Could Taiwan’s Commercial Banks Cover the Lifers‘ Hedging Need? (Part 4)

Who is on the other side of the massive ($250 billion) hedging need of Taiwan’s life insurance industry? The local banking system covers at most a quarter of the life insurers hedging need, and foreigner investors provide less than that…

By experts and staff

- Published

Brad W. SetserCFR ExpertWhitney Shepardson Senior Fellow

Brad W. SetserCFR ExpertWhitney Shepardson Senior Fellow- Guest Blogger for Brad Setser

This is the fourth post in a series* on Taiwan’s life insurers and their private & sovereign FX hedging counterparties. It’s the product of a collaboration with S.T.W**, a market participant and friend of the blog. Printable versions of entries in this series will be available in pdf format on his site (Concentrated Ambiguity).

Part Four: Searching for Counterparties: Foreigners, Banks & Corporates

The search for the counterparties to lifers’ FX hedges is a daunting endeavor. Since there exists no central, publicly available dataset detailing exposures across all relevant actors, a multitude of adjacent sources have to be combined to create an understanding of the underlying activity. Three factors help in this regard:

- First and foremost, the sheer size of lifers’ FX hedges (USD 250bn) virtually guarantees that other firms & sectors will be impacted by either supplying or facilitating their hedging demands.

- The life insurance sector is undoubtedly the largest buyer of FX hedges, thus the task is more or less limited to figuring out the supply side of the hedging transactions.

- Since FX hedging is done via OTC markets, firms or sectors without access to it can quite quickly be eliminated from the discussion.

A. Three Types of Counterparties

The institutions that could take the other side of lifers’ FX hedges can roughly be subdivided into three groups:

- Institutions, which coincidentally have an opposing on balance sheet FX exposure as lifers and thus equally require an FX hedge to reduce risks. One example would be corporates, with debt issued at beneficial rates in foreign currencies, ’domesticizing’ such issuance via FX derivatives. Another would be banks with large domestic FX deposits, but little business abroad who decide to lend in local currency and balance their currency exposure via derivatives.

- Institutions, which initially have no unbalanced FX exposure, but will facilitate lifer demands for a fee (i.e. a negative cross-currency basis). To do so, they will deliberately mismatch their on-balance-sheet exposures, but will (including the derivative transaction with the insurer) remain overall FX neutral. Domestic and foreign banks, as well as versatile overseas investors (with flexibility in their cash management) arbitraging negative bases is the typical case.

- Institutions, which wish to purposefully acquire a long USD, short TWD exposure. The demand can be of speculative nature or by an official institution stabilizing or intervening in the FX market.

An economy is oftentimes partitioned into the following sectors: the central government, the monetary authority, the banking sector, non-financial corporations, the rest of the world, households and other financial institutions. Of these, three sectors can be excluded with a relatively small effort. Central governments typically only enter the FX arena when they have issued debt in foreign currencies—which Taiwan has not—and otherwise leave FX issues to the central bank. Households do, in all but exceptional circumstances, not have direct access to OTC markets, which requires an ISDA (or ISDA-like) agreement and are the domain of larger institutions. Even if parts of the personal wealth management business (family offices etc. of locals) is included within the household sector, their size should be immaterial to the discussion at hand. Taiwan has a range of other financial institutions apart from life insurance companies including Credit Cooperative Associations, Credit Departments of Farmers’ and Fishermen’s Associations, Chunghwa Post Co., Money Market Mutual Funds and Trust and Investment Companies. All of these are domestically focused institutions, with no or minimal foreign business, all of which have not grown by much during the past decade. They are thus not natural counterparties to the lifers’ hedging needs.

This leaves the rest of the world, the banking sector, nonfinancial corporations and the monetary authority.

B. The Foreign Sector

Foreign institutions occupy a special place in the provision of FX hedges, as they are the only sector able to supply quasi unlimited amounts to counterparties. This is due to their ability to secure cheap funding in their base currency, in this case USD. In Japan and the Euro Area, both like Taiwan large purchasers of overseas FX-hedged debt, foreigners are the prime supplier of FX hedges. But Taiwan emerges as a somewhat different beast.

Of the three types of counterparties described in the first section of this chapter, the second category—the arbitrageurs—are the most potent overseas force able to provide lifers the required FX hedges. [1]

If a Taiwanese lifer enters into an FX swap to acquire USD denominated debt, this can work as follows: An institution with ample USD funding (for instance a U.S. bank) recognizes a large negative cross-currency basis in Taiwan’s FX market, enabling it to profit by lending USD via FX swaps. So at initiation, the U.S. bank exchanges[2] USD for TWD with the life insurer.[3] Now, with TWD deposits on its balance sheet, the U.S. bank attempts to allocate these funds to the safest TWD-denominated asset available—after all, its profit arises from the peculiarities of pricing in FX markets and not from excessive risk taking in Taiwan.[4] Preferred safe assets include government bonds & bills, repurchase agreements secured by the former or deposits directly with the central bank.

The reason for spelling out the sequence of actions the U.S. bank takes is that while the FX swap transaction is more or less invisible (since it’s an OTC transaction), the bank’s subsequent transactions in search for safe assets in TWD markets is not. It can be followed with some precision in Balance of Payments statistics—in theory not only in Taiwan’s, but also in the corresponding entries in counterparty host nations.

In Japan’s case for instance, where similar to Taiwan, life insurers, Japan Post Bank and Norinchukin Bank have acquired very large amounts of FX-hedged[5] U.S. debt in recent years, the collateral reinvestment of arbitrageurs is clearly visible in the BoP as foreign demand for JGB bills & bonds, JPY-repos and deposits held directly with the Bank of Japan. All these dynamics are common market knowledge and anecdotal evidence for these activities is ubiquitous when institutions involved are consulted.

