Time for China, Germany, the Netherlands, and Korea to Step Up

The world’s surplus countries have the ability to do more to support global growth.

The world—OK, the world’s manufacturing exporting economies—has been relying heavily on the United States for demand over the past two years.

And Donald Trump really doesn’t want to be the world’s engine of demand.

Citi’s Catherine Mann has noticed this too:

“There is an inconsistency between the U.S. acting as a locomotive for the world and the objective of the Trump administration’s policy to reduce the trade deficit.”

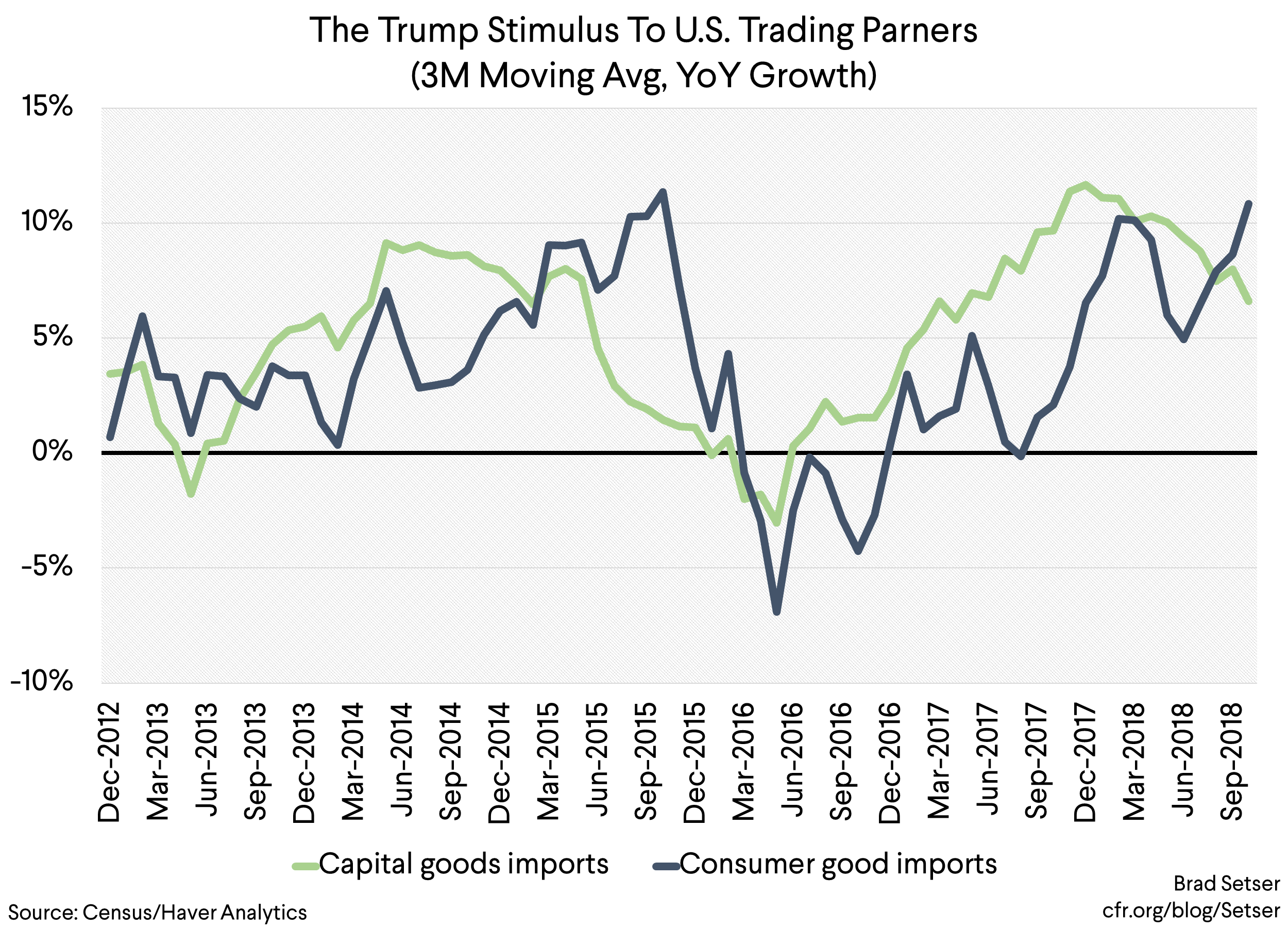

Remember that, at least until now, Trump’s tenure in office has been pretty great for the world’s manufacturing exporters. “Real” imports of capital goods grew quite rapidly in 2017, and real imports of consumer goods jumped in 2018.

