The Common Framework and Its Discontents

The IMF’s debt sustainability assessments for Zambia and Sri Lanka differ so greatly that it’s hard to understand how both emerged from the same institution. Case-by-case only works with some consistency across cases.

The Common Framework, developed by the G-20 back in the fall of 2020, hasn’t provided a pathway toward the quick restoration of debt sustainability in obviously distressed cases. The need for financing assurances from China for the International Monetary Fund (IMF) to lend has led to long delays in the provision of IMF financing. And so far, the Common Framework hasn’t even provided a structure for starting to negotiate financial terms in any of the important test cases—most notably, Zambia.

Yet the proposed reforms often seem underwhelming. Faster timetables are important, but that is making the existing architecture work a bit better—not dramatic reform. I am all in favor of allowing private creditors to restructure ahead of bilateral creditors—but that requires that everyone agree upfront to strict debt targets that are actually met to assure that the restructuring terms offered to different groups of creditors are fair. Speed would trade off with flexibility. Restructuring sovereign bonds ahead of bilateral creditors (bilateral creditors are other governments who have lent a distressed country money) isn’t an architectural change on the par with, say, introducing new “aggregation” provisions into sovereign bond contracts, or even pulling a subset of Chinese policy bank claims into the process for restructuring “official bilateral” claims.

The core problem right now is simple, but hard to solve.

No framework for coordination among official creditors can work if official creditors don’t have enough in common to work together. The “Common Framework” exists in name only.

Best that I can tell, the official bilateral creditors committees composed of both the traditional Paris Club creditors and China’s Export-Import Bank (representing China’s government) haven’t been able to make substantive progress on actual restructuring terms when real debt relief is needed.

The main source of difficulty is clear: Chinese official creditors are acting like old-fashioned commercial creditors and want to maintain both the par value of their claim and a coupon that covers their cost of funds. LIBOR plus a couple of hundred basis points apparently remains their goal.* Most other official bilateral creditors, together with the IMF and the World Bank, long ago accepted that claims on very low-income countries should carry concessional rates.

The most plausible explanation for the currently stalled restructuring process thus is not a new financial cold war, but rather a basic dispute between China and other official creditors over the financial terms of several specific restructuring cases.

However, one of China’s current demands does risk a true fracture the multilateral system: China’s insistence that the World Bank and the other multilateral development banks (MDBs) take a haircut along side bilateral and commercial creditors.

That particular demand either reflects an ideological view that Chinese policy lenders shouldn’t be treated differently than the MDBs, or a simple effort to limit the losses the policy banks face by expanding the scope of the debt restructuring.

Whatever its motive, it stems from a superficial analysis of the debt burden generated by the current stock of MDB claims on low-income countries.** MDB lending after HIPC debt reduction has been done in a financially responsible way. The current debt overhang in a set of low-income countries stems from “bilateral” lending from new creditors (mostly China) together with commercial borrowing (from China and the bond market).***

Securing a return to debt sustainability for the current key cases thus requires finding the basis for an agreement with China’s policy banks, its state commercial banks, and commercial bond holders that provides a clear path back to resumption of payments and leaves the country with a sustainable debt structure. The financial details matter. The new debt restructuring architecture is more likely to emerge out of case law and actual practice than from more abstract discussion in forums like the IMF’s new Sovereign Debt Roundtable.

I fear that the IMF’s technical work has made it more difficult than it should be to reach an agreement that restores debt sustainability in both Zambia (the most significant current Common Framework case) and Sri Lanka (the most important case that lies just outside the Common Framework).

In Zambia, the IMF is insisting (correctly) on real concession from Zambia’s external creditors, but has calculated the cash flows in a way that reserves almost all debt servicing capacity for foreign holders of Zambia’s local currency bonds—leaving very little for either bond holders or the Chinese banks. In Sri Lanka, the IMF appears to have the made the opposite error: it hasn’t set out debt targets that are strong enough to assure a return to debt sustainability, presumably in an effort to avoid confrontation with China and other “new” bilateral creditors. This creates the risk that Sri Lanka will end up with more debt than it can realistically pay.