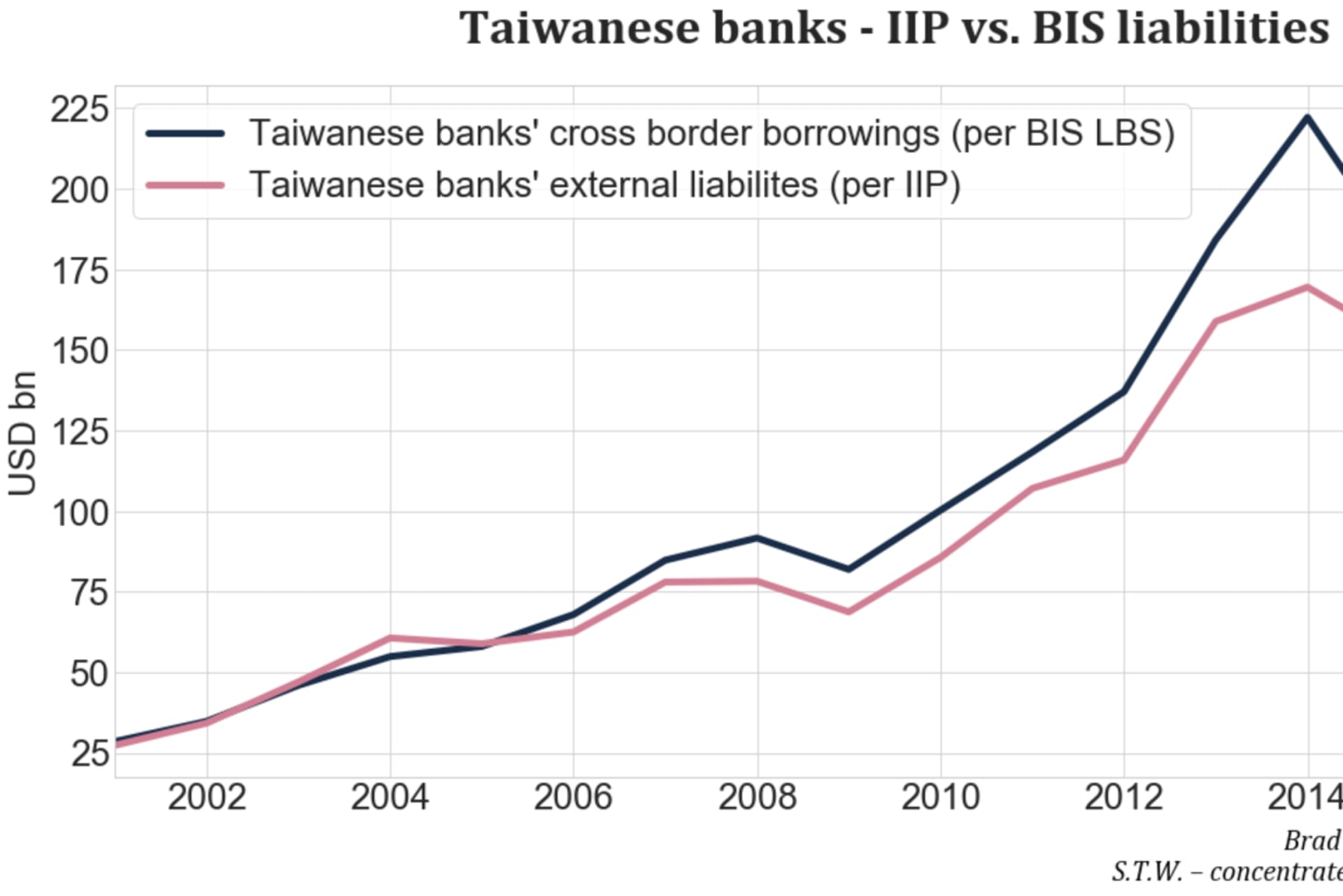

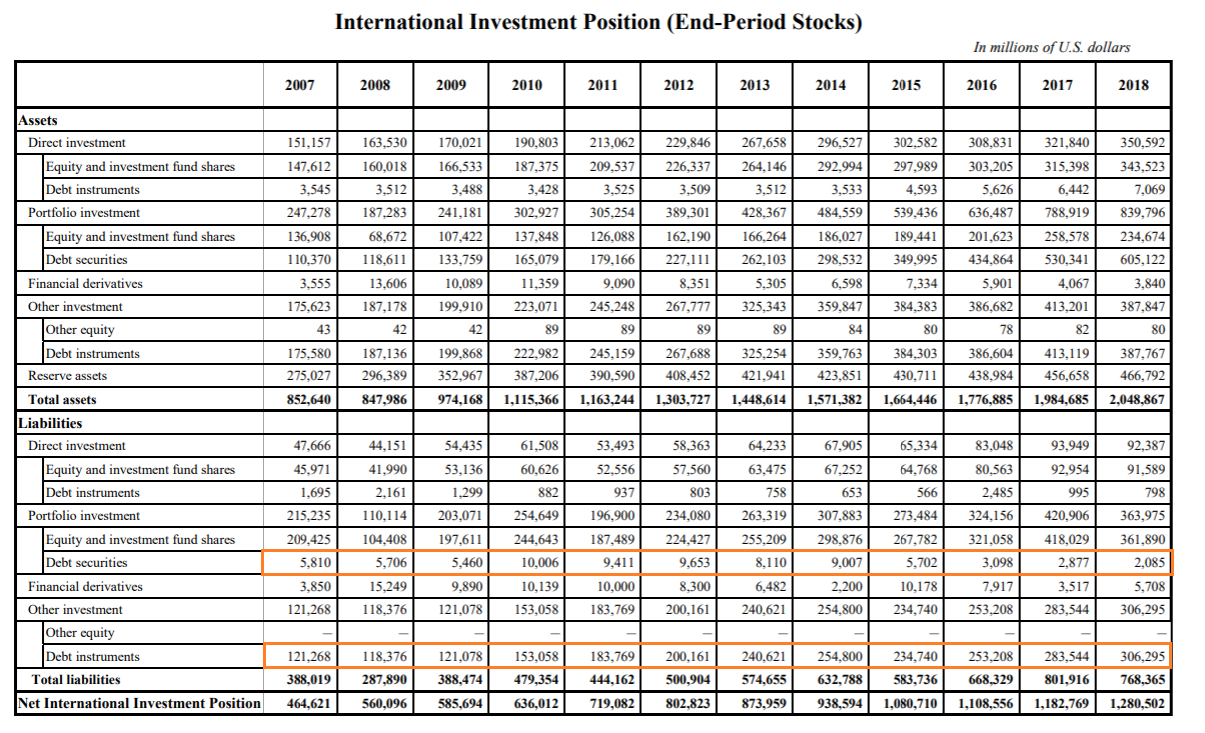

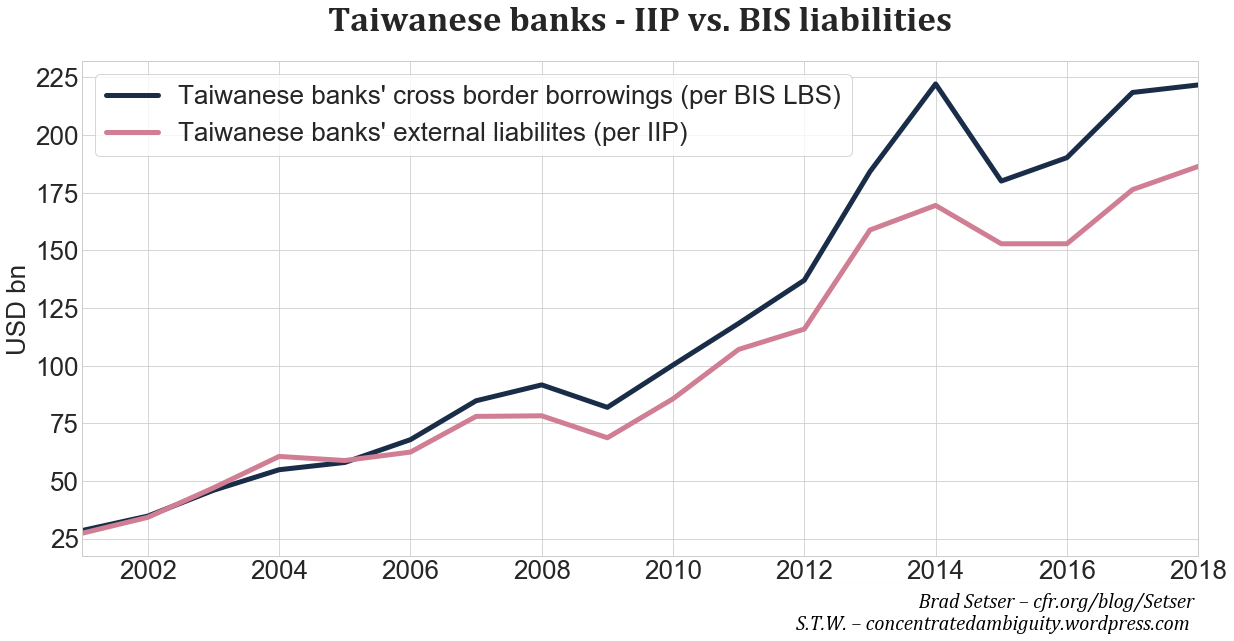

Taiwan looks different. Taiwan’s International Investment Position (IIP), shown in Fig. 1, does not feature large foreign holdings of debt securities. Taiwan in fact has a range of regulatory impediments that make it difficult for non-residents to hold its domestic debt securities. Instead, foreign residents hold a USD 300bn and increasing claim in the ’Debt Instruments’ section in the ’Other Investment’ category. This category is commonly composed of currency and deposits foreigners hold with banks, other overseas loans and trade credit. In Taiwan, these account for USD 186bn, USD 30bn and USD 87bn respectively at the end of 2018. If these were all TWD-denominated and the result of the search for collateral by FX counterparties, the puzzle surrounding lifers’ FX hedges would be solved.

National statistical bodies do not normally release the currency composition of cross-border borrowing & lending directly, but they do collect the data and submit these to the Bank of International Settlements (BIS). The BIS compiles these submissions across the globe into two large databases, the Locational and Consolidated Banking statistics. Taiwan, as well as all relevant counterparty countries, report to the BIS, so that it is possible to work out the currency composition of the IIP accounts.

