The Case for a Significant German Stimulus Is Now Overwhelming

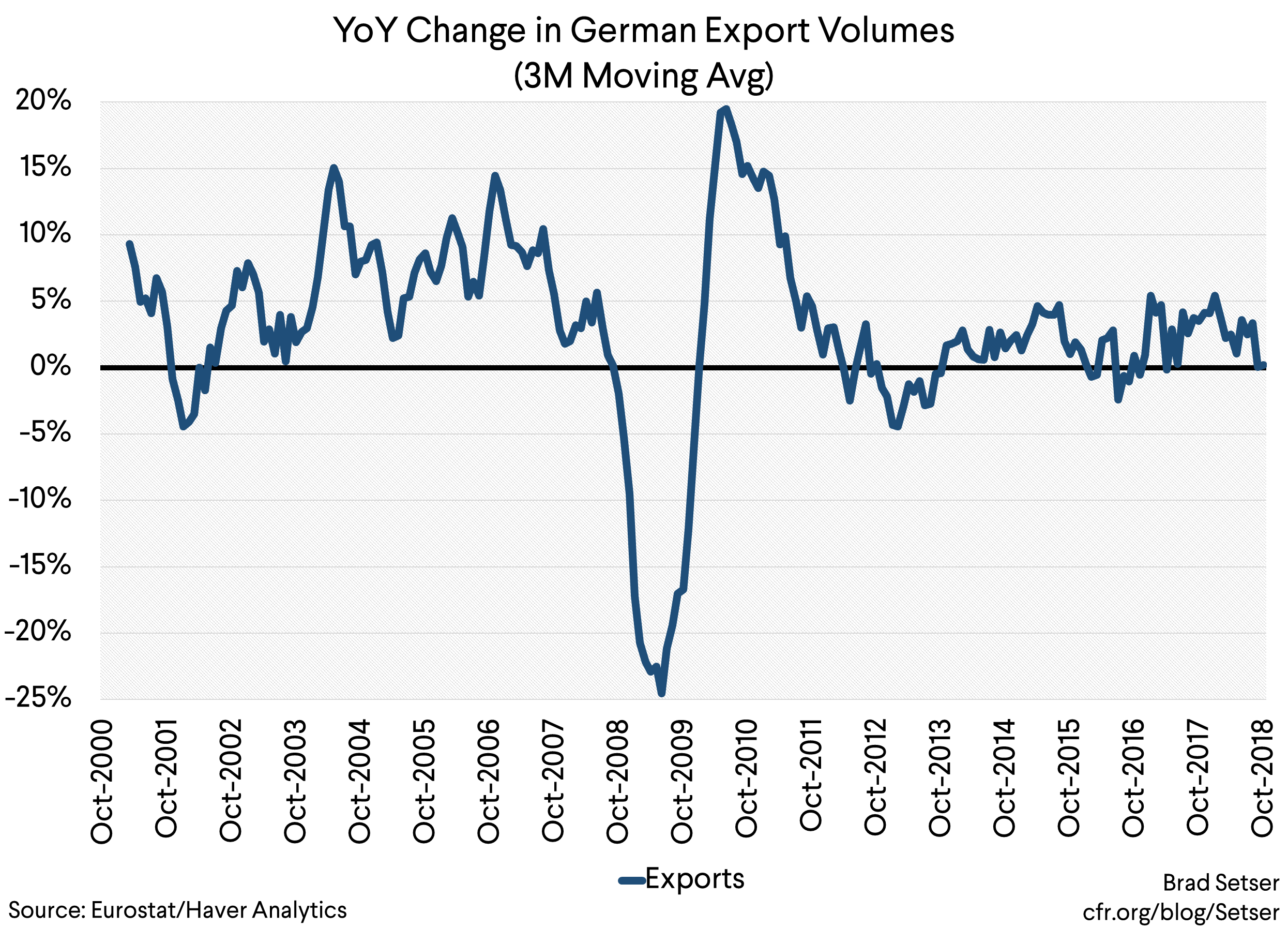

Germany’s economy is slowing by more than can easily be explained by the obvious slowdown in exports (see Gavyn Davies, who, to be fair, believes there were some one-off drags to German growth in h2 2018).

