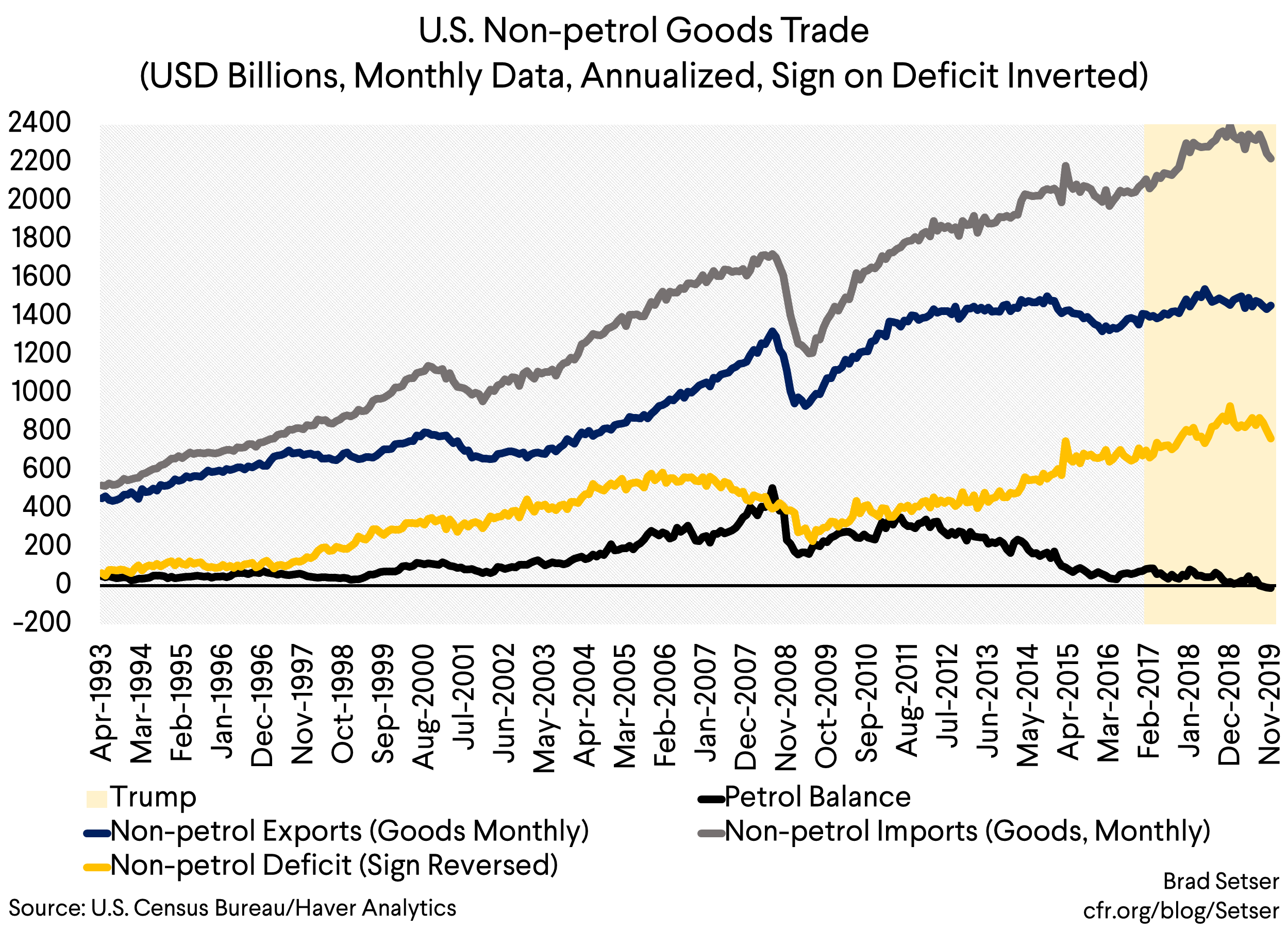

More Trade Destruction than Trade Diversion Right Now

Earlier in the year, there was a plausible argument that Trump’s tariffs were mostly just diverting U.S. demand to other markets. But in recent months imports from China and imports from the United States’ other trade partners are both falling. And the fall in imports has brought the non-petrol trade deficit down significantly from its levels this summer, though perhaps not permanently.

