (ROW); and global demand.

Table 2 shows that the long-run effects of U.S. tax reform are minimal under a wide range of input assumptions for how the future oil market behaves. The highlighted figures demonstrate that global prices and demand change by up to 1 percent, and U.S. production changes by less than 5 percent, regardless of the assumptions of future oil prices and how OPEC will respond. Although these changes are greater than those projected by previous studies, they are still small. An oil price increase of up to 1 percent would be over three hundred times smaller than price spikes in the 1970s and ten times smaller than the average annual increase in oil prices from 2009 to 2014. It would raise domestic gasoline prices by at most two pennies per gallon at the pump.“