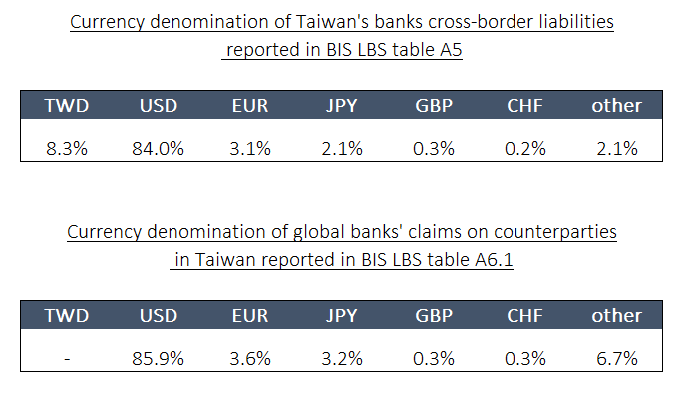

The USD 186bn claim foreigners hold on Taiwan’s banking system can be reconstructed using cross-border borrowings reported by Taiwan’s banks in the BIS Locational Banking Statistics survey. The correlation between the two series (Fig. 3) is very high, indicating a large overlap in the underlying exposures and thus allowing extrapolation of the currency details the BIS provides to the IIP. These indicate that over 92% of claims foreigners have on Taiwan’s banks are denominated in currencies other than TWD, mostly in USD, which accounts for USD 172 bn (or 84%) at the end of 2018. This fact alone makes it highly unlikely foreign arbitrageurs are active in Taiwan in sizes large enough to meet lifers’ FX hedging needs.

By the nature of the foreign arbitrageur’s business model, it is very unlikely that funds extended as trade credits, or to the non-financial sector generally, are part of FX arbitrage trades. As a precaution, Fig. 2 also contains the currency composition of global banks’ claims on all counterparties in Taiwan. Were trade credits for instance denominated in TWD entirely, they would boost the ‘other’ category[6], which at 6.7% makes this an unlikely proposition. This is also in line with the consensus, stating that trade credit is overwhelmingly USD-denominated.

