A Puzzle in Japan’s Balance of Payments: What Explains Strong Foreign Demand for JGBs?

Japanese investors have an obvious incentive to search for yield abroad. But why has foreign demand for Japanese bonds almost matched Japanese demand for foreign bonds?

Japanese investors have been big buyers of foreign bonds—and U.S. bonds in particular. The lifers, the Japanese government through the government pension fund (GPIF), the Japanese government through Post Bank (which takes in deposits and cannot make loans so it buys foreign bonds since it cannot make money buying JGBs), and Norinchukin.*

But—and this is the surprising thing—foreigners have also been big buyers of Japanese bonds. Since 2010, foreign holdings of Japanese debt have been rising alongside Japanese holdings of foreign debt, which puzzled me for a long time.

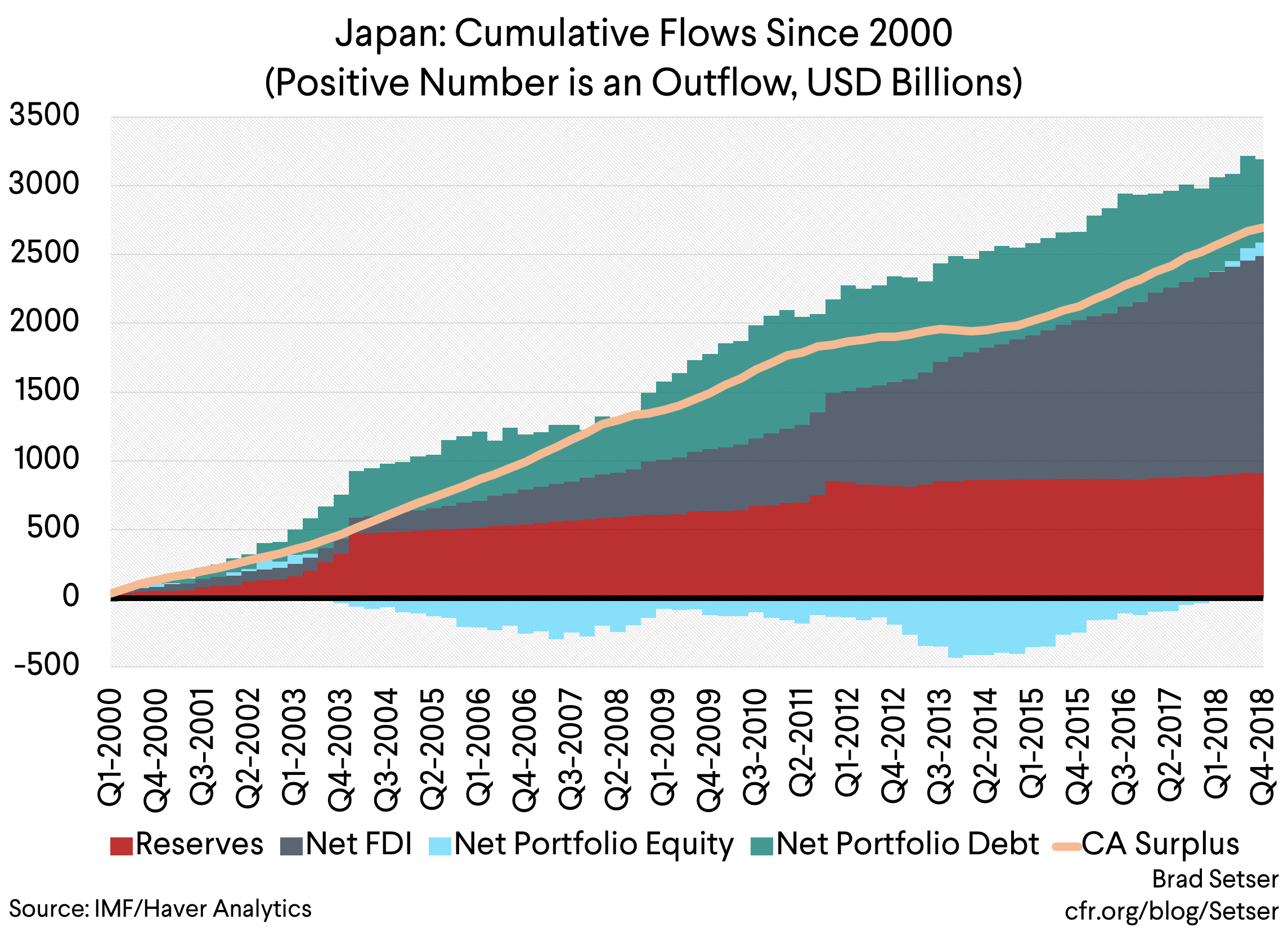

The net outflow out of Japan over the last fifteen years has primarily come from the growth in (unhedged) reserves and foreign direct investment—net private portfolio outflows (e.g. bond and equity outflows, net of bond and equity inflows) have actually been modest. That at least is what I take from a chart summing up quarterly flows in the balance of payments over the last twenty years.

