Renewing America Series: The Debt Ceiling Fight and the Future U.S. Debt Picture

Event date

From Renewing America Series and Renewing America.

Speakers

- Managing Partner, Lindsay Goldberg LLC; Visiting Professor of International and Public Affairs, Columbia University School of International and Public Affairs; Former U.S. Treasury Secretary (2013–17); CFR Member (speaking virtually)

- Founder, Portman Center for Policy Solutions, University of Cincinnati; Distinguished Visiting Fellow in the Practice of Public Policy, American Enterprise Institute; Former U.S. Senator from Ohio (R-OH)

Presider

- Anchor and Senior White House Correspondent, CNBC; CFR Term Member

As the battle over raising the U.S. debt ceiling continues to take shape, former Treasury Secretary Jack Lew and former Senator Rob Portman discuss the politics surrounding the coming fight, the possible consequences of a default, and the implications of mounting debt for the United States going forward.

TAUSCHE: Thank you so much to everyone who has joined us here in person, and good evening to everyone who is joining us by Zoom, as well.

Our two guests tonight really don’t need an introduction, but I will introduce them nonetheless.

On stage with me is Rob Portman, the founder of the very newly created Portman Center for Policy Solutions at the University of Cincinnati, but you probably know him as the one-time senior senator from the state of Ohio until last—until, I guess, earlier this year.

PORTMAN: Right.

TAUSCHE: Senator Portman, thank you for being here.

PORTMAN: You bet.

TAUSCHE: And joining us virtually is Jack Lew, who is now a managing partner at Lindsay Goldberg. He is also visiting professor at Columbia University. But you also probably best remember him from his time as secretary of the Treasury during the Obama administration. Before that, he was the director of the Office of Management and Budget—so two very esteemed voices to be participating in this conversation about the debt ceiling, which is so topical given where we are in the economic environment right now.

And I’d like to just open it up first for your high-level thoughts about how you believe we got here, and how high the stakes are this time around. And Secretary Lew, we’ll give you the first answer.

LEW: Thanks very much, Kayla, and good to see you, Senator Portman.

PORTMAN: Good to see you.

LEW: How we got here is no mystery. The debt limit gets extended and it runs out. And we’ve known it’s going to run out for some time, and the only real question is what are we going to do about it. You know, it doesn’t, in any kind of fiscal sense, really follow logically that after, you know, you’ve authorized spending money, after you’ve decided what kind of revenue you’re going to raise, that then you have a debate about what your fiscal posture should be. You should have made that decision when you incurred the expenses.

Right now, what we know is the bills are going to come in, and if we don’t raise the debt limit, we’re not going to be able to pay them. And the consequence of that could be devastating in terms of default. I don’t think you’ll probably hear much disagreement in the conversation tonight about whether or not default is a good or a bad idea. Default is a bad idea.

The question is, is it appropriate to use the debt limit as a way to frame a fiscal discussion. You know, I can’t help but go back a little bit in history because I’ve seen the kind of way that the debt limit debate has shifted from a piece of must-pass legislation that you could attach something on to, to an existential crisis where, if I don’t get my demands, we’re going to drive off the cliff and default.

But that’s where we’ve gotten to. Since 2011, it’s been a very different character to the discussion. I think at the moment, given that we have a House of Representatives where the speaker is on notice that if any five members—no matter how extreme they are—say they want to vote of no confidence, he could lose his speakership, the idea that we’re going to drive to the edge of the cliff again, to me, makes no sense. I think Congress is going to need to act. There will have to be some way for that to happen. We’ll talk over the course of this evening what those options are, so I don’t think there is any choice but for Congress to act. And, you know, we can talk a little bit more about whether there ought to be any linkage in any way to other issues.

I would just say, in opening, that you have to distinguish between agreeing to a fiscal policy in the context of a budget and appropriations, and then saying, OK, we’ll extend the debt limit, from a situation where the way it’s set up is, if concessions of certain kind aren’t made, we’re going to default. That’s just unacceptable.

TAUSCHE: Senator Portman, your view?

PORTMAN: Well, first, Kayla, thank you for being here all the way from CNBC, and everybody who is here, both in the room and virtually. We’ve got a good crowd because it’s a major issue. And Jack and I have talked about this a little bit in the last few days. I’m glad to hear him say that you could have some sidecar on an agreement on the extension of the debt limit because that’s all that has ever worked.