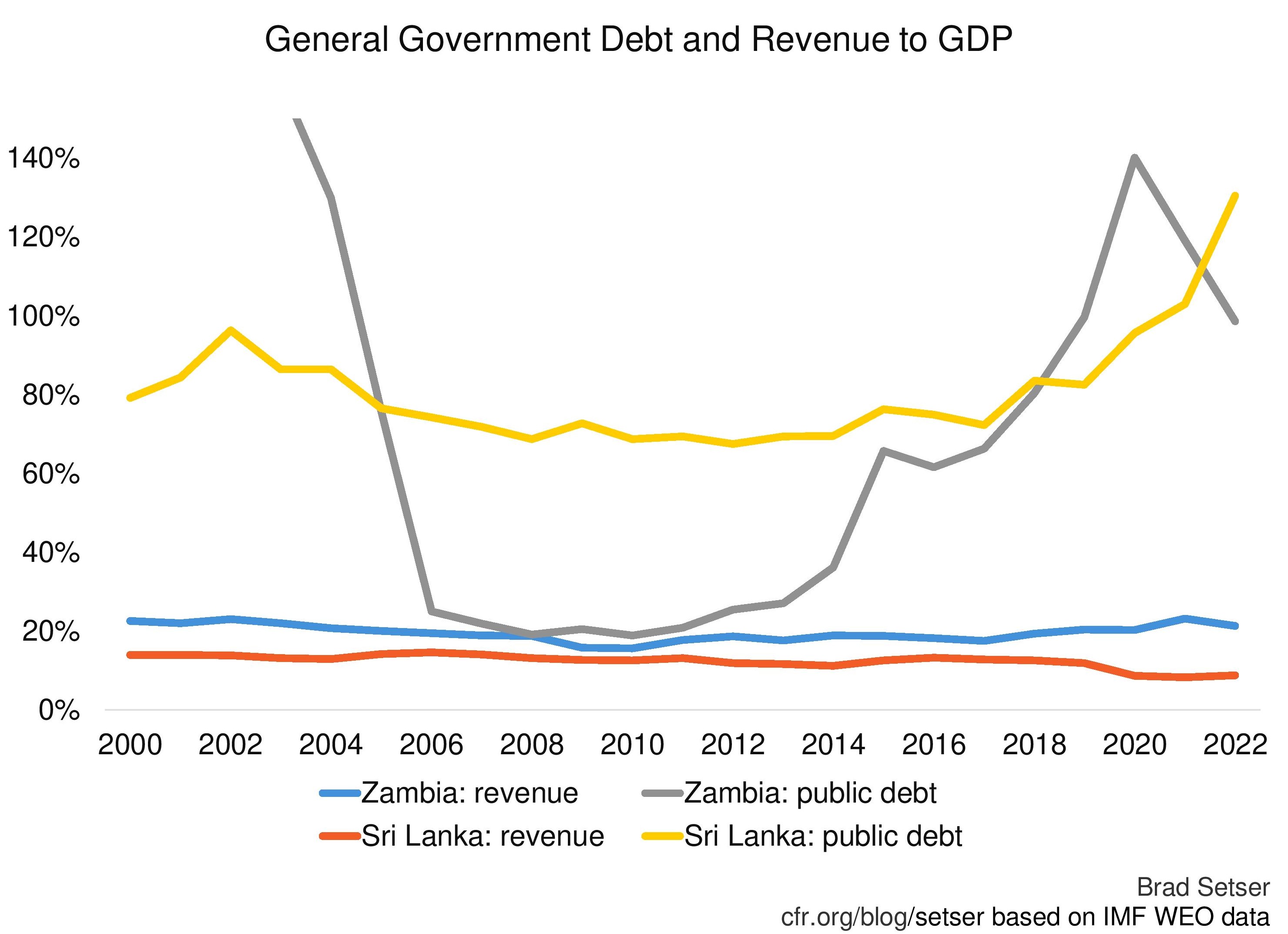

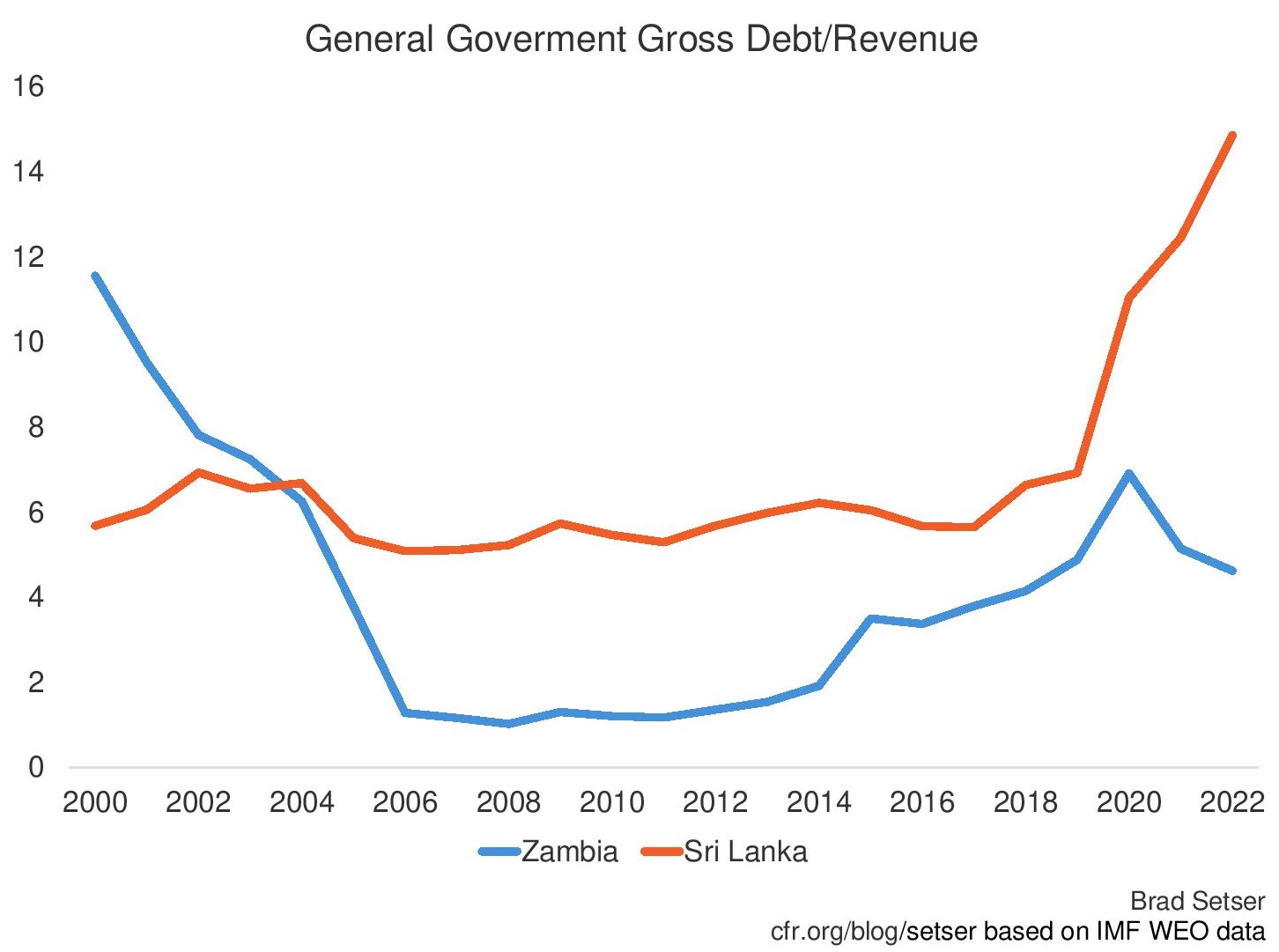

While Zambia is somewhat poorer than Sri Lanka, both countries have high levels of fiscal debt relative to revenue—and significant stocks of public and publicly guaranteed external debt. This fundamental similarity makes the differences in the IMF’s debt targets for the two countries hard to justify analytically. Although, they clearly reflect the fact that Zambia’s program was designed around IMF’s framework for debt sustainability in low-income countries, and Sri Lanka’s program was anchored by the (very different) framework for assessing the debt sustainability of market access countries.