U.S. imports have been very weak after the 15 percent tariff on $112 billion of imports from China (now reduced to 7.5%) was introduced this September. Ratcheting up the previous 10 percent tariff (on $200b of imports) to 25 percent also has had an impact.

But there are non-tariff related reasons for imports to be weak. Investment has been on the soft side (to the chagrin of proponents of the tax reform)—which is in part related to tariffs and uncertainty and in part a function of the slowdown in the oil patch and in part a function of the lagged impact of the Fed’s rate hikes back in 2018. More generally, the goods producing part of the economy is weak—and goods are still way more import intensive than services.

No matter—

The fall in imports in the last few months has been strong enough that it should change the narrative around the impact of the tariffs a bit, at least for a while.

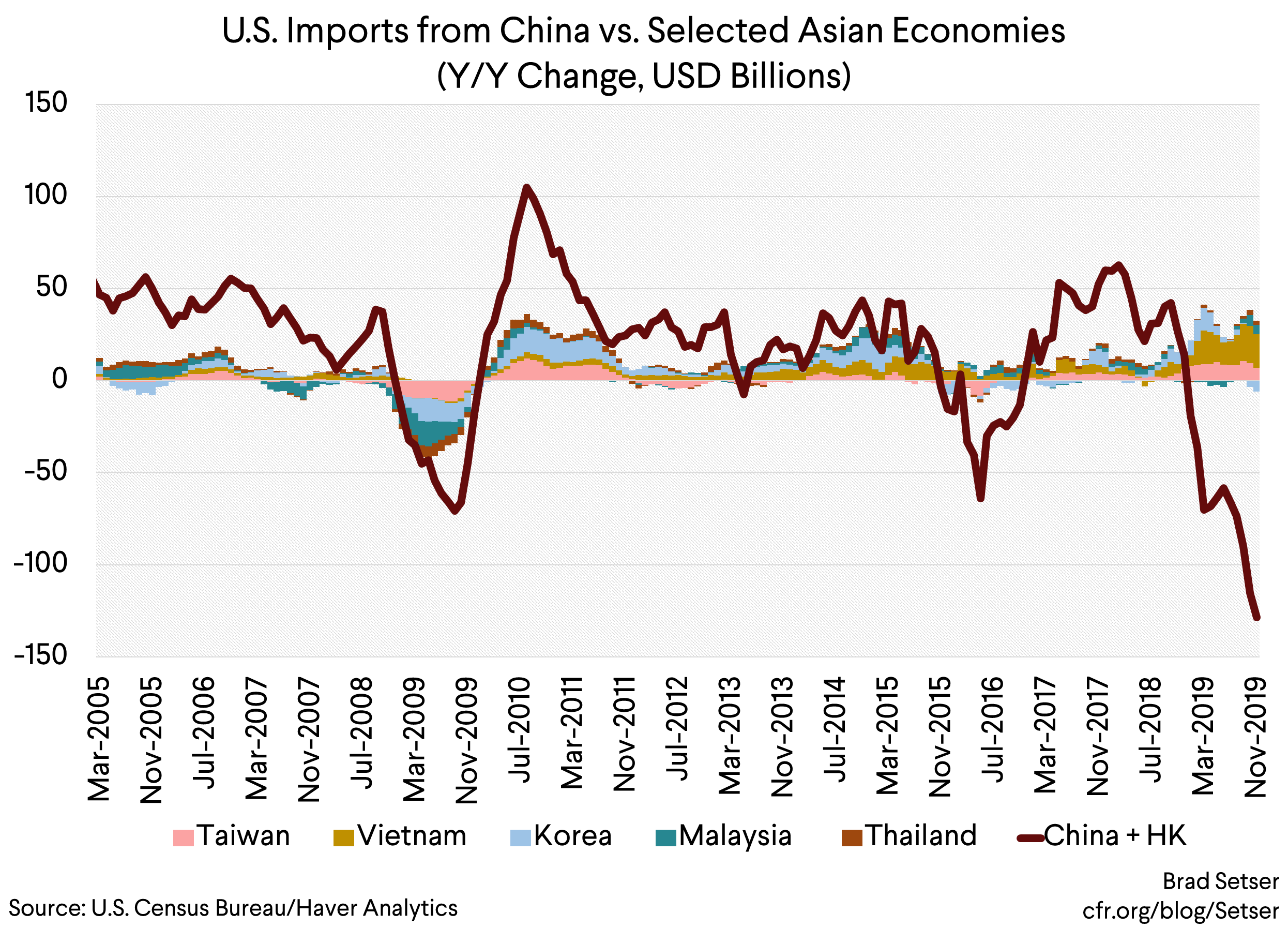

There has been some trade diversion—imports from Vietnam and Taiwan are clearly rising as firms relocate some production (or at least final assembly) to avoid the tariffs. But the numerical impact of trade diversion—higher imports from countries other than China—clearly hasn’t been enough to fully offset the fall in imports from China.

