The Role of the European Central Bank

Updated

As Europe has weathered a succession of economic crises, the European Central Bank has responded with an aggressive set of monetary policies that have redefined the bank’s original mandate.

What are backgrounders?

Authoritative, accessible, and regularly updated Backgrounders on hundreds of foreign policy topics.

Who Makes them?

The entire CFR editorial team, with regular reviews by fellows and subject matter experts.

The European Central Bank (ECB) is the central bank for the eurozone, the group of nineteen countries who use the euro common currency. Its mandate is to maintain price stability by setting key interest rates and controlling the union’s money supply.

After the emergence of the eurozone’s sovereign debt crises between 2009 and 2011, the ECB sparked controversy by undertaking a range of unorthodox monetary policies—including a program of unlimited bond buying, the use of negative interest rates, and a $3 trillion quantitative easing plan—that divided policymakers between those who thought the bank overstepped its authority and those who argued for it to take more aggressive action. Meanwhile, the ECB has been placed at the center of an initiative to create a eurozone-wide banking union that would grant the bank new powers of supervision over Europe’s largest financial institutions.

History and Mandate of the ECB

The 1992 Maastricht Treaty created the European System of Central Banks (ESCB), which comprises the ECB and the twenty-eight national central banks of the European Union (EU), including those from countries that do not use the euro. Under the ESCB sits the Eurosystem, which comprises the ECB and the national central banks of eurozone countries. The ECB took over responsibility for monetary policy in the euro area in 1999, two years before the euro was introduced into circulation.

The ECB is made up of three decision-making bodies: the General Council, the Executive Board, and the Governing Council. The General Council, which operates as an advisory body for the ECB, includes all of the EU’s national central bank governors, as well as the president and vice president of the ECB.

The Executive Board, where day-to-day decisions are made, consists of a president, vice president, and four other members, all appointed by the European Council. The Governing Council comprises the Executive Board and all of the eurozone’s national central bank governors. It sets monetary policy for the euro area.

The ECB aims to achieve price stability by setting key interest rates, through which it seeks to keep inflation just under 2 percent. In addition, the ECB is the sole issuer of euro bank notes and manages the eurozone’s foreign currency reserves. Moves toward greater banking union have also augmented the ECB’s supervisory power over financial markets.

The Bank’s Response to the Debt Crisis

The eurozone sovereign debt crisis, and the ECB’s subsequent decision to step outside of its traditional role by purchasing government bonds, generated debate over the bank’s position. Unlike the U.S. Federal Reserve, the ECB does not have a mandate to pursue full employment, and the Maastricht Treaty prohibits it from directly financing national governments. The absence of a fiscal union, including a eurozone-wide treasury to pool debt, has also complicated the ECB’s potential role as lender of last resort.

As the eurozone struggled through the global financial crisis, European leaders debated the ECB’s ability to support ailing economies. Divisions arose between France’s center-left government and German conservatives. In 2012, German Finance Minister Wolfgang Schaeuble outlined the objections to a more activist ECB, arguing, “If the central bank finances government debt, it’s a modern form of the old bad habit” of printing money. For Schaeuble, ECB intervention in bond markets would reduce the incentives for eurozone governments to undertake difficult budget reforms.

Nonetheless, as Greece’s sovereign debt crisis intensified, the ECB, under President Jean-Claude Trichet, initiated its securities market program (SMP), through which it purchased Greek government bonds on the secondary market. The ECB eventually extended the program to Ireland, Italy, Portugal, and Spain, temporarily bringing down borrowing costs.

