China Isn’t Going to Run Out of Reserves Anytime Soon

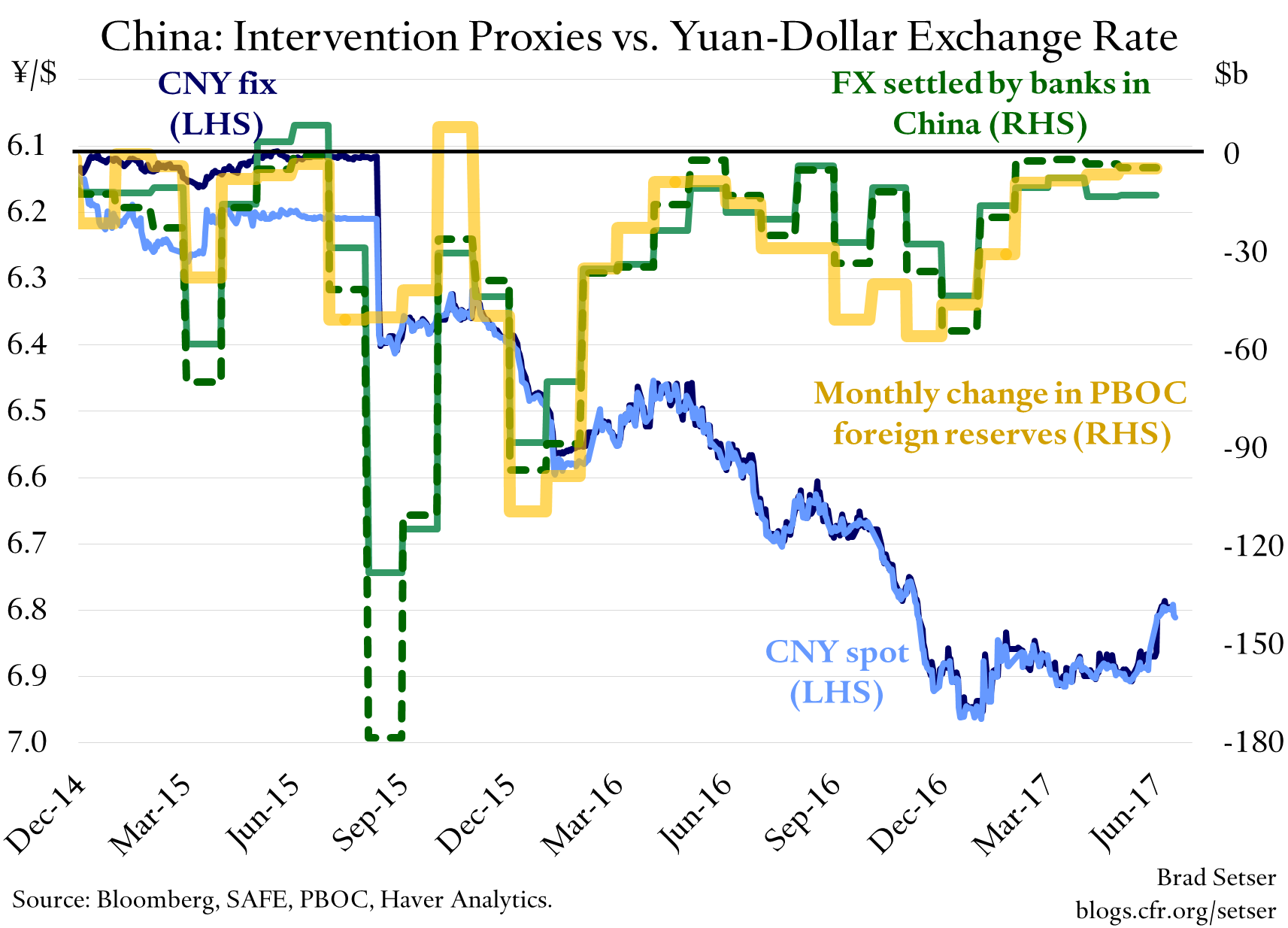

The proxies for Chinese intervention in May do not show any significant reserve drain

There is no real evidence that China’s current policy mix of controls and a fairly stable exchange rate (whether against the dollar or against the basket) is under pressure, at least so long as China is willing to keep its interest rate above the U.S. policy rate. And right now China and the U.S. are both looking to tighten policy, making it easier to sustain some sort of peg.

The May proxies for China’s foreign exchange reserves are out, and neither suggests any real pressure.

The foreign assets of China’s central bank fell by about $5 billion—one of the smallest falls in several years (foreign assets is a slightly broader measure than foreign exchange reserves).