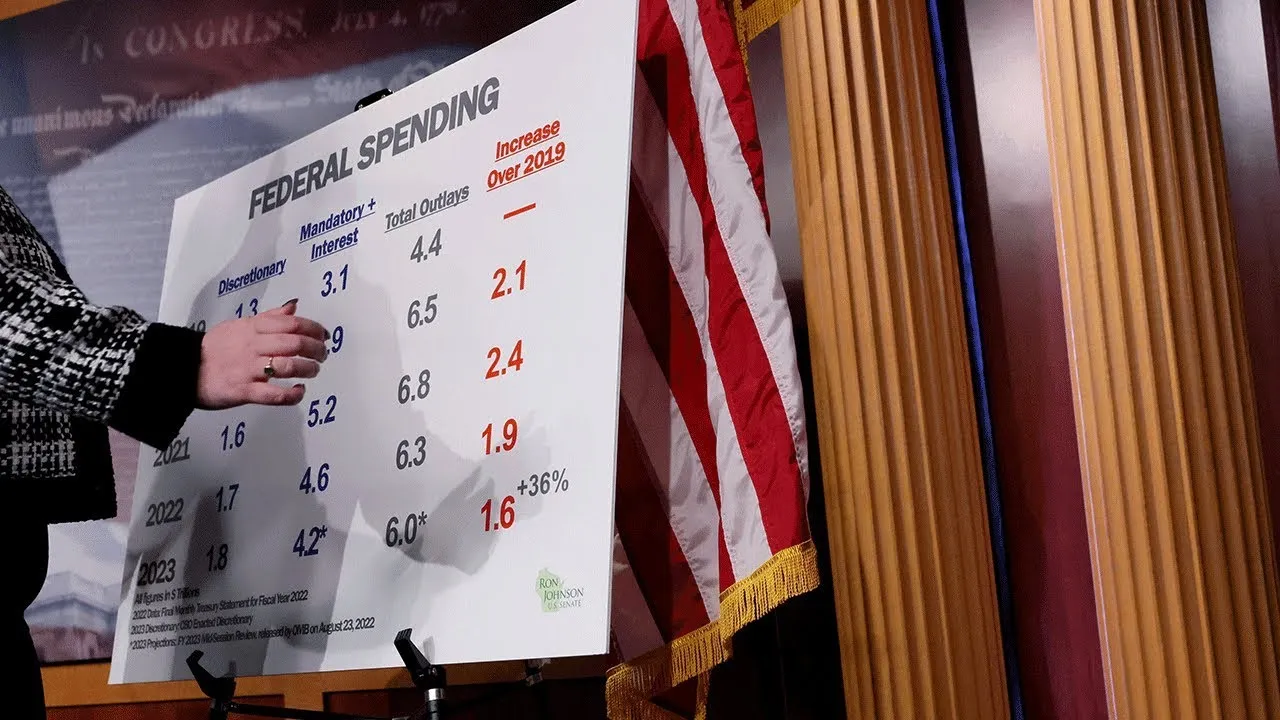

I mean, when I look back on my time at the Office of Management and Budget, and my time even back in the first Bush White House, yes, we were able to pass debt limits, but they were associated with some sort of recognition that the underlying problem is that the debt had grown too large. And certainly now everyone who is listening this evening acknowledges that. I mean, this debt limit is—(laughs)—$31.4 trillion. I mean, we’re at a point where the debt—and talking about public debt alone—is a hundred percent of our GDP. The only time it has been higher was right after World War II. And by the way, those expenses were declining rapidly already, and we didn’t have the issues we have now on the mandatory side.

So this is truly unprecedented, and it is a danger to our future, certainly a danger to our economy. It puts pressure on everything from inflation to interest rates. So we need to do something about the underlying problem.

And again, if you look back, since 1985 until now, there have been eight significant, you know, efforts to reduce spending. One was the so-called Supercommittee on which I sat, which wasn’t so super. But most of the ideas that came out of the super committee ended up getting implemented, one way or another. So all eight of those came out of what process? A debt limit discussion—all eight.

So the notion that we cannot even negotiate—and Jack’s not saying that, and I appreciate his comments tonight—but the Biden administration is saying we can’t even talk about this issue, we can’t talk about the underlying problem; the debt limit needs to be extended no matter what, I think is irresponsible. I think it’s irresponsible from a fiscal point of view. I also think it’s impractical from a political point of view, and that must be considered here.

So three options basically: one is simply extend it without having any changes on policy in terms of spending. The House Republicans, as you know, talked about a lot of different ideas, like to put a cap on the 302(a)s going forward. It wouldn’t happen immediately, of course, but putting it off a little bit, which is always easier. They’ve talked about the TRUST Act, which is this process bill that allows us to look at the Social Security, Medicare, and other trust funds, and come back to Congress with an up-or-down vote, which many of you support it. There is also talk about doing something on permanent reform; not necessarily directly related to spending, but certainly something that Republicans and Democrats can agree on.

But we need to give something, I believe, and that is the second option: to provide some sort of a sidecar that actually gets at the underlying problem. By the way, if we were to follow the first one, which is an extension where the Republican leadership—Speaker McCarthy in particular—accedes to that and allows it to go forward, I don’t believe he could retain his speakership at this point.

TAUSCHE: Well, it seems like Secretary Lew also believes that. He mentioned that in his comments.

But I want to tee off what you said about the Biden administration’s current posture, which is that the debt has been accumulated over a period of two hundred years, that most recently there were clean debt ceiling increases, and so that should be done again.

Secretary Lew, I’m wondering if you think that’s a dangerous position to take, and whether they should be more willing to negotiate with their counterparts.

LEW: Well, first, I think that we decided after 2011 you can’t negotiate with a gun to your head because, even if you don’t tend to go to the limit and pass it, you could accidentally fall off the cliff and default—because we got awfully close in 2011. We were, in the middle of the night, not sure if, in the morning, we were going to be at a place where we had an agreement, or where the market said this is going the wrong way, and we would see a crash.

That can’t happen again. I do think that there is going to have to be a fiscal conversation. I don’t think it should be with the threat of default. Congress will have to agree on what level of appropriations to add, but just to be clear, when they say general things like, we want to freeze spending at 2022 levels—well, what does that mean? If you were to do that and not cut defense, which is what I think I’ve heard them say, and you don’t want to cut veterans, you could be cutting everything else by 20 percent if you are willing to cut things like NIH. If you want to protect things like that, then you have to cut deeper. And what ends up being on the exposed list are things that effect very vulnerable people, things like Women, Infants and Children programs for food and nutrition.

So I think there will have to be a negotiation at some point about appropriation levels. I don’t think that the threat of default if we don’t get cuts—which people don’t even understand in terms of the scale—is the way to do it.

You know, there are ways to frame discussions on issues. You know, I was part of the 1983 process that bought more than fifty years of solvency in the Social Security Trust Fund. It was a bipartisan agreement. It wasn’t in the context of the debt limit.

Andrews Air Force Base, in 1990 in the Bush administration, was not in the context of a threat of default. The 1997 balanced budget agreement was not in the face of the threat of default. I actually don’t think we’ve seen significant budget reductions by threatening default. We’ve seen significant budget reductions when people get together and make hard decisions. If you’re not ready to raise taxes, and you’re not ready to deal with entitlements, there is not a long-term plan and there is not a short-term crisis. We have a crisis—maybe—ten years from now. I think it’s a problem now—we should deal with it. If we could figure out how to have those kinds of conversations again, it would be a lot better for the country than threatening default.

TAUSCHE: Well, Senator Portman, you mentioned a few of the proposals that Republicans have made, but some of the criticism is that it actually wouldn’t save enough money to make a meaningful difference. And as the secretary says, if you’re not willing to raise taxes, and you’re not willing to touch entitlements, how do you get to the levels that Republicans say the government needs to be at?

PORTMAN: Well, first, let me just clarify the record a little bit. I was in the room in 1990 when President Bush made a fateful decision to say, despite his pledge never to raise taxes, that he was willing to work with Democrats—they had the majorities in the House and the Senate—to come up with a budget proposal that would make a difference, and he did. It was Andrews Air Force Base, 1990 agreement. It was in the context of a debt limit, Jack, and a government shutdown, and what happened was that those proposals which were implemented at that time ended up being the major reasons we got to a balanced budget in, you know, 1998, ’99 and 2000.

So, you know, it required the president, the executive branch, in this case, to take a huge risk; in fact, most believe that that’s the primary reason he was not reelected.