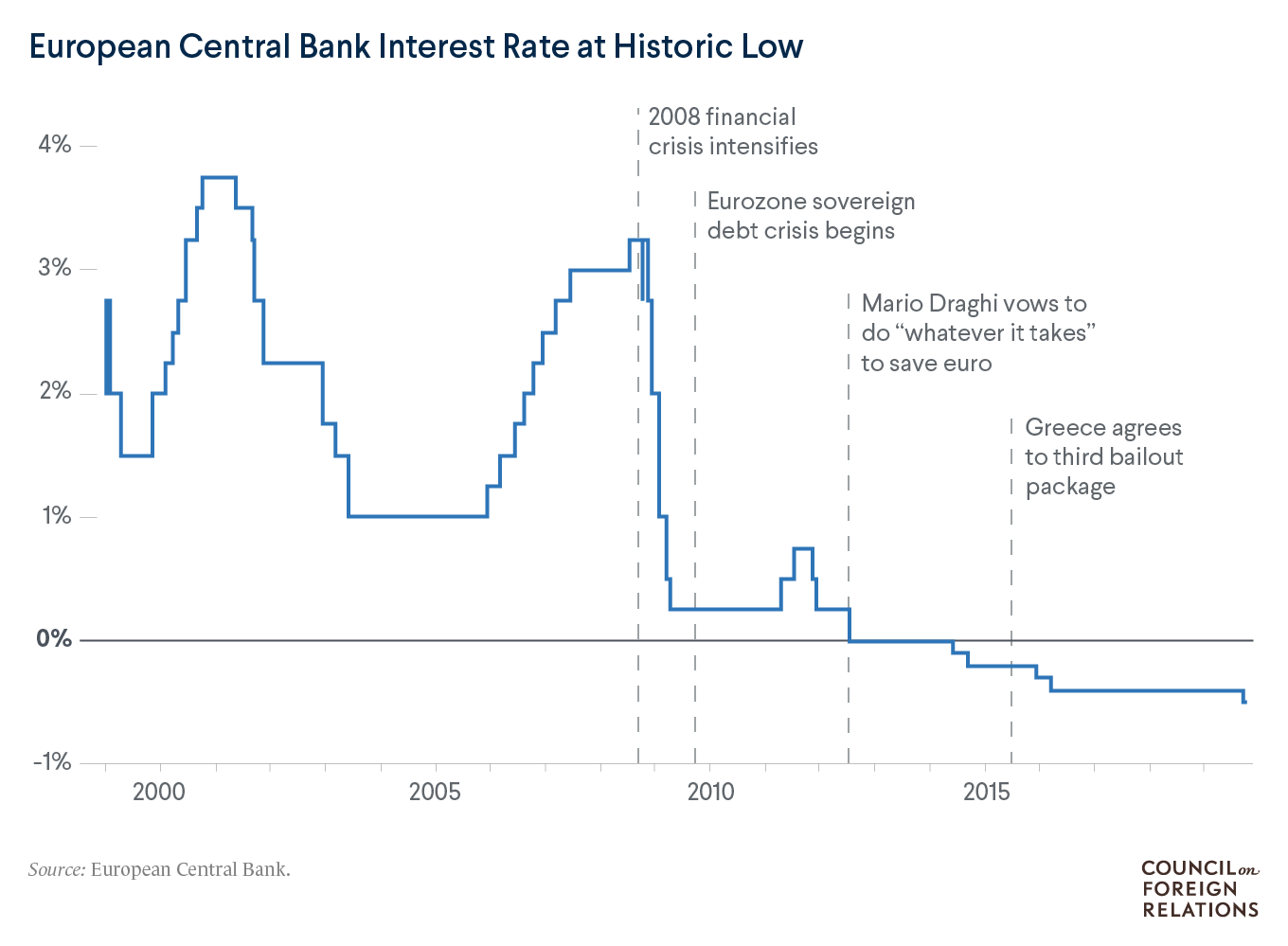

When Italian central banker Mario Draghi took over the ECB in November 2011, some feared he would not be as hawkish on inflation as Trichet. Draghi won the support of German Chancellor Angela Merkel, but he ultimately reversed Trichet’s controversial interest rate hike. Just days after taking office, Draghi lowered the ECB benchmark rate from 1.5 percent to 1.25 and then 1 percent, beginning a slide toward 0 percent and even negative interest rates that continues through the present.

The Introduction of Open-Ended Bond Buying

In 2012, fear over the potential breakup of the eurozone peaked as bond yields in Italy and Spain reached unsustainable levels. As markets panicked, Draghi made a forceful public comment on July 26. “The ECB is ready to do whatever it takes to preserve the euro,” he said.