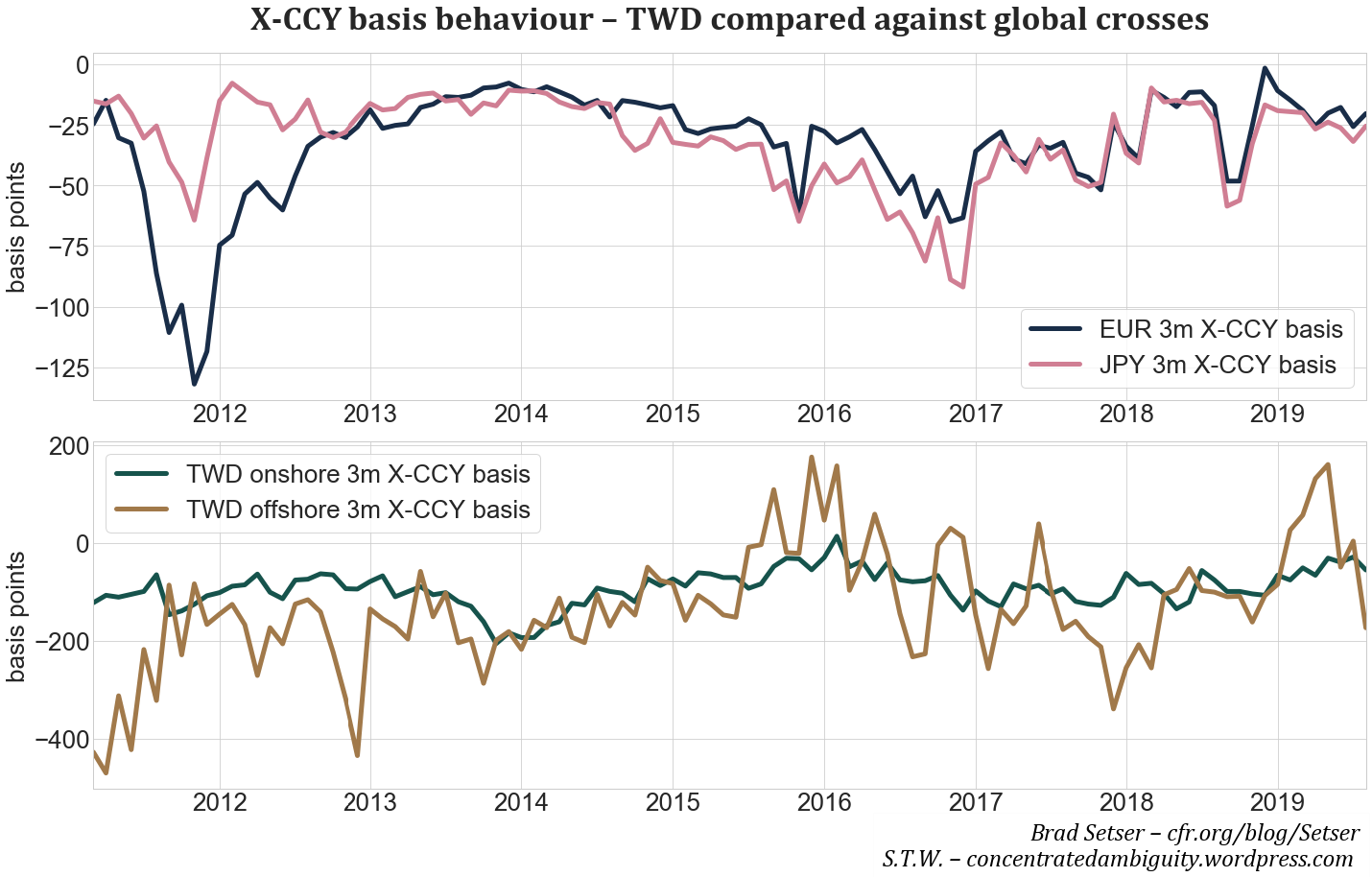

Lastly, it is also possible to show that Taiwan’s currency market behaves very differently than the markets in Europe and Japan. A cross-currency (X-CCY) basis is the deviation in price an FX derivative exhibits relative to the no-arbitrage indication based on interest rate differentials in the two currencies involved. As long as natural hedging demand and supply are of similar size, the X-CCY basis does not veer far from zero, as dealers can efficiently match up buyers and sellers. If, as is the case in Taiwan, Japan and Europe, the natural level of demand for FX hedges (all into USD in this case) exceeds natural supply, institutions in these nations have to offer an extra compensation to counterparties to nonetheless facilitate transactions. This extra compensation manifests itself as a negative X-CCY basis.

As outlined in a quarterly BIS review article[7], the level of the basis can be thought of to depend on a) the level of the demand-supply differential, b) the willingness of arbitrageurs to facilitate transactions. This in turn depends on the financial openness and regulations of the target market, as well as comparative returns on other nearly risk-free assets on offer for arbitrageurs. At the end of the day, the level of the X-CCY basis of a country is determined by country specific factors; in the short-term however, the business model of the arbitrageurs takes precedent.

In practice, this means that from the perspective of an arbitrageur (say, again, a flexible Treasurer at a U.S. bank), different FX basis markets (here JPY and EUR) directly compete with one another, but are also affected by common factors related to the overall business model of the arbitrageur (e.g. their funding sources, regulations in the arbitrageur’s home jurisdiction, yields on other investments etc). For this reason, the shorter-term dynamics of X-CCY bases in currencies in which hedging is facilitated by a common set of arbitrageurs should show a high degree of co-movement. For Europe and Japan, this is empirically the case. The r2 of regressing the EUR[8] 3m X-CCY on the JPY equivalent in level-terms from 2012-19 is 0.82, while the r2 of monthly changes is a still high 0.64.

Taiwan’s market by contrast looks different. The TWD basis in both onshore and offshore markets does not show any correlation with moves in the EUR and JPY X-CCY basis. This again showcases the unlikeliness of the ’regular’ international arbitrageurs present in Taiwan, providing FX hedges to lifers.

An entirely different possibility to consider relates to the large foreign holdings of Taiwanese equities also shown in Fig. 1. If all such holdings were FX-hedged, the problem would equally be solved. Since FX hedging equity portfolios is not the norm, especially helped in this case by the TWD’s stability relative to USD, the possibility of this to be true seems remote. All of the larger USD-denominated Emerging Market equity funds are offered as non-hedged version first and foremost. FX-hedged ETFs do exist, but further cement the point: Blackrock’s broad iShare Emerging Markets ETF (EEM) currently has assets under management of USD 25.5bn, while the currency-hedged version (HEEM) merely posts holdings valued at USD 180mn.

A last but unlikely proposition would state that foreigners provide FX hedges to lifers without creating an offsetting TWD position in cash markets in Taiwan, i.e. going long TWD outright via derivative markets. Such a behavior lacks a solid foundation, since an outright FX bet (of large size nonetheless, to match lifers) does not fit the business model of any overseas institution well. The opacity of OTC markets does not allow for direct refutation; the concluding method discussed next however affirms the expressed view.

Finally, if foreigners—regardless via which of the outlined channels—provided hedges to Taiwanese lifers, such transactions should also leave a mark on the derivatives section in Taiwan’s Balance of Payments and its International Investment Position.

The accurate accounting of derivatives in the BoP is a lengthy subject[9] but in brief, the accounting for FX hedges works as follows:

- As per chapter 5.80 in the IMF’s manual, “Transactions and positions in financial derivatives are treated separately from the values of any underlying items to which they are linked”, implying that the hedges themselves are always accounted for separately from the exposure to be hedged.

- Per 5.82, ”many [...] derivatives contracts are settled by payments of net amounts in cash, rather than by the delivery of the underlying items. Once a financial derivative reaches its settlement date, any unpaid overdue amount is reclassified as accounts receivable/payable.”, implying that settlement of exposures can take place via delivery of securities/assets or by cash payments of equal value and that the timing of these can be delayed, thus not immediately affecting the BoP, but rather being reported as contingent claims or liabilities in the IIP.

- Per 5.84-5.89, ”There are two broad types of financial derivatives—options and forward-type contracts.”, the latter category also encompassing futures and swaps.

- Per 5.90, ”At the inception of a forward-type contract, risk exposures of equal market value are exchanged, so a contract typically has zero value at that time. As the price of the underlying item changes,[...] the classification of a forward-type contract may change between asset and liability positions.” This means that before the ultimate termination of a forward contract, it will give rise to contingent claims/liabilities in the IIP, the BoP only being affected[10] once closeout occurs.

- Referencing FX swaps directly, 5.92: ”At the time of settlement, the difference in the values, as measured in the unit of account at the prevailing exchange rate, of the currencies swapped are allocated to a transaction in a financial derivative, with the values swapped recorded in the relevant other item (usually other investment).”, meaning the currency aspect of FX swaps & CCS are recorded in the same way as vanilla FX forwards.

