Currency Crises in Emerging Markets

Updated

Projected capital outflows are placing pressure on the currencies of some of the world most dynamic emerging markets.

Introduction

As the global economy regained its footing after the 2007 recession and financial crises in Europe, the anticipated normalization of monetary policy by the United States is revealing cracks in some dynamic emerging markets that were considered the engines of growth during the downturn. Once-booming countries like Brazil, India, Indonesia, South Africa, and Turkey in mid-2013 were dubbed the “Fragile Five” due to the mounting pressure on their currencies. Slower growth in China, the decline in oil and other commodity prices, and the prospect of higher interest rates roiled even more emerging market currencies in 2015 and prompted economists to reduce global growth expectations for the year.

Currency crises, which many economists define as a swift decline of more than 20 percent of a local currency against the dollar, have hit dozens of emerging markets over the past three decades, and have occasionally triggered regional recessions like the Latin American debt crises in 1982 and the Asian financial crisis in 1997–98. The United States has augmented aid packages arranged by the International Monetary Fund (IMF) in the past to help stabilize important trading partners and limit contagion, recognizing that tremors even in small economies far away could hurt domestic growth. Drawing on lessons from previous crises, the IMF has developed new tools and a revised approach to avert the quick collapse of currencies. Still, few economists are convinced the world has seen its last currency or financial crisis.

Origins of a Currency Crisis

Currency declines typically follow a series of political, economic, and market forces that combine to pressure the exchange rate. Countries in crisis tend to run persistent current account deficits, importing more than they are exporting or borrowing capital from foreign lenders, often with short-term maturities, to finance public budget deficits and long-term projects. Capital flows can be fickle, and after years of inflows from foreign investors, sentiments can suddenly shift and dollars are sucked out of an emerging market, driving down exchange rates, depleting reserves, raising domestic interest rates, and sometimes triggering recessions.

Policymakers should make adjustments early and quickly, especially in smaller countries.

Stanley Fischer, Council on Foreign Relations

Although it takes years for a shaky economic environment to develop, financial crises unfold rapidly. The Asian financial crisis in 1997–98 was triggered by Thailand’s decision to float its currency, the baht, on July 2, 1997, after abandoning its peg to the dollar. By December of that year, the dollar was worth more than 48 baht, a sharp appreciation from the 25 baht–per-dollar peg only six months earlier. Thailand’s plummeting currency caused foreign investors to reassess other economies in the region, withdrawing their capital, and soon Indonesia, Malaysia, South Korea, and Taiwan were all mired in financial crises of differing degrees. In addition to IMF bailouts, the United States intervened directly to rescue these economies rather than risk further contagion or the quick transfer of a financial crisis across countries, both near and far, that could dampen its own prospects. Widespread currency and financial crises can also stall trade agreement negotiations, hindering global economic growth many years after countries are stabilized.

Economists identified some common characteristics that caused the crisis after the dust settled in Asia: The region’s currencies were overvalued; economies were over reliant on short-term borrowing from foreign lenders; private banks and finance companies were fragile and weakly regulated; and governments lacked the necessary political consensus needed to take swift and painful measures to adjust and stabilize the economy.

Policymakers should make adjustments early and quickly, especially in smaller countries that aren’t “anchors of the international system,” Stanley Fischer, U.S. Federal Reserve Vice Chairman, said in a 2013 interview. Important data on the real economy, such as GDP, are usually months out of date, so waiting rarely results in a much clearer picture of the economic situation. Furthermore, Fischer said, in an interview with CFR, that “economic medicine takes a while to work, and needs to be taken earlier rather than later. This means that policymakers generally need to move in anticipation of changes in the economic situation, about which inevitably they are uncertain.”

Emerging Market Currency Risks

Emerging markets such as Brazil, Indonesia, and Turkey, among others, have become darlings of international investors over the past decade, attracting capital to their fast-growing industries and delivering a boost to the global economy. But unlike the United States, United Kingdom, Japan, and increasingly, China, emerging markets have an inherent weakness: few investors are willing to stockpile their currencies. If cracks are detected in an economy, investors will dump the local currency and extract dollars, leaving behind devalued reais, rupees, and liras. This dynamic has caused crises in several regions over the past decades.