Zambia

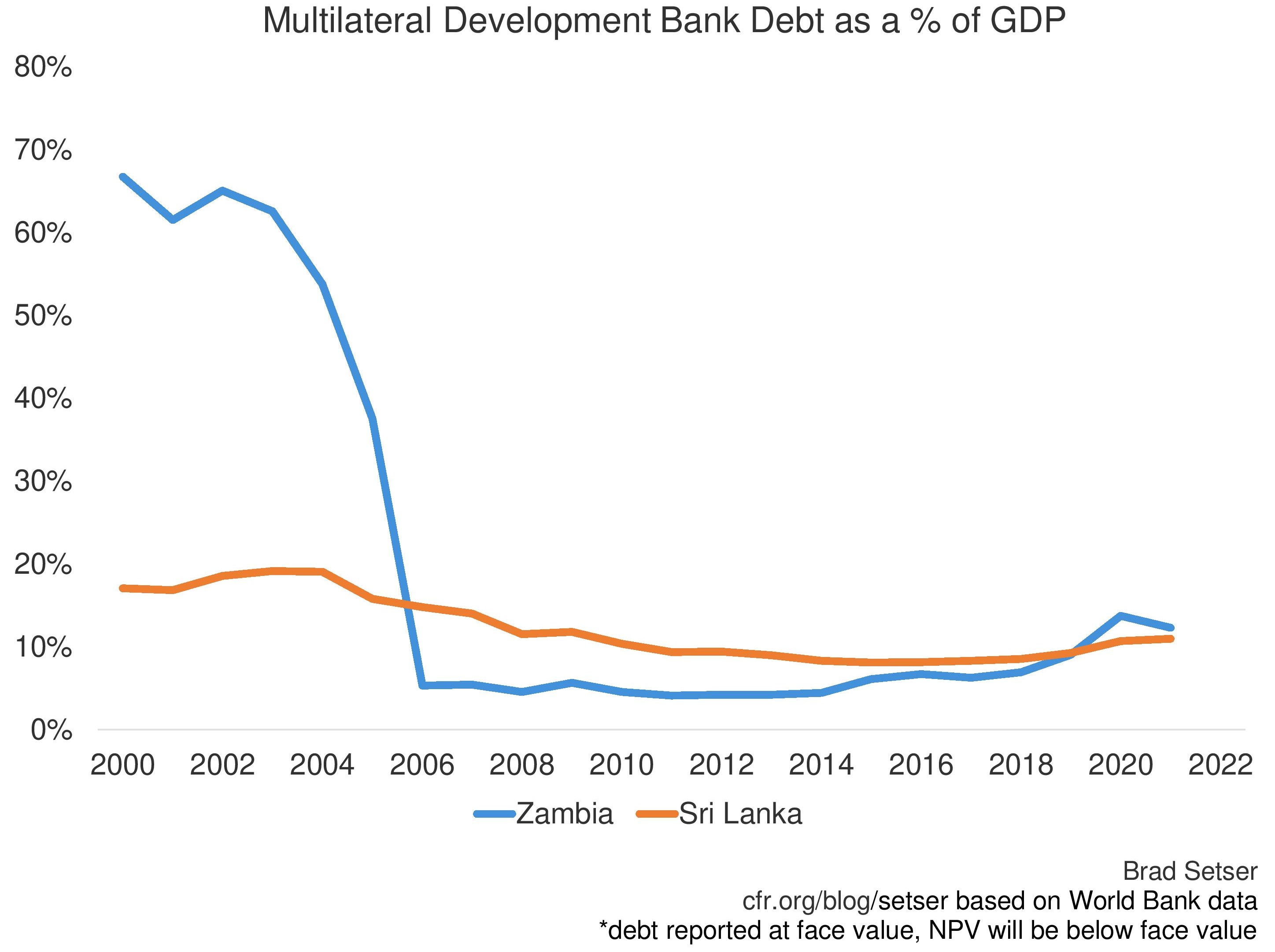

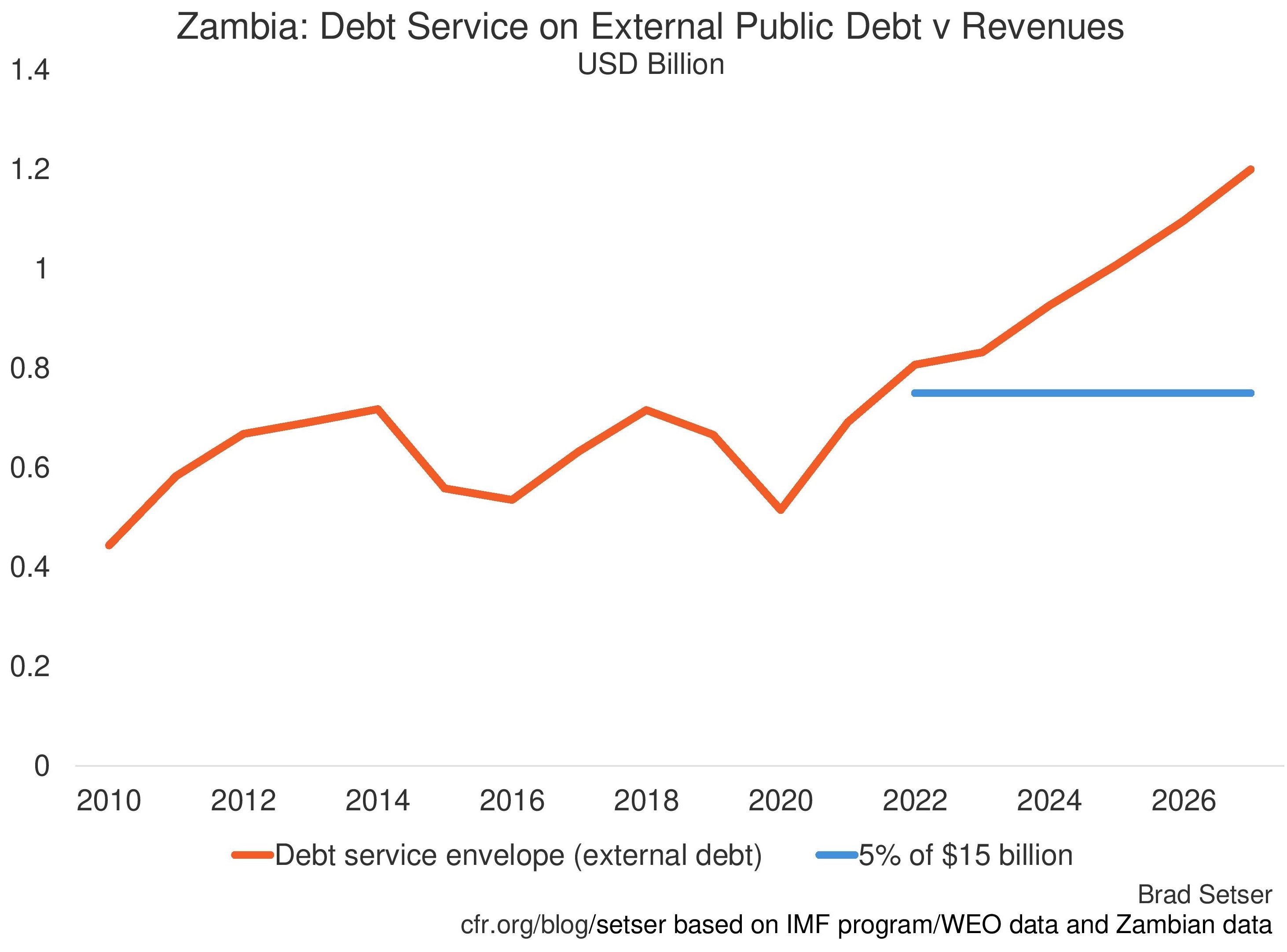

Foreign creditors now have about $20 billion in financial claims on Zambia. The IMF wants the “net present value” (NPV) of these foreign claims on Zambia to be reduced to around $15 billion. The $2.6 billion in MDB claims (with an NPV of $1.46 billion; see Zambia’s debt disclosure) on Zambia are excluded from a formal restructuring, as are around $3.2 billion in foreign hold local currency bonds and about $1.5 billion in payment arrears. The result is that the NPV of the remaining $14 billion (face value) in external claims—including at least $6 billion in claims from Chinese bilateral creditors—needs to be reduced to around $7 billion, or by about 50% (see Zambia’s investor presentation, p. 11-14).

China has complained vociferously about the exclusion of the MDBs from the restructuring, presumably in part because of concern that protecting the MDBs‘ preferred creditor status implies larger losses for China’s own policy lenders.

But these complaints clearly lack technical merit.

The MDBs‘ loans to Zambia are already on highly concessional terms, with an average coupon of 1% on roughly $2.5 billion of claims, or annual interest payments of only $25 million.

That is nothing—the IMF estimates Zambia’s sustainable debt service capacity is about $1 billion a year. It simply doesn’t significantly impact the calculations of debt service available for other creditors.

The MDBs will also provide financing going forward at concessional terms, meaning at the 1% or less. Their lending helps rather than hurts Zambia’s future financial position. And by helping to support Zambia’s recovery without generating a significant debt burden, MDB lending actually makes it easier for Zambia to repay the claims of all creditors.