But in this case looking at the net flows misses the story, as the limited net outflow through is the result of large gross flows in both directions.

Think about the large inflow into Japanese government bonds (JGBs) for a minute. JGBs more or less yield zero. Unless foreign investors are making a massive unhedged bet on yen appreciation, this kind of inflow into safe Japanese bonds doesn’t make sense.

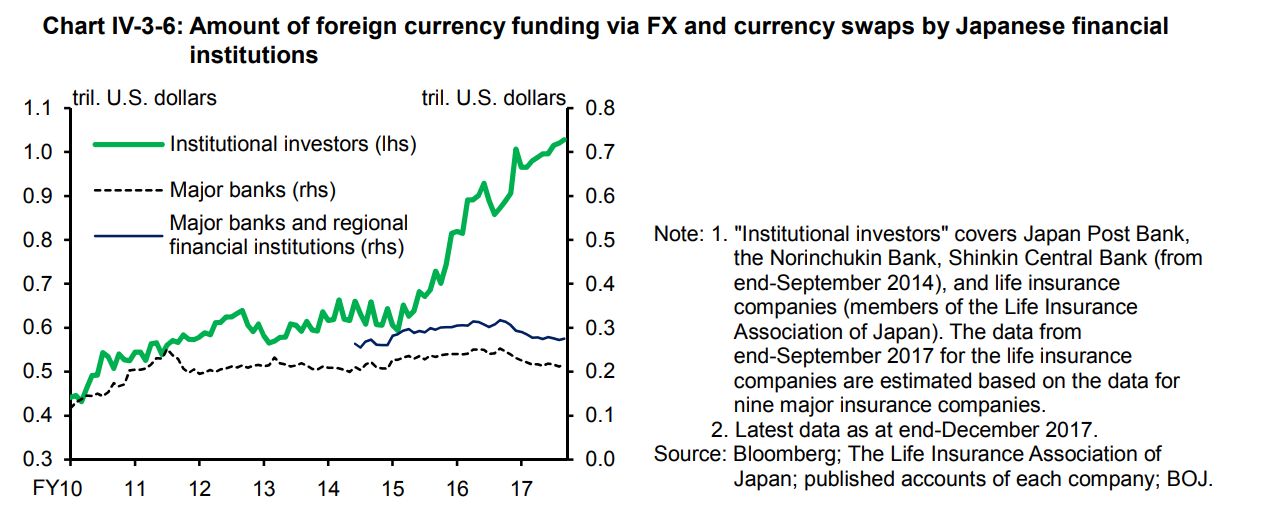

But there clearly is more going on. The big inflows into JGBs are a consequence, in all probability, of the fact that the bulk of Japan’s bond investment abroad has been hedged, often through the cross currency swaps market. See Chart IV-3-6 in Japan’s April 2018 Financial System Report, which shows that “institutional investors”—a category that includes Post Bank and Norinchukin as well as the lifers, had around a trillion dollars in FX and currency swaps in 2017).**

With a cross currency swap, Japanese investors get dollars that they can then invest abroad. And foreign investors—if they are the suppliers of dollars—get yen. Those yen are then invested into the local bond market. That’s why there has been a large inflow into the Japanese government bond market over the last five years even though JGBs yield zero. The suppliers of dollars are capturing the premium that Japanese financial institutions are willing to pay for dollars—not the yield (ha!) on offer in the JGB market (for more on cross currency funding markets, see Chapter 5 of the IMF’s Global Financial Stability Report).

In broad terms, a number of Japanese financial institutions have become, in part, dollar based intermediaries. They borrow dollars from U.S. money market funds, U.S. banks, and increasingly the world’s large reserve managers (all of whom want to hold short-term dollar claims for liquidity reasons) and invest in longer dated U.S. bonds. They are taking the risk that U.S. short-term rates will rise before their bonds mature (as they typically hedge with short-term contracts), and of course any credit risk associated with their portfolio. There is a chain of risk intermediation here, sort of like that employed by the European banks pre-crisis. (big hat tip to Brender and Pisani here). That’s how Japanese lifers, for example, seek to close the gap between the returns they have promised the buyers of their policies and the return available in the Japanese government bond market (see Figure 3.1 in the October Global Financial Stability Report).

