Argentina: Sustainable, Yes, with Adjustment. But Sustainable with A High Probability?

Probably only connoisseurs of IMF Access Policy debates understand the importance of being judged “sustainable with a high probability” by 19th Street.

That’s what unlocks the keys to the kingdom, so to speak.

Sustainable, with a high probability, countries can borrow large sums from the IMF without having to worry about locking in their private creditors in some way.

What happens when a country that is sustainable, but not with a high probability, needs large sums?

Well, it is complicated.

I suspect I could litigate the precise meaning of the early 2016 access policy decision with the best of them, and I am not sure. The Fund broadly expects private creditors to maintain their exposure, but that goal can be achieved in a lot of different ways (selling some bonds to the private IMF?), and it may not always be necessary.*

I have little doubt that the Fund considers Argentina to be sustainable with a high probability (the last Article IV signaled more concern about the value of the exchange rate than about debt sustainability), and thus eligible for exceptional access. The U.S. certainly does.

I don’t disagree—public debt to GDP isn’t that high (yet).

But I do think it is a closer call than many.

Largely because of a variable that isn’t the focus of the new access policy.

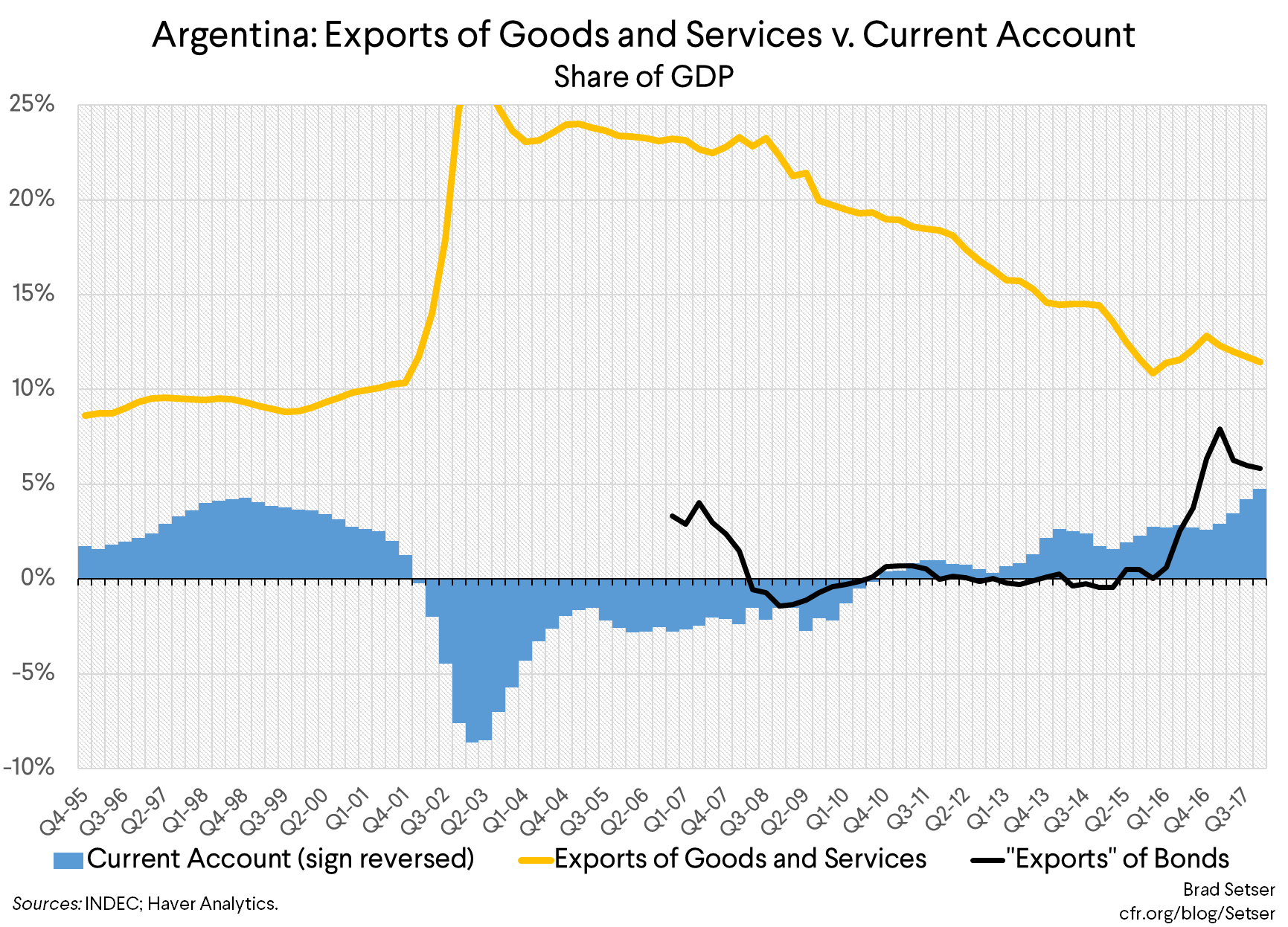

Namely, exports, or the lack of them. In 2017, exports were only a little above 10 percent of Argentina’s GDP.