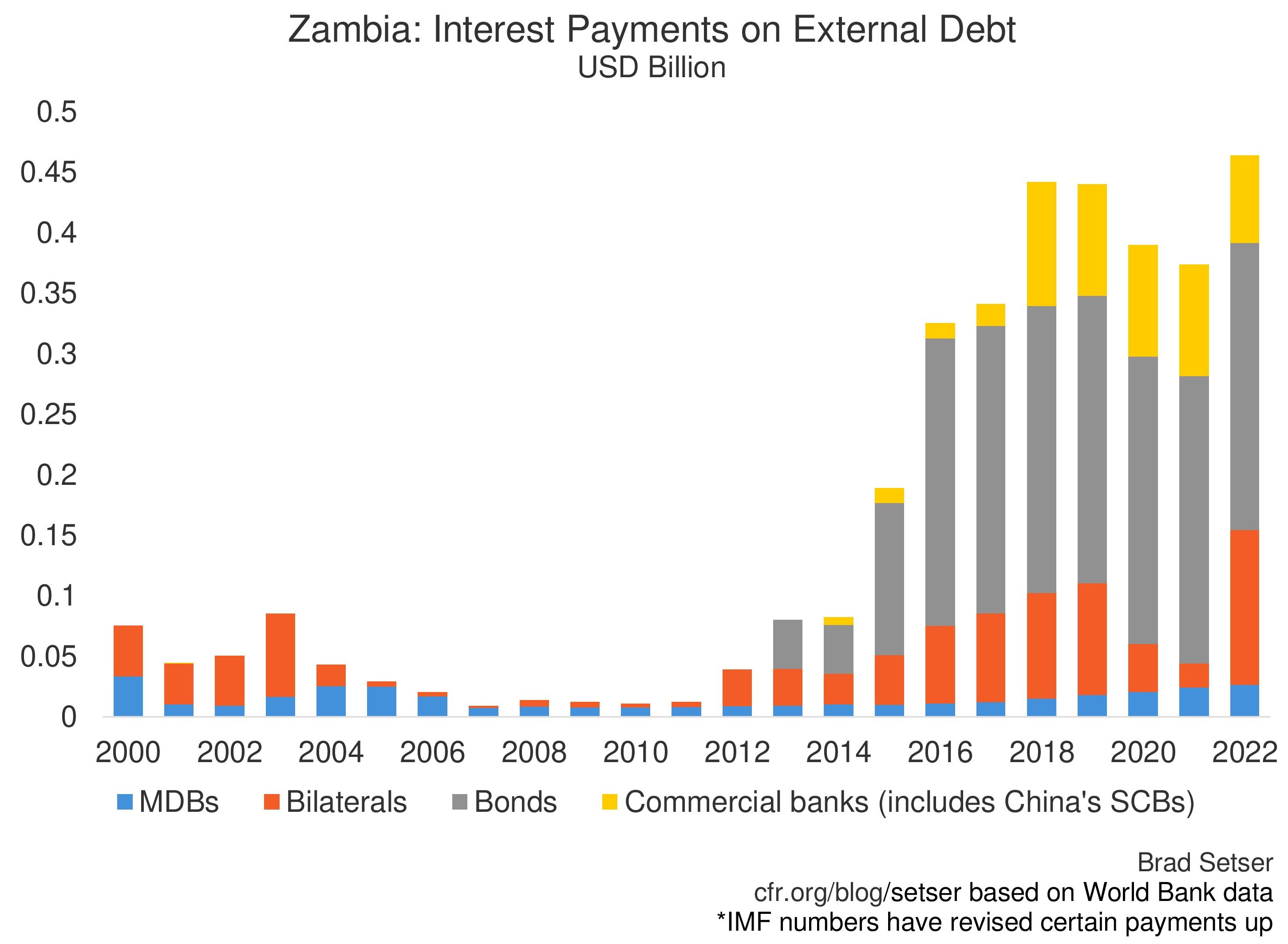

(Note: the dip in bilateral debt service in 2020 and 2021 was the result of China Exim’s participation in the Debt Service Suspension Initiative; the underlying path of payments is better captured in the numbers for 2020 and 2022. Zambia’s latest debt service tables also include more interest payments on guaranteed state enterprise debt than appears in the World Bank’s formal data, with total interest payments to bilateral and commercial banks topping the $240 million owed to the Eurobonds in 2022. See p.7 )

There is an easy way to demonstrate this.

If China’s policy lenders were willing to accept the same terms in the restructuring as the MDBs already have on their existing lending, China’s $6 billion in recognized bilateral exposure to Zambia would not be a problem. A 1% coupon would imply only $60 million of annual interest payments, a sum that Zambia could easily afford. Zambia’s only real financial problem then would be the 8% coupon on its $3 billion in outstanding bonds—a sum that is actually over $3.5 billion now due to two plus years of missed coupon payments.****

China’s push to restructure the debt of the MDBs is thus both politically toxic and financially unwarranted.

It has also diverted attention away what is actually a real problem: the treatment of Zambia’s roughly $3 billion in foreign held, local law, local currency debt in the IMF’s debt math.

A bit of background: the IMF-World Bank joint debt sustainability targets for low-income countries were designed for countries with lots of external hard currency debt, not countries with lots of external local currency debt. And since domestic debt typically has a very different maturity profile than external foreign currency debt, foreign holdings of local currency bonds muck around with standard debt service metrics for low-income countries.

It is easiest to illustrate this point with real numbers from Zambia:

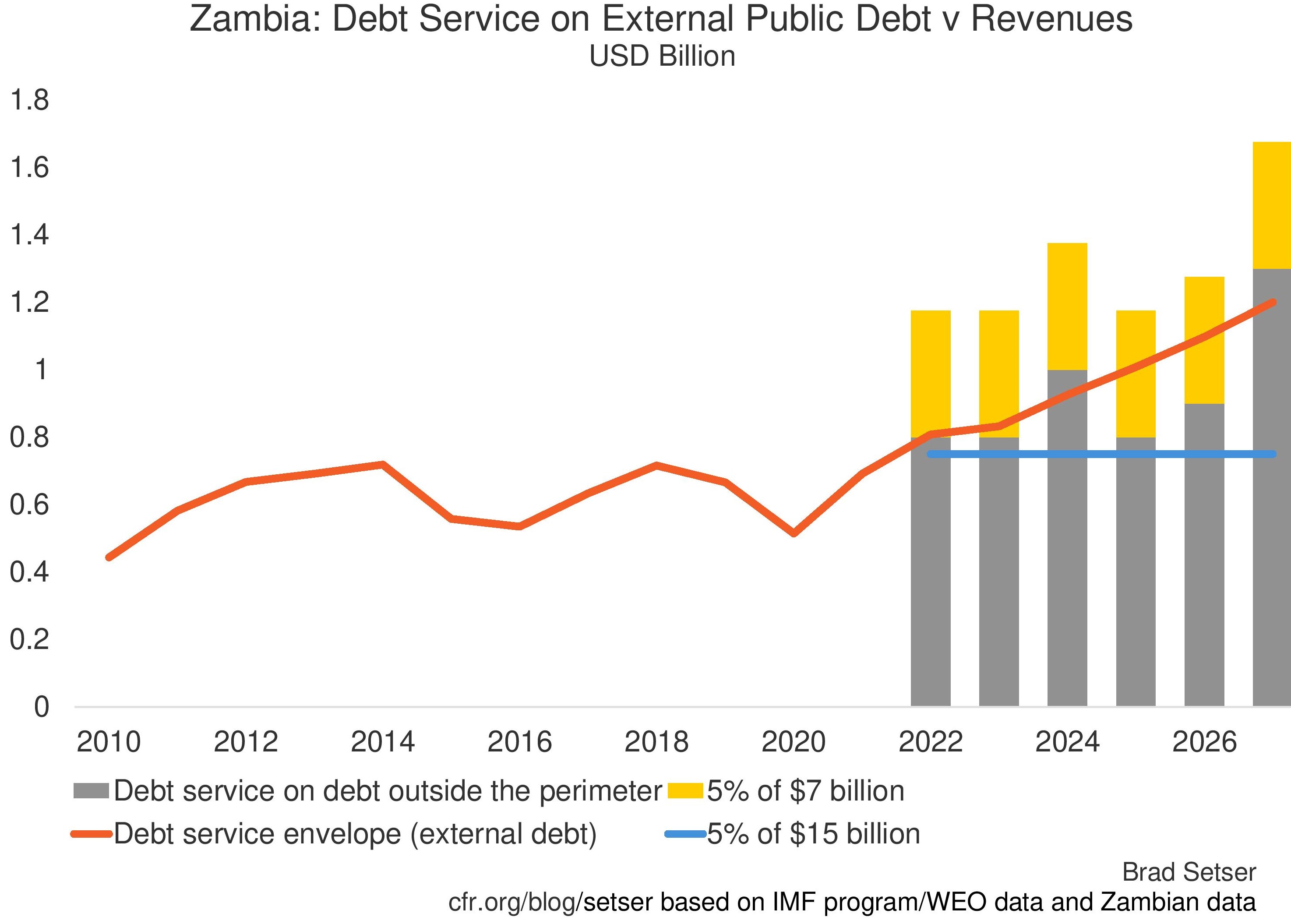

The debt service constraint under the applicable guidelines is the lower of 14% of revenue and 10% of exports. It turns out that 14% of revenue is more binding. Revenues are forecast to be around 20% of 2025-27 GDP, with GDP estimated to be in the $30 to $35 billion range. That works out to a limit on external debt of around $1 billion a year (using either the IMF’s WEO data or Zambia’s investor presentation).

Debt service on the foreign holdings of local currency debt is currently absorbing almost all this payment capacity. The IMF’s data shows that roughly $500 million of these claims mature in each of the next few years (IMF Zambia staff report, see Table 1 of the debt sustainability analysis on p. 109 of the PDF—the IMF could do a better job of putting these kinds of important details upfront). Throw in a 10% plus coupon, and total debt service on these claims is around $700 million a year—so roughly 15% of the external debt stock is absorbing nearly all of the identified debt service capacity (the numbers below include debt service on the MDB debt, and are taken from the October investor presentation).

Moreover, my understanding (and it could be off) is that the IMF’s treatment of local currency debt assumes that the bulk of maturing local currency bonds held by foreign investors roll over (Zambia assumes that foreign investors will buy 15% of new local currency bond issuance). Thus, amortizations on the projected future stock of foreign holdings of local law, local currency debt are more or less are a perpetual drain on debt service capacity of roughly $500 million a year.

That resulting large drain on projected debt service capacity from a relatively small share of the total debt stock seems a bit off to me, even if the IMF is going strictly by the book here (foreign held local currency bonds are external debt, and the low income country debt sustainability criteria are written for all external debt).

For one, the use of the formal maturity structure to determine the risks posed by foreign held, local currency claims actually seems to understate the real risks here. Holders of foreign currency claims in aggregate can only exit for good when the country makes scheduled payments, but foreign holders of local law instruments can exit at any time by selling their claim (likely at a discount) to local investors and then selling local currency to the central bank for foreign exchange. In theory, of course, the central bank could let the local bond market and a floating exchange rate absorb all of the selling pressure. In practice, no frontier market central bank would do so—the impact on the local bond market and the exchange rate would be too extreme, with consequences for financial market stability as well as inflation.

As a result, I believe that it intellectually makes more sense to look at the stock of foreign held local claims against the stock of foreign exchange reserves rather than the capacity of the government to raise tax revenue.

The combination of a perpetual drain on debt service from maturity structure of these claims together with the fairly constant overall stock from assumed new inflows also means that these claims have a truly disproportionate impact on both near-term debt service capacity and on the 2027 NPV constraint.

The financing assumptions assume that the local currency bonds could roll off as they come due in the initial period, and thus reserve debt service capacity against that risk. Fair enough. But then in a sense the claims should disappear from the debt service tables from then on, as the country will already have set aside reserves to pay down the stock (as well as in theory maintaining a revenue buffer sufficient to allow the Treasury to pay down a portion of maturing claims out of tax revenue).

The concerns expressed by the bond holders committee about the impact of the foreign held, local law claims on the restructuring thus strike me as having technical merit.