Draghi’s statement was soon backed up by policy. In September, he announced a new program of eurozone-wide bond buying, known as outright monetary transactions (OMT). Under OMT, in contrast with the previous securities market program, the ECB could buy struggling eurozone countries’ bonds on the secondary market in unlimited amounts. Applicants would be held to stringent conditions, including mandated economic reforms. OMT bond buying would also be “sterilized,” meaning that the ECB would remove an equal amount of money from elsewhere to keep the total money supply constant.

The ECB is ready to do whatever it takes to preserve the euro.

Mario Draghi, ECB President

The sterilization rule was meant in part to soften opposition to the program among German policymakers. According to Guntram Wolff, director of the Brussels-based think tank Bruegel, German conservatives, including Bundesbank chief Jens Weidmann, argued that OMT amounted to “monetary financing” of governments, which is proscribed by EU treaty. Weidmann was the only member of the ECB Governing Council to vote against OMT.

OMT has never been used, but many observers argue that the fact that the ECB was willing to wield this “big bazooka” calmed investors. Challenges to this new ECB authority persisted, however, with some experts calling it illegal. Yet, in June 2015 the European Court of Justice upheld OMT [PDF], concluding that “the purchase of bonds on secondary markets does not exceed the powers of the ECB.”

The Push for Banking Union

Meanwhile, in 2012, EU officials had begun to discuss a eurozone banking union. The economic crisis had led to a cascade of unpopular bank bailouts, totaling over 590 billion euros ($653 billion) in European taxpayer assistance by 2012. A banking union could make banks less likely to fail and also provide a more orderly process for dealing with any such failures. To provide better oversight, the Council of the European Union created the single supervisory mechanism (SSM).

The ECB took over primary responsibility of the SSM in 2014, further enlarging its authority over Europe’s economy. Under the SSM, the ECB is charged with monitoring the financial stability of all euro currency members. This means directly supervising all “significant” banks, defined by those with a large share of a country’s economic activity. Smaller banks remain supervised by national regulators.

The ECB’s first major effort as the new supervisor was a series of stress tests to determine the health of Europe’s banks. The yearlong assessment investigated 130 financial institutions, which together accounted for over 80 percent of eurozone banking assets. The tests found that banks faced a cumulative $30 billion capital shortfall—less than estimated by private analysts. Still, a number of critics argued that the verdict was overly optimistic. Economist Philippe Legrain called the results a “whitewash.” New York University economist Viral Acharya found that major banks were much weaker [PDF] than the ECB indicated, while CFR’s Benn Steil and Dinah Walker also argued that the tests were flawed.

Quantitative Easing and the Return of the Greek Crisis

By the start of 2015, the ECB’s efforts had calmed the immediate crisis, but Europe still faced major economic headwinds. Growth was low, unemployment was in the double digits, and inflation was falling fast: in December 2014, consumer prices in the eurozone fell for the first time in more than five years.

To fight deflation—which makes debt harder to service and dampens consumer spending—the ECB announced another unorthodox monetary policy in January 2015 with the launch of quantitative easing (QE). QE, already pursued by the Bank of Japan and the U.S. Federal Reserve, involves large-scale asset purchases to inject liquidity into the economy in the hopes of sparking inflation and growth. The ECB plan called for 60 billion euros ($66 billion) of monthly public debt purchases until September 2016, for a total expenditure of some 1.1 trillion euros ($1.2 trillion), a figure that eventually reached 2.6 trillion euros ($3 trillion) as QE continued through 2018.

The introduction of quantitative easing followed the bank’s highly unusual decision to introduce negative interest rates, but for many supporters it did not come soon enough. George Mason University economist Scott Sumner argued that the ECB was not moving aggressively enough, while Pimco founder Bill Gross called the QE program “too little, too late.”