And foreign investors who are on the other side of the cross-currency swap market are in effect substituting Japanese short-term bills (or near dated JGBs) for U.S. Treasury bills or similar instruments. They hold yen-denominated debt because of the premium they get lending dollars to Japanese institutions, not because yen interest rates are attractive. The roughly 1.5 trillion dollars now parked—according to the balance of payments—in Japanese government bonds yielding next to nothing (and heavily in fairly short-term Japanese bills with negative yields) thus should be viewed as an indirect measure of Japan’s demand for higher yielding European and U.S. assets.

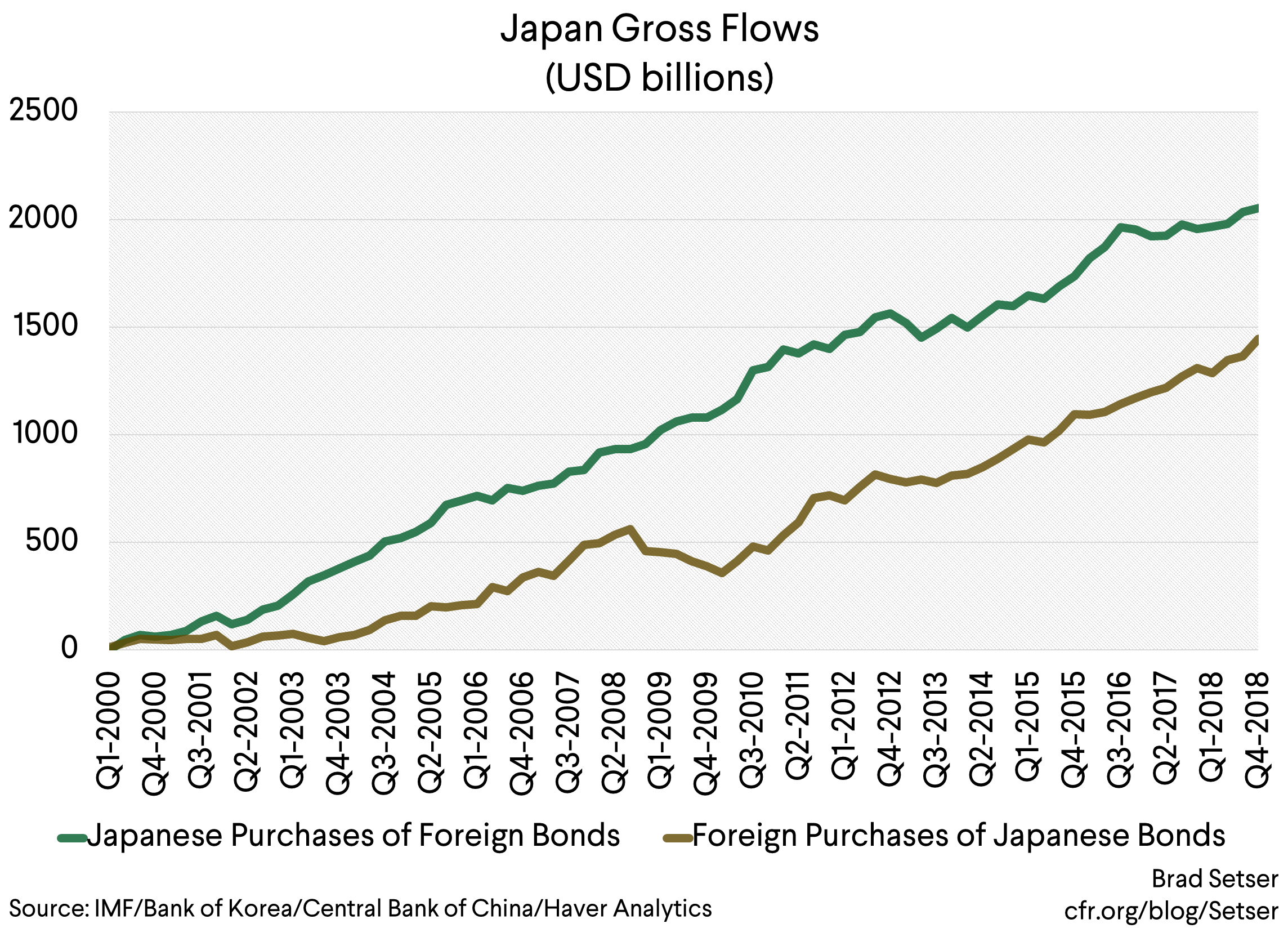

What’s interesting is that this two-way flow has become fairly big. In the last decade, foreign investors have put about a trillion into Japanese government bonds, and Japanese investors have put a roughly similar sum into foreign bonds. And, as Hyun Shin has emphasized, symmetric flows that create large gross positions can give rise to large risks even if the “net” position is balanced.

That’s the issue here. Japanese banks and insurers have effectively become big enough swap-funded dollar financial intermediaries that they could have a systemic impact on U.S. markets. Or at least an impact on some important corners of the market. Yet they are regulated by Japan’s regulators, who might not be quite as focused on how their institutions impact the broader U.S. market as U.S. regulators could be. Sort of like Europe’s banks were big players in the chain of risk intermediation that supported the U.S. private label asset backed securities market before the U.S. financial crisis while being regulated (or not regulated) in Europe.