Real import growth (excluding oil, which has its own dynamic) has been substantially stronger than in Obama’s second term. Rising U.S. imports likely provided close to a percentage point of U.S. GDP boost to global manufacturing demand ($200b) in 2018—enough to more than offset the very sharp slowdowns in Turkey and Argentina. And since U.S. export growth has slowed, that “net” boost to the rest of the world’s manufactures from a rising U.S. deficit will be close to 75 basis points of U.S. GDP. *

But U.S. demand growth isn’t likely to continue to rise by 3 percentage points of more of U.S. GDP. And, as the stimulus fades, U.S. import growth should slow too. The pace of growth in capital goods imports has already started to slow.

The world shouldn’t be counting on getting the same impetus from selling to the United States over next two years that it got in the past two years.

And that’s potentially a problem. It certainly seems like both China (in a big way; auto sales were down 20 percent y/y in December) and Europe (in a small way) have lost momentum.

The obvious policy answer—the win-win for the world—would be for China and the world’s twin surplus countries (countries with both a fiscal surplus and a current account surplus) to provide more support for their own growth. And there are pretty straight-forward steps they could take to do so.

China has tended to stimulate its economy by juicing credit and investment, and the recent slowdown reflects a policy decision to slow credit growth to limit the buildup of debt and leverage. But the current slowdown in China also reflects a slowdown in the pace of consumption growth (hence weak auto sales, and it seems, weak sales of top-of-the line smart phones).

And it provides China with an opportunity to focus its current shift back toward stimulus on steps to raise consumption.

Household savings remains about a third of household income, a very high level compared to other countries. As a result, China’s household savings is close to 23 percent of its GDP—versus a global norm of more like 8 percent of GDP. So households in China save something like three times more than households in a “typical” economy these days.

The IMF didn’t really mince words in a recent paper:

“With GDP per capita in PPP terms being similar to Brazil’s, consumption per capita in China is only comparable to Nigeria. If Chinese households consumed comparably to Brazilian households, their consumption levels would be more than double.”

And there are relatively obvious policy steps China could take to raise consumption and lower savings, as “government social spending…remains low compared to international standards.“

First, tax low-income workers less: social contributions are relatively high at the low end of the wage distribution. The IMF notes: “The current tax structure is regressive, especially for the very poor. While personal income tax has a relatively high exemption threshold, the flat nominal amount of social contribution at the bottom puts a heavy burden on poor households, with an effective tax rate of over 40 percent.”

Second, provide a larger basic pension benefit to all workers; more retirement security equals more spending by current retirees, and less savings at the low end of the distribution.

Finally, above all else, raise public spending on health care (see the New York Times on the limitations of China’s health care system). The IMF’s big paper on savings puts public spending on health at 1.7 percent of GDP in 2016 with a planned rise to 2.4 percent of GDP ( see p. 21).** That’s far too small an increase—China should be spending more like 5 percent of its GDP on public health, if not more.

All are doable steps—socialism with Chinese characteristics could benefit from a bit more socialism, so to speak. Or at least a bit more social insurance. There is abundant research from the IMF and the World Bank indicating these kinds of policies would be effective—they aren’t moon shots.

