Adjustment Is Hard, Especially if it Involves the Dollar

Trump’s tax cut has not, to date, unleashed a wave of global demand for U.S. dollar assets.

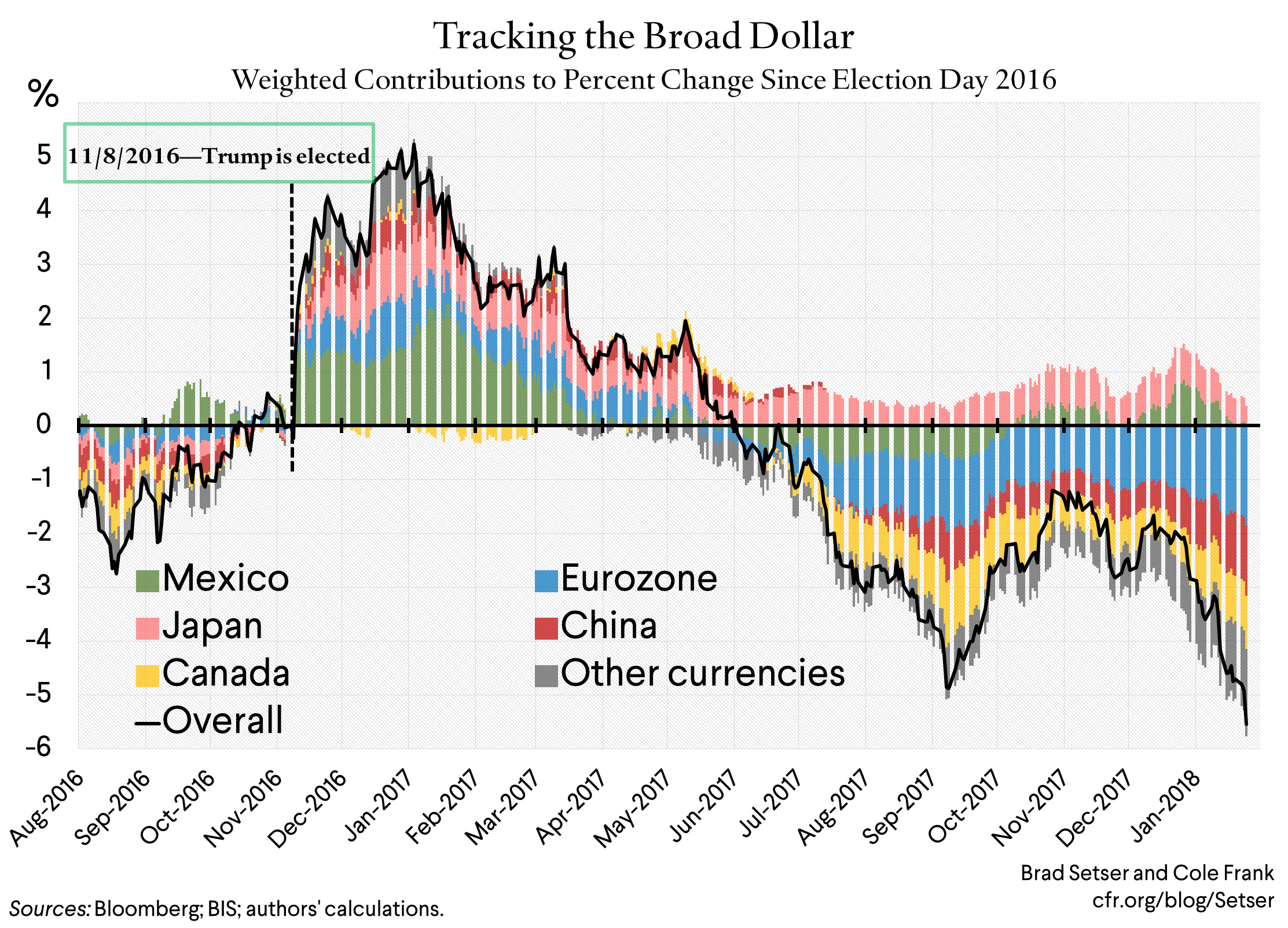

In fact, the dollar weakened as prospects for the tax cut—and associated rise in the U.S. federal budget deficit to over 5 percent of U.S. GDP—increased. And it has depreciated further this year (and even more today).

It seems like the best explanation of the dollar’s weakness is the unexpected strength of the entire global economy right now—and in particular the strength of Europe’s recovery. Just as the dollar moved up in 2014 in anticipation of the Fed’s policy normalization, the euro seems to be strengthening on expectations that the ECB might actually need to tighten in 2019. Any exchange rate reflects developments abroad as well as developments at home.

