Online Store

Online Store

World Growth Can No Longer Explain Soaring Commodity Prices.

Jeffrey Frankel

Note: This post is from Jeffrey Frankel not Brad Setser.

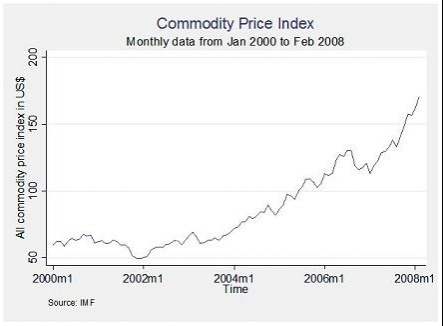

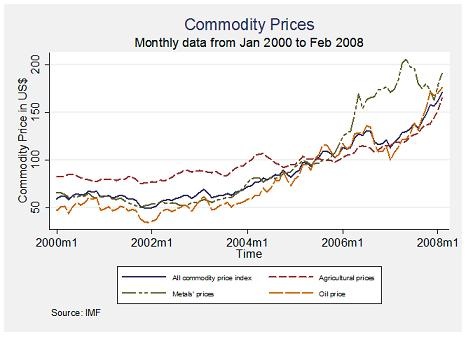

It is hard to remember now, but mineral and agricultural commodities were considered passé less than ten years ago. Anyone who talked about sectors where the product was as clunky and mundane as copper, corn, and crude petroleum, was considered behind the times.In Alan Greenspan’s phrase, GDP had gotten "lighter."Agriculture and mining no longer constituted a large share of the New Economy, and did not matter much in an age dominated by ethereal digital communication, evanescent dotcoms, and externally outsourced services.The Economist magazine in a 1999 cover story forecast that oil might be headed for $5-a-barrel oil.

Since then, of course, we have seen tremendous increases in the prices of most mineral and agricultural commodities, many of them hitting records in nominal and even real terms. Oil is now well above $100 a barrel, and gold has just crossed the $1000 an ounce line.

The question is why.

There could well be merit to many of the explanations that have been offered for the rise in the price of oil; one is the "peak oil hypothesis," and another is geopolitical uncertainty in Russia, Nigeria, Venezuela and - above all - the Gulf. Corn prices have been impacted by American subsidies for biofuel. And other special microeconomic factors are relevant in other specific sectors. But it cannot be a coincidence that mineral and agricultural prices have risen virtually across the board. Some macroeconomic explanation is called for.

The popular explanation since 2004 has been rapid growth in the world economy. The strongest growth has of course been coming from China and other recently minted manufacturing powerhouses in Asia, but the expansion has been unusually broad-based - including up to last year the United States and even a reinvigorated Europe. So growth has pushed up demand for farm products, energy and other industrial inputs, right?

This reigning explanation now looks suspect. Since last summer the US economy has slowed down noticeably, and is probably entering a recession. Despite talk of decoupling, it is clear that other countries are also slowing down at least to some extent. In its most recent forecast, the IMF World Economic Outlook revised downward the growth rate for virtually every region, including China. The overall global growth rate for 2008 has been marked down by 1.1% (from 5.2 % in July 2007, just before the sub-prime mortgage crisis hit, to 4.1 % as of January 29, 2008). And prospects continue to deteriorate. Yet commodity prices have found their second wind over precisely this period! (Up some 25% or more since August 2007, by a number of indices. So much for the growth explanation.

How to explain commodity prices up while the economy turns down? I will offer my answer in my next posting here.

This post also appeared on Jeff Frankel’s Blog here.