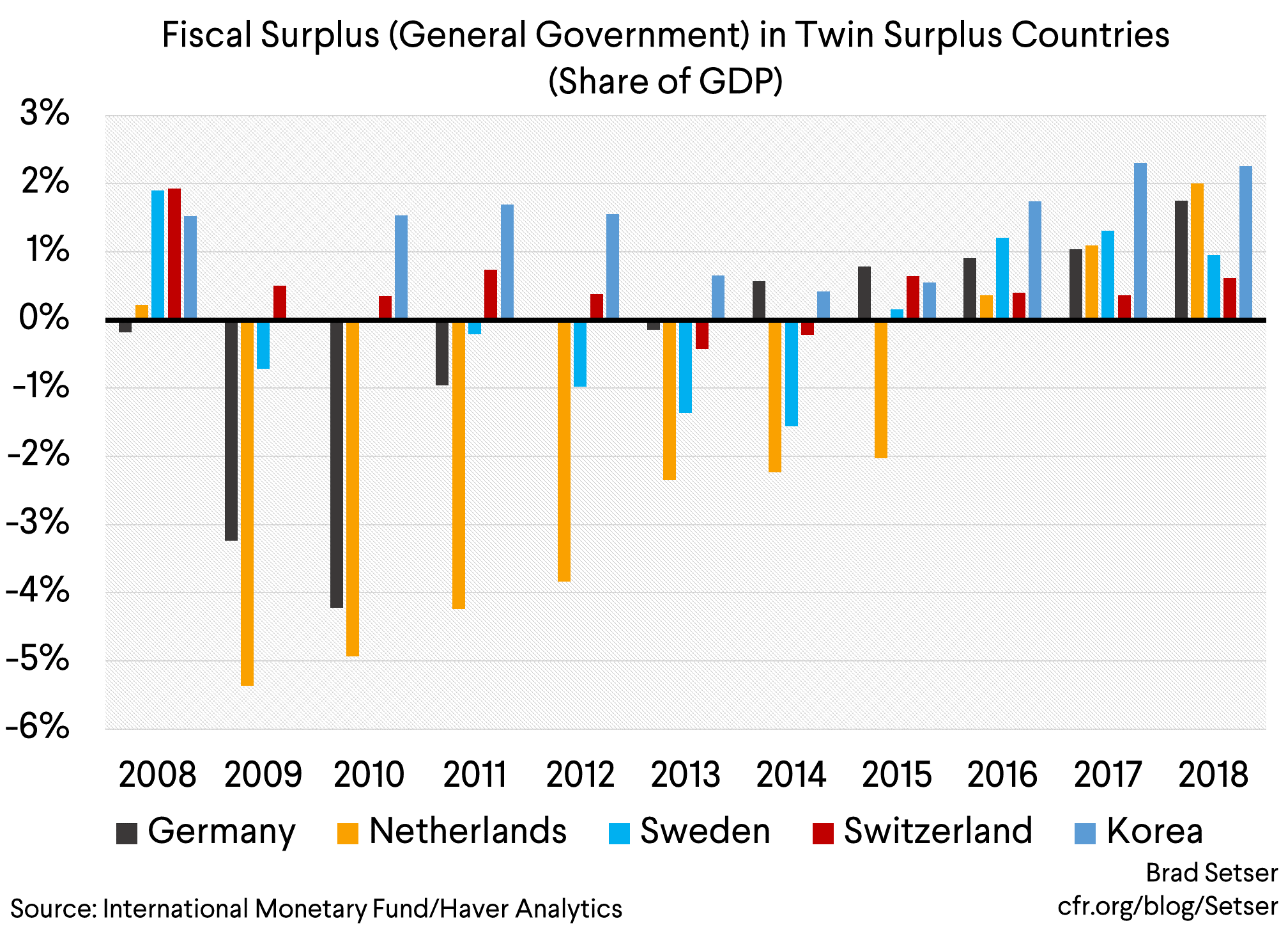

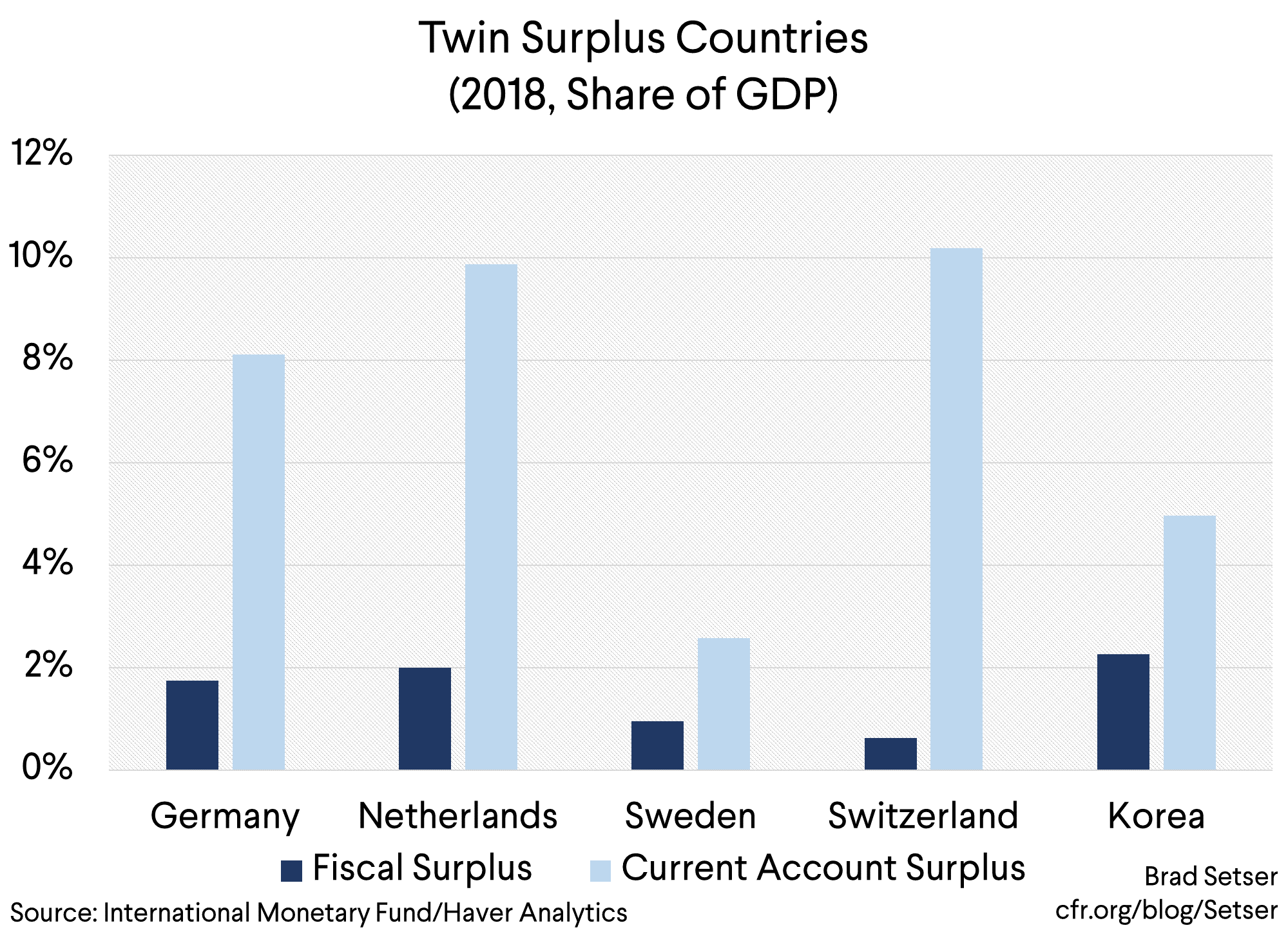

And there are a set of countries that rely heavily on manufacturing exports and that have large current account surpluses and that also run large fiscal surpluses. Korea’s general government fiscal surplus has been over 2 percent of its GDP for some time now (see the IMF’s WEO data, or the OECD’s data). Germany’s 2018 fiscal surplus looks to have increased to 1.75 percent of its GDP. The Netherlands fiscal surplus is likely to be 2 percent of Dutch GDP; revenues have outperformed (probably intentionally understated) expectations.

Sweden and Switzerland also run fiscal surpluses along with large external surpluses.

The fiscal surpluses of the twin surplus countries are now about as big as they have ever been, so just bringing these countries fiscal surpluses down to zero could provide a helpful bit of incremental stimulus to the global economy. Personally, I think most could run small deficits (they generally have low debt levels, and maintaining a constant debt to GDP ratio and thus a constant supply of “safe” assets for their economies would imply modest ongoing deficits). But that’s a fight for another day—a complete reversal of the recent move up in the surpluses of Germany, the Netherlands, Korea, Sweden, Switzerland and a few others would be sufficient on its own to provide a helpful impetus to a slowing global economy.

And a bit of insurance against a new Trump trade surprise as well.

These ideas aren’t exactly new. But China has been remarkably slow in building out a modern, national system of social insurance (benefits are still too tied to hukou in many cases) and has resisted significantly increasing its spending on public health (it also collects too little in income tax, but that’s also a problem for another day).

Germany, the Netherlands, and Korea have all done “fake” fiscal stimulus in the past—selling small increases in public spending as “stimulus” to appease their trade partners even as revenues rose by more than spending, and thus their overall fiscal surpluses continued to rise.

But with the free ride from rising U.S. imports potentially coming to an end and flagging domestic growth, there is really a compelling case for the surplus countries to be a bit less fiscally tight.

And with China slowing, the time has come to do a consumption—rather than investment—focused stimulus.