I prefer the onshore FX settlement data largely because it includes the banking system. At times China has used the banks to hide the scale of its intervention to hold the currency down (from ‘06 to ’08, and again in 2013), and in the process build up a hidden stockpile of assets. The settlement data also shows that at times in the past few years China has had the banks sell down their stock of foreign assets to help prop up the yuan—notably in August 2015. Basically, if China is hiding something, it often shows up in the settlement data.

The banking system all told sold $12 billion in foreign exchange in May, but its stock of forwards (net forward sales) also fell. After adjusting for the change in forwards, I get about $5 billion in sales (excluding the banks’ small FX purchases for their own book).* Based on the settlement data, the banks’ forward book peaked in January and has been falling since.

The monthly reserve burn now isn’t a concern. $5 billion a month/$60 billion a year is nothing relative to China’s $3 trillion in reserves, especially as—in my view—China actually would be fine with about $2 trillion in reserves. I do not think a country with controls needs to hold reserves against all bank deposits, and I do not think China should drop its controls before it is ready to float. And hopefully that won’t be at a time when China will float down.

It is true, as the Financial Times noted, that reserve sales have now continued for quite some time—albeit at very low levels in the past few month. China last looks to have been a net buyer of foreign exchange in early 2014 (e.g. prior to the dollar’s broad appreciation). And it is also true that China’s decision to reintroduce the discretionary fix as a tool of exchange rate management suggests that China itself wasn’t completely happy with the way its exchange rate regime was functioning.

At the same time, I think the evidence continues to mount that the scale of outflows is significantly a function of expectations—so the best way to limit outflows is simply to hold the exchange rate stable for an extended period of time (technical note: China has an ongoing current account surplus, so stable reserves imply ongoing outflows at a modest pace). As the graph above shows, periods of stability/appreciation against the dollar over the last three years have been marked by modest reserve sales—China only has really had to dip into its reserves when it is trying to carry out a controlled depreciation. And a controlled depreciation is one of the hardest moves for any central bank to carry out.

The recent period of exchange rate stability—together with a domestic economy that calls for a tightening of monetary policy—thus offers China a bit of scope, I hope, to start the process of recapitalizing its financial system. Anbang looks more like a shadow bank (funding short at a high rate to invest in illiquid assets) with a massive currency mismatch (though it borrowed in China to invest abroad, so it stands to benefit from a weaker currency —see this article from FT) than an insurance company. And China’s mid-tier and city commercial banks need both capital and more stable funding sources after blowing out their balance sheets in the past few years.

One last point, one that I will develop further after the complete balance of payments data for q1 is out.