In the fourth quarter, goods imports from China look to be down over 20 percent y/y. And with a pre-tariff base of over $500b, that’s an (annualized) fall of well over $100 billion.

The $18.4 billion rise in imports from Vietnam and $6.9 billion rise in imports from Taiwan doesn’t come close to offsetting the fall in imports from China in dollar terms (to be fair, U.S. imports from Taiwan jumped in Q4 of last year as well; the base always matters in y/y comparisons).

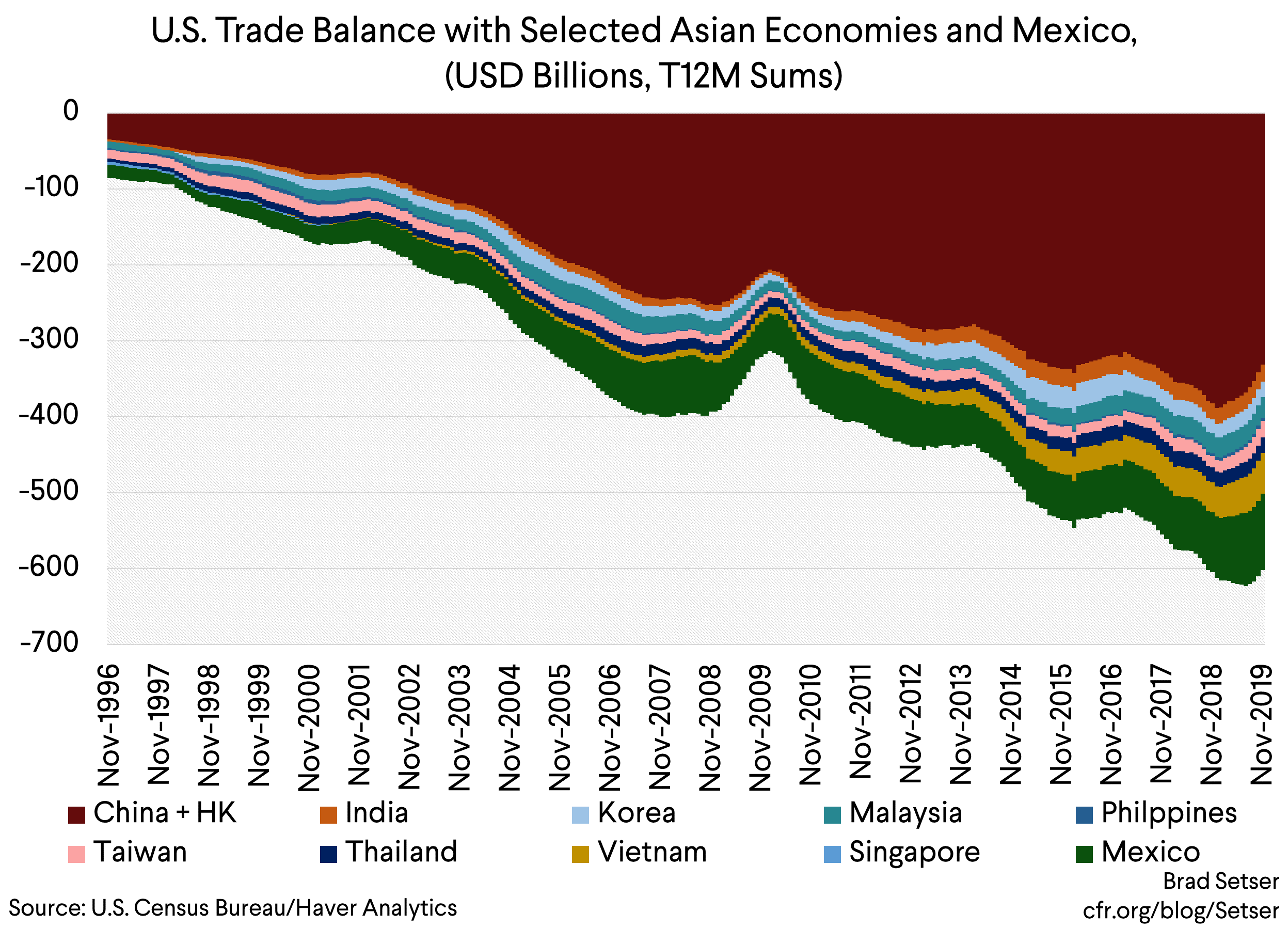

This also shows up if you plot the trailing 12M sum of the U.S. bilateral trade deficit with a host of manufacturing exporters in the emerging world. The total deficit in dollar terms is down now (it would be down a bit more as share of U.S. GDP—but I need to wait for the Q4 GDP data and the December import data to have a good chart).

Of course there has been some trade diversion. Trump’s tariffs haven’t been an effective tool for promoting U.S. manufacturing, but they have been reasonably effective at encouraging firms to move supply chains out of China. It is just that right now the scale of the “diversion” is not big enough to offset the the scale of the fall in imports from China.

