On Designating China as a Currency Manipulator…

China really did manipulate its currency before the global crisis. It really doesn’t do so now. But how China’s manages its currency still matters for the global economy.

Trump’s designation of China as a currency manipulator has triggered a lot of good reporting about China’s current system of currency management, and the legal meaning of a designation.

The Wall Street Journal and Bloomberg were particularly good at explaining how China now manages its currency, and how the discretion to set the fix away from the PBOC’s rule gives China’s central bank a tool for managing the market without large direct sales.

I think my 2016 blog on how the Trump administration legally could name China as a manipulator (under the 1988 act) has stood the test of time. It may even provide a roadmap of sorts for the legal reasoning the Treasury will use in its next foreign exchange report, as it tries to explain why it yielded to Trump’s personal pressure for a designation. The Treasury isn’t bound by the three criteria set out in the 2015 trade act; the 1988 trade act is still on the book. Obviously, the United States will emphasize that China wasn’t forced to set the “fix” below 6.9 CNY to the dollar (a level that implies a yuan is worth about 14.5 cents) —and argue that its decision to do so was intended to give China a competitive advantage and thus technically it meets the criteria in the 1988 trade act. The Treasury has already confirmed in a recent foreign exchange report (p.4) that it is legally possible to be designated as a manipulator using the standards of the 1988 trade act even if the country doesn’t meet the standards set out in 2015.

In some ways, the administration actually has slowly been building toward this designation for a while: Navarro and others have argued that China should be resisting depreciation as strongly as it resisted appreciation, and that China’s use of the currency to counter U.S. sanctions for its unfair trade policies is an additional unfair trade practice.

Alan Beattie was particularly pithy in describing the legal consequences of a designation (nada).

Yet while designation itself has no real legal consequencess under the 1988 trada act, I would note that nothing precludes tying a manipulator designation to a punishment that is legally grounded in a different part of the trade law. In the past, I have suggested that the Bush Administration could have tied a designation to the use of section 421 special safeguards against China. The special safeguards were designed to counter surges in imports in the twelve years after China joined the WTO, but a safeguard case was subject to presidential review and the Bush administration didn’t accept any cases. I think it should have had a policy of accepting all cases so long as China was manipulating. More recently, I suggested that a designation of manipulation (based on a modified version of the Bennet criteria where China would not have met the standard for manipulation) could be linked to an explicit threat of counter-intervention. Bottom line: If the Trump administration wants to use “manipulation” as a justification for further escalation in the trade conflict, it won’t be limited by the non-existent sanction for manipulation set out in the 1998 trade act.

I also thought Josh Barro did a good job of describing why this all matters—the United States in a sense wants China to continue to resist market pressure for its currency to depreciate. The IMF continues to argue that China should move toward more “flexibility” in its exchange rate, but I suspect the bulk of the Fund’s members would rather that China manage the yuan for a bit longer (and keep its controls up too, even if that makes the yuan’s participation in the IMF’s SDR basket a tad awkward). If China stopped managing its currency and the yuan fell sharply, the world would face a nasty, deflationary shock. The conditions for an orderly exit from China’s current system of exchange rate management aren’t currenttly present in the market, or in the world.

There isn’t all that much left to add.