Here you have a president who is saying not only is he not willing to take these big risks, but he’s not even willing to negotiate; I mean, to literally sit at a table, like this table here, and negotiate it. Instead, this is being negotiated in public, which never works. So he has asked that, in order to sit down at the table, the House

Republicans have to put their proposals out publicly. As they do that, they are getting criticized, as you’ve seen, politically, and attacked.

So, I mean, look. Both sides—Republicans and Democrats—we’re all at fault here. We’ve gotten ourselves in this situation. But the answer is not to say you won’t even talk.

This is, by the way, not something the American people support. The American people believe he should sit down and negotiate. And they also think spending is a big issue, partly because I think now the American people understand that this inflation that we’re all experiencing—which is something that they feel in their own families, their own kitchen table—is partly as a result of the overspending by Congress because of stimulus spending that, you know, post-COVID that ended up causing this huge bubble and the increase in demand. So they are looking at this and thinking, this spending really does affect me and my family. So the American people are not supportive of saying we’re just not going to talk.

TAUSCHE: Where specific programs are concerned, there is a lot of support. I was interviewing Senator Bill Haggerty a few weeks ago, and he said that one of his proposals will be just to have the Biden administration not go forward with some of the things that it has already proposed, like student loan forgiveness, which would save hundreds of billions of dollars. But that would also have political consequences.

Do you think that there is real low-hanging fruit on the spending side that Republicans could be willing to risk politically?

PORTMAN: Well, I do, and I get back again to the mandatory spending side of the ledger because that’s where, even if Republicans were willing to make some tough cuts on the appropriations side—and I agree with what Jack has said, those would be pretty severe cuts—the bigger issue, as we all know, is on the mandatory side. It’s now 70 percent of the budget. It’s on autopilot. There is no vehicle for us to address this in the appropriations process.

But there is debt limit context, and that’s been done in the past. Again, look at Gramm-Rudman or other proposals like that that came out of the debt limit, 1997 budget agreement. So that’s why, in 2011, Joe Biden, then vice president, went to meet with—after everything else failed—Mitch McConnell, and they were able to negotiate something. And that’s why they focused on the entitlement side and mandatory spending.

So I—you know, the proposal by Senator Hagerty is one. There is another out there that’s a proposal that’s bipartisan. It’s called the TRUST Act. It is sponsored by Mitt Romney and Joe Manchin, and again, it’s simply a process, but it’s an important process because it takes to the Congress this decision: What are we going to do with regard to this totally unsustainable, mandatory side of the budget—again, 70 percent of the budget now, on autopilot, not being addressed in the appropriations process, and the fastest-growing part of the budget.

TAUSCHE: You mentioned 2011. Secretary Lew, you also had a front-row seat to those negotiations. I’m wondering how you view those talks—in hindsight now—if they were as productive as Senator Portman is making them out to be, and if there were real costs to how close the economy came to the brink?

LEW: So, look, to be clear, the real discussions about a balanced approach with everything on the table—taxes, entitlements, and discretionary spending—was the grand bargain negotiation between the president and then-Speaker Boehner, you know. And I was deeply involved in those talks. They came close, but they didn’t get there. We can debate why they didn’t get there, but they couldn’t reach an agreement on what to do about the big pieces, largely because of problems getting the votes for it in the Congress.

And at the point when the vice president—then-vice president—began the negotiation with Senator McConnell, it was about how do we get to the point where we avoid default. It wasn’t about a grand bargain. What came out of it was the Budget Control Act, which was a pretty bad piece of legislation. I had a very strong hand in writing it—I’m not proud of it—but it was a lot better than default.

I don’t know that you could do something like that again. I don’t know that there is another mechanism or gimmick. What I worry about is you get to that eleventh hour, and they don’t even have people around the table who were deeply involved in 1984 when the mechanism was designed. You know, it happened that there were a number of us then who still were. I don’t know how they solve the problem now, and I worry that they’re going to default.

The one thing I will say that was very positive that came out of it, that was apropos of what, you know, Senator Portman said about the super committee, you know, there was a side process where Vice President—then-Vice President Biden and then-House Majority Leader Eric Cantor went through what is kind of called “other mandatories”—the littler things than Social Security and Medicare. And they came up with several hundred billion dollars of ideas that, over time, did happen. So things did come out of it in that sense, but we didn’t deal with Social Security, Medicare, or revenue coming out of that discussion. And we almost defaulted. It would have been a catastrophe if we defaulted.

And I’m happy to talk about even what happened approaching the line cost a lot. You know, in 2013, when it was a lesser level of national frenzy than in 2011, you know, interest rates went up on the ten-year Treasury bill, you know, by something like six basis points. Five basis points over ten years costs almost $25 billion. That’s just money burned. And if you had a real default, if you had a non-payment event, we don’t know what the size of the impact would be, and it could cause a major economic shock.

TAUSCHE: Senior officials have told me, though, that the rubber won’t actually meet the road on this debate this time around for at least another few weeks; that the Treasury will have to disclose another X date, which is the date by which their extraordinary measures would be exhausted. And they won’t know that date until the tax receipts come in later this month, and they know exactly what the government is making in terms of revenue.

So at what point, Secretary, do you see these debates actually starting to become more substantive, either within the administration or within the Republican Party.

LEW: So, Kayla, I think, first, in April, when the tax revenues come in, it is the best clear moment when you have an idea about when the deadline is. You still don’t know; there’s huge amounts coming and going every day.

And when I was Treasury secretary, I got daily reports with a range of options where you could easily make a mistake if you picked the wrong point on the spectrum and said, that’s when the deadline is. They just don’t know it that precisely because of the way the demand for payment is made on things that are out there in the system already, and the rather unpredictable way the revenue comes in after the major tax filing date.

You know, I say this without any intention of disrespect—because I grew up in the House and the Speaker’s Office, and I love the institutions of the Congress—Congress always wants to know the last minute to act. This is a dangerous subject to drive to the last minute because you could get there before you know it, and Congress can’t always act that quickly. You know, I’ve heard people talk as if discharge petitions work in a heartbeat. It takes two months to get a discharge petition. If you have a political challenge in the House of how do you get a bill to the floor, the Speaker is the only one who can take a bill to the floor. And if I were kind of in the middle of the conversations now, I would say, how do you speed up the conversation on the not-debt-limit issues—unrelated to the debt limit? They have an appropriations process. Start talking about what the appropriation levels should be, and then see where it gets you. Don’t link it to the debt limit where you are demanding things you can’t get.

TAUSCHE: It’s sort of like the inverse of that old saying, “Hurry up and wait.” In this case, it’s wait, and then hurry up.

