The Rise of Islamic Finance

Published

After growing to a $1 trillion asset class in Muslim countries, Islamic finance is poised for an era of globalization.

Introduction

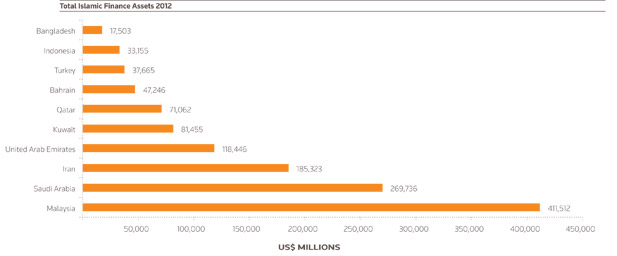

Global Islamic financial assets have soared from less than $600 billion in 2007 to more than $1.3 trillion in 2012, an expansion rooted in the growing pool of financial assets in Muslim-majority countries driven by consumer demand for products that comply with religious codes. Assets are concentrated in Muslim countries of the Middle East and Southeast Asia, but the sector appears poised to enter Western markets and complement conventional financing.

Prime Minister David Cameron announced in 2013 that the United Kingdom will issue a £200 million ($327 million) Islamic bond, or sukuk, making it the first non-Muslim country to tap into Islamic financing. Companies in the United States are also considering Islamic finance to fund business ventures and infrastructure projects. Demand for new Islamic investments is expected to outstrip supply by as much as $100 billion by 2015, an imbalance that could translate to much-needed liquidity in some tight markets. But the industry remains small and will need to expand considerably to have a significant impact on global financial markets.

Origins and Controversy

Muslims invested in and stored financial assets according to their religious principles for fourteen centuries before the emergence of the first Islamic financial institution, Dubai Islamic Bank, in 1975. (Conventional finance has also considered ethics in its centuries of development, which can be observed today in corporate social responsibility investments.) Hundreds of Islamic banks have been launched since 1975, with millions of Muslims using Islamic finance products from Malaysia to Michigan. Some countries—including Malaysia, the United Arab Emirates, Iran, and Saudi Arabia—actively foster the nascent and growing industry.

Reinterpreted medieval Islamic contract laws form the basic structures of the new asset class that doesn’t contravene sharia, or Islamic law. Sharia-compliant financial instruments can’t pay or collect interest, due to Islam’s proscription of usury; Islamic investments also can’t be associated with alcohol, pork, gambling, pornography, or other Muslim prohibitions. Risk-sharing and profit-sharing must be structured into contracts, investments should enhance society, and financing should be backed by assets. Islamic banks have developed tools to address these constraints and perform their basic function: to take deposits, invest them, and profit from the spread.

Sharia boards acted as a safeguard against the excess of conventional finance.

Ibrahim Warde, Tufts University

One of the basic building blocks of Islamic finance is murabaha, where “two parties agree to trade at a price equal to the cost plus mark-up or profit,” writes Rice University professor Mahmoud Amin El-Gamal. This allows, for example, a bank to purchase an asset, like a car, for $10,000 and sell it to its customer for $11,000 in installments over a year. In conventional finance, the bank lends money at a certain interest rate using the car as collateral, while the murabaha transaction the bank purchases the goods and then sells it to its customer. Other financial instruments and tools such as ijarah (leasing), mudarabah (profit sharing, usually between investors and managers), musharakah (joint venture), sukuk (Islamic bonds), and takaful (Islamic insurance), allow the development of Islamic financial products that span retail and corporate banking, private equity, and insurance.

This financial innovation has created an asset class that caters to more than a billion Muslims worldwide and is fueled by rising incomes in many Muslim countries, from Persian Gulf oil exporters to dynamic Muslim economies in Southeast Asia. Muslims concerned that their money would be involved in un-Islamic activities at conventional banks can head to Islamic banks in more than fifty countries to open checking and savings accounts, apply for credit cards, finance cars and homes, and purchase insurance.

A major principle in Islamic finance is to have a direct link between the real and financial economy. Sharia boards—oversight committees made up of experts in Islamic finance who are paid by banks to sign off on products and practices—have been lenient at times with some structures, but hold firm to the principle that financing must benefit the real economy. Ibrahim Warde, a professor of international business at Tufts University, says some bankers were annoyed with their sharia boards for forbidding Islamic banks from following the lead of conventional banks during the run-up to the global financial crisis. “Sharia boards acted as a safeguard against the excess of conventional finance,” he says.

