China Still Wants To Import Commodities, Not Manufactures (Judging From The “Early Harvest” Trade Deal)

China tends to import natural resources—oil, iron ore, soybeans and the like. Now that China has a large industrial economy, it doesn’t have much choice: China wasn’t blessed with a ton of oil or gas, or a ton of arable land (relative to its population).

And China tends to export a lot of manufactures relative to its own imports.

It isn’t just that the cargo ships that sail across the Pacific often struggle to find cargoes for the return trip—the trains that have been set up to send China’s manufactures to Europe as part of China’s highly touted One Belt and One Road Initiative also often return empty. Jörg Wuttke wrote in the Financial Times last week:

“The planned rail link between central China and Europe, which is undergoing trials, highlights the challenges: five trains full of cargo leave Chongqing for Germany every week, but only one full train returns.”

Wuttke’s anecdote captures something important about the nature of manufactured trade with China.

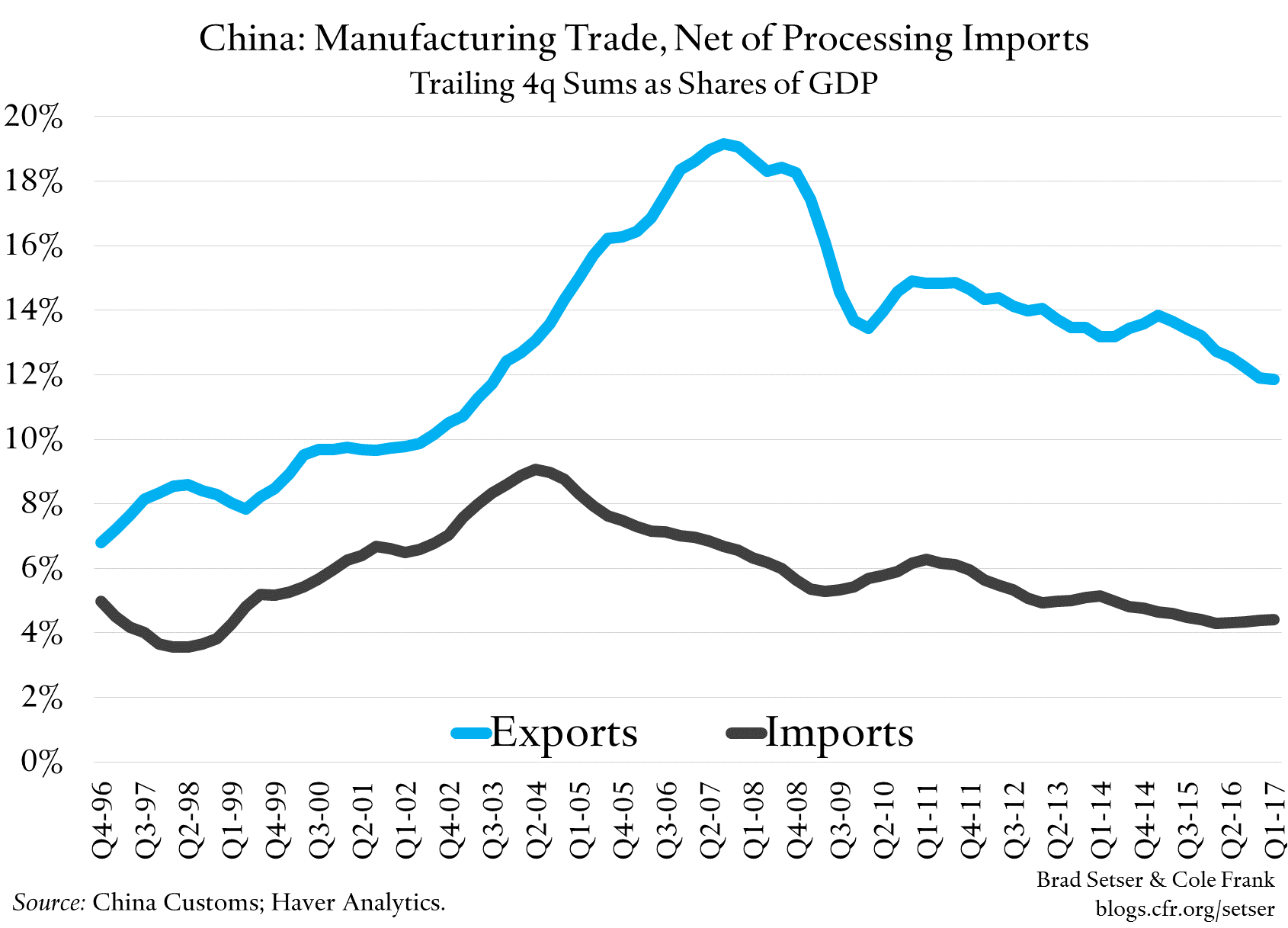

If you net out imported components for reexport, China really doesn’t import many manufactures: manufactured exports are about 12 percent of its GDP, and imports—net of processing imports—are just over 4 percent of GDP, leaving China with a large surplus in manufacturing trade. Exports as a share of GDP have come down after the crisis, but so too have China’s imports of manufactures for its own use.

Some imbalance here is normal: China naturally will trade its manufactures for the world’s commodities, and run a manufacturing surplus.

But China’s the size of China’s manufacturing surplus has created something new, given the size of China’s economy.