PORTMAN: Yeah, but it shouldn’t be.

TAUSCHE: But how do you instill some urgency?

PORTMAN: Well, one way you get it started is you have a negotiation. So here we are, only several months from the deadline. I believe the Treasury is now saying possibly in June. Other economists are saying, as they look at it, more likely at the end of August. We’ll see. Extraordinary measures will probably be used to push it back into the late summer, maybe even early fall if revenues come in, as Secretary Lew says, higher than projected.

But let’s get started now—I mean, absolutely, I couldn’t agree more. But how do you get started when the White House is saying they simply won’t sit down to even talk? I mean, we need to start the discussions right now. They are on a two-week recess right now, so I guess that’s, you know, two more weeks lost, but they can’t get started unless you have the players at the table, and the players has to be the president. The president has to do what other presidents have done, and he did as vice president, which is to go talk to the Congress, find out what’s possible, what’s practical, and deal with the underlying problem while you’re dealing with this debt limit.

Of course it has to be extended. You haven’t asked me this, but I don’t think that there is any way to prioritize, by the way. I understand why a lot of Republicans think that’s an attractive option. But I think it’s impossible at the end of the day to have that be sustainable, for obvious reasons—how do you choose between Social Security, Medicare, and Veterans, NIH, and so on—but also because I think the politics of it aren’t great that you are protecting bond holders rather than your own constituents, and in a way they become—you’re protecting China rather than your own constituents. I don’t think politically that’s sustainable.

So I think the best option here is to start the discussion and let’s find out what’s possible and do something about the underlying problem. The American people are demanding that we do something on spending. They don’t necessarily understand all the details of all these programs, and as you say, some of them are quite popular. But they do understand that it’s out of control, and it’s hurting the economy, and will hurt them and their kids and grandkids if we don’t do something about it.

TAUSCHE: And we’re going to talk a little bit about those levels into the future, but Secretary Lew, is it your read, when you speak to members of the administration—which I know that you still have an audience with many of them—that they truly believe they will get a clean debt ceiling increase if they just wait long enough and hold Republicans’ feet to the fire, and hope that they come up empty? Or is this a negotiating strategy ultimately?

LEW: I haven’t heard the administration say they won’t negotiate fiscal policy. I’ve heard them say we’re not going to negotiate over a debt limit, we’re not going to negotiate with a gun to our head. And I think those are different things.

There are ways to have a conversation with Congress about spending levels. You don’t have to tie it to a catastrophic event. I don’t know what it takes to navigate the House. You do know that there are enough votes in the House to pass a debt limit. I think I’ve talked to enough Republicans in the House, you know, with Democrats who would vote for a debt limit.

This is a question of the politics in the House, and I agree with Senator Portman. It’s not a great thing to have a speaker have to choose between putting something on the floor and losing their leadership. But the job of a leader is to navigate that and to figure it out. And I think the idea of setting up the notion that if you sat down and negotiated over the debt limit—I haven’t seen anything on the House Republican side that suggests there is an end there that could be the meeting of the minds. And, you know, they are going to have to do preparation bills. They are going to need to start soon if they want to go to the regular order, and the sooner they get started on that negotiation, the better. You know, it doesn’t have to happen today or tomorrow, but it shouldn’t be June, July, August before they get to it. We shouldn’t get that close, because even as you approach the deadline, there start to be consequences.

And one thing I’ll say about prioritization—which I totally agree with Senator Portman—it just doesn’t work. This may not be a satisfying thing in terms of the condition of our systems. You don’t have the ability to say: On a given day I’ll pay A, B, and C, but not X, Y, and Z. The systems don’t work that way. There are a lot of them that they’re on, or they’re off. And if you have to wait until you can turn one of the systems on to pay everything, you might be waiting a little while if you’re close to the deadline. So this is a complicated business. And I also totally agree with the notion of it not being tenable to say we’re going to pay bondholders but not people and businesses that the government of the United States owes money to. It’s just choosing different forms of default.

TAUSCHE: And at a practical level, it seems that even behind closed doors, there’s some admission that that’s not a realistic strategy. But we’ve talked so much about House Republicans in this conversation. And, Senator, I want to get your take on what you think the role of the minority leader, Senator Mitch McConnell, should be in this, because he has participated in so many of these—in so many of these increases over the last several decades. And, you know, he would seem all too happy to let Republicans in the House figure out their own position before he gets involved and figures out what the Senate can pass. But do you think that that he should play a bigger role in these negotiations, given his role in the past?

PORTMAN: This is a very sensitive issue, because my friend Mitch McConnell would prefer to allow the House to act, understandably. I mean, they have a majority in the House. He doesn’t. And he could negotiate something with the White House that the House Republicans could reject. And to Jack’s point that he’s talked to enough Republicans that think something would pass the House, I don’t think there’s a single Republican who’s off the reservation at this point in terms of saying we’ve got to get something for this. I think it’s a—whether you’re a moderate, or a conservative, or somewhere in between, libertarian, vegetarian, whatever, Republican, you’re on the same wavelength on this one. So I don’t think Mitch McConnell wants to get involved in that.

However, he’s incredibly effective when he does, because he knows the facts. He’s very straightforward about it. He knows what the politics are better than anybody.

TAUSCHE: He knows the president very well.

PORTMAN: He knows the president. He knows what the, you know, possibilities might be with the White House. So eventually, I think he can be a very important part of this. But at this point, I believe he’s taking the right approach, which is to say this is really about the House majority, and seeing what they are comfortable with. If they’re comfortable with something, then the votes will be there in the Senate.

TAUSCHE: When you talk to your other former colleagues in the Senate, do they feel that this time is different? Or do they feel like this is just another moment in history repeating itself?

PORTMAN: Well, I talked to one of my colleagues today, actually on the Democratic side, and I think his view was more déjà vu, all over again, as you were saying. In other words, we’re just going back through the same process again. And this is why my view is let’s speed it up and get to the negotiation and come up with something that actually makes sense.

I’ll throw out one idea which probably nobody supports, because commissions now are viewed as reports that collect dust on the shelf.

TAUSCHE: Why not? Throw it out.

PORTMAN: But let’s go for another Simpson-Bowles, but this time, make it different, make it one where you actually take a proposal back to the House and Senate for an up or down vote. And so it would have to be a statutory recommendation, which it wasn’t last time, you recall. We tried to do that in the House and Senate. We were unsuccessful. But, you know, it would have to be something where members of Congress were

engaged and involved, and probably the leadership of Congress. But you know, this is a time where I think everybody realizes we have to do something. If not, within less than a decade probably, we’ll be a $2 trillion a year on deficits.