Or to make a more technical argument, if the scale of the ECB’s asset purchases was driving a lot of funds out of the European fixed income market and into U.S. bonds, the reduction in the ECB’s pace of buying (which the ECB would no doubt describe as ongoing easing just at a slower pace, as its balance sheet continues to rise) might also have an impact (though the connection between flows and price moves is complex, see Coure’s speech at the IMF’s research conference). The dollar was certainly on the move even before Secretary Mnuchin’s comments today.

All this said, I certainly didn’t expect bigger fiscal deficit and a tighter monetary policy as the Fed started to reduce its balance sheet and continues to raise policy raises to combine to lead the dollar to fall. I don’t claim to fully understand the reasons for the dollar’s current weakness.

No matter.

It has become clear over the past few weeks that most of the world—at least those parts of the world with large current account surpluses—like the dollar more or less where it is, and do not particularly want it to weaken further.

They are, as a result, resisting—in various ways—a currency move that would bring the world’s trade into better balance (reminder: U.S. non-petrol exports responded in the way that one would expect given the dollar’s 2014 appreciation, and subsequently have underperformed global growth).

Last week, Europe—meaning parts of the ECB—did a bit of soft verbal intervention. Various members of the ECB’s governing council highlighted that a stronger euro would make it harder for the ECB to achieve its inflation target, and thus hinted that further currency moves might lead to a delay in any ECB tightening.

Fair enough. But if the Eurozone accepted a stronger currency and offset the drag on both exports and inflation with a more expansionary fiscal stance, it could simultaneously move closer to both external and internal balance. The eurozone now has the tightest fiscal stance—judged by the size of the structural fiscal deficit—of any of the world’s big economies. There is certainly scope for the largest and most export-driven eurozone member-state to offset the impact of a stronger euro with a bit of demand support. Germany’s fiscal surplus is heading to over 1.5% of its GDP absent policy changes from a new government.

And the reaction in Europe has been mild compared to the reaction in Asia.

Almost all the big surplus economies in Asia—with the notable exception of Japan —appear to have intervened to keep their currencies from appreciating against the dollar in the past few weeks.

Korea is the most obvious case—it jumped in loudly to keep the won from strengthening too much, and looks to have drawn a new line in the sand around 1060 won to the dollar.

But it isn’t alone.

China doesn’t seem to want the yuan to be all that much stronger than 6.4 yuan to the dollar—though there isn’t (yet) hard evidence of intervention, and the yuan did move a bit beyond 6.4 today.

While Taiwan hasn’t defended 30 NTD/USD since late December (to be fair, Taiwan’s central bank maintains the private demand for dollars just happens to surge at about that level), it does seem to have resisted pressure for the Taiwan dollar to strengthen much beyond 29.1 to 29.2 earlier this week (or it just happened that private demand for dollar rose at this level).

Thailand—which now runs a current account surplus of around ten percent of its GDP—unquestionably has been intervening, though it seems more to smooth the baht’s appreciation than to completely halt it. Thailand releases weekly reserves data, and its combined reserve and forward book jumped by $4 billion in the first two weeks of the year (valuation changes could explain perhaps $1 billion of the change).

I will have more on the details of Asia’s intervention soon.

But before going into individual cases, I wanted to highlight the big picture: A lot of Asian countries with big external surpluses remain ready to step in and keep the dollar from depreciating against their currency. And in the process they block market pressures that might otherwise bring the U.S. trade deficit down.

This of course isn’t new. The same thing happened when the dollar floated down against the euro in 2003—Asia initially more or less followed the dollar down, thanks to a surge in intervention. And it happened again when the dollar was under pressure to depreciate in 2009 and 2010 (in part because the ECB kept its monetary policy far too tight back in 2009, 2010, 2011, and 2012, adding to dollar weakness). Basically, when the market wants to fund the U.S., the U.S. historically has accepted the inflow and the stronger dollar—and when the market doesn’t want to fund the U.S., many of the world’s surplus countries have tended to step in and resist the appreciation of their currencies and in the process finance bigger ongoing U.S. trade deficits than the market wanted to fund.

And I see some early signs that this process is repeating itself.

Basically, the market is now creating pressure to bring the U.S. trade deficit down (which, by implication, means the rise in the U.S. fiscal deficit would need to be funded domestically). But the world’s big surplus countries also need to do their part with policies that help rather than hinder global adjustment. Otherwise I worry that the market pressure for trade adjustment will fade —and the pressure for a bigger trade deficit created by the rising U.S. fiscal deficit will come to dominate.*

* I have long believed that the dollar’s 2014 rally left the dollar too strong for the tradeables sector of the U.S. economy. U.S. exports have lagged since—and the U.S. trade deficit looks to have taken another leg up in the fourth quarter.