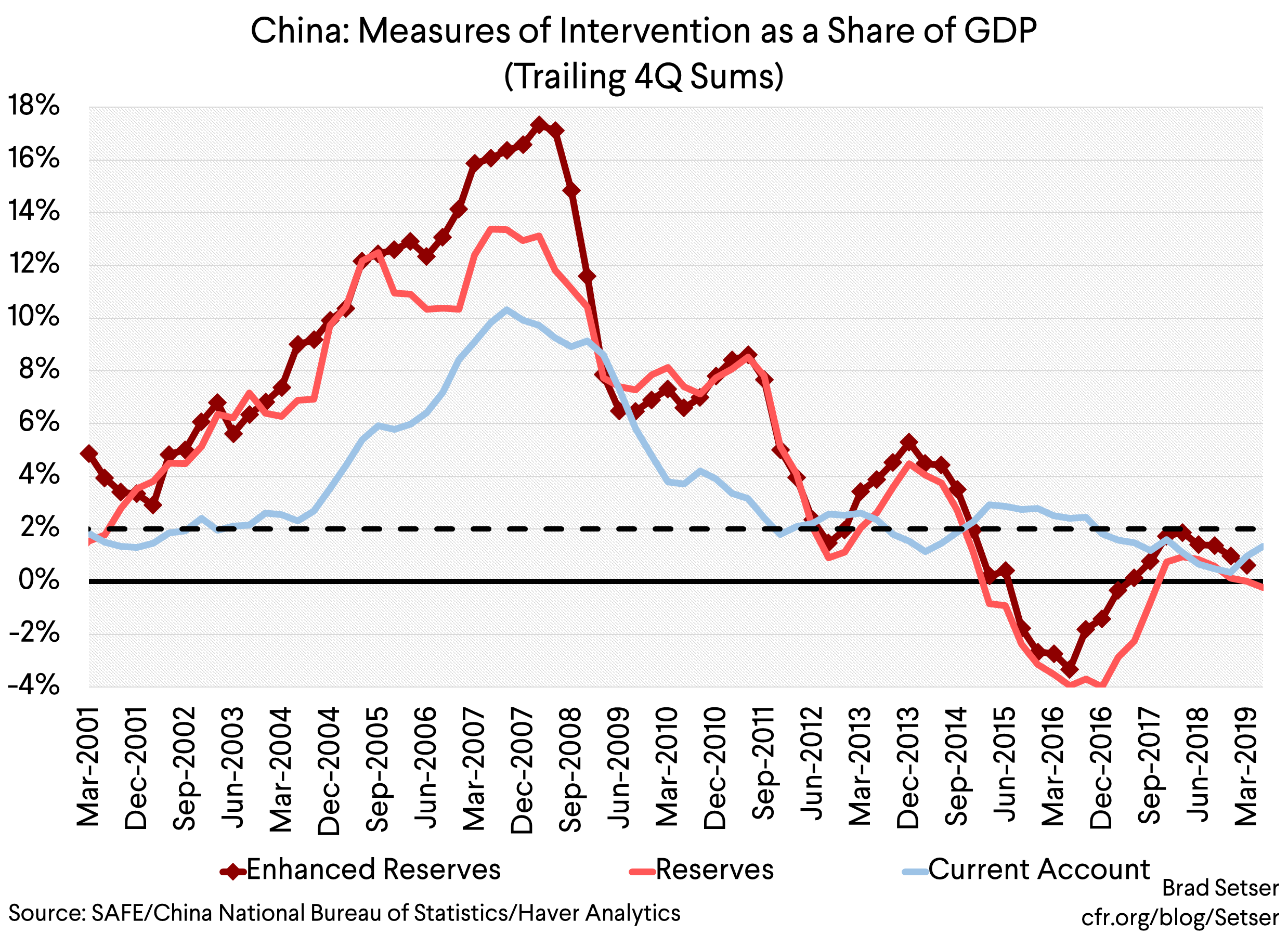

I do want to provide the charts to support a point that I have been making elsewhere (notably, on Twitter)—namely, that the designation for China came fifteen years too late.

The easiest way to see this is to retroactively apply the standard—a 2 percent of GDP current account surplus and 2 percent of GDP in intervention—the Treasury now uses to assess the case for manipulation under the Bennet amendment retroactively to China. I like to look at a broader measure of China’s intervention, one that captures the funds China shifted to the state banks in 2003 and 2005 and in 2007 and the funds shifted to the CIC.* But it doesn’t really matter—China crossed the 2 percent of GDP in intervention threshold back in 2002 and the 2 percent of GDP current account threshold in 2003, though it was close on the current account. By 2005, the case for designation—using the Bennet criteria—was clear cut. And that case basically disappeared over the course of 2014.*

There is one important point here—the yuan went from being undervalued (in my view) in early 2014 to being a little overvalued in 2015 not because the yuan moved against the dollar, but rather because the dollar appreciated against everyone else. That led to a big move in the yuan—one that China partially reversed over the past five years in the context of its move toward a basket peg (once the BIS index reflects the August move, China likely will have come close to fully reversing the 14-15 appreciation of its currency; that’s one reason why China’s non-tariffed exports have held up relatively well amid the broad global slowdown).