I mentioned the 100 percent of GDP debt already. You reminded me that by 2050, it’ll be like 137 percent. Is that what you said?

TAUSCHE: 217 percent.

PORTMAN: 217 percent. That’s not fathomable. I mean, this is—this is the eyes of the world—

and Jack talked about how the global community reacts to all this—you know, this is essentially bankruptcy of the United States of America unless we get hold of this. So I do think, again, it’s just a process, but it’s an important process that could be part of this, and could have the statutory authority to be able to take something to the House and Senate for an up or down vote, Congress would still have the opportunity to vote it down. But it would give us a chance to try to come up with the grand bargain that has been missed time and time again. And if we don’t do that, I think we failed our kids and grandkids at this moment.

TAUSCHE: Secretary Lew, what is your best idea that you would put on the table for anyone who might be involved in these negotiations who might get their hands on this transcript?

LEW: Well, I think it takes a certain amount of creativity to make it possible for all of the

parties to take the actions they need to take without having broken their kind of fundamental core principles. That’s kind of how any negotiation works if there’s an agreement, I think the idea of setting up a negotiation over the debt limit is unlikely to lead to a very good outcome. Because I think it creates a false impression of how much leverage you have. I think changing the subject and getting into a conversation about the things that have to be decided this year, and then after that figuring out what your pathway is to navigate to the debt limit, would be better. Now the problem is, the deadlines don’t help you. We may have a debt limit deadline before the end of the fiscal year. Congress knows how to reschedule things if they want to.

If you go back to 2011, you know, we dealt with the immediate spending issues. We then faced near default without a spending issue. And it actually was a lot harder. You know, appropriating, keeping the government running, Congress knows how to do that, administrations know how to negotiate that. And in the end, if you reach an agreement on what the funding level for the year is, it lowers the temperature on other things. I don’t hear any discussion about that, to speak of. And I worry that coming first the debt limit in the summer, it could go off the rails. And you know, I’ve seen very often that you end up in places you didn’t mean to be, but you don’t normally end up in the place you said you would never be. And so we—call it a sidecar. Call it doing the regular order. Kind of changing the subject and figuring out where you can reach some agreement would to me be a sensible course.

TAUSCHE: But the president did release his budget just a few weeks ago, and there will be an appropriations process that gets underway. In 2024, in fiscal 2024, Secretary, the White House proposed a 9 ½ percent increase in discretionary spending. What do you think an appropriate level for that is, if not the level that Republicans have laid out?

LEW: Look, I’m not close enough to the numbers to say where the right level today is. I do know that when you talk about numbers that sounds simple, like freeze at X level, you have to ask the hard question, what is the consequence of that? What will the impact be? I know some of the people I sat across the table from over the years thought it was tiresome that I asked that question. But that’s the question that you need to ask: What does it mean? What will it—what will it require you to do? If you’re not prepared to take the actions that come after it, you can’t agree to it. It doesn’t work. There is some level of slowing the rate of discretionary spending that I think the sides could agree on. I can’t tell you I know exactly what that number is. I don’t think it’s a freeze at

’22 levels, protecting defense and veterans, because I think, you know, even Congressman Cole on the Republican side acknowledged this in an appropriation hearing last week, you know, where he said it’s a legitimate concern to worry about whether the level of reductions would be on the order of 20 percent. So, I actually think Republican and Democratic appropriators alike care about the consequence of where these numbers are. I mean, they, contrary to popular opinion, actually go line by line and work really hard and try to come up with workable funding levels. I don’t think you can have an abstract discussion that doesn’t give them the ability to do that.

So it’s not a simple answer to your question. I don’t think it’s a formulaic thing like that. There will be savings. And look, the problem is, I think the amount they could agree on savings would not meet the demands of everyone in the House Republican Caucus. I don’t think there are savings at that level to be realized this year, which is why expectations have to be set more realistically.

TAUSCHE: Senator.

PORTMAN: So what the appropriators say not just that, you know, they work hard in account by account and try to come up with something sensible; they say, why are we doing all the work? (Laughter.) You know, 70 percent of the budget is on autopilot. You’re asking us to take the 30 percent, more than half of which is defense, and make all these cuts? So it gets back to the point we made earlier. I mean, when mandatory spending is 70 percent of the budget, this is incredibly important programs, but not sustainable in their current form. And Jack said earlier that we’re not really in a crisis yet. I mean, I think as a Social Security beneficiary, now that I’m over sixty-five.

TAUSCHE: It was hard for you to say but it’s okay.

PORTMAN: Yeah, I was thinking, you know, I should have said sixty-two. But I mean, look in less than ten years, we’re talking about a reduction under law of about 24 percent in benefits. We can’t have that. Of course, people say it won’t happen, Congress will change it. Well, you know, let’s have this discussion, because the appropriators are frustrated. They’re trying this year to do a process—and I really appreciate that—so we don’t end up with a continuing resolution again, which is so inefficient for government, including for defense. And so instead, let’s have a plan. I think Patty Murray and Susan Collins on the Senate side are sincere about this. I support them strongly. But they need to know what the parameters are here. And is anything going to happen on the 70 percent side? Are you going to have it all taken out of the discretionary side at a time when, again, more than half is defense—it may be up to 60 percent—and at a time when we face not unprecedented—we’ve had a cold war. After all, we’ve had world wars, but a very serious global challenge now from China, from Russia, from Iran, from North Korea—I mean, it’s just too much to ask them to do. And this is why I say we’ve got to back up and figure out how do we have a real budget and a process. And I mentioned having the commission do it. Another idea is simply to say, let’s have a process in Congress where there is a vehicle to address this. Let’s have a whole budget where everything is put together. That’s a budget process reform that could come out of this, at least to look at these numbers and understand where we are.

I see the Committee for Responsible Federal Budget is here. I think you guys would agree that would be very helpful to at least know where we are as a country in terms of our spending.

TAUSCHE: And I think that’s a great segue to where we are in our program right now, where we’re going to be taking questions from CFR members both in our audience here in Washington, and who are joining us virtually. We’ll start here in the room in Washington.

We’ll start here in the back. I saw your hand first.

Q: Thank you both for your time. My name is Jamaal Glenn. I’m a technology startup investor.