As with the previous debate over OMT, many German policymakers opposed QE. As part of a compromise with its German critics, the ECB agreed to the condition that risk would not be shared equally across the eurozone, but rather that each national bank would buy the bonds—and bear the risk of any losses—on their own. In addition, Greek bonds were excluded from the plan while negotiations for a new bailout proceeded.

After the January 2015 election of the anti-austerity Syriza government in Greece, the ECB was again thrust into the center of Europe’s debt drama. Despite Greece’s troubled financial sector, its banks had received liquidity from the ECB at the same rate as all other eurozone countries since 2010, as long as Greece complied with its bailout requirements. When Prime Minister Alexis Tsipras put Greece’s cooperation in doubt, however, the ECB limited this cheap access to capital. By February 2015, Greece’s banks could only receive ECB funds through emergency liquidity assistance (ELA), at the ECB’s discretion and higher interest rates.

Though the ECB is an avowedly nonpolitical institution, Greece’s reliance on ELA gave the bank an unavoidable role in the fraught negotiations over a new Greek bailout. As the crisis intensified, more people withdrew money from Greece’s banks, making them increasingly reliant on the ECB, whose emergency liquidity support surpassed 88 billion euros ($97 billion) in June 2015. The ECB capped ELA, forcing Greece to impose capital controls, but did not halt its support—and Tsipras eventually agreed to lenders’ terms for a rescue program.

The Future of EU Monetary Policy

In August 2018, Greece completed its rescue program, nearly a decade after its debt crisis began and three years after Prime Minister Tsipras accepted the terms for a third bailout. Economists have mixed views on the bailouts’ success. Some laud Greece’s deep reforms, its return to growth, and its budget surplus. Others, including the International Monetary Fund (IMF), warn that the country’s debts are unsustainable, pointing to an economy that is still smaller than it was a decade ago, with rising poverty and the eurozone’s highest unemployment rate.

Incoming ECB President Christine Lagarde, a former French finance minister and head of the IMF, will face other challenges as well. Italy, a much larger economy than Greece, has the third-biggest government debt in the world and is running a larger budget deficit than EU rules permit. Lagarde, who has never before worked at a central bank, will also have to overcome weakening economic conditions at a time when the ECB is running low on ammunition. Many observers expect Lagarde to follow along the path laid out by Draghi, noting that she has praised central bank stimulus measures in the past. But interest rates are already below zero, currently at negative 0.5 percent, meaning borrowers are being paid to take out loans—an unconventional policy to spark the economy and nudge inflation up, but one that also hurts Europe’s banks, because negative rates cut into their profits.

Lagarde will have to overcome weakening economic conditions at a time when the ECB is running low on ammunition.

Lagarde will also have to navigate new tensions with the United States. Her predecessor Mario Draghi, though celebrated by many economists for his stewardship of the bank during difficult times, drew the ire of U.S. President Donald J. Trump for lowering interest rates and thus causing the euro to depreciate against the dollar. Trump has already taken aim at the EU, placing tariffs on steel and aluminum and threatening more, and a trade war could further depress the unsteady European economy. If the ECB responds by continuing to lower rates, some fear it will lead to a cycle of competitive devaluations across the world.

Recommended Resources

The European Central Bank: History, Role, and Functions [PDF] by Hanspeter K. Scheller traces the origins and mandate of the ECB.

The Economist analyzes the nature of the eurozone’s banking stress tests, and the role of the ECB in carrying them out.

Benoit Coeure, a member of the ECB’s Executive Board, discussed the risks of negative interest rates in a 2016 speech at Yale.

This Bloomberg explainer on European quantitative easing provides background on the ECB’s unorthodox monetary policies.

In Foreign Affairs, Petr Polak places the ECB’s fight against European deflation in the context of similar efforts in Japan and the United States.

The Wall Street Journal examines how the ECB’s persistent low interest rates can affect countries beyond the eurozone.t

Colophon

Staff Writers

- James McBride

- Andrew Chatzky

- Christopher Alessi

Additional Reporting

Header image by Kai Pfaffenbach/Reuters.

Backgrounder

Backgrounder

Backgrounder

Backgrounder Backgrounder

Backgrounder