One way to see this is to consider a hypothetical 5% coupon on the $15 billion of permitted external debt, basically, the easier possible restructuring. The $15 billion stock number implies a cap on external interest payments of around $750 million a year (~ 2.0% of projected 2027 GDP), a sum that on its own fits comfortably within the projected limits on debt service relative to revenue. For the foreign currency external creditors, this works out to coupon of about $600 million a year.

However, the large projected drain on debt service capacity coming from amortization of the foreign holdings of local currency bonds plus the interest on these bonds essentially makes the coupon payment consistent with the IMF’s own NPV stock constraint impossible ...

China thus would be on far stronger grounds if it challenged the share of debt service capacity going to the foreign holders of local currency bonds rather than continuing its quixotic campaign against the preferred creditor status of the MDBs.

I can also think of two technical adjustments the IMF could make that would be both analytically justified and that would smooth the path to a debt restructuring agreement.

One is to just assume that a substantial share of maturing local law claims held by foreign creditors roll off.

The foreign holders of local law claims would still eat up the near term debt servicing capacity. But the foreign held local currency claims would then disappear from the stock over time, and wouldn’t weigh on the long-term debt carrying capacity calculations. This change would leave scope to maintain the economic value of other external claims over time. The $3 billion in projected 2027 local currency claims would fall to around $1 billion by 2027, allowing a smaller haircut on all other external claims. The NPV available for existing external foreign currency claims (excluding the MDBs) in 2027 would rise from $7 billion to around $9-10 billion (relative to about $14 billion face value in claims).

A second approach would be to assume that foreign investors in the local currency bonds roll over their claims and then to only count the interest payments on foreign held local law claims against the external debt service target. That would be analytically justified by an assumption that the stock of local law bonds held by external investors stays constant over time. The debt service burden from foreign held local law claims would be calculated a bit differently than the debt service on foreign currency claims, but in an analytically justified way.

Of course, the risk that these bonds would roll off would need to be factored into the program in other ways—notably through the level of reserves that the program would target. But the basic idea is straightforward—for local currency debt, the flow cost (the interest payments), rather than the amortization of the stock, is the real drain on fiscal debt servicing capacity. Ultimately, solvency is primarily determined by the interest burden on the debt stock, not its amortization profile.

A final approach would be to have a separate target for the debt service on foreign held, local law, local currency bonds and for the debt service on foreign currency claims held by external creditors. Intellectually, this isn’t totally satisfactory: foreign held local currency bonds do pose distinct risks from locally held local currency bonds. But it is consistent with the intellectual history behind these targets. The IMF-World Bank joint debt sustainability criteria for low income countries were established for countries that in general had no history of attracting foreign participation in their local currency bond market, while the debt sustainability framework for market-access countries emphasizes fiscal rather than external debt sustainability and differentiates between local and foreign currency debt rather than the debt owed to residents and the debt owed to non-residents.

Sri Lanka

Sri Lanka, while a poor country, isn’t quite poor enough to be formally part of the “Common Framework” (as the GDP per capita is around $4,000). It thus also isn’t covered by the joint IMF-World Bank debt sustainability framework for low-income countries.

This has given the IMF much more flexibility in the criteria it uses to assess debt sustainability.

And it appears—based on the numbers in the IMF’s program—that the IMF has used this flexibility to limit the losses creditors will need to take. In fact, the proposed debt targets appear to be so generous to creditors that they call into question the ability of a restructuring to return Sri Lanka to debt sustainability (the key targets and the debt sustainability analysis are found in Annex 2, which starts on p. 54).

There consequently appears to be a substantial gap between the debt sustainability criteria applied to low-income countries and the debt sustainability criteria applied to market access countries that are just above the low-income cut off line—which to me is a real “architectural” issues.

The IMF appears appears to have concluded that Sri Lanka can support public debt of over 100% of GDP through 2028, and a high debt to GDP ratio for several years after that (technically the target is for 95% of GDP in 2032).

That is just a remarkably high level of public debt for a country that collected on average tax revenues of 12% of GDP in the ten years before the pandemic (Zambia on average collected over 18% of GDP in revenue). The IMF program is of course built around increasing Sri Lanka’s capacity to collect revenue over time, but programs built around big positive shocks to deliver debt sustainability don’t have a great record (IMF programs for Argentina and Pakistan come to mind).

The binding constraint on external debt payments seems to have been set through the backdoor. Unlike in Zambia, the IMF hasn’t laid out binding criteria on the NPV of external debt (relative to either GDP or exports) or binding criteria on external (public and publicly guaranteed) debt service relative to either exports or revenue.

Rather, foreign currency debt service was capped at 4.5% of GDP.

Foreign investors don’t hold any significant local currency claims on Sri Lanka. Sri Lanka does have a few domestic-foreign currency bonds, but those are likely to be settled in domestic currency over the next few years. The foreign currency debt service constraint thus reduces to the constraint on external debt service.

And 4.5% of GDP is far too high in the absence of an NPV stock constraint.

A bit of debt math:

External public and publicly guaranteed debt peaked at around 70% of GDP and now looks to be around 60% of GDP over the next few years, though the precise number depends on the exchange rate. The IMF uses a 5% discount rate in low-income countries. By implication an NPV neutral extension of Sri Lanka’s debt stock that delayed maturities but maintained a 5% coupon over time would require interest payments of roughly 3.0% of GDP. That obviously is a sum below the cap on foreign currency debt service.

In other words, the criteria set out in India’s letter suggest that the IMF doesn’t believe that any NPV reduction (at a 5% discount) is needed to return Sri Lanka to sustainability. Best I can tell, extending the maturity on all bonds and Chinese policy loans by ten years (so principal payments fall outside the period of the debt service caps) at an interest rate of 5% would meet the criteria that the IMF has set out. That is especially surprising as Sri Lanka’s external bonds trade at 30 to 40 cents on the dollar, a price that strongly suggests that bond investors expected to be asked to deliver significant debt relief.