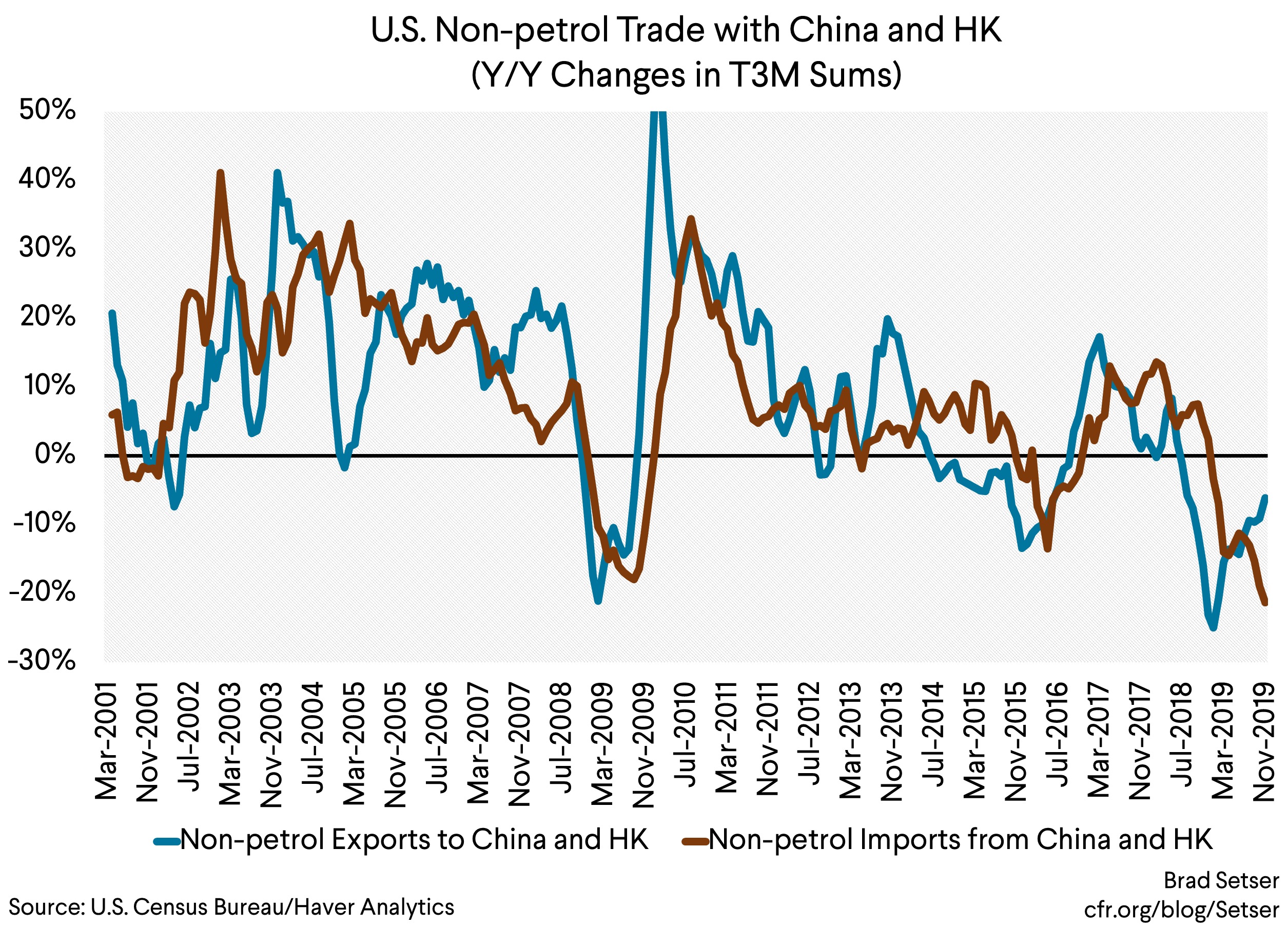

Year over year, non-petrol imports from China are way down, while exports have been starting to recover (China did a lot of retaliation in q4 of last year, but not much since).