Islamic finance has long faced the criticism that it’s just mimicking the broader market. Even the main premise of Islamic finance, that interest is forbidden in sharia, isn’t a settled issue. Muhammad Sayyid Tantawy, then the grand mufti of Egypt, issued a famous fatwa in 1989 that differentiated between riba (usury), defined in sharia as excessive interest similar to loan sharking and predatory lending, and interest used in conventional banking. Analysts say his conclusion that modern finance doesn’t contravene sharia, as well as the collapse of several Islamic saving schemes in Egypt in the 1980s, are the reasons why Egypt’s large Muslim population has lagged in adopting Islamic finance.

Many bankers in the Middle East are also skeptical of Islamic finance. Hassan Heikal, a prominent Egyptian banker who founded EFG Hermes, one of the region’s largest investment banks, has been a vocal critic of the industry. In 2006, he dismissed sukuk as “conventional bonds that are coated with an Islamic shell.”

When Islamic banks appeared in the 1970s, the goal was to create an alternative financial system, but pragmatism set in and the industry developed products similar to those used in conventional finance, Warde says. “The criticism of the industry is valid, up to a point,” he adds. That point was clear when Islamic banks avoided subprime lending and trade in exotic derivatives, demonstrating that the industry wasn’t blindly following conventional finance.

The debate over the origins and basic principles of Islamic finance has waned in recent years, and the focus has shifted to claiming a stake in the growing market. Even funds managed by EFG Hermes have made sharia-compliant investments.

A Rising Asset Class

Assets held by Islamic banks continue to grow by more than 15 percent per year, and analysts at Standard & Poor’s predict the potential size of Islamic financial markets could reach several trillion dollars. Banks in the Persian Gulf and Malaysia have become flush with sharia-compliant deposits and are scouring for regional and international opportunities to deploy them in Islamic financial instruments to diversify risk and improve yields.

Islamic banks have played an important role in financing infrastructure projects in Muslim countries, and have been a source of funding for foreign companies and joint ventures operating in the Middle East and Asia. International banks such as HSBC, Crédit Agricole, and Standard Chartered have established sharia-compliant banking divisions, and advised corporations and governments on issuing sukuk and other financial products. Islamic banks have popped up in some Western countries, such as the Kuwait-backed Bank of London and the Middle East (BLME), which is sharia-compliant down to the lease contracts on its photocopy machines. This geographic expansion is expected to continue both to cater to Muslim consumers and to find new investment opportunities for large, cash-rich Islamic banks in the Middle East and Asia.

Sukuk: A Global Trajectory

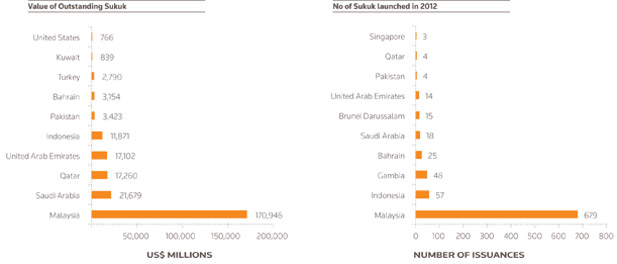

One of the most promising developments in Islamic finance that has wide applications outside Muslim countries are sukuk, or Islamic bonds. Sukuk (plural of sakk) are capital market securities issued by companies or countries. They act like bonds, delivering a stream of payments to investors until maturity. Sukuk deals typically are backed by an underlying physical asset like a power plant, oil field, or real estate, a structure that complies with sharia and may reduce the risks that investors face in the event of a default. However, in many cases, Islamic bonds don’t confer ownership of an asset to their holders, which caused some confusion among investors when some sukuk defaulted in 2009 and 2010.

The global sukuk market has doubled since 2007, driven mostly by issuances in Malaysia, which had $170 billion in outstanding sukuk and represented 68 percent of total global sukuk at the end of 2012, according to the 2013 Islamic Finance Development Report published by the Islamic Development Bank and Thomson Reuters. Countries such as Saudi Arabia, Qatar, the United Arab Emirates, and Indonesia comprise the rest of the market.