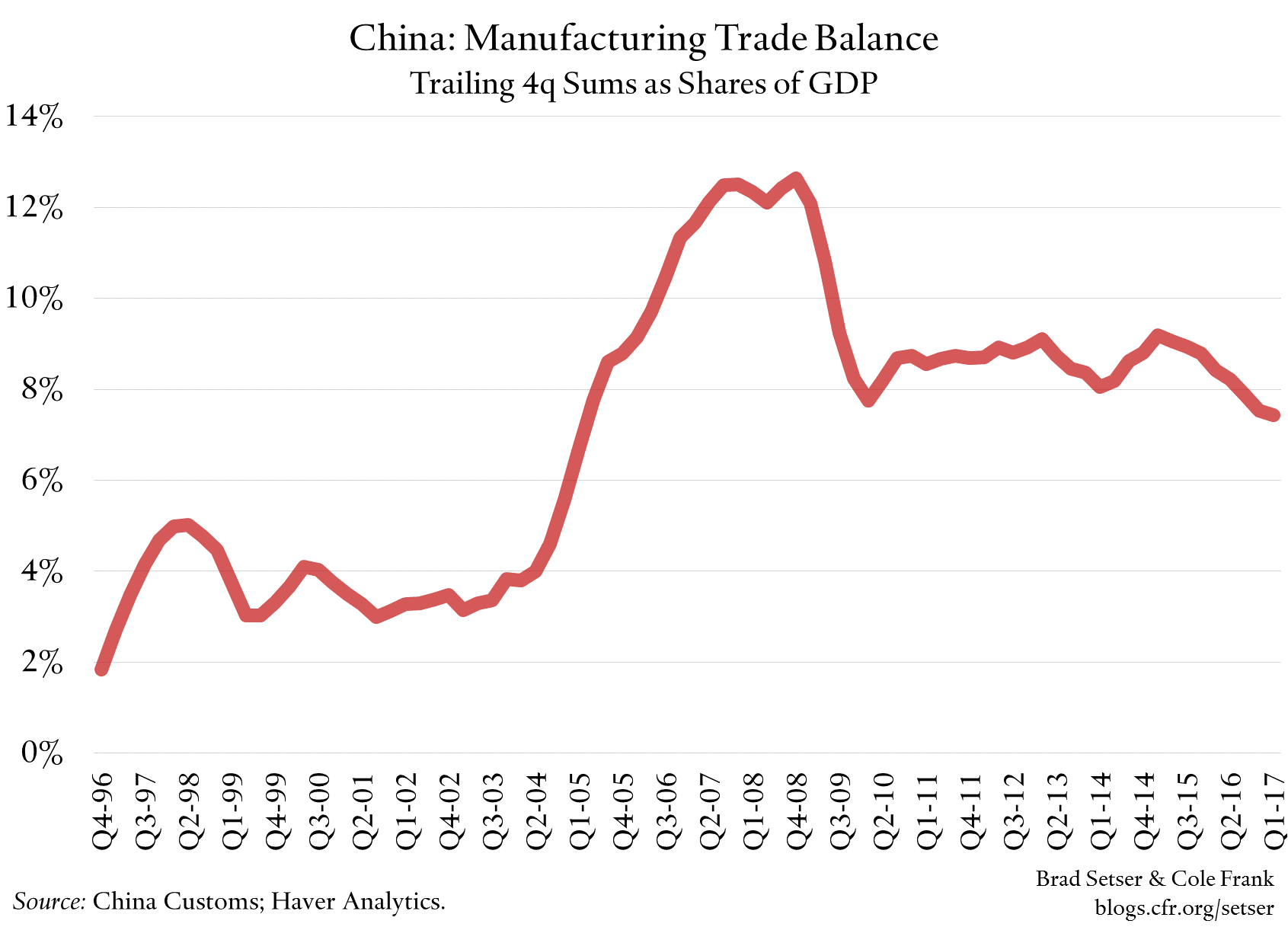

China’s manufacturing surplus topped 10 percent of China’s GDP at its peak before the crisis—so it has come down a bit. But its manufacturing surplus is still large. Since 2009, it has ranged from about 7.5 percent of China’s GDP to around 9 percent of its GDP (thanks to China’s recent stimulus it is at the low end of that range).

Most of the fall in China’s reported current account surplus after the crisis thus has not come from a fall in its surplus in manufacturing. Rather, much of the change in the overall balance reflects a swing in the income balance (better measurement of reinvested earnings, and a fall in interest income on reserves), from a rising commodity import bill and, recently, from rising tourism imports (excluding tourism, China isn’t a big importer of services).

Bilateral number can mislead—so if you want to avoid the next bit, feel free.