Sometimes simple, straightforward policy recommendations are best. It is time for the world’s manufacturing exporters to step up and take the steps needed to do a better job of generating the demand for the products they produce internally.

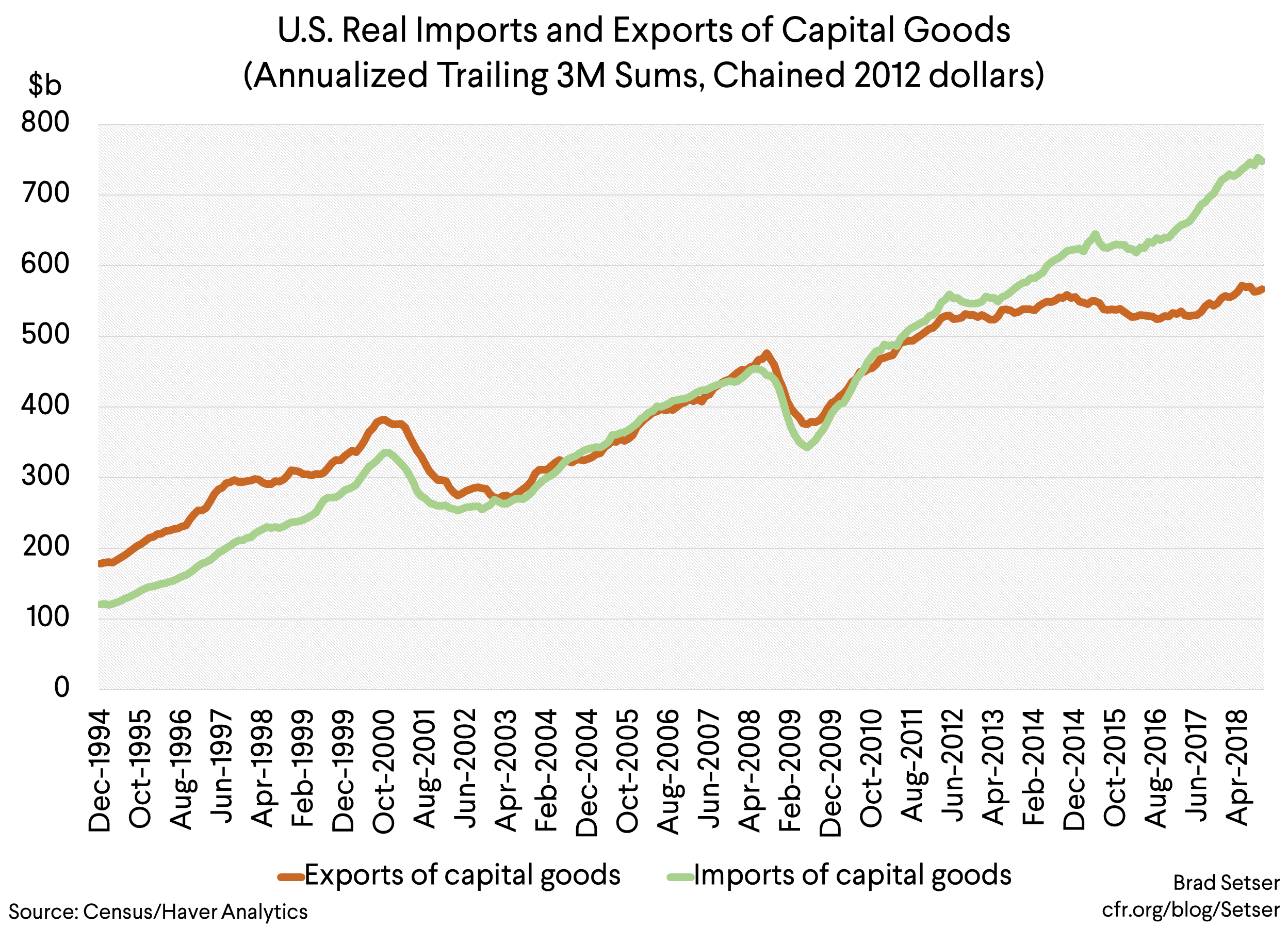

* A look at real capital goods exports versus real capital goods imports tells the basic story relatively well. The actual numbers for q4 won’t be out until the government reopens. My estimates are based on the data through q3.

** The IMF used a slightly higher number in its EBA (external sector) modelling. Spending on public health turns out to have a large impact on the current account and thus is an important variable in the IMF’s workhorse external sector model.