So we’ve been asking this will we/won’t we recession question for what feels like the better part of the year. We’ve seen historically steep rise in interest rates, which led to a

relatively short-lived banking crisis that I think is contained but not—I’m not convinced is fully resolved. And I think there’s a looming commercial real estate issue on the horizon. So my question is, to what extent, if at all, does this broader macroeconomic context fit into this debt ceiling fight?

TAUSCHE: We’ll start with Secretary Lew with that one.

LEW: Yeah, thanks, Kayla. Look, I think the current situation, macroeconomic situation U.S. globally is as uncertain as any that I’ve ever seen. We’ve seen how small things can create outsized consequences. You know, a change of tack of budget policy in U.K. triggers a pension crisis. You know, the failure of a bank, you know, relatively medium-sized bank, sets off a risk of systemic runs. I think that’s a very dangerous environment to be approaching potential default of what is considered the definition of risk-free debt in the world, US Treasuries. So I actually think it raises the stakes not to make a mistake this time. You know, I think, you know, whether we’re going to have a recession or not have a recession, I think it’s pretty safe to say that if we were to default, it makes the odds of a recession, almost certain. You know, Mark Zandi’s estimate was we’d lose 4 percent of GDP if we had a sustained recession. I don’t know if that’s right. It certainly moves the needle in the wrong direction. It just means it’s a very dangerous time to be going through this kind of brinksmanship.

And, you know, I just would—kind of going back to the last comments that Rob made, you know, I’m forever proud of having worked on Social Security reform in 1983 and on multiple rounds of healthcare savings that have helped Medicare over the years. I think we need to have conversations to make those systems sound. I don’t think you’re going to see that in the context of a threat of default. It’s going to have to come in some other contexts where people take the temperature down and are looking at something that’s a little closer than ten years out. I wish we could have done it when it’s fifteen years out. You know, it would be better to do it farther and away from the deadline. But I think it’s not the thing that is driving the current debt limit, and it’s not the answer to avoiding default.

TAUSCHE: Senator, how do you see macroeconomic conditions impacting the debt ceiling and vice versa?

PORTMAN: Well, Jamaal, I think you’re right. At least I infer from your question that you think we’re in an uncertain time right now with regard to interest rates, inflation. And even the banking crisis, which I agree with you is—it seems like we have resolved that issue, but there’s sort of bubbling underneath some uncertainty. So it’s—I don’t disagree with what Secretary Lew said. All the more reason, though, for us to do something on the spending problem, because if you look at how the bond market would react, you know, how the equity market would react for that matter, I mean, people are really nervous when they look at these numbers. So you take the debt limit from 31.4 trillion up to 30-some trillion, and you’re looking at, again, this notion that our debt is going to be bigger than our whole economy this year? So it is it is truly frightening.

And to Jack’s point, look, I get it. We don’t want to go over the debt limit. But it’s all that has worked. And there’s no other vehicle or mechanism for us to look at 70 percent of the budget and the fastest growing part of the budget. So why wouldn’t we? Let’s take this opportunity to do something that actually positions us better for the mid and longer term. And, you know, again, people can say it’s not a crisis. It’s right around the corner. I mean, it’s—you know, the Social Security actuaries just changed the date, I think, to 2033 from 2034, for when the Old-Age and Survivors Trust Fund is belly-up. So I mean, we’re here, folks, and we should do something about it, and this is an opportunity.

TAUSCHE: We’re going to go to a virtual question now.

OPERATOR: We will take our next question from Meena Bose.

Q: Thank you.

Both speakers have discussed the difficulty of having these discussions in public. I believe Senator Portman said that it’s very difficult to have budget debates and conversations in public. Secretary Lew just spoke about the importance of having conversations of ends and means. Given the nature of the near impossibility of having private discussions today, would both of you comment on how we move past, after this current crisis, how we have a real long-term conversation of what our budget priorities are and the resources to meet those priorities in the next few decades?

Thank you.

TAUSCHE: Senator Portman, we’ll start with you this time.

PORTMAN: Oh, well, I—it’s a great question. And I agree with you that it’s hard to do anything privately these days, partly because people have their iPhones with them in the meetings and immediately tweet something out. But it’s not impossible. And I think Jack would agree with me that during the discussions on the grand bargain, there was a lot of confidential back and forth. Now and ultimately, the backstop was Senator McConnell and Vice President Biden. And again there, there was there was a lot of very, you know, sensitive information shared that didn’t go public. John Boehner’s book did talk a lot about the grand bargain. So it comes out eventually.

But I think there’s an opportunity to have an adult conversation. There has to be. If we’ve gotten to that point in our democracy, we’re in really deep trouble. So I don’t—I don’t think that’s impossible. And I think it has to be at the highest level. And it has to be, you know, a discussion about all the—all the spending, not just the appropriations process, which is again, 30 percent of the spending, more than half of which is defense spending, but we have to look at everything and have an honest discussion. So, I would not be as negative about those prospects.

TAUSCHE: Secretary Lew, your response?

LEW: So, I mean, I think it’s a great question. But I have always been an optimist. And I have to believe that if not now, there will be a moment when those kinds of conversations can happen. In 1981, ’82, ’83, we thought we were living in the most partisan moments known to man, and we found a way to negotiate Social Security through a trusted third party. And the commission was actually a front for negotiation between the president, Ronald Reagan, and the speaker, Tip O’Neill. I don’t know what the mechanism right now is. But I think the leaders are going to have to figure out what it is.

The thing that is going to have to happen for there to be a conversation about broader fiscal policy, though, is it’s not just going to be about discretionary spending. I agree 100 percent with Senator Portman that you can’t solve this problem that way. But you can’t do it just by talking about entitlements. You have to talk about revenues. You have to overcome the unwillingness to talk about what’s the right level of revenues to support what we need for this country. We’re stuck now that you can’t talk about revenues. Until you can talk about both revenues and entitlements, you’re not going to get anywhere.

What makes me hopeful is that I don’t think anyone’s going to be prepared to let Social Security and Medicare ever go off a cliff, so we’ll get to the moment when you can have a conversation about a balanced approach. It only happened in 1983 because we were months away from not paying full Social Security checks. It was not ten years away. It was months away. I don’t think we should let it get that close. But I don’t think you have to treat it being ten years out as being a crisis such that we should threaten the possible default of the United States.

TAUSCHE: 2033 will be here before we know it, though.

We’ll take another question from the audience right here. And please introduce yourself.

Q: Sure. Thank you very much. Tom Kahn from American University. Hey, Jack.