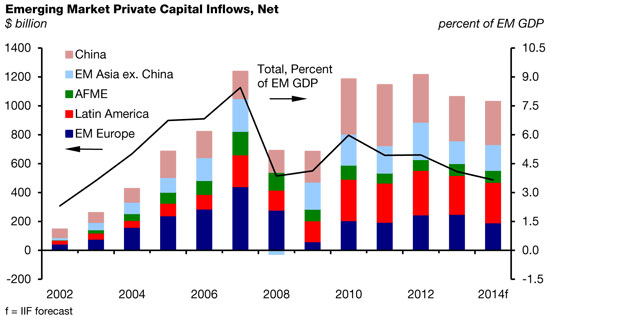

Sometimes well-performing emerging markets can still suffer from capital flight, which was the concern in the summer of 2013 after the U.S. Federal Reserve hinted that it would start “tapering” its $85 billion-a-month bond-buying program. Since the 2007 global recession, the Fed has kept interest rates near zero, prompting investors to seek higher returns in emerging markets. Private capital inflows to emerging markets surged to over one trillion dollars in 2010. Inflows to emerging markets hit a record of $1.35 trillion in 2013 and declined to $1.1 trillion in in 2014, according to the Institute of International Finance (IIF), representing the reversal of a trend of elevated outflows from developed economies since 2009. (There was a “flight to quality” in 2008–2009, when investors bought U.S. financial assets in the depth of the global recession). Net capital flows to emerging markets were forecast to decline in 2015 for the first time since 1998, the IIF said in an October report.

“If you look at the long arc of past emerging market crises, a lot of them were triggered by a tightening of global monetary conditions,” says CFR Senior Fellow Robert Kahn. But the reversal of capital flows doesn’t affect all emerging markets equally, Kahn adds, and it’s the “countries that were living off easy money and were not adjusting policies that have imbalances, and, as a result, when the party ends they have an extreme reaction. These countries also tend to have the most liquid markets and access to international capital markets, so capital reversals are more harshly felt.”

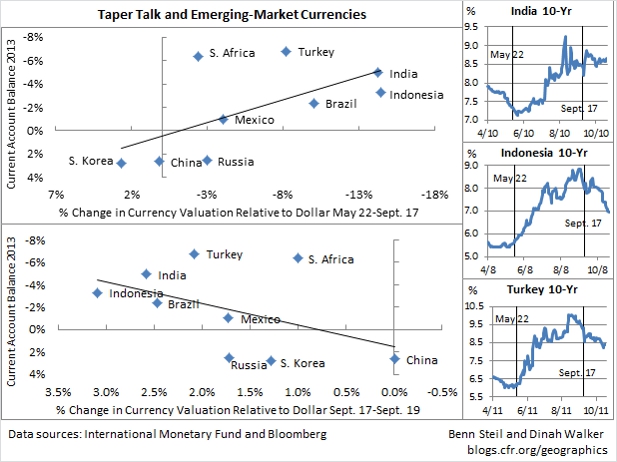

Benn Steil, senior fellow and director of international economics at the Council on Foreign Relations, says former “Fed Chairman Ben Bernanke’s now-famous taper comments on May 22, 2013, were on the surface very modest—all he was suggesting was that the Fed might, only if the data merited it, soon begin scaling back the size of its extraordinary monthly asset purchases. Yet the markets reacted brutally because the Fed had trained them over the past three years to expect ever-more accommodative policy; suddenly the chairman was changing the trajectory.“

Currencies in Brazil, India, South Africa, and Turkey rebounded after declining sharply on the taper news. The respite continued in 2013 when the Fed decided to postpone the taper in October, mainly due to weak economic data. Currency markets remained stable after the Fed said in December 2013 it would begin tapering its bond-buying program the following year, but that performance didn’t assuage concerns that a crisis may be looming for some of these emerging markets.

The Fed sparked a similar reaction when it began signaling it would normalize policy and begin increasing interest rates in 2015, with many emerging market currencies appearing especially vulnerable. These economies were further rocked by a small devaluation in China’s renminbi in August 2015 which raised doubts over the assumptions of China’s role in global economic growth.

Even the top currencies were losing against the dollar. The renminbi, the second-best emerging market currency against the dollar, was down 2.4 percent by October since the beginning of 2015, while the worst, Brazil’s real, slumped 32.4 percent. Concerns about U.S. interest rates, the benchmark for lenders around the world, were only part of the story. Economists also pointed to structural problems in Brazil and Turkey, sanctions on Russia, slower growth in China, and a sharp decline in commodity prices as factors pressuring exchange rates.