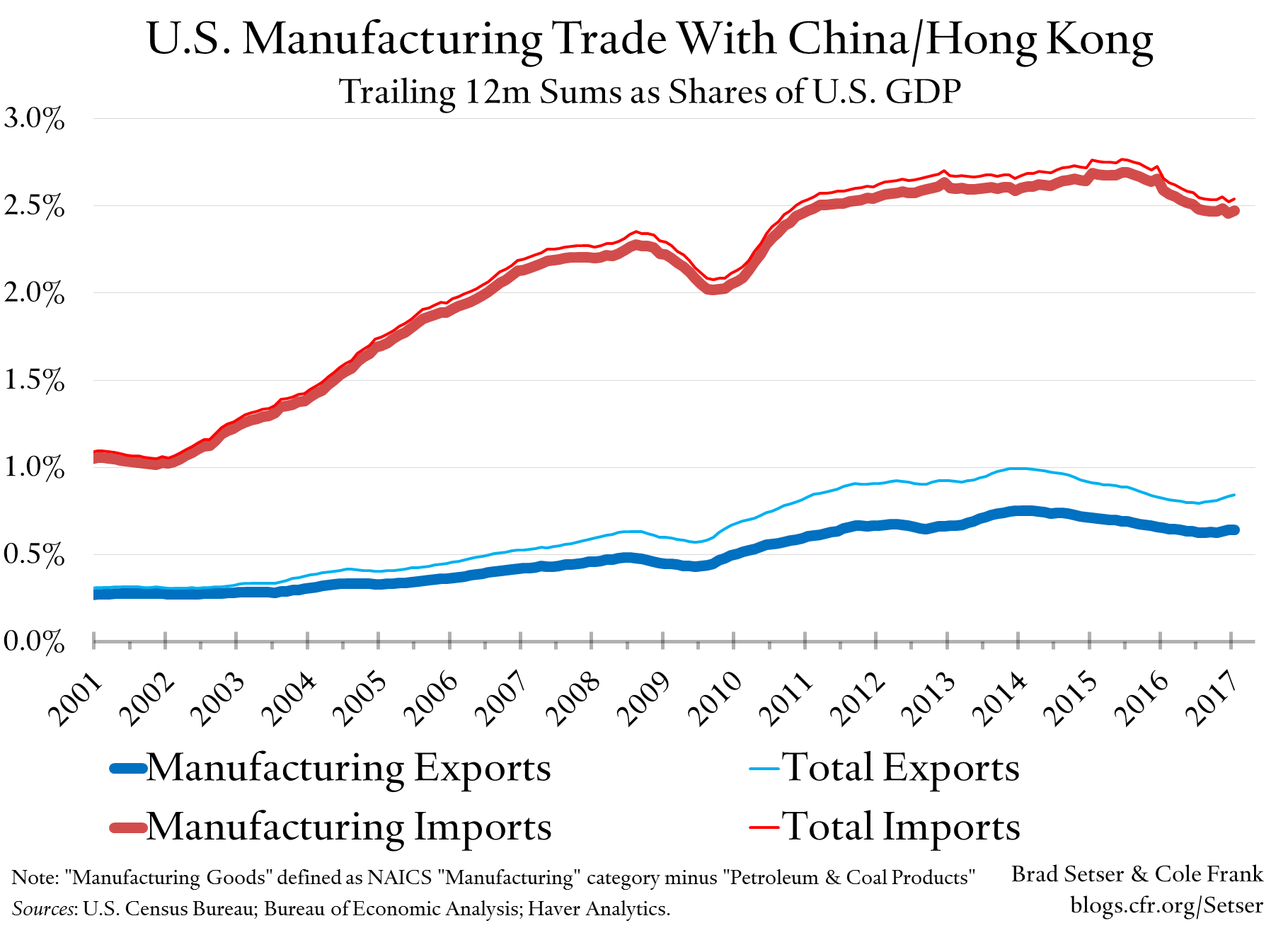

U.S. manufactured imports from China are roughly four times as big as U.S. manufactured exports to China (counting exports to Hong Kong, and using the NAICS definition of manufacturing, which includes petrochemicals). Adjust roughly for value added, and the discrepancy falls to maybe 3 to 1—as China’s exports have a bit more imported content than U.S. exports (OECD numbers here).

In this case, I think the bilateral numbers illustrate something that is also globally true: China exports about three times as many manufactures as it imports, once imported components are netted out—its pattern of trade with the U.S. is actually fairly typical. And the U.S. also imports far more manufactures than it exports.

Changing this basic pattern will be hard. On the U.S. side, tax cuts that push up the budget deficit won’t help, especially if budget deficits raise interest rates and push the dollar up. And for all of China’s new pro-trade rhetoric, China remains committed to developing an indigenous aircraft industry, an indigenous semiconductor industry, and a stronger medical equipment industry. In a host of sectors where China is now an importer, it wants to become an exporter: see Keith Bradsher’s reporting in the New York Times.

The new, highly touted “early harvest” deal with China doesn’t try to change this pattern. It focuses on commodity exports (beef, natural gas) and increasing the ability of U.S. financial services firms to compete in China—not on opening new opportunities to export manufactures to China. That in part is why Dan DiMicco of Nucor is not a fan of the deal: “This is disappointing on many levels. We are rewarding China before stopping their massive trade cheating.”