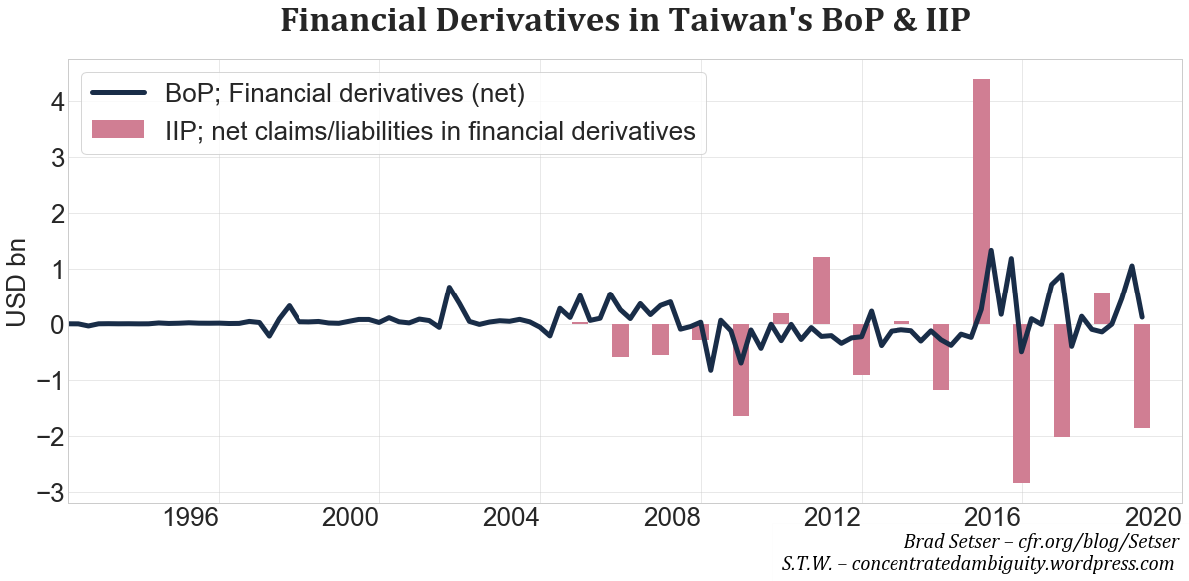

If foreigners provided FX hedges to lifers, the profits and losses these create whenever exchange rates fluctuate and their ensuing settlement should be observable in the derivatives section of the BoP and IIP, both shown in Fig. 5.

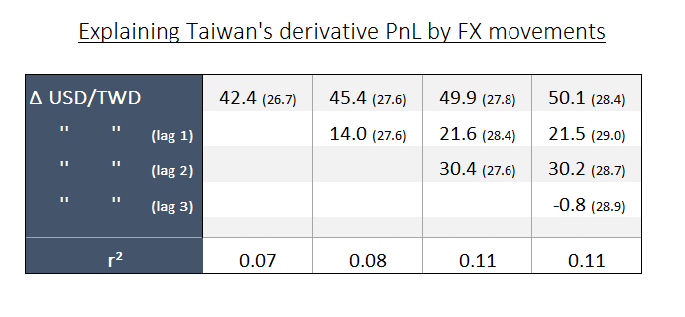

First, given the anecdotal lack of large derivative transactions in other product categories (equity, interest rates & credit) with foreigners, such FX transactions should be the primary driver of the derivatives section in Taiwan’s BoP. Furthermore, since most of lifers’ hedging transactions have a maturity of ≤1y and involve USD, a simple regression of current quarter FX returns plus appropriate lags[11] should explain a sizable portion[12] of Taiwan’s derivative BoP section.

The results of such analysis using the overall derivatives time series[13] is shown in Fig. 7 and corroborates the considerations in the prior sections. The explanatory power of the exercise is low (even if including a full year of FX movements) and none of the coefficients are statistically significant. Furthermore, given that lifers are long TWD in the forward market, one would expect the coefficients to be negative[14]. Size-wise, the BoP entries furthermore come in at levels much lower than would be expected by multiplying the size of lifers’ FX hedges by the relevant exchange rate movements during the respective quarters.