Other countries have expressed interest in tapping demand for sukuk by issuing their own sovereign and corporate paper. The United Kingdom plans to be the first Western country to issue a sovereign Islamic bond, while Singapore, Gambia, Senegal, South Africa, and Nigeria are planning to expand the footprint of Islamic securities in 2014. Hong Kong is also considering sukuk in 2014.

The UK government’s proposal to issue Islamic sukuk was “driven primarily by a senior Muslim member of the government, Baroness Sayeeda Warsi, who has made a compelling argument that the UK can compete with Malaysia and the Gulf in drawing sharia-compliant investors,” says Ed Husain, CFR’s senior fellow for Middle Eastern Studies. A British bond may spur other Western governments to follow suit. In addition to opening a channel to a new pool of capital, a British bond “can send a message to Muslim populations in the West and Muslim countries in the East that European governments are not hostile to Islam and Muslims,” Husain adds.

Sukuk and Islamic banking won’t have a dramatic impact on global finance for the foreseeable future: Total Islamic financial assets are less than half of the assets controlled by one major Western bank, JPMorgan Chase. But its expansion in the West can have political benefits and “help the nascent industry become more professional, standardized, and creative,” Husain says.

Islamic Finance in the United States

Sharia-compliant products, mainly personal home mortgages, have been available in the United States since at least 2002, when Guidance of Reston, Virginia, was established. (These financial institutions were prudent with their lending and didn’t tap the subprime borrowers.) But only a few billion dollars of Islamic home financing are provided each year, a tiny fraction of the multitrillion-dollar conventional mortgage industry. Some U.S. companies with global operations have issued sukuk, such as General Electric’s $500 million offering in 2009.

As the sharia-compliant asset pool swells in the Middle East and Asia, a mismatch has emerged between available capital and supply of investments in the region, prompting many banks and investors to look outside the Islamic world for returns. Bankers say investors are eyeing opportunities in the United States in a variety of sectors such as infrastructure, oil and gas, and real estate.

Sharia-compliant products, mainly personal home mortgages, have been available in the United States since at least 2002.

Paolo Curiel and Ibrahim Mardam-Bey, two executives at Taylor-DeJongh, a Washington, DC-based investment bank that has brokered sharia-compliant deals in the United States, note that Islamic banks in the United Arab Emirates have deployed only 80 percent of their deposits, just one example of the capital glut in Islamic financial institutions. These institutions have historically allocated international investments into real estate but are now looking to diversify into new sectors, which could provide new liquidity to small and medium-sized companies in the United States. Infrastructure sukuk similar to those issued in Saudi Arabia and Malaysia are also seen as a potential source for funding in the United States [PDF].

Some U.S. financial institutions and lawmakers have expressed concern that Islamic banking transactions may deliver funds to terrorists. However, experts have testified in Congress that there is no evidence to prove that Islamic banks are more prone to facilitating transactions for money launderers and terrorist financiers than other banks. A Congressional Research Service report on the industry notes that there may be a “conflation of Islamic finance with hawala” [PDF], which is an informal, trust-based money transfer system that has been used for centuries in the Middle East and has been associated with terrorist financing in recent decades.

Islamic banks and investment firms are regulated by finance ministries and central banks that also oversee conventional banks in Muslim countries. The existing financial laws and regulations are viewed to be broad enough to accommodate the industry, according to the CRS report. Standards for the industry are mostly set by the Islamic Financial Service Board (IFSB) and the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), two bodies that include representatives from regulatory authorities. But different interpretations of sharia and regulatory practices across countries pose challenges to standardizing the industry.

Recommended Resources

This Congressional Research Service report provides a broad overview of Islamic finance and its policy implications for the United States.

This 2012 IMF Working Paper explains the differences between Islamic and conventional financial institutions in Malaysia.

The New York Times reports on sharia-compliant investment opportunities in the United States.

Tufts University professor Ibrahim A. Warde explains the origins and rise of the industry in Islamic Finance in the Global Economy.

Rice University professor Mahmoud Amin El-Gamal explains the development of the sector in Islamic Finance: Law, Economics, and Practice.t

Colophon

Staff Writers

- Mohammed Aly Sergie

Additional Reporting

Header image by Samsul Said/Reuters.

Backgrounder

Backgrounder Backgrounder

Backgrounder

Backgrounder

Backgrounder