Question is—and Secretary Lew referenced it earlier—clearly, if there are going to be any serious negotiations and Democrats are going to agree to significant mandatory adjustments, it’s going to require both sides of the ledger, which means revenue increases. Senator Portman earlier referenced President George Herbert Walker Bush was the last Republican president who agreed to revenue increases and then his defeat in 1992. Is there ever a scenario where Republicans would agree to revenue increases? And I think back on the super committee and Simpson-Bowles were that that was really a high obstacle to overcome.

PORTMAN: That’s me, Tom?

Q: Yes, sir.

PORTMAN: So Tom was a witness to the super committee not being so super. I think you were Iron Man. Or was that me? We all became caricatures.

But, you know, as you know, we did have discussions on entitlements and on revenue. And we did have some proposals, including one that was proposed by members of my party, others proposed by Democrats. And, you know, I think that’s acknowledged, that if you’re going to do what you have to do in terms of righting this fiscal ship before it’s too late, there’s going to have to be some on both sides.

What it is exactly is, of course, another issue. And when George HW Bush made the agreement to do it, he only did so with, you know, getting serious commitments on the spending side. Later, he believed that some of those were not met. But as I said earlier, it did form the basis of the success and—at the end of the ‘90s. And capital gains helped too, because remember, the capital gains cut went into effect and $100 billion showed up, which seems like nothing today—that was a lot of money back then—that no one expected. So I think you’re right.

And I mentioned earlier, let’s take this opportunity to establish another process that truly looks at the whole picture and is balanced and comes up with an answer and goes back to Congress for an up or down vote. Congress would still have it say, but we would avoid it being nickeled and dimed and made too political. The far right and the far left are not going to support it. You go into that, knowing that’s going to be the case. But you also go into that knowing that this could actually prepare us for the next few decades and not put us in this constant peril of where we have these debt limit discussions and we come up to the edge and, you know, cobble something together at the last minute. And it puts our country economically in a much stronger position. So yeah, I don’t disagree with you, Tom. But I think it’s got to be something that has buy-in from the leadership of Congress.

TAUSCHE: And, Secretary Lew, I know you touched on revenues in your prior answer. So we will move on to the next virtual question as well.

OPERATOR: We will take our next question from Sue Cobb. Miss Cobb, please accept the unmute. You seem to be having technical difficulties.

We will take our next question from Dee Smith.

Q: Thank you very much, everyone, for such an interesting discussion. I’m Dee Smith in Texas, CEO of Strategic Insight Group.

And my question is, I guess, primarily for Secretary Lew, although I would be interested in everyone’s take on it. And that is concerning the idea that the Treasury could mint a $1 trillion coin. Is that a serious possibility, do you think? And what would be the consequences, the effects on the dollar, the effects on faith in the U.S. government, and so forth? Thank you.

LEW: So, you know, I think the kinds of things that you have to think about when you’re approaching default stretch any reasonable definition of credibility. You have theories that might work, might not work.

I can tell you when you walk into the president of the United States and one of these ideas is on the table, the risk that it might not work is a very heavy burden. And the risk that you lose your seriousness if you try is a real consequence. I don’t think any of these things are good solutions. I’m not going to give an absolute answer. There are no absolute answers. I mean, I know what my opinion was at the time. I know what—you know, what the decisions were at the time.

You know, the idea of default is unthinkable, and it puts presidents in positions where they have to think about things that is almost ludicrous for presidents to be thinking about, which is why you need to reframe the debate so it’s not around the cataclysm of default.

I don’t disagree with Senator Portman that it’s hard to frame serious conversations about hard issues. It’s not easy to have a discussion about a problem that’s ten years away. But I don’t think, you know, the solution is for us to kind of pretend that there are easy things like a magical coin that solves the problem. The only real way to solve this problem is for Congress to act. It says in the Constitution that Congress has the power to borrow. And the deadline was meant to simplify that. It obviously has become far from simple.

TAUSCHE: To put a finer point on it, Mr. Secretary, did you at any point propose minting a trillion-dollar coin to President Obama?

LEW: I always believed that any of the ideas that were kind of fringe ideas were very risky. I’m not going to say with absolute certainty what you can and can’t do. I wouldn’t recommend taking those risks.

TAUSCHE: All right. We’ll leave that there.

Do we have any other questions in the room? All right, we’ll come here to the front.

Q: Hi, Senator Portman, Secretary Lew. Thank you for joining us today. My name is Laura Temel at Bank of America.

One comment, Senator Portman, that you made, made me a little nervous that, I guess, representatives were thinking that this was like déjà vu. And I guess my question, are our representatives being too complacent right now, if that’s the attitude?

PORTMAN: Well, I mean, it depends on which, which body and which side of the aisle we’re talking about. But Republicans are focused on the fact that the administration won’t even talk about a negotiated way out of this to have some sort of a proposal or set of proposals that deals with the underlying problem. And they have put some ideas out there, as you know. So they feel like, you know, they’re putting out constructive ideas.

Some are, you know, pretty, pretty tough to implement in terms of the caps on discretionary spending. Joe Manchin, who happens to be a Democrat, has a proposal that you have a 1 percent increase in appropriations going forward for a period of time. So it would be a slight increase. The question always is, what is the base, you know, what do you start with? He would probably start with a little higher base than Republicans would in the House, but those sorts of ideas are out there.

So I don’t know that they’re complacent. I think they’re discouraged and wondering, how do you engage, how do you have a discussion if one side won’t even come to the table? Because this is the debt limit, therefore, we can’t talk about it. And again, in the context—and I—Jack and I may have a disagreement on this. But when you look at, you know, from Gramm-Rudman up to now, all that’s ever worked is having this debt limit discussion. There’s no other vehicle to have this discussion. So I think that’s where a lot of Republicans are.

Democrats, I don’t know. I told you I’d talked to a colleague today who said it’s déjà vu all over again. I think some of them also are waiting to see what the White House ultimately decides. They believe that the current position probably is not sustainable. At some point, there has to be a discussion. And they’re eager to know what the parameters will be of that.

So I think it’s mixed, you know, depending on which chamber and in which party. But look, it needs to have a sense of urgency now, because Jack is right. Some of these things take a while to even negotiate, much less implement. And there’s—you know, there’s discussion of a discharge petition that some Democrats are saying let’s just do a discharge petition. We’ll get a few Republicans to sign it. Again, that that does take time, probably at least a couple of months. And I’m not saying that’s the right solution. I think the right solution is to sit down around the table and come up with a solution.

