By experts and staff

- Published

Benn SteilCFR ExpertSenior Fellow and Director of International Economics

Benn SteilCFR ExpertSenior Fellow and Director of International Economics- Benjamin Della RoccaAnalyst, Center for Geoeconomic Studies

U.S. tariffs cost China about $35 billion in export receipts for the first half of this year, and—even if so-called Phase One talks succeed—are set to continue sapping revenues well into 2020. Meanwhile, China’s own retaliatory tariffs have boosted food and other prices, squeezing Chinese consumers. The trade war, in consequence, has helped push Chinese GDP growth last quarter to its lowest level in nearly three decades, and the OECD is forecasting even larger drops next year.

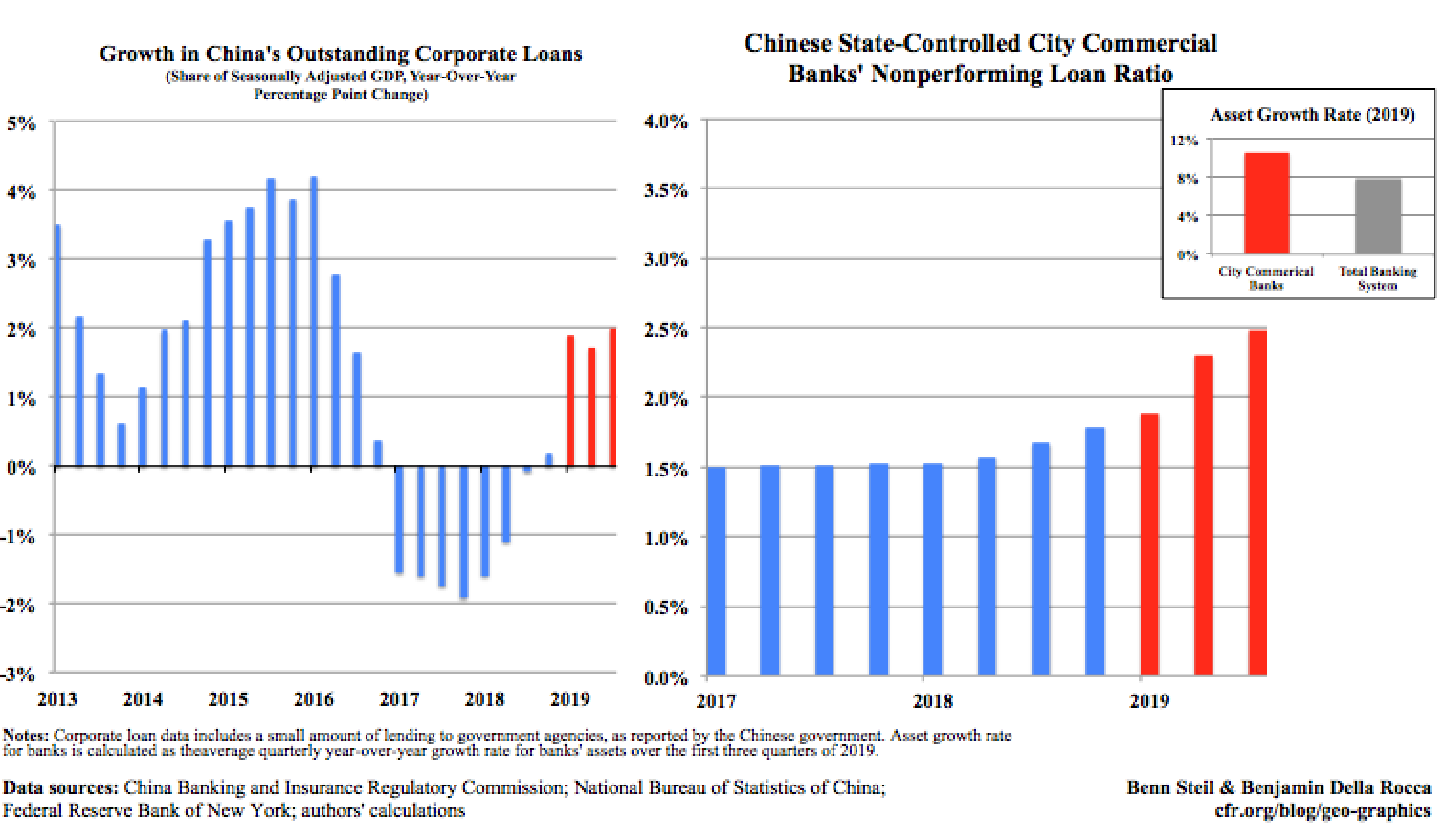

To keep growth from falling below the official 6–6.5 percent target, the government has turned to its favorite tool—boosting debt. It is now back to its highest level since 2015, in spite of Beijing’s stated commitment to rein it in.

The state’s fingerprints are all over the new lending boom. As the right-hand graphic above shows, non-performing loans at so-called City Commercial Banks—state-controlled banks that lend to local businesses and governments—have soared. The result is that Beijing’s determination to keep growth over the magic six percent mark—stressed even on official Chinese Ministry of Foreign Affairs social-media accounts—is accelerating the country’s path to debt crisis.

What should it be doing instead? It should be doing more to end the trade war. Whereas the Trump administration’s import-target demands are wholly misguided, and should be resisted, many of the structural demands, particularly those related to SOE supports and intellectual-property protection, are conducive to China’s long-run economic stabilization and productive relations with all its trade partners. President Xi would be wise to embrace them.