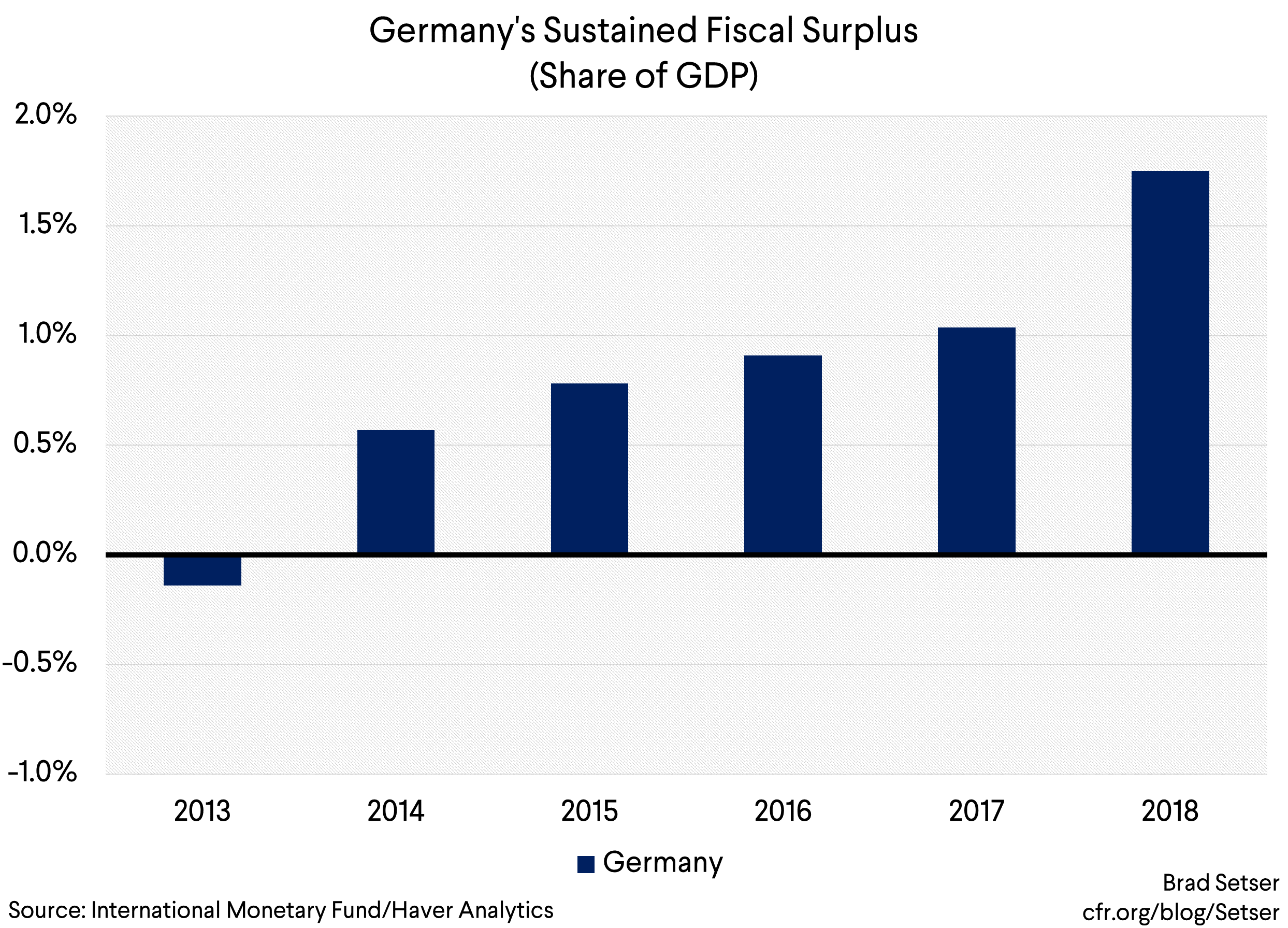

Germany ended 2018 with a fiscal surplus of something like 1.75 percent of its GDP.

Germany has under-invested in public infrastructure for years. See Alexander Roth and Guntram Wolff of Bruegel: “since the 2000s, Germany has exhibited very low and even negative public fixed net capital formation ratios—below most other European countries.”

And President Trump has a point when he criticizes Germany’s failure to meet its NATO defense spending commitments.