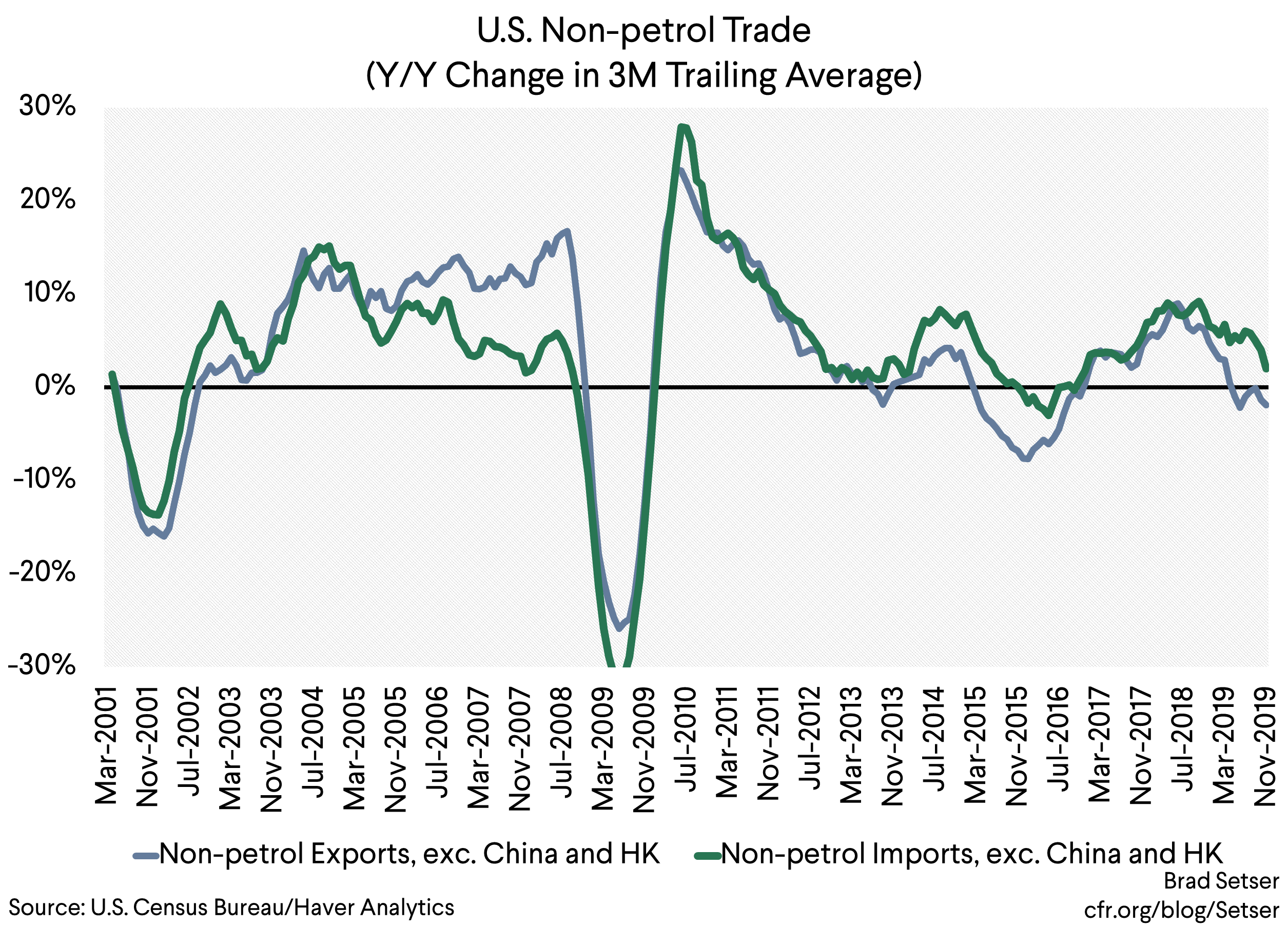

But it is significant that in the past few months, non-petrol imports from the rest of the world are also falling. A lot of this is in machinery and transportation equipment, categories that are not (yet?) dominated by China— but the fall continued after the GM strike was settled and pre-dates Boeing’s decision to cut 737 production.

I have to revise my priors here a bit too. In the summer I argued that if you took out trade with China, overall U.S. imports were growing in line with U.S. GDP—and thus the United States wasn’t responsible for the broader slowdown in global trade. That’s now changed.

I should give the IMF a bit of credit here—the elasticity of U.S. imports from China to the tariff on China (the bilateral elasticity) has been between 1 and 2, more or less what the IMF’s gravity model predicted back in April 2019 (other models have the bilateral elasticity at 3 or even more, which would imply the 25 percent tariff is prohibitive—which still may be the case, but only in the long-run). And the gravity model also “predicted” that the fall in imports from China would only be partially offset by rising imports from the rest of the world. The IMF got China’s current account surplus wrong in 2019 (as did most investment bank economists)* but I think they got the trade effects of the tariffs more or less right.

Many economist (and journalists) have argued that the main effect of tariffs is to re-route and reduce trade, not to change the trade deficit. But economic theory would also predict some reduction in the overall trade deficit from the tariffs. After all, the tariffs are a tax increase, and if the funds aren’t injected back into the economy through other means, putting significant tariffs on around 20 percent of U.S. imports of manufactures (2 percent of U.S. GDP) should induce a modest slowdown in the economy. Throw in the additional impact of uncertainty on investment and there should be some impact on the overall trade balance (and on growth), particularly as investment likely was slowing for other reasons as well. It’s just that the impact on the trade balance has largely come through slower overall growth,* not through the import substitution that proponents of the tariffs hoped for…