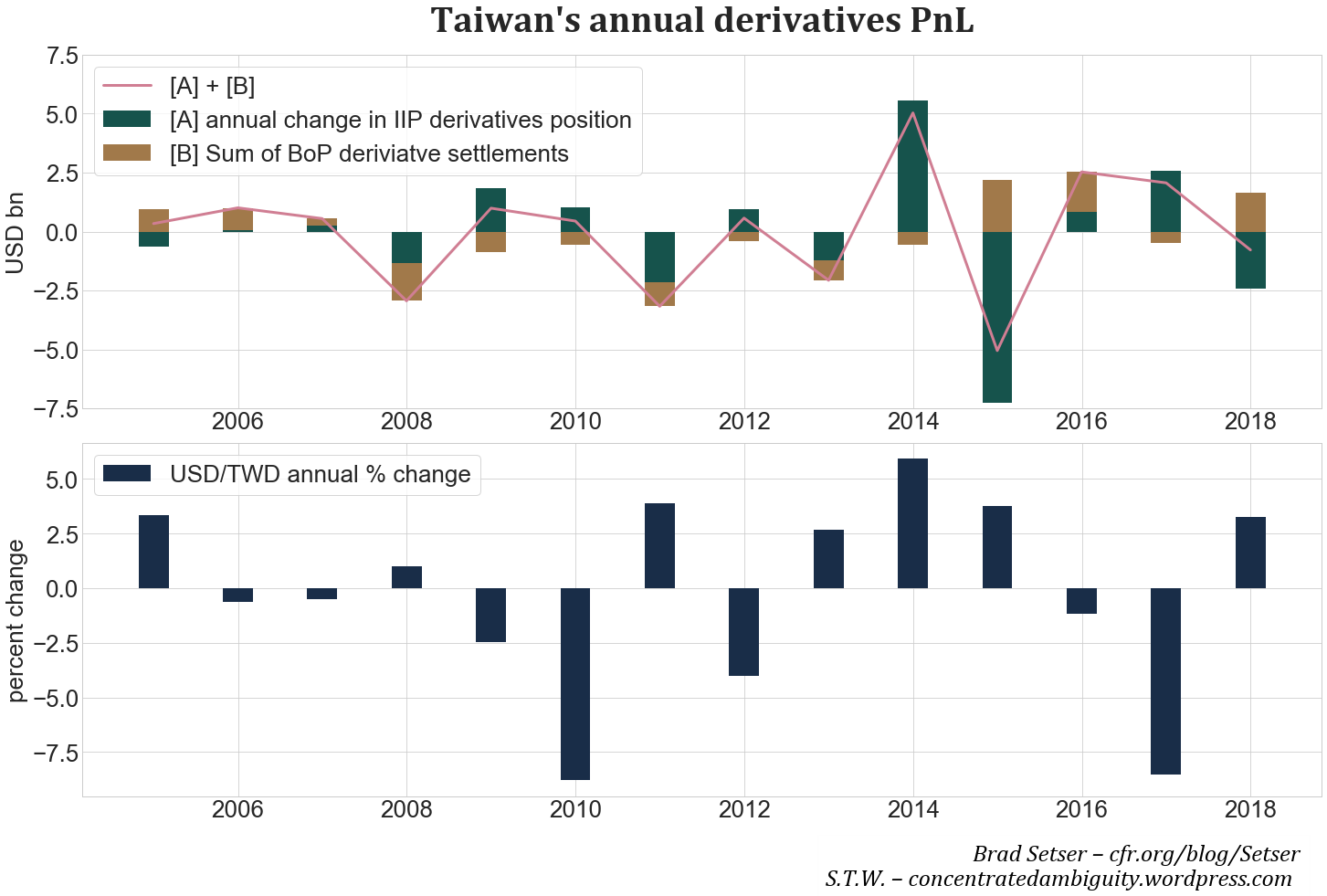

Second, the same analysis can be repeated at an annual frequency[15], incorporating BoP and IIP data. A year’s derivatives PnL is calculated by adding the cash settlements during the four quarters from the BoP to the change in the value of the derivatives position in the IIP. Here too, a clear correlation with changes in the USD/TWD exchange rate is not discernible.

Putting all the pieces together, it seems unlikely in the extreme that foreigners provide lifers the majority of FX hedges, necessitating at least one other actor to fill this position.

C. Taiwanese Banks

Domestic banks are, second to foreigners only, best equipped to manufacture FX hedges for customers. The ‘manufacturing perspective’ is key, as banking institutions are in almost all cases unable to take FX risk outright[16]—highly leveraged bank balance sheets are rather optimized to taking on duration and (limited amounts of) credit risk. Given this fact, the following equation is usually a good baseline for assessing a bank’s overall FX exposures, as well as that of individual currencies:

On-balance sheet FX position + derivatives ≈ 0 (1)

In consequence, if a bank has large net exposures to FX derivatives, it is almost always true that its on-balance sheet FX position tilts in the opposite direction. Of course, causality can run both ways:

- A bank, for whatever reason[17] , finds it has substantial FX exposure in its on-balance sheet section. The subsequent addition of FX derivative hedges neutralizes these, and the transactions truly serve as ’hedging devices’ for the bank itself.

- Alternatively, a bank faced with large & one-sided customer demands for FX derivative hedges can decide to manufacture these hedges itself[18] , by purposefully mismatching its on-balance sheet assets/liabilities to remain overall FX neutral.

But no matter which way causality runs, the result is the same: FX assets[19] exceeding FX liabilities requires an FX short position via derivatives to neutralize FX exposures, while FX liabilities exceeding FX assets requires a corresponding long FX exposure.

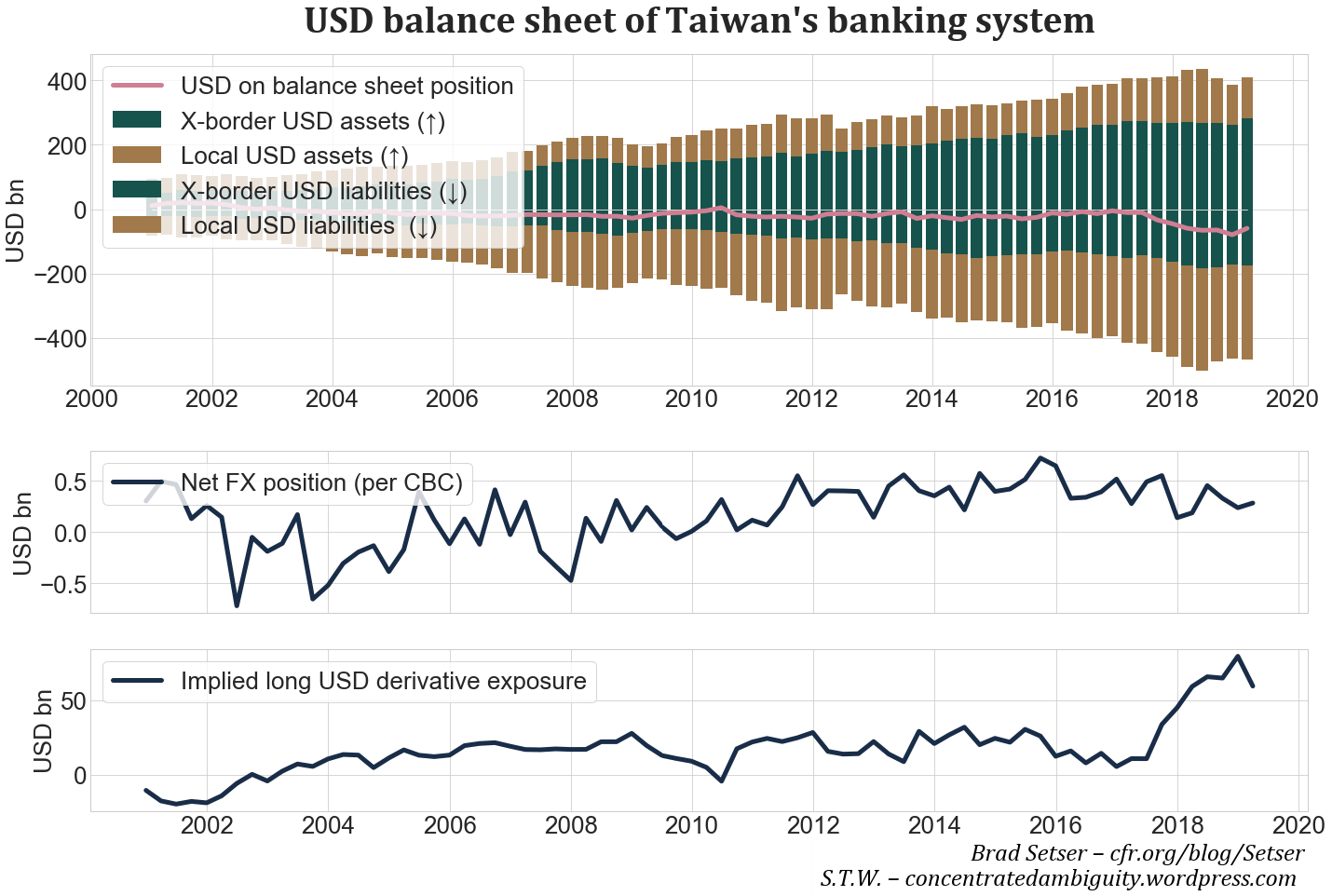

In order to construct the USD balance sheet of Taiwan’s banking sector, the previously consulted BIS Locational and Consolidated Banking Statistics results for Taiwan are drawn upon again. A seminal BIS working paper from 2009 lays out in detail how this source can be used to gain insight into the currency exposures of a country’s banking system. In brief, the on-balance sheet exposures to the major currencies of a country’s banking system can be decomposed into three categories:

- Cross-border assets/liabilities: These are positions booked by all offices of the selected country worldwide on entities located in a country other than itself, and in all currencies. For instance, Taiwan headquarter lending USD to a manufacturing company in Japan.