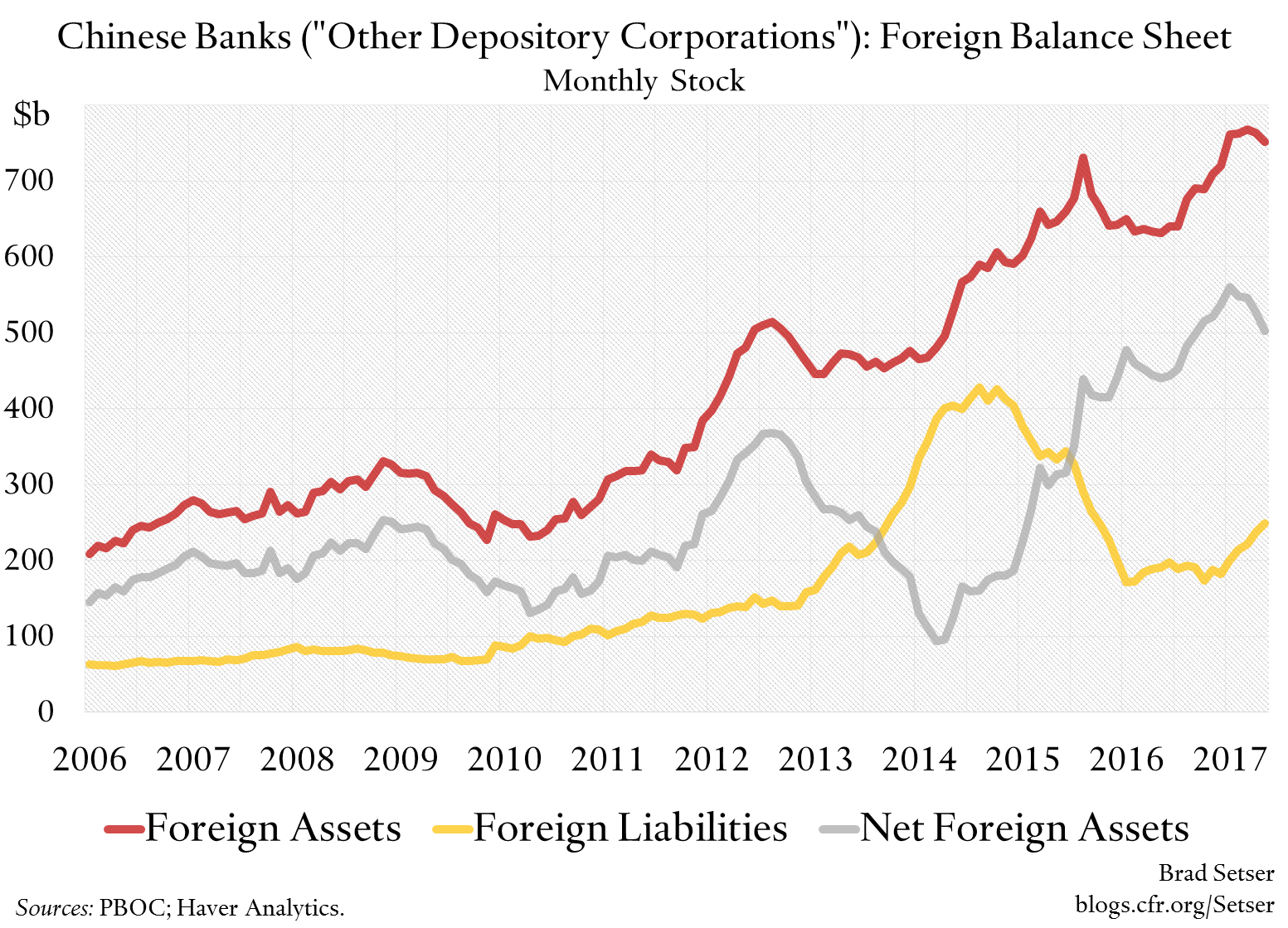

The available evidence indicates that China’s state banks returned to adding to their stockpile of foreign assets in 2016. Consider the foreign assets the PBOC reports of “depository corporations, e.g. banks”—relative to their foreign liabilities.

Total assets are now over $700 billion. This sum excludes the roughly $100 billion in foreign exchange the banks hold as part of their reserve requirement at the PBOC (presumably because it is scored as a claim on the PBOC).** And I am not sure if it includes the CDB (the CDB had a $300 billion foreign currency balance sheet at the end of 2015) and the China Export-Import Bank ($300 billion balance sheet). The CDB isn’t a deposit taking institution (if anyone knows for sure what is included, please contact me).

Total liabilities have fallen over the last few years, as the old carry trade inflows (moving money into China to take advantage of higher Chinese rates and expectations of yuan appreciation) unwound.

The net foreign asset position of the banks thus is now slightly over $500 billion. Not all of that is liquid of course. But it does imply that a substantial share of the reserve loss in 2016 stemmed from a policy choice—namely the choice to allow the banks to build up their foreign asset even as SAFE was selling off the liquid securities China holds in its reserves. That choice no doubt has deep support inside China: bank lending funds the Belt and Road initiative, and thus China’s geostrategic ambitions. Yet it is also something that China should be able to turn off if it ever is really worried about its reserves.

And since I think I know the state banks foreign book was the counterpart of some of last year’s reserve fall, I worry a bit less. The substantial build-up of the state banks foreign asset position is one more bit of evidence that China’s credit excesses have all been financed domestically.

Incidentally, the rise in the banks’ foreign liabilities this year has matched the rise in their foreign assets, which helps to explain the stability in China’s reserves in 2017.

* Goldman has noted that the SAFE data shows ongoing use of the yuan to settle payments abroad (the gap noted by Zero Hedge). The puzzle here is what happens to the yuan used for payment—right now, it isn’t clear that there is a ton of global desire to hold yuan (yuan settlement was a way of creating offshore CNY back when the yuan was rising, but why hold yuan now if it is expected to depreciate?). If yuan is being used to settle payments offshore it should be going somewhere, but no one seems to be able to find it. The stock of yuan held in say Hong Kong went down last year and has been stable this year, roughly. The SAFE data I think implies it should be rising, as foreigners accept yuan for payment of China’s imports. I also have not been able to match it with anything in the balance of payments, or on the books of the state banks -- at least not yet. The available evidence suggests to me that the state banks are building up both their foreign assets and their foreign currency assets, which suggests to me that China’s aggregate position is a bit stronger than implied by the reserves data. And so far at least the offshore settlement doesn’t seem to be generating a drain on reserves. I consequently am sticking with my tried and true adjusted measure of settlement.

** These assets dating back to 2007, are sort of like Apple’s Irish subsidiary. Not so long ago, the U.S. authorities viewed Apple Sales International as Irish (and thus allowed Apple to defer tax on its Irish income until it was repatriated), and the Irish authorities thought it was American—so no one collected tax. The foreign exchange the banks hold as part of their reserve requirement shows up on the PBOC’s balance sheet as a foreign asset, but shows up as a bank asset in the balance of payments and net international investment position. It is hard to explain but relatively easy to track.