When the full data for Q4 is out, it is likely that the fall in imports (which looks quite large, on an annualized non-petrol imports are down about $80 billion from their peak) will have moderated the impact of the slowdown in demand on the U.S. economy. In other words, it looks like the rest of the world took most of the hit in Q4 from slowing U.S. demand—limiting the impact on the broader U.S. economy (though of course the manufacturing sector is still hurting from the slowdown in investment, weak exports, and increasingly the fall out of Boeing’s 737 debacle).

I don’t expect that result to be replicated in subsequent quarters. Some of the fall in imports in Q4 was likely the result of pulling imports forward ahead of the threatened tariffs (raising Q3 import at the expense of Q4). That should naturally reverse. The “trade creation” impact of the 7.5 percent tariff reduction on $112b of imports from China is likely to be minimal—but a “deal” that takes off the risk of further escalation may moderate incentives to shift more production out of China. If the “Trump” effect is basically a 12 percent increase in tariffs on China and a 3 percent global increase in the U.S. applied tariff on manufactures (imports from China are about a fourth of manufactured imports), the long-run effect should be a modest reduction in overall trade (Krugman is the obvious reference here)—but not a “structural” shift in the basic relationship between U.S. demand growth and imports.

Or put differently, if U.S. investment growth does pick up in 2020**, the rest of the world should get a bit of a boost—just, in all probability, not China.

* The IMF could have caught this with closer attention to the quarterly trade and balance of payments data coming out of China. The fall in the 2018 current account surplus was largely a function of the q1 2018 data print—and it was already clear at the turn of last year that China’s trade balance was changing direction and the surplus was starting to rise again. It wasn’t hard to see that once q1 2019 replaced q1 2018 in the data, the surplus was set to stabilize or rise (in macroeconomic terms, this was a function of China’s limited stimulus and the resulting fall in China’s imports). The most important part of the 2019 Article IV (which was premised on a steady fall in China’s current account surplus) was basically out of date the moment it was published, which is a shame.

** The Fed has moderated some of the broader impact of the tariff cuts. The Fed cannot offset the direct trade disruption, but by lowering rates, it can help support broader demand growth. The drag on residential investment from the Fed’s tightening cycle for example appears to be fading.