It is a little hard to understand why China’s policy banks didn’t jump at these terms as well.*****

I hope Sri Lanka’s authorities and its debt advisors treat this as an upper limit, and that Sri Lanka’s external creditors have the good sense to recognize that high levels of debt service set the stage for bonds that never rally to par and that ultimately have to be re-restructured (as will be the case with the bonds Argentina issued in 2020).

Concretely, Sri Lanka’s history would suggest aiming for a public debt to GDP level that is closer to 70% of GDP than to 100% of GDP, and trying to cap interest payments on external public and publicly guaranteed debt at less than 2% of GDP.

“Common Framework” (or Almost) Yet Different Outcomes

The gap between the debt relief (measured in NPV terms, so it can be achieved to be sure by extending principal at a concessional coupon) that the IMF is demanding in Zambia and the absence of similar demands for debt relief in Sri Lanka is hard to understand. Levels of public and publicly guaranteed external debt are similar. Total public debt is also similar. If anything, Zambia has a stronger export base (though its ability to export copper depends on a high level of foreign investment that requires a commercial return) and a slightly better record of collecting tax revenue.

Sri Lanka’s debt to revenue ratio is just very high, which suggests its capacity to sustain a high level of public debt is limited.

The low-income country debt sustainability framework is different from the market access country debt sustainability framework. Sri Lanka also apparently scores highly on the probability of a positive debt sustainability shock for some obscure reasons. But sometimes the IMF needs to apply a bit of judgment. If Zambia and Sri Lanka look reasonable similar on a set of standard debt metrics, the expected NPV haircuts shouldn’t be radically different. Sri Lanka’s end of 2022 stock of external public debt (64% of GDP, p. 54) isn’t too far from Zambia’s stock of external foreign currency debt at the end of 2021 (66%, see p. 109; Zambia also had 13% of GDP in external local currency debt)

Where does that leave the world?

Well, China has finally allowed the IMF to lend to Sri Lanka, which is a good thing. Sri Lanka is out of reserves and needs the IMF’s dollars even more than Zambia.

Yet China continues to make financially unfounded demands for the World Bank to restructure its already concessional loans—demands that call into question its willingness to participate in the “Common Framework” in good faith. Hopefully these demands are pure politics and will fade away once China Exim and the China Development Bank get serious about negotiating actual restructuring terms.

But the IMF is also struggling to develop a consistent approach to setting debt sustainability targets in complex cases.

The initial integration of foreign-held local currency bonds into the debt sustainability framework for low-income countries didn’t really work. The debt service that is now assigned to cover Zambia’s local currency bonds held abroad is simply too high—as a small share of the debt ends up hogging the estimated external debt servicing capacity.

In Sri Lanka, by contrast, the IMF’s application of the market access country framework has only set out fiscal targets, not targets for external debt or external debt service.

And, no doubt in part because of the different frameworks used for low-income countries and market access countries, the gap between the IMF’s estimate of Zambia’s external debt carrying capacity and the IMF’s estimate of Sri Lanka’s debt carrying capacity is enormous. I tend to think the IMF is closer to being right in Zambia than in Sri Lanka—but no doubt some creditors would disagree.

There is actually an agenda for reform in these observations—one that is a bit more ambitious than trying to make the official bilateral creditor committee’s move on a timetable that matches the Swiss Railway system. But it does require knowing a bit of debt math, and caring about financial outcomes as well as the easier to understand procedural questions linked to the integration of Chinese policy banks into the process for coordinating a necessary change in payment terms.

*/ The commercial part of the loan for Kenya’s Standard Gauge Railway pays LIBOR plus 360 basis points, which is a quite steep rate right now. A 15 year loan with 5 years grace is also fairly onerous when it is designed to support the construction of infrastructure with a long service life. I understand why Kenya wants to adjust the terms of this loan.

**/ I disagree with those who look at the face value of the MDBs claims and then argue that the MDBs are too big a share of the total debt stock not to participate in a debt restructuring. The stock of MDB claims needs to be adjusted for the fact that these claims on low-income countries are already concessional. MDB claims also generally haven’t increased significantly as a share of the borrowing country’s GDP in the key distress cases, at least not prior to the COVID shock.

***/ China’s bilateral claims have been defined to be the claims of the Export-Import Bank of China (China Exim) and claims of other Chinse state creditors that are guaranteed by its Sinosure. The claims of China’s other big policy bank, the China Development Bank, are considered to be commercial claims in the absence of a Sinosure guarantee.

****/ The eurobonds‘ legal claim in Zambia is for the face value of their bonds plus accumulated interest arrears, which rise by about $240 million a year (with a bit of 2020, 2021 and 2022 already in the stock—and one assumes 2023 as well). The accumulated claim is thus rising towards $4 billion—which matters for the valuation of the bonds and the bond holders restructuring strategy. See Greg Makoff’s forthcoming book on Argentina’s legal woes.

*****/ The financial capacity of the policy banks to absorb losses is an open question, given the opacity of their capital position and sources of external funding. China Exim and the China Development Bank received a capital injection of $62 billion back in 2015, when SAFE converted a portion of its reserves into equity in both banks. According to the Financial Times, “the capital injections will come in the form of entrusted loans that convert to equity.” If the PBOC has similar exposure to the policy banks now, a similar financial transaction could be used to capital a bad bank in each institution—or simply to allow the distressed exposures of both institutions to be held against equity capital. Equity funded loans to low income countries incidentally is the model that the World Bank’s concessional arm (IDA) uses.