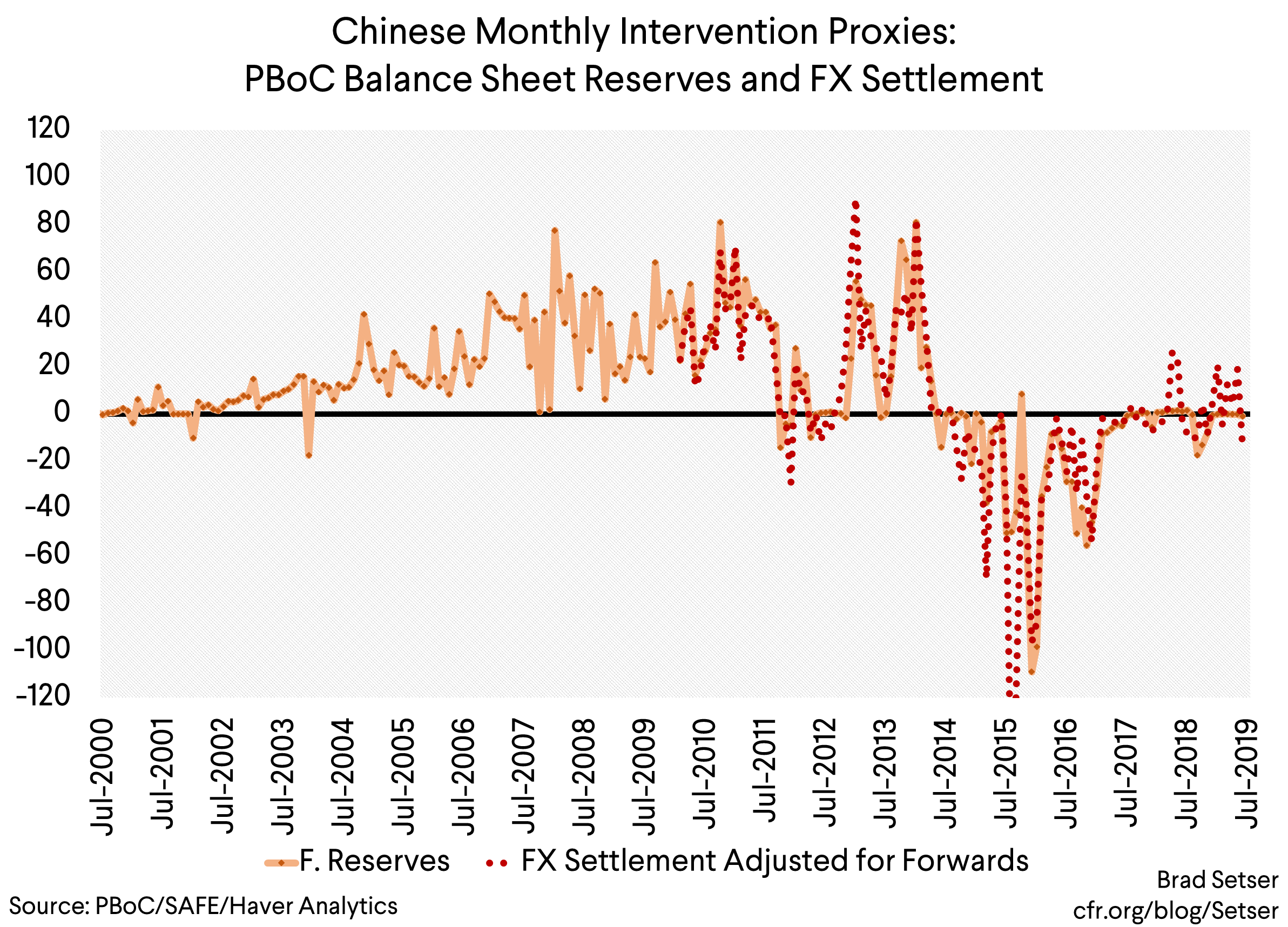

One thing that puzzles many people is how China manages its currency without a lot of visible intervention (broader measures that show the activity of the state banks suggest more activity than the PBOC’s balance sheet, which increasingly looks massaged to provide the appearance of stability). The answer in a sense is that China has a credible intervention threat—and has developed the capacity to signal where it wants the yuan to trade.