- Local Positions in Foreign Currencies: These are claims/liabilities booked by the foreign affiliates of a country’s banks, vis-a-vis residents of the affiliate’s host country. For instance, the Australian subsidiary of a Taiwanese bank lending USD to an Australian manufacturing company.

- Domestic claims/liabilities in Foreign Currencies: These are positions booked by domestic banks on local residents in foreign currencies. For instance, a Taiwanese bank borrowing USD from a Taiwanese household.

Information for the first category is found in the Crossborder section in the Locational Banking Statistics, the other categories in the Local Positions in Foreign Currencies section. In contrast to the referenced BIS paper, the analysis here has to be conducted at the geographic country level, rather than the broader nationality (of the banking entity) level, as Taiwan does not submit the latter[21] . In practice, this should not distort the results too much, as Taiwan’s banks do the largest share of their business from Taiwan headquarters, with affiliates of relatively minor importance in an international comparison.

Fig. 8 shows the result of compiling the numbers according to the laid-out plan. Panel one shows that for the largest time since 2000, Taiwan’s banks kept on-balance sheet USD exposures broadly in balance, with slightly more FX liabilities than assets on average. Since 2017, USD liabilities, i.e. crossborder borrowings and FX deposits from Taiwanese residents, have grown faster than USD assets[22] , resulting in an imbalance of USD 60bn as of March 2019.

Panel two shows a time series obtained from the CBC, depicting the net FX position of the Taiwanese banking system. As expected, the aggregate position does not stray far from zero. Given that USD is by far the most transacted foreign currency in Taiwan, this time series is largely a reflection of USD positions.

Panel three combines the prior two panels and extracts the net USD FX derivative position according to Equation 1. A mirror image of the first panel, it shows Taiwan’s banks were net long USD in FX derivatives for most of the time since 2000, i.e. providers of FX hedges to other actors. The provision of hedges has picked up substantially since 2017 and stands at the same referenced value of USD 60bn as above. This USD 60bn explain about 25% of lifers’ overall demand for FX hedges—a substantial portion, but far from the whole story.

D. Non-financial Taiwanese corporations

Non-financial corporations establish FX derivative positions for two primary purposes:

- Hedging bonds issued in a different currency. If a corporation has no natural FX revenues or FX assets, hedging is usually done for the entire maturity via a cross-currency swap.

- FX hedging of future export & imports invoiced in a foreign currency. While some FX hedging of this sort, usually via FX forwards or options, is common for most companies, such transactions only grow large when absolutely necessitated by a company’s business model, e.g. large, multi-year projects with payment in FX only at contract conclusion[23] .

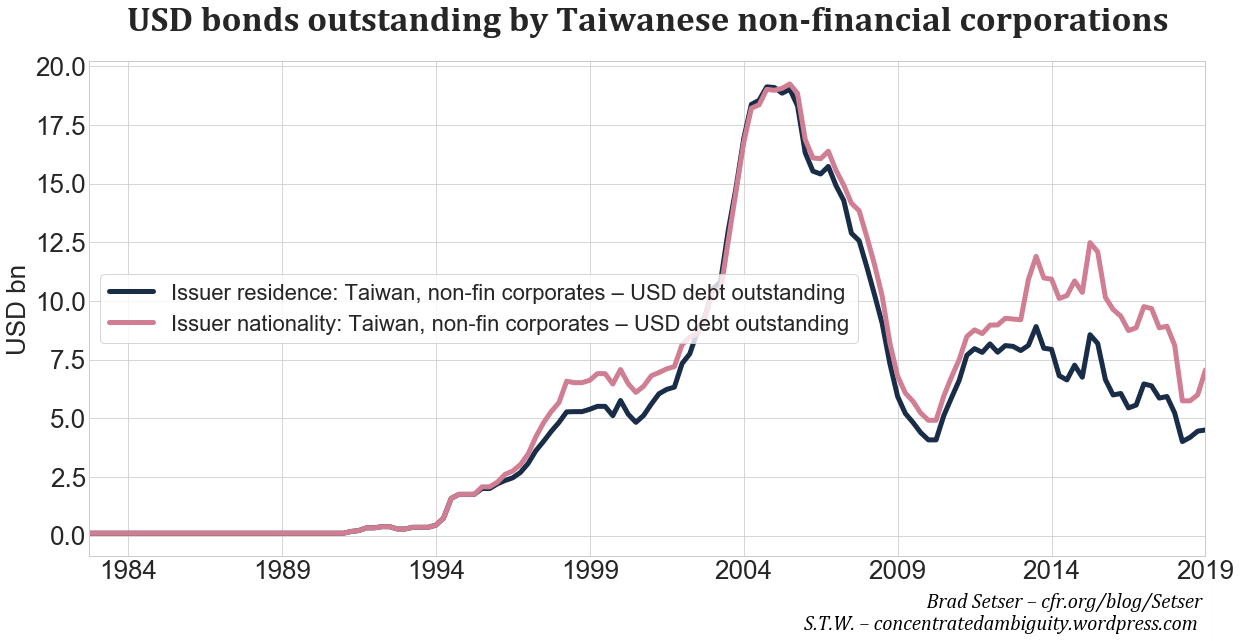

The upper limit for FX hedges resulting from bond issuance is easily established by compiling the universe of USD denominated bonds[24] issued by Taiwan’s non-financial corporations.

Non-financial corporations issued up to USD 20bn in the run up to the financial crisis, which were however mostly repaid by 2010. No significant net issuance has occurred since then. With no more than USD 7bn outstanding, such issuance can only play a minor role in supplying FX hedges to the life insurance sector.

FX hedging of future exports and imports in large sizes is equally unlikely, if only for the fact that Taiwan’s position in the ICT value chain is a high turnover business, with relatively short payment cycles.

