After the Pandemic: Can the United States Finally Retool for the Twenty-First Century?

Over the more than half a century since the United States embraced its integration into the global economy, it has produced both the strongest and the weakest of the advanced economies.

The strengths are obvious in the United States‘ brilliant scientific establishment, its top-ranked universities, its lead in innovation, and its world-beating companies from Apple to Amazon.

The weaknesses have never been more obvious than during the current outbreak of the coronavirus–among these a woefully inadequate health insurance system, lack of paid sick leave and other basic job protections, and an unemployment insurance system that encourages companies to fire workers quickly.

The virus has ruthlessly exposed the shortcomings of a country that has failed to remake itself for the world it now occupies. When the pandemic recedes, the United States will face some of the toughest questions in its history about how to retool itself for the modern world.

In my 2016 book, Failure to Adjust: How Americans Got Left Behind in the Global Economy, I told the story of how economic globalization caught the United States off-guard. For most of our history, we were a reasonably self-sufficient economy, with an expanding domestic market that was more than large enough to exploit economies of scale. So as trade, global travel, and financial integration began to grow explosively in the 1960s, the United States was slow to recognize that it needed to adapt its institutions to the new realities.

One of the most telling examples is the program known as Trade Adjustment Assistance (TAA). It was launched by President John F. Kennedy in 1962 with the explicit goal of helping to support and retrain those who would lose jobs as a result of the coming acceleration of global competition that Kennedy and future presidents embraced. “When considerations of national policy make it desirable to avoid higher tariffs,” Kennedy said, “those injured by that competition should not be required to bear the full brunt of the impact.”

Despite the soaring rhetoric, the program was stillborn–under-funded by Congress and overly restrictive from the start. When the surge in Chinese imports in the early 2000s contributed to the loss of millions of manufacturing jobs, only a small fraction of displaced workers received TAA. Far more exited the labor market entirely through programs such as Social Security disability.

TAA is only one example of where U.S. institutions are poorly designed to deal with disruptive change, which has been accelerating over the past several decades. Whether the causes are trade competition, financial crises, job-displacing automation, or an unexpected and lethal pandemic that spreads across the world, the United States sorely lacks the capacity to help its citizens manage these shocks.

Two of the most glaring deficiencies are the absence of sick leave for a significant portion of the workforce, and an unemployment benefits system that requires companies to fire their employees before those workers have access to any government aid. The first has helped undermine efforts to contain the virus, and the second means that economic recovery in the United States is likely to be especially prolonged.