When China moved toward more flexibility in 2015 (a decision that also provided cover for a devaluation in my view) it made a technical error. It said that the close in the spot rate the previous day would almost mechanically (after adjusting for overnight moves in the dollar against other big currencies) set the start of the yuan’s daily trading range the next day.

China wasn’t though, willing to live with the results of an unfettered market. It ended up influencing the next day’s trading range by intervening in the market to move the close around. That took up a lot of reserves.

Over time, China gave itself a bit more flexibility to guide the market by introducing a discretionary factor into the central point of the yuan’s trading band. That signal made it possible to manage the yuan without using reserves so heavily. Visible reserve growth —at least judging from the PBOC’s balance sheet— has essentially disappeared (there were small sales last fall after the yuan depreciated over hte summer that helped set a floor under the yuan at 6.9 for a while). The settlement data, which includes the state banks, shows more activity, but not a consistent pattern (see the dotted line above).

The fall in outright intervention, in both directions, has made assessing the case for “manipulation” harder. But there is no doubt that over the summer, China used its discretion to try to limit the yuan’s depreciation—one bank calculated that if the yuan had mechanically followed the previous days close and overnight moves in the dollar, it would now be at around 7.3. The latest balance of payments data also suggest that the PBOC sold a bit of foreign exchange in the second quarter, so they were using the reserves to push back (though it raises a question of why the sales in the balance of payments aren’t reflected on the PBOC’s balance sheet) .

So what’s next?

It is hard to tell.

The United States and others want China to use its ability to manage the yuan (notably through the daily fix) to prevent further depreciation. That though is an ask that China may not be willing to give if the United States goes through with more tariffs and doesn’t help China out on Huawei. Time will tell how worried the Chinese still are about the risk of renewed outflows.

And conversely, if China lets the yuan slide too fair, it could trigger yet more escalation (more tariffs I suspect, not direct U.S. buying of the yuan but you never know) from the United States.

I do though think it is important for the global economy, not just for the U.S., that China continue to try stabilize the yuan, and that it rely on fiscal policy not a weak currency to stabilize its own activity.

Seven yuan to the dollar is a pretty weak yuan vs. the dollar. With the yuan’s 10 percent (or a bit more) broad depreciation against the basket of the currencies of China’s trading partners since 2015, China is a competitive exporter once again. Take claims to the contrary from consulting firms about China’s fading competitiveness with a grain of salt: I am not convinced that they are well grounded in the actual trade data. China is a less competitive producer of apparel thanks to rising wages, but it is an increasingly competitive producer of batteries, cell phone and tablet screens, auto parts and autos and—famously—5G networking equipment. China’s exports out-performed global growth considerably in 2017, and slightly out-performed global trade growth in 2018 even with U.S. tariffs.

China’s current account surplus is also rising again—with the q2 data, it is up to $185 billion (around 1.5 percent of GDP). Add in the $85 billion estimated miscalculation of China’s services balance** and China’s current account surplus may be heading back toward the Treasury’s 2 percent of GDP threshold.

The IMF missed the signs of this swing back toward surplus in its latest assessment of China. The Fund in my view hasn’t come to terms with the fact that China’s current account surplus has come down in no small part because China has run a fiscal policy that the Fund thinks is far too loose.

And the Trump Administration is increasingly facing the risk that an ever escalating trade war could end up triggering a shift in China’s currency management—or a premature shift to a float when a float would lead to a big fall in the yuan. If that happened, the world, not just the United States, would experience a second China shock. The stakes thus are high.