As result, Argentina’s external debt—the debt it owes to the rest of the world—is pretty high relative to Argentina’s limited exports. External debt of thirty-five percent of GDP should be a bigger concern in an economy that exports 11-12 percent of its GDP (and relies on the almighty soybean, often processed, and other agricultural products for about a half of its exports) than in an economy like Germany, or Korea.

The same point applies to Argentina’s 5 percent of GDP current account deficit. It is large relative to Argentina’s export base.

Argentina thus isn’t a simple liquidity crisis—a crisis caused more by too few reserves than by too much overall debt.

And Argentina also isn’t (yet) a country that obviously has too much overall debt.

But it is a country that is adding to its (external) debt at too rapid a pace.**

Argentina thus falls into the category of countries that are “sustainable if they can successfully adjust.”

The Fund thinks that Macri’s government can carry off the needed fiscal adjustment, and that financing to allow a smooth path of adjustment will make the needed changes socially and politically sustainable. The Fund also believes—see the Article IV—that a gradual tightening of fiscal policy will allow a looser monetary policy and thus help bring the peso and the current account down over time. Fair enough. Ultimately, this is the kind of judgement call that the IMF has to make.

But the path to sustainability strikes looks difficult.

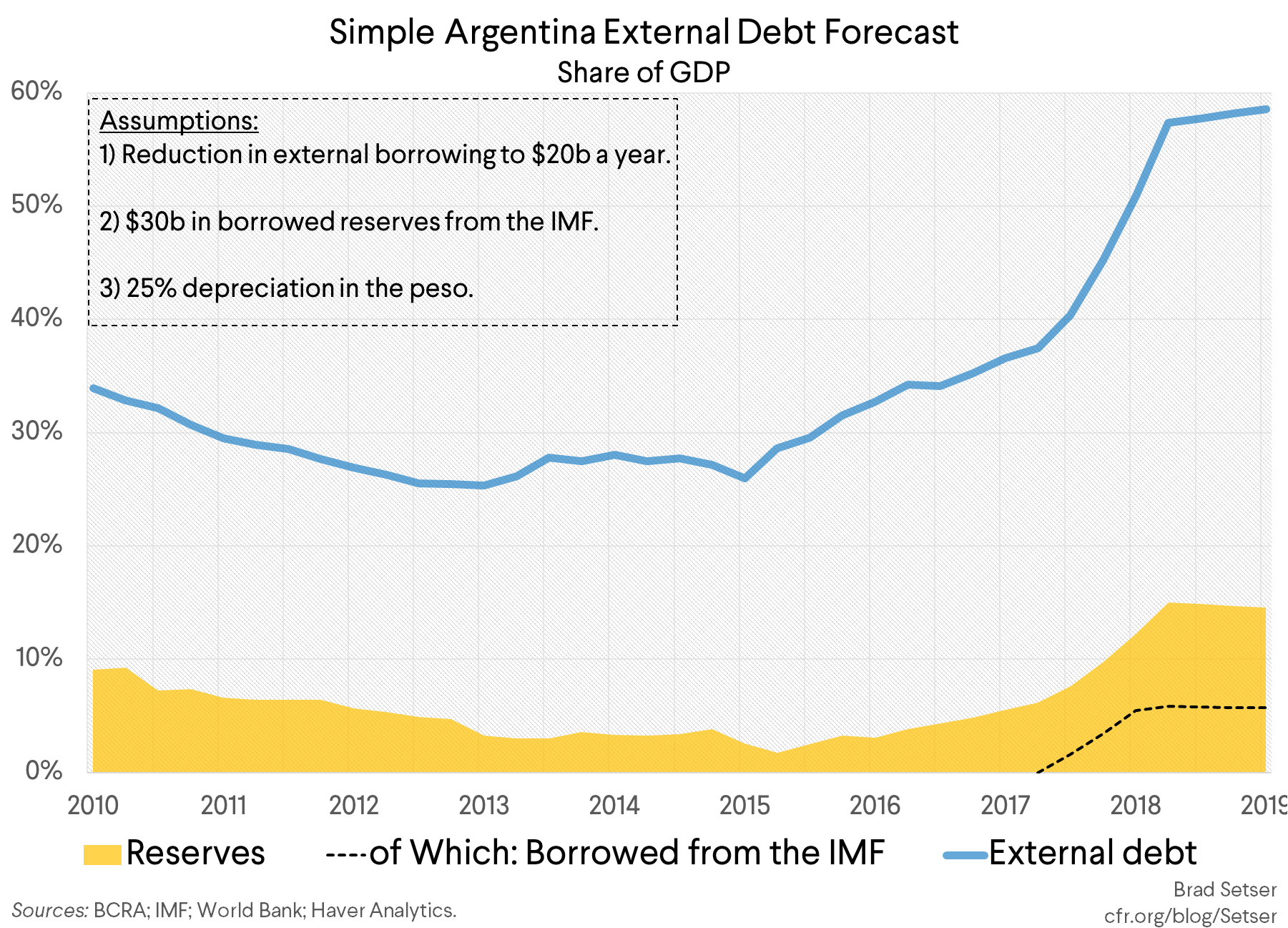

Argentina’s external debt isn’t really 35 percent of its GDP. That’s the ratio at an over-valued exchange rate. With a 25 percent depreciation, external debt rises to close to 50 percent of GDP (and Argentina now pays on average about 6 percent on its external bonds, — so interest payments aren’t small relative to Argentina’s export base). Exports would also obviously go up versus GDP if the peso depreciates, so the ratio of external debt and debt service to exports wouldn’t change).***

I did a quick estimate of what happens to Argentina’s debt to GDP path if:

- it reduces its external borrowing to $20 billion a year (likely by reducing its current account deficit, but it could come through a rise in foreign direct investment);

- it borrows $30 billion in reserves from the IMF (e.g. an IMF program) and;

- the peso depreciates by 25 percent (lowering GDP in dollar terms commensurately).

This is a bit of ballpark math—but hopefully it is a reasonable bit of ballpark math.**** Thanks to the need to borrow reserves, external debt to GDP rises to close 60 percent of GDP at the end of 2019, against exports of around 15 percent of post-depreciation GDP and reserves of around 15 percent of GDP.

A bad harvest, a large rise in the dollar (as U.S. treasury yields rise to pull in the funds the U.S. needs and prevent the economy from over-heating in the face of unneeded fiscal stimulus), or bad dynamics around the peso and the growing stock of short-term peso debt that Argentina needs to roll all could throw the needed adjustment off track.

Argentina needs enough foreign demand for its bills to allow the central bank to lower rates. But not so much that the inflow of funds bids the peso up and prevents adjustment in the current account.

Argentina went into its 2001 crisis with an external debt to GDP ratio of 60 percent and a current account deficit of around 3 percent. So Argentina is on a trajectory that will potentially get it close to quite problematic debt levels.