China’s willingness to trade beef for poultry isn’t new, or a surprise—in fact China had already agreed in principle to resume beef imports last year. In some ways, the most interesting bit of the agreement is the hint of a future agreement to increase U.S. LNG exports to China. The details aren’t all that clear. The announced deal didn’t actually do more than encourage Chinese energy companies to buy U.S. LNG: “The United States welcomes China, as well as any of our trading partners, to receive imports of LNG from the United States. .... Companies from China may proceed at any time to negotiate all types of contractual arrangement with U.S. LNG exporters, including long-term contracts, subject to the commercial considerations of the parties.”

As China already buys some LNG from U.S. liquefaction facilities in the spot market, the real impact of this will only come if China commits to a long-term contract to take up a steady stream of LNG.

There are several additional points to make here.

First, China doesn’t actually need to buy LNG to meets its domestic energy needs. China has no shortage of domestic coal, and its domestic coal is cheaper than imported gas. But gas is cleaner—and less carbon intensive. Now that global traded gas prices are down a bit, the cost is probably a bit easier to swallow.

Second, Asia actually doesn’t need much U.S. gas right now. The Asian market is currently well supplied—thanks to large amounts of Australian LNG capacity that are now coming on line. Gas in Asia has traditionally been expensive because Qatar used its market power (Qatar has a ton of low-cost gas—it just didn’t want to flood the market) to keep prices high. But with lower oil prices and new competition from East Africa and Australia, Asian prices have come down. This is a problem for the U.S. LNG export story—the liquefaction is actually quite costly, and it isn’t clear that the current price differential is high enough to support a major expansion of U.S. gas exports. Clifford Krauss of the New York Times recently reported that some investment groups have all the permits they need to build more LNG capacity, but haven’t chosen to go forward because they haven’t found a buyer for the gas:

I am not sure that China is committed to buy at any price. Nor is it clear that the U.S. is committed to allow Chinese investors to take an equity stake in a LNG liquefaction facility—a part of China’s preferred deal structure (see, for example, China’s equity stake in the Yamal LNG facility in Siberia).

Third, the implications of higher U.S. gas exports on the broader U.S. economy are ambiguous. The construction of a terminal no doubt generates demand for steel and for a range of high-end components, and raises demand for domestically produced gas. But exports also tend to pull up the domestic price of gas, and most Americans are consumers of gas (and of energy more generally) not producers. Exports thus make the average household worse off—even as they generate concentrated gains for the owners of gas fields, workers in the natural gas sector, and those workers who supply components to the liquefaction facilities. And to a degree exports of gas also trade off with exports of energy-intensive manufactures.

The scale of the impact of higher exports on domestic prices is likely modest in the U.S. (it has been significant in Australia). U.S. gas supply now looks to be relatively elastic, so it won’t take much of a rise in price to induce the additional drilling needed to meet higher export demand. Especially as it still isn’t clear to me that China is willing to commit to long-term supply contracts at a price that would make investment in additional LNG export capacity economically attractive on a scale that would make a material impact on the market.

But I do wonder—like Rory McFarquhar—whether the U.S. could have used China’s desire for a special relationship in gas as a source of leverage to try to get a bit more out of the negotiations in other areas, areas where China is less ready to give than in beef. LNG is as much a Chinese ask as a U.S. ask, and, well, the U.S. had a set of realistic non-Chinese alternatives. Using the gas at home as part of a domestic manufacturing strategy, for example. Or expanding pipeline exports to Mexico as part of a stronger energy partnership in NAFTA, or prioritizing LNG sales to allies in Europe and Asia, like Japan ...

Bonus charts:

Chinese manufacturing trade surplus (goods trade net of primary products), as a share of China’s GDP:

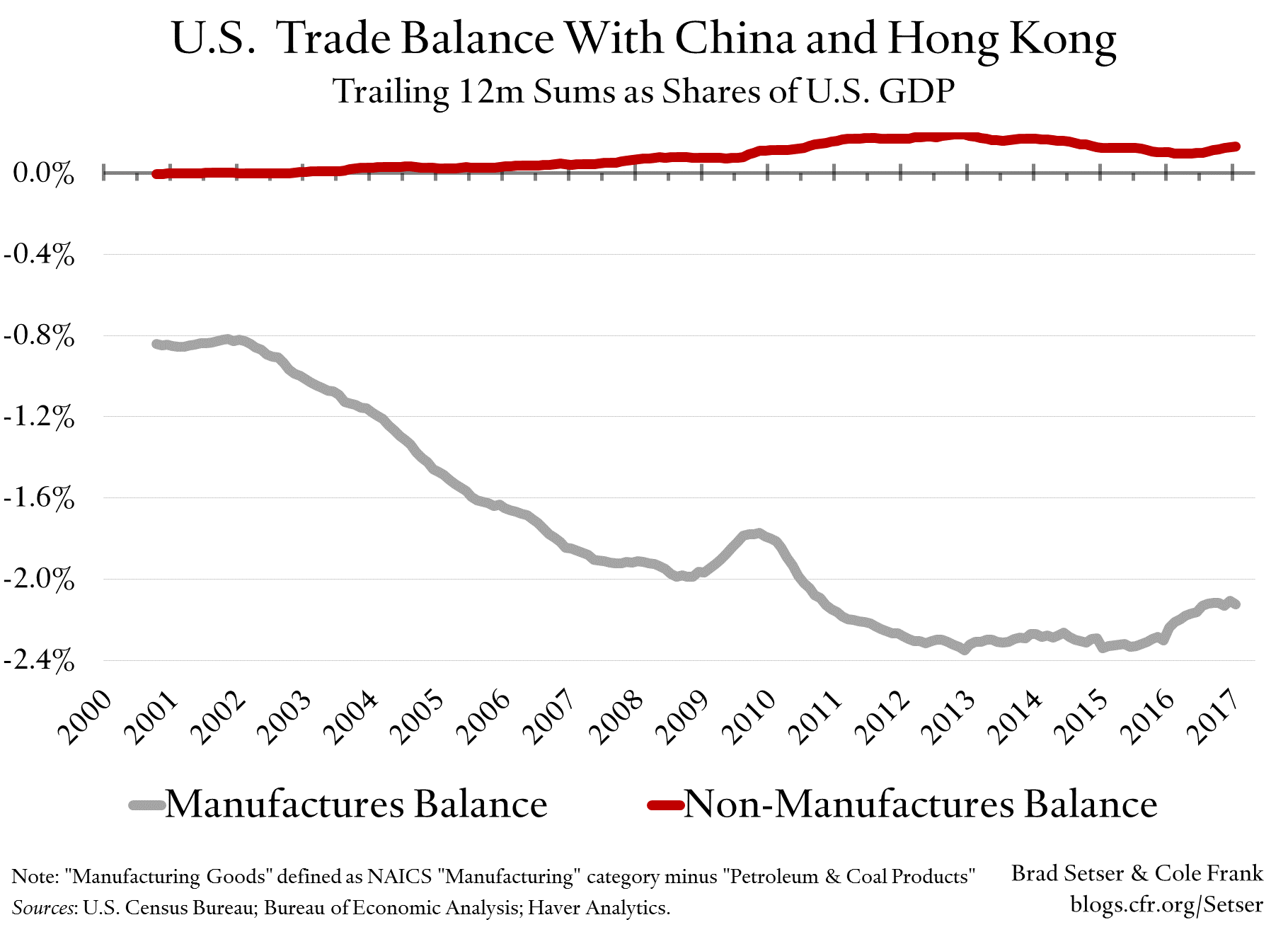

And the U.S. manufacturing and non-manufacturing trade balance with China and Hong Kong, as a share of U.S. GDP:

Both sides of the imbalance fell a bit in 2016, as U.S. consumer goods imports were weak and China’s stimulus pulled in imports. I though have questions about the sustainability though of both legs of the adjustment -- as U.S. imports seem likely to pick up after an inventory correction and China’s weaker real exchange rate should support China’s exports going forward while China is pulling back on its stimulus.