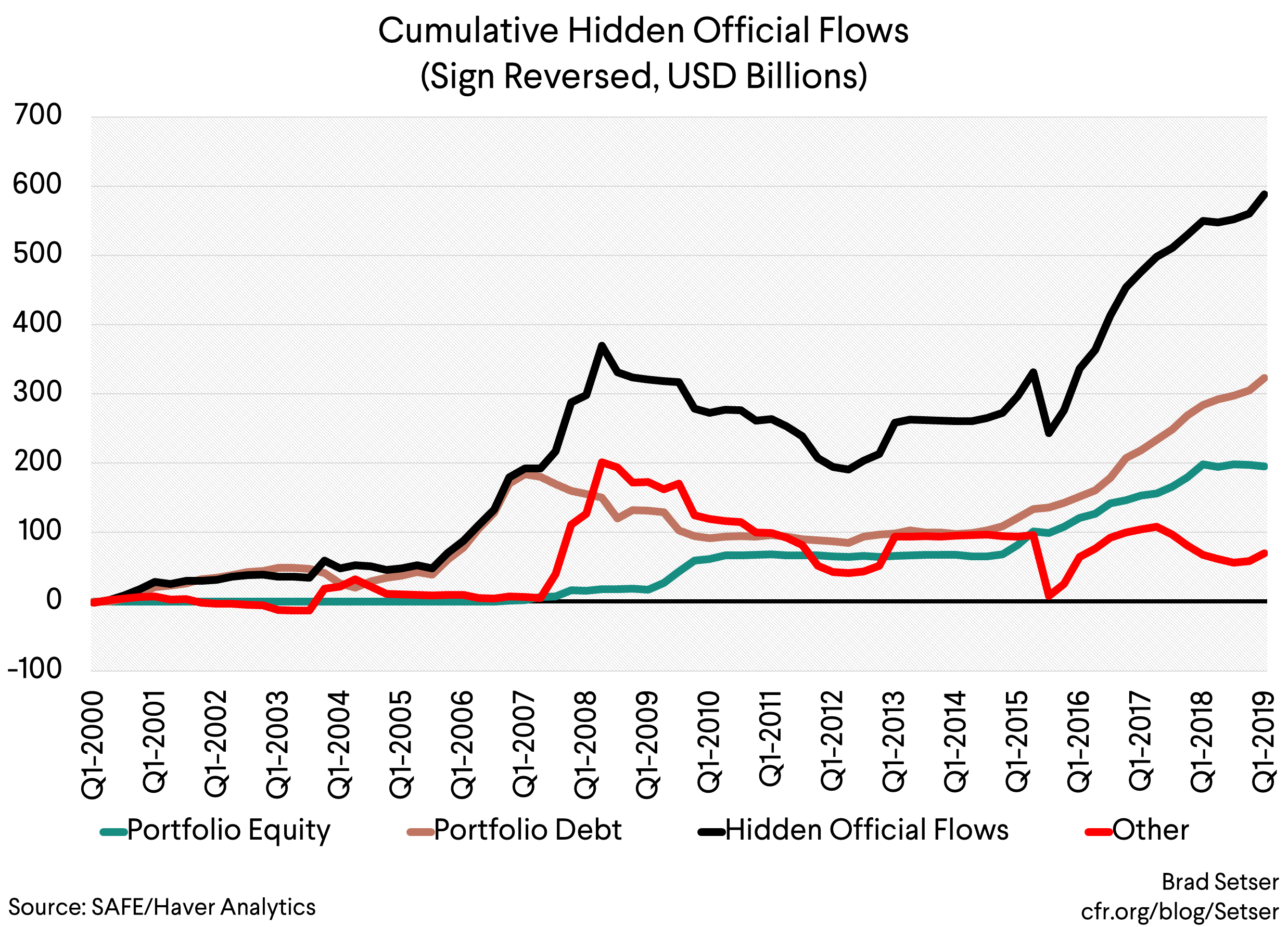

* My measure of enhanced intervention includes the reserves that China hid away in the state banks back before 2008, and the funds shifted to the China Investment Company (the CIC). There are some conspiracy theories floating around that suggest that China never deducted the funds that went over to the CIC from its reserves, and thus China has fewer “true” reserves than claimed—that’s pretty clearly not true, though the transfer was gradual and not totally transparent (it included foreign exchange that previously had already been moved to the banking system). The BoP clearly shows a spike in portfolio equity purchases in early 2008 and again in 2010—that was the buildup of the CIC’s external assets. It didn’t register in reserves because, well, China was adding to its reserves at the time, so it registered as slower reserve growth rather than as an outright dip in reserves —and also because the state banks were at the time unwinding the bond portfolio that they bought with the PBOC’s spare foreign currency back in 2005 and 2006. Lots of folks forget that China was squirreling away foreign currency in a lot of different places before the crisis.