The main difference is that back in 2001 Argentina’s currency board—and its highly dollarized banking system (see the case study on Argentina here)—made depreciation impossible without a crisis. The fact that the peso now floats gives Argentina a chance to put its external debt on a more sustainable long-term trajectory without creating a domestic banking crisis or throwing the economy into deep recession.

But I do think that the Fund needs to look a bit beyond public debt when it thinks about an economy like Argentina. The combination of a low level of domestic savings and a low level of exports have long been Argentina’s Achilles heel.

*/ The exceptional access policy decision for cases in the grey zone: ”It would be appropriate for the Fund to grant exceptional access so long as the member also receives financing from other sources during the program on a scale and terms such that the policies implemented with program support and associated financing, although they may not restore projected debt sustainability with a high probability, improve debt sustainability and sufficiently enhance the safeguards for Fund resources … Directors noted that, in applying this more flexible standard in circumstances where debt is assessed to be sustainable but not with high probability, there would be a range of options that could meet the prescribed requirements. There would be no presumption that any particular option would apply. Rather, the choice would depend on the circumstances of the particular case … If the member has lost market access and private claims falling due during the program would constitute a significant drain on available resources, a reprofiling of existing claims would typically be appropriate …. In this context, the scope of debt to be reprofiled would be determined on a case-by-case basis, recognizing that it would not be advisable to reprofile a particular category of debt if the costs for the member of doing so—including risks to domestic financial stability—outweighed the potential benefits.” Not clear? Good. There should be a bit of flexibility. The staff paper behind the exceptional access policy decision can be found here [PDF].

**/ Though between the growing stock of central bank paper—Lebacs—and short-term domestic law dollar borrowing—Letes—Argentina also does have too much short-term debt.

***/ Compared to the Fund, I obviously put more weight on external debt relative to exports than public debt to GDP. To make this difference concrete, think of the difference between Japan—a high domestic public debt country that is a net creditor to the world, and Argentina. Japan is a net creditor to the world and its government’s solvency improves with a yen depreciation (as Japan’s government has lots of foreign currency-denominated assets, and its debts are all in yen). Argentina is a net borrower from the world, and primarily in foreign currency, so its solvency deteriorates when the peso depreciates. Countries like Russia and Brazil are more resilient because their governments are net long in foreign currency, as their central banks have more reserves than the government (and the big state firms) have foreign currency debt.

****/ I didn’t model peso and foreign currency debt separately, so I implicitly assumed that foreign investors would make up any losses from the peso’s depreciation through high interest rates. As most of the peso debt seems short-term, that is likely to be close to true. I also would recommend the external debt sustainability analysis in the IMF’s latest staff report (buried a bit in Annex I, which starts on p. 41); the real depreciation shock modeled on p. 48 scares me, but in the model it comes after several more years of current account deficits).