Mounting a Defense

Central banks and finance ministries in emerging markets have few options once their currencies start plummeting, and often must intervene in exchange markets in what is usually a futile effort to stabilize the rate. Countries such as Argentina, Brazil, Indonesia, Russia, and Thailand depleted their foreign reserves to prop up their currencies and ultimately turned to the IMF to stem the losses. Tapping the fund comes with conditions, and countries must agree to introduce structural changes to their fiscal policies and financial system. The IMF has received much criticism for proposing stringent conditions, known as the “Washington Consensus,” on Asian borrowers in 1997–98, which stipulated austerity measures and the removal of capital controls. The IMF has altered its approach over the years and is now more flexible on government budget cuts, but its stabilization policies still spur popular discontent.

Many economists cite the importance of acting before the crisis. But individual investors and some policymakers have found this difficult, especially in euphoric eras when they are keen to maintain rising profits and growth despite looming risks.

When the U.S. Fed first floated the possibility of a reversing its loose monetary policy in May 2013, many emerging markets were caught off-guard. The Brazilian real, Indian rupee, Indonesian rupiah, South African rand, and Turkish lira weakened against the dollar, and some of these governments quickly intervened in their foreign-exchange markets. Indonesia and Turkey tapped into their reserves and hiked interest rates, while Brazil introduced a $60 billion currency swap and repurchase program that provided access to dollars and reversed the slide of the real. Unlike the Asian financial crisis fifteen years earlier, none of these countries had to defend a pegged exchange rate, so their currencies were able to adjust, but the downward pressure raised fears of stoking domestic inflation.

Market turbulence after China’s surprise devaluation of the yuan against the U.S. dollar in August 2015 presented new challenges to shaky currency regimes, which were already grappling with an expected increase in U.S. interest rates. Kazakhstan and Vietnam abandoned the peg to the dollar, and currencies in countries such as Nigeria and Venezuela were at risk of further devaluation, according to Jorge Mariscal, emerging markets chief investment officer at UBS Wealth Management.

The policy dilemma that faces central bankers and governments in emerging markets with current account deficits is that supporting currencies by raising interest rates, thus making domestic financial assets more attractive to foreign investors, can also slow the economy. On the other hand, a 20 percent currency decline makes a country’s exports cheaper, which shrinks the current account deficit but can stoke inflation as the cost of imports—especially for basic goods like oil and rice—increases. Striking a balance during a crisis is difficult, and Steil says this task is complicated in countries like Brazil, India, and Turkey, which don’t have independent central banks, putting politicians—who resist painful adjustments for political concerns—in control of setting interest rates and monetary policy.

Spotting the Next Crisis

Economists haven’t reached a consensus on the root causes and triggers of currency crises despite hundreds of examples in the past century. Three generations of models developed by prominent economists over the past three decades haven’t been able to predict the timing of currency crises, and researchers are split on which model provides the best characterization of a crisis, according to an IMF working paper by Stijn Claessens and M. Ayhan Kose.

Given this unsettled scholarship, it isn’t surprising that economists differed on both the causes and the potential consequences of the expected reversal of capital flows as the U.S. Fed scaled back its bond-buying program. While some analysts and investors are wary of an imminent emerging-markets financial crisis, others argue that vulnerable exchange rates are due more to structural problems in emerging markets than to external shocks.

Economist Menzie Chinn of the University of Wisconsin–Madison sees the current stresses as a result of the “impossible trinity,” in which a country can’t “simultaneously pursue full exchange rate stability, full monetary autonomy, and complete financial openness.” One way to deal with this “trilemma” and reduce the pressures on currencies is through the accumulation of foreign reserves, with the stable South Korean won cited by Chinn and other economists as a successful example of this approach.

There is greater consensus among economists that a repeat of widespread tumult in emerging markets is unlikely. “Countries in Asia still remember the 1997 crisis very well,” says Steil. Many have since boosted their dollar reserves; reduced their reliance on foreign debt, especially loans with short-term maturities; and reformed their banking sectors, which helps reduce the risk of repeating previous crises and limit the potential for contagion. There is still “a lot of bitterness left over from that crisis, and they are determined never to have to go back to the IMF or U.S. Treasury for assistance,” Steil adds.

Recommended Resources

This IMF policy paper examines the global impact and challenges of unconventional monetary policy.

Morgan Stanley analysts review the performance of foreign exchange markets and provide forecasts in these August and September 2015 reports.

This 1998 Congressional Research Service report provides an analysis of U.S. foreign policy interests during the Asian Financial Crisis.

Economist Simon Johnson examines whether middle-income countries will face a financial crisis in this New York Times article.t

Colophon

Staff Writers

- CFR Staff

Additional Reporting

Header image by Murad Sezer/Reuters.

Backgrounder

Backgrounder Backgrounder

Backgrounder

Backgrounder

Backgrounder