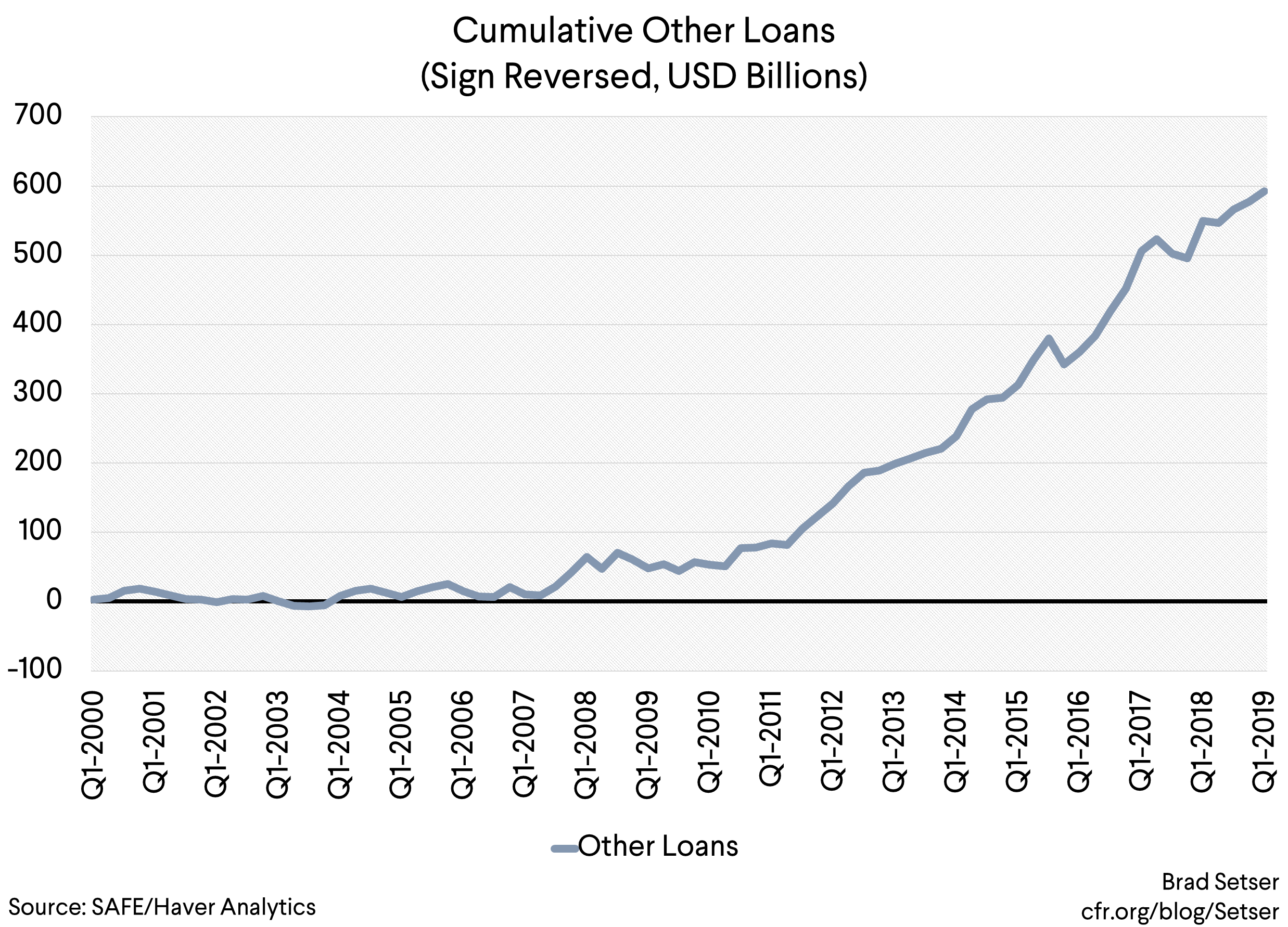

The CDB’s external lending also registers in the balance of payments, as a rise in China’s extenral loans

China’s government thus has at least $1 trillion more in foreign assets than it reports as foreign reserves.

** The Federal Reserve’s economics staff believes the tourism deficit is now overstated primarily because China undercounts its tourism exports. The 2017 revision to China’s tourism data largely got rid of the overcounting of imports (see the appendix to Anna Wong’s paper), but it created a new problem on the export side—China keeps changing its methodology without ever really getting rid of questions about the accuracy of its numbers.