Germany’s coalition agreement implies a modest stimulus this year. But Germany has a history of delivering less stimulus than many expect. The IMF has been forecasting Germany’s fiscal surplus would fall for many years now, yet the surplus has kept on rising.*

This time may be different, but, well, Germany needs to prove it…and frankly it should throw in a bit of extra stimulus now just to make sure.

The German finance ministry’s worries that Germany’s scope for stimulus is limited—because it might possibly run a deficit of well under a percent of GDP in 2023—just aren’t that convincing. Shahin Vallee has noted that Germany’s finance ministry has a recent history of systemically underestimating revenues, by something like half a point a year.**

In 2017 and 2018 the argument that Germany needed to stimulate essentially rested on the need to move toward a more balanced global economy, and the value additional German stimulus would provide to its trading partners. Demand growth inside Germany was solid, and the German economy was humming off the combination of okay domestic demand growth and solid external demand. The hope was that a bit of stimulus (or a less restrictive fiscal policy if you prefer, as Germany could provide a positive impulse to demand while still running a budget surplus) would spill over to Germany’s partners through higher German imports. And maybe help to support ongoing wage growth in Germany too.

Now, well, Germany itself has clearly slowed, and its economy could use a boost.

A sharp deceleration in growth caused in part by a weakening of external demand provides an opportunity for Germany to, more or less seamlessly, bring its own economy into better balance by strengthening the economy’s internal motor, and thus naturally starting to replace some of the outsized role external demand has played in keeping Germany’s economy humming.

And there is basically no downside.

The stimulus could be financed without any borrowing—Germany just needs to save less.

If Germany did need to borrow a bit, it could do so at a negative real interest rate. Ten year bunds have a yield of 10 basis points right now; even if the ECB consistently misses its inflation target that would still imply a real rate of negative one.

Inflation is currently low.

A stimulus could put Germany’s massive excess savings to work at home, and thus reduce the risks that German savers are now taking abroad.

Keeping the labor market relatively tight would help German wages continue to grow (real wage growth hasn’t been that strong in 17 and 18, judging from the FT’s chart), helping to support demand throughout the euro area—and right now Germany’s European partners could use a bit of a lift. A relatively tight German labor market would also help speed up the integration of the 2015 migration wave.

Stronger domestic demand growth would provide a bit of insurance against a disruptive Brexit.

What’s not to like?

(By the way, the same basic argument applies to several other “twin surplus” countries in Europe, including the Netherlands. Dutch growth also decelerated in the third quarter, and the Dutch don’t really need to continue to run sizable fiscal surpluses given their low debt levels.)

* The IMF noted in its 2017 Article IV (emphasis added) “Fiscal policy was again neutral in 2016, as the government posted its third consecutive yearly surplus. The general government balance climbed to 0.8 percent of GDP—almost a full percentage point higher than planned—, while the structural balance stood at 0.7 percent.” The IMF went on to note “In fact, fiscal plans proved overly conservative through the whole post-crisis period, mostly because tax revenue consistently exceeded official estimates.” Yet even after noting this history, the IMF still forecast a fall in Germany’s surplus in 2017...a fall which failed to materialize (see the chart above).

** I thought the FT jumped the gun a bit in its claim that the euro area has now turned toward stimulus. The biggest stimulus in the FT’s chart appears to come from Italy, and, well, the Commission didn’t go along with Italy’s fiscal plans. The expansion of over a percentage point of GDP appears to come from an October document (the November numbers were similar), and it corresponds with a headline fiscal deficit of around 2.9 percent of Italy’s GDP. The final compromise with Italy authorized a fiscal deficit of about 2 percent of GDP. Germany’s coalition agreement makes some overall stimulus for the euro area likely given that France clearly isn’t going to consolidate in 2019. But, as I noted in the previous footnote, the German finance ministry has a history of underestimating revenues and that has led the Commission to join the Fund in underestimating the growth in Germany’s surplus in the last few years. And, well, the aggregate result of the Commission’s projections (with the large fiscal relaxation in Italy that was not approved) was a rise in the headline fiscal deficit for the euro area from 0.6 pp of GDP to 0.8 pp of GDP. And with German borrowing costs still falling, a 0.4 pp primary expansion in Germany implies something like a 0.3 pp change in the headline fiscal balance, so a general government surplus that would still be close to 1.5 pp of German GDP...