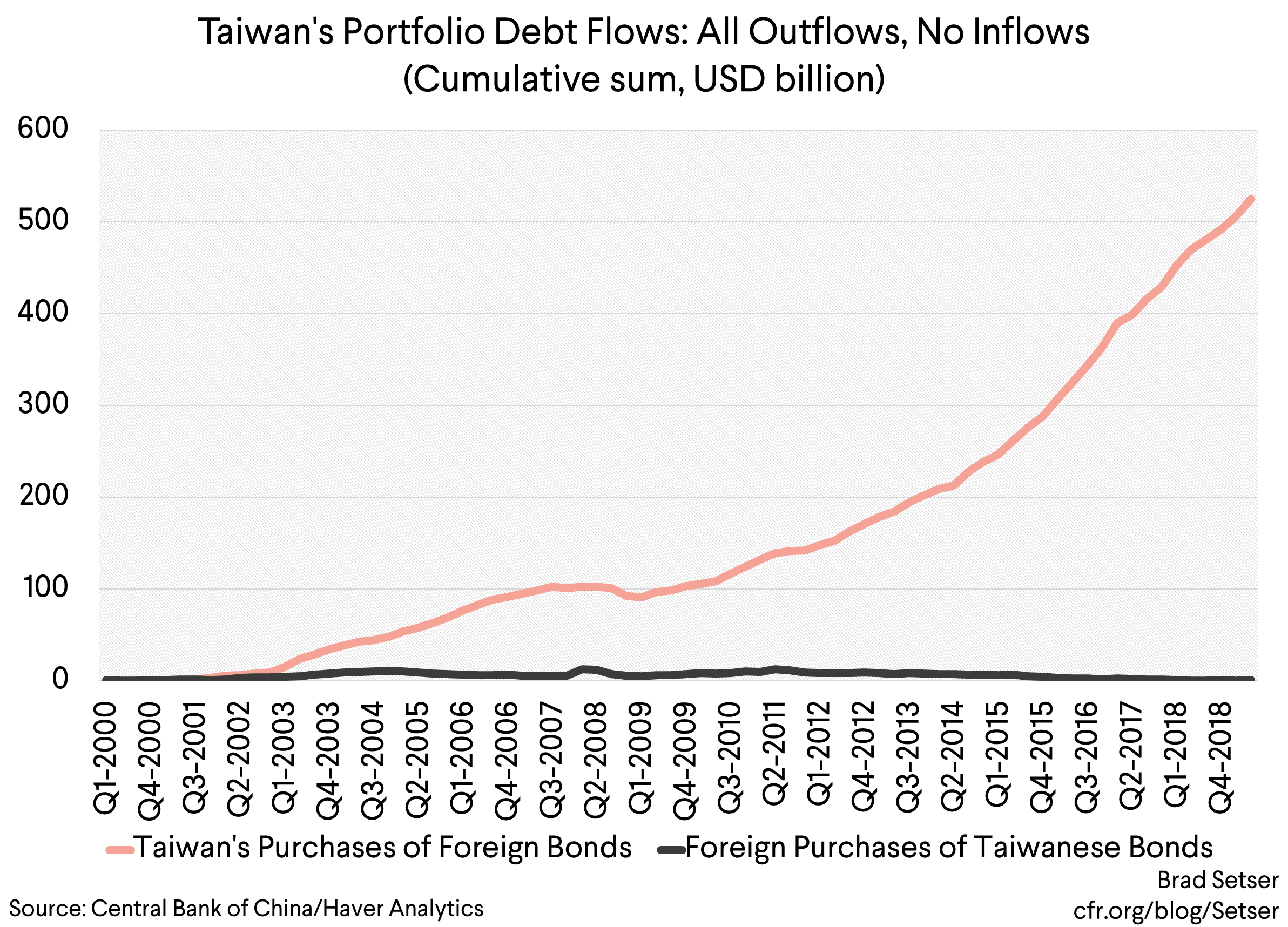

Taiwan, incidentally, is a bit different. While the bond outflow isn’t the main counterpart to Japan’s current account surplus (net portfolio flows including equities are very balanced over time), the bond outflow from Taiwan has more been the main offset in the financial account to Taiwan’s balance of payments surplus. There isn’t a comparable inflow in Taiwan’s government bond market. The gross outflow into foreign bonds is also the net flow.

That’s important. It implies that the counter-parties to the hedging need of Taiwan’s life insurers are mostly local actors, whether domestic banks or Taiwan’s central bank.

* Norinchukin is the Japanese farmers and fishers cooperative, which has become a big investor in CLOs. Technically, Norinchukin doesn’t buy U.S. bonds—or directly make leveraged loans to American firms. Rather it buys claims on financial vehicles based in the Caymans, which in turn provide the leveraged loans to U.S. firms. Those structures have raised gross cross-border claims on the United States