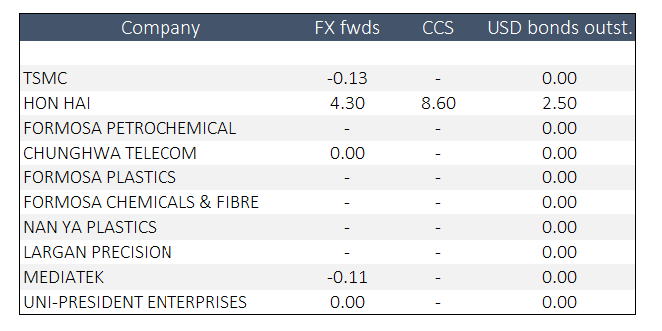

An analysis of the 2018 year-end financial statements of the ten largest publicly traded non-financial companies in Taiwan tends to confirm this notion. As in most countries, publication of notional positions in derivatives is not obligatory, yet companies in which FX hedging forms an integral part of a business model tend to disclose these nonetheless. Of all covered entities, only Hon Hai has larger exposures in FX derivative markets. It has USD 2.5bn debt securities outstanding and holds an aggregate long FX derivatives position of USD 12.9bn, obligating it to exchange TWD for USD in the future. Among the other companies, it is usually mentioned that opportunistic FX hedging might occur, but no numeric disclosures are provided, most likely due to negligible sizes. This is confirmed by the commonly small claims & liabilities resulting from derivative transactions in companies’ balance sheets.

Since Taiwan’s trade with the rest of the world is mostly denominated in USD or other major currencies, it appears unlikely that foreign non-financial corporations engage in larger FX hedging in TWD markets. While disclosures of internationally operating firms with supply chain exposures to Taiwan do not allow a proper analysis, if such transactions were common, they should be visible in the Taiwan’s Balance of Payments. Since the prior analysis of Taiwan’s BoP did not detect larger net FX derivative transactions with the rest of the world, FX hedging of trade-related transactions by firms abroad is deemed insignificant.

Put together, non-financial Taiwanese companies might be a marginal supplier of FX hedges due to Hon Hai’s exposures, but are not systematically doing so at scales large enough to match lifers hedges at USD 250bn.

In summary, the three typical providers of FX hedges examined in this chapter do indeed provide lifers a portion of their FX hedges. Domestic banks appear to provide around USD 60bn, with the numbers for the foreign sector and nonfinancial corporations meaningfully lower, and most probably not exceeding USD 20bn each. Even in the most optimistic scenario, these three sectors do not even cover 50% of lifers USD 250bn FX hedges.

* The Council on Foreign Relations takes no institutional positions on policy issues and has no affiliation with the U.S. government. All views expressed on its website are the sole responsibility of the author or authors.The Council on Foreign Relations takes no institutional positions on policy issues and has no affiliation with the U.S. government. All views expressed on its website are the sole responsibility of the author or authors.

** Contact at [email protected]

[1] From the regulatory setup already—which will be examined in greater detail in a later chapter—strong reasons exist to assume traditional FX arbitrageurs are not active in Taiwan in large sizes. This is due restrictions imposed on all incoming foreign funds, limiting their deployment to fixed income and money market instruments to 30% of the overall amount.

[2] This might occur via the U.S. bank’s local subsidiary or, if executed from U.S. headquarter, be intermediated by local Taiwanese banks.

[3] At termination of the contract, this exchange would be reversed, but for the moment it is assumed the transaction is rolled indefinitely, as it is beneficial to all parties.

[4] Which, in all likelihood, is not among the core competencies of the U.S. bank.

[5] See for instance page 46 of the October 2017 BoJ Financial Stability Report for an assessment of FX hedges established by Japanese institutions.

[6] There is not a singular TWD category in this dataset.

[7] Borio, C., R. McCauley, P. McGuire, and V. Sushko, 2016, ’Covered Interest Parity Lost: Understanding the Cross-Currency Basis’, BIS Quarterly Review, September, pp. 45–64, Bank for International Settlements, Basel.

[8] By convention, X-CCY bases are quoted against USD, with negative values reflecting the extra annual cost a foreign institution has to pay their USDbased counterparty to enter a transaction.

[9] The sixth edition is available from the IMF here. Relevant paragraphs start on page 94.

[10] As also stated in 5.90, periodic settlements can restore a zero market value prior to the conclusion of contract. In some countries, the U.S. most notably, statistics on collateral exchanges (with equivalent effects to intermediate settlement) before trade conclusion are also collected, providing the most comprehensive perspective.

[11] Due to the settlement only occurring at trade conclusion. For instance, if a 1y forward experiences a mark-to-market positive shock in Q1 of its existence, the accounting in the BoP (if the exchange rate then stays at that level) only occurs at the end of Q4.

[12] Given that lifers hedges have grown substantially, the coefficients would capture the average over the entire 9y period, which, while not referencing a particular quarter, would nonetheless be expected to be highly statistically significant.

[13] The same analysis can also be repeated with the sectoral time series included in Taiwan’s BoP. The results are functionally similar.

[14] I.e. rises in TWD vs. USD would create a positive derivatives PnL, and vice versa.

[15] Taiwan unfortunately only releases its IIP once per year.

[16] As opposed to duration or IG credit risk, the degree of FX volatility is much less predictable, exposing highly levered institutions to potentially perilous amounts of risk, if overall FX exposures stray far from zero. Regulations are rightly punitive to open FX exposures, but institutions typically limit such risk taking on business grounds already.

[17] Common reasons include differentials in the price of funding in jurisdictions around the globe, specific regional knowledge on the lending side or, lastly, arbitrage opportunities created by differences in regulations.

[18] Because such transactions are balance-sheet heavy and regulatorily inefficient, banks resort to the manufacturing only if large imbalances in orderflow exist, no (foreign) arbitrageurs step in in sufficient quantities and the compensation (via a negative X-CCY basis) is appropriately sized.

[19] FX assets here meaning any asset denominated in a currency other than the bank’s base currency. In Taiwan’s case specifically, replace FX with USD.

[20] McGuire, P and G von Peter (2009):’The US dollar shortage in global banking and the international policy response’, BIS Working Papers, no 291. Especially the Data Appendix.

[21] This means use of ’Locational Banking Statistics by residence’ rather than ’Locational Banking Statistics by nationality’.

[22] In terms of causality, this would indicate a mix of the two directions outlined. FX deposits from residents are hard to decline, but if appropriate USD assets cannot be sourced, translation into TWD and domestic lending paired with FX hedges might be the most profitable investment. On the other hand, USD cross-border borrowings are largely voluntary, thus indicating an arbitrage intention, when paired with FX hedges.

[23] The best historical example of such a condition are Korean shipbuilders precrisis, receiving large USD-based orders payed upon delivery. This exposed builders to FX risk for one to two years, which they resolved by selling USD forward to Korean banks.

[24] Non-financial corporates in Taiwan have in addition borrowed ∼USD 8bn from international banks. In contrast to bonds, where it is the ample liquidity of overseas markets attracting foreigners and as a result necessitating an FX hedge, borrowings from banks can be tailored to a client’s needs, implying FX hedges for loans from overseas banks are much less common than on the bond side.