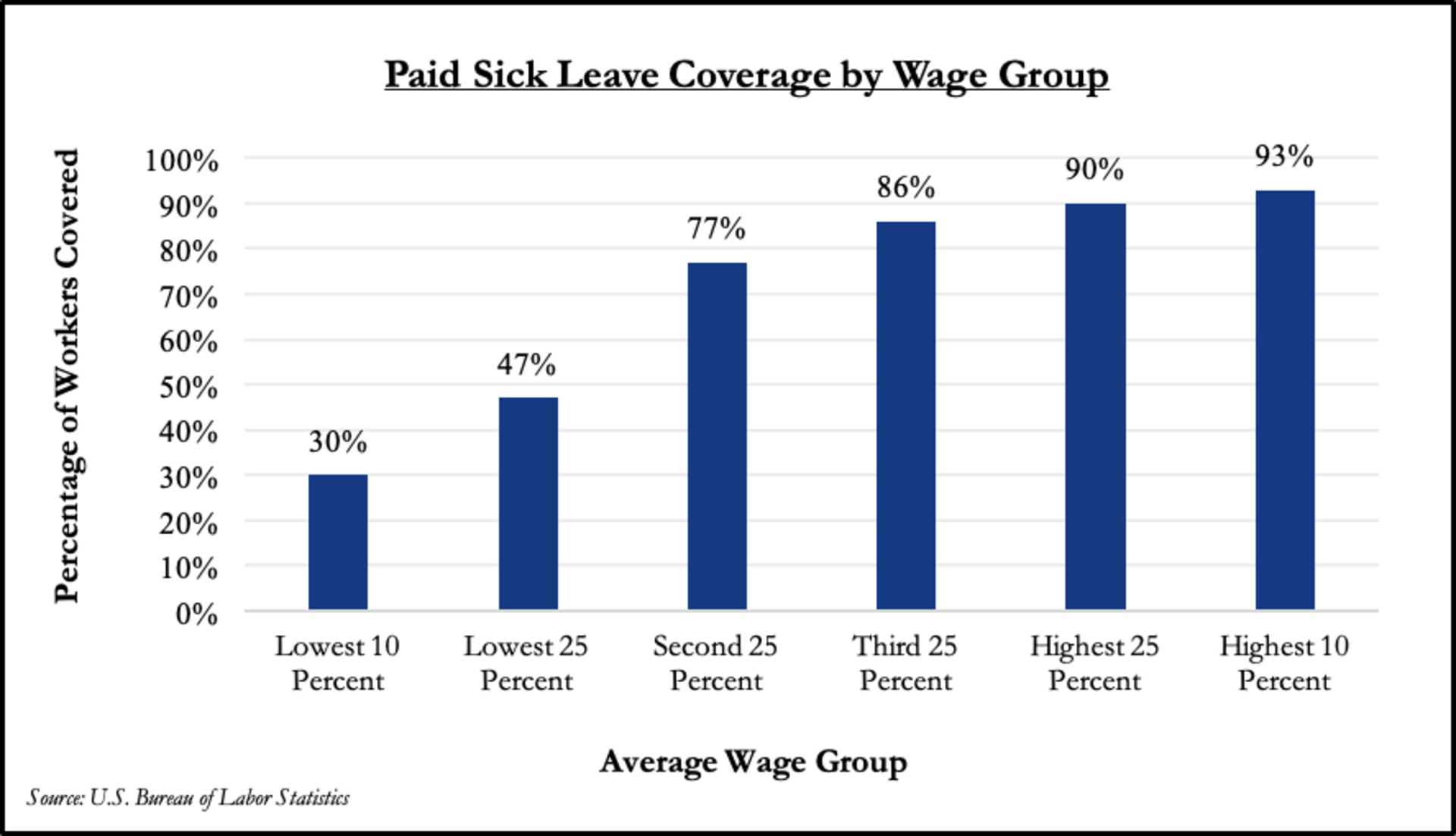

The importance of paid sick leave has never been more obvious than during this pandemic. Workers who fear losing pay, or even their jobs, if they fail to show for work are likely to shrug off the slight cough or fever that is the first sign of infection. Yet a large portion of U.S. workers lack access to this basic right. Only 43 percent of part-time workers get paid sick leave, for example, compared with 83 percent of the full-time employees. Among the top 10 percent of income earners, 93 percent have paid sick leave; for the bottom 10 percent, fewer than one in three enjoy the same right.

The unemployment insurance system is similarly riddled with holes. Benefits for workers only kick in after they have been fired from their jobs, which has encouraged companies to lay off workers in droves. In the last two weeks of March, more than ten million Americans were thrown onto the unemployment rolls, more than 6 percent of the entire U.S. labor force.

In contrast, Germany, the UK, Denmark and many other European countries are supporting the wages for workers who remain employed, allowing companies to keep them on staff and resume operations quickly as the economy recovers. In contrast, many U.S. workers will not be rehired until the consumer economy picks up and companies regain confidence in the future. That could take several years, depending on how long it takes to develop a vaccine or other cures for the coronavirus.

Unemployed workers also face impossible choices on health care coverage, because the United States remains the only advanced economy without some form of universal health insurance. They can maintain their former job-based plan–if they had one–only by paying the full costs through COBRA. Or they can take their chances on the ObamaCare market, where many plans come with huge deductibles.

These issues are just the tip of a very large iceberg. Lower-income Americans are woefully unprepared for retirement, and the crash in stock markets will make it worse. A new St. Louis Federal Reserve Bank survey says that among those without a high school diploma, or only a GED, just 22 percent had any sort of retirement savings, and among those with savings the median balance was just $35,000. Even among middle-income families, the picture is fairly bleak. The average retirement savings for couples over sixty-one, for example, is just $132,000–enough to generate just $5,200/year in retirement income on top of Social Security.

One piece of good news is that the stimulus bill passed with strong bipartisan support in Congress was properly ambitious. The measures to increase unemployment insurance, including expanding coverage to gig economy workers, will be especially critical in helping the growing ranks of the jobless.

But the bill was premised on a short-term economic shutdown of no more than a few months. If it lasts longer than that, Congress will either need to find more funding, or many Americans will run out of resources. Poorer Americans will be at the mercy of whether the two parties in Congress can continue to find ways to cooperate. If the money does not keep flowing from Washington, many Americans will find themselves unable to pay for mortgages, rent, health care bills, and other critical needs.

What the country needs is not a series of short-term bailouts, but long-term plans to ensure that most Americans are protected against such crises in the future.

Will this be the event that finally drags the United States into the twenty-first century? We certainly have the capacity to learn. The 2008 financial crisis, for example, exposed the dangerous fragility of the U.S. banking system; reforms put in place by Congress and the Obama administration in the aftermath, for all their shortcomings, left the financial system in a much stronger place to withstand the current economic shutdown.

But the lessons of the pandemic will be harder to absorb, because it has fully revealed the massive inadequacies of a social safety net designed for another era. We can learn that lesson and remake the country for the world we now inhabit. Or we can keep lurching from one crisis to the next.