TAUSCHE: We’ll take another virtual question. We have just a few minutes left.

OPERATOR: We will take our next question from Peter Galbraith.

Q: I want to follow up on a couple of previous questions. And thank you so much.

First, moving away from the idea of the gimmick that is the trillion-dollar coin, what about the Fourteenth Amendment in Section 4, which says that the public debt of the United States shall not be questioned? I mean, could an administration simply say we’re going to pay our debts?

And second, I wonder if you could drill down a bit on prioritization. Is it technically possible to pay Social Security and not Medicare? Is it—or is it technically possible to stiff, you know, people who have contracts with the government? I mean, how sophisticated is the payment system itself to enable you to prioritize?

TAUSCHE: Secretary Lew?

LEW: So on the payment system, there are a number of payment systems that pay different kinds of federal expenses but mostly they’re all mixed up kinds of payments coming out of the same payment center. When I was there, there was no ability to say we’ll pay some of them but not others. The system didn’t have a way to flag things by type. You would have to have an individual go through and make manual decisions on each item, which just is unworkable.

So I think, you know, you’re talking about very clunky degrees of control. I don’t know how any human being would make the decision of which of your obligations you should pay and which of them you should default on. You’d be in default on anything you didn’t pay. And that’s not a fair position to put any president in, if they could. And the idea that you turn on the system that pays bonds and turn off the system that pays people, I don’t know how you survive that, you know, politically or morally.

The debate over the Fourteenth Amendment has gone on, you know, for a number of years. I think you got to go back to the history. It was written to pay Union debts and to treat Confederate debts not as Union debts. It was not meant to be a broad grant of power. Whether you could come up with a theory that you could convince a court was legitimate, I think it’s just a risky thing to do. Somebody could challenge the legitimacy of the action. And again, we’re the reserve currency of the world. Full faith and credit is unquestioned. If you put it into question, I think it’s risky to the whole enterprise, which affects our economic and national security.

So all these ideas are kind of what you do if you can’t do what you have to do, which is raise the debt limit.

PORTMAN: So one additional thought in terms of prioritization that we didn’t talk about today that I think is important to note is that if you, indeed, prioritize and say, as an example, that government contracts would not be honored—including, you know, with businesses large and small, and for those small businesses it would really be damaged by that—in other words, you had a procurement with the federal government, it’s cut off

because of the prioritization, because that would unlikely be a high priority as compared to Social Security, say, or paying bondholders to avoid the default—then those individuals actually would be able to sue the federal government—(laughs)—which they should because they’ve been defrauded, right? And when they are paid back, they’re paid back with interest. And I think the interest—Jack, correct me here—it’s over 4 percent, 4.1, (4.)2 percent or something, as I recall. So it actually costs the government more. (Laughs.) It’s a little like these government shutdowns. You know, we had these government shutdowns and then you—you know, all essentially employees are allowed to stay; others have to go home. But then they get paid. They were at home—(laughs)—but they get paid, and it ends up costing the Treasury more.

So I wish there was something like that that could work that would make sense for our country to end up with not defaulting and yet, you know, making the appropriate budget decisions. That has to be done in the Congress, not through a prioritization, in my view. And I just don’t think it’s a practical way forward. So my hope is that we do find the negotiators sitting at one of these roundtables, like the one we have in front of us here, and figuring out how to—how to get to yes, how to find out—how to figure out how to make these compromises to be able to come up with something that does deal with the underlying issue.

As I said earlier, given the difficulty today—given the partisan gridlock and the division in our country—maybe the best major proposal that could be passed in this context would be a process one where we agree to pull back the curtain and look at everything, including the mandatory spending side, which is the largest part of our—of our budget and the fastest-growing part. So my hope is that that’s what happens over the next several weeks and that we are able to use this debt limit, as we have in the past, as an opportunity to make some changes that actually help move the country forward.

TAUSCHE: We’re nearing the end of our conversation, but I want to close just talking about the future generation and what the economy looks like for them. The government’s own estimates, as you alluded to before, Senator, show that in thirty years the deficit will be 200 percent of GDP and the federal debt held by the public will be 217 percent of GDP. What do you think is the appropriate number for that? What do you think is a sustainable level going forward into the future?

PORTMAN: Well, none of it’s sustainable. I mean, once you go over a hundred percent of GDP—you think about your business if you’re running a business. You know, you can have some debt. A lot of businesses do. But when you’re over a hundred percent of your revenue—(laughs)—in terms of your debt, you begin to get a little nervous. And your GDP, you know, is even—it should be even a more balanced ratio. So a hundred percent of GDP is frightening. And one would have thought only a couple decades ago that that would have led to probably credit agencies stepping and saying we’re going to downgrade the debt. That hasn’t happened yet. It did happen; you remember one of the credit rating agencies downgraded the debt—Jack, when was that, 2011? 2011?

LEW: 2011.

TAUSCHE: 2011.

PORTMAN: Yeah. And so none of it’s sustainable, Kayla. I really—I really believe, you know, that we are—we are facing the fiscal crisis already. And we have to do something about it, and the next several months here is an opportunity to do that.

TAUSCHE: Secretary Lew, we’ll give you the final word. What’s your message to the future generation who will be inheriting the decisions that are made today?

LEW: I think the question of debt sustainability I think is a little more complicated than for a business or for an individual. And I’m not advocating that our debt should rise to 150 or 200 percent of GDP, but there isn’t a magic number that says when it’s not sustainable.

I think the problem is, you know, we need to demonstrate that there is a kind of hand at the—at the steering wheel that’s in control. If we could make some decisions like not extending tax cuts and having it add to the deficit even more, like not ignoring the pay-as-you-go rules or saying they only apply to spending but not taxes, have a kind of comprehensive picture—as did coming out of the 1990 budget agreement, you know, under the Bush administration—I think you could restore confidence that it’s going to tick at a slow enough rate that it will stay under control.

I think the notion that there’s not the ability to make those kinds of decisions causes more immediate risks than the kind of exact number. And I certainly hope that going into the next few years we can regain—you know, start by paying for what we do. Let’s not default. And let’s find a way to have a conversation about a broad, balanced plan with everything—revenues and everything else—on the table. It can’t just be nondefense discretionary spending.

TAUSCHE: Well, in the meantime we’ll be focused on the coming weeks and coming months. But we appreciate you both setting the table.

To our esteemed guests, to our CFR members joining us both in person and virtually, thank you all for being here. We appreciate it.

PORTMAN: Thanks, Kayla. (Applause.)

(END)