without generating large net inflows, as the Federal Reserve international staff explained in a recent note. Norinchukin seems to be the main foreign buyer of these structures; most CLOs are held by U.S. investors. Mechanically that means U.S. holdings of “foreign bonds” are rising (e.g. bonds issued by entities in the Caymans) while U.S. firms are increasingly borrowing from abroad (e.g. the financial entities set up in the Caymans to make leveraged loans). Remember that the bulk of U.S. holdings of foreign bonds these days are claims on various entities in the Caribbean…

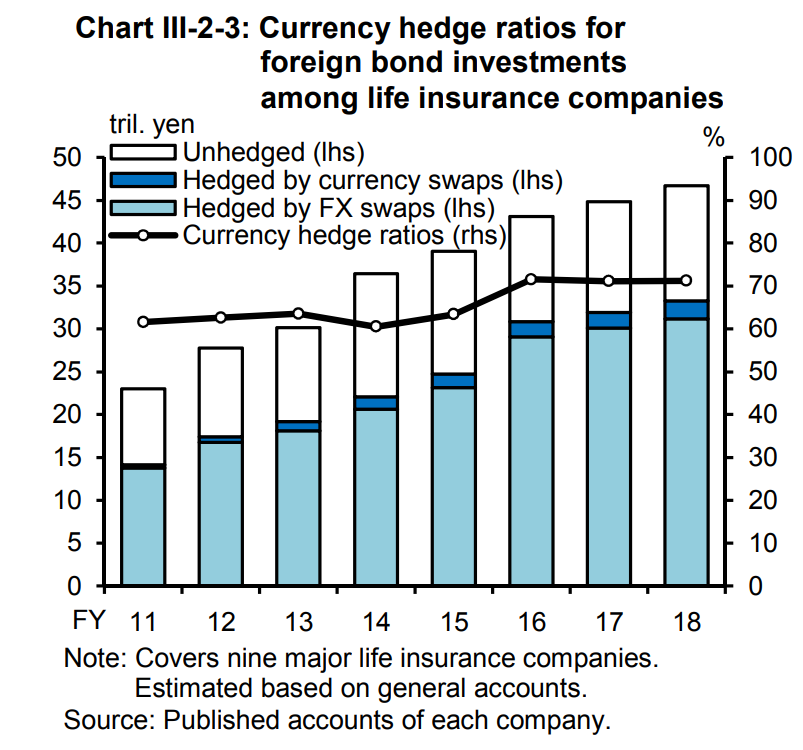

** For those curious, the latest Financial System Report from the Bank of Japan (table III-2-3) shows the top nine Japanese life insurers had around $300 billion in currency hedged foreign bonds at the end of 2018, and they hedged about 70 percent of their FX risk. These totals have evolved since: Japan’s life insurance sector now has almost $900 billion in foreign securities, counting foreign equities as well as foreign bonds (data here)