China’s reported desire to slow its Treasury purchases briefly generated a lot of attention (China subsequently denied the report). China’s Treasury holdings have basically followed its reserves, so if reserves were likely to more or less stay stable in 2018, there was no particular reason for China to be a significant (net) buyer of Treasuries—China’s 2017 purchases reflected, in my view, a desire to rebuild its Treasury portfolio after it had been depleted by China’s need to sell its more liquid assets when its reserve were under pressure in 2016 rather than anything more fundamental.

The flurry of attention quickly subsided once the Treasury market stabilized—as, well, no one who is watching China closely really thinks China is about to sell a ton of Treasuries. And if it did want to sell for financial reasons, it presumably wouldn’t want to broadcast that fact. The bond market can go back to debating the timing of the ECB’s “exit,” the impact of the very real rise in the U.S. funding need after the tax cut (see Jason Furman) and underlying inflation dynamics.

But the flurry of attention did result in a slew of new market research on China’s Treasury portfolio.

And I quickly realized that some adjustments that I make when looking at the data aren’t (at least not yet) completely standard. I have been watching developments in China’s external portfolio for a long time now—more or less since the end of 2004. So I have a fair amount of conviction on the value of these, fairly simple, adjustments (I can do much more complex adjustments too, these are just the basics!).

1) China’s reserves are a bit higher than formally reported.

China doesn’t count the foreign exchange that Chinese banks hold as part of their required reserves as part of its formal reserves (other countries—cough, Turkey—do). The banks required holdings of foreign exchange—and at times, these requirements have been “adjusted” to take pressure off formal reserves show up as a separate line item on the PBOC’s balance sheet (“other foreign assets”) and as a special line item in international investment position (“other, other, assets”). This isn’t a huge adjustment now—but it has really mattered at times when the peg/basket peg has been under pressure. Bottom line: I now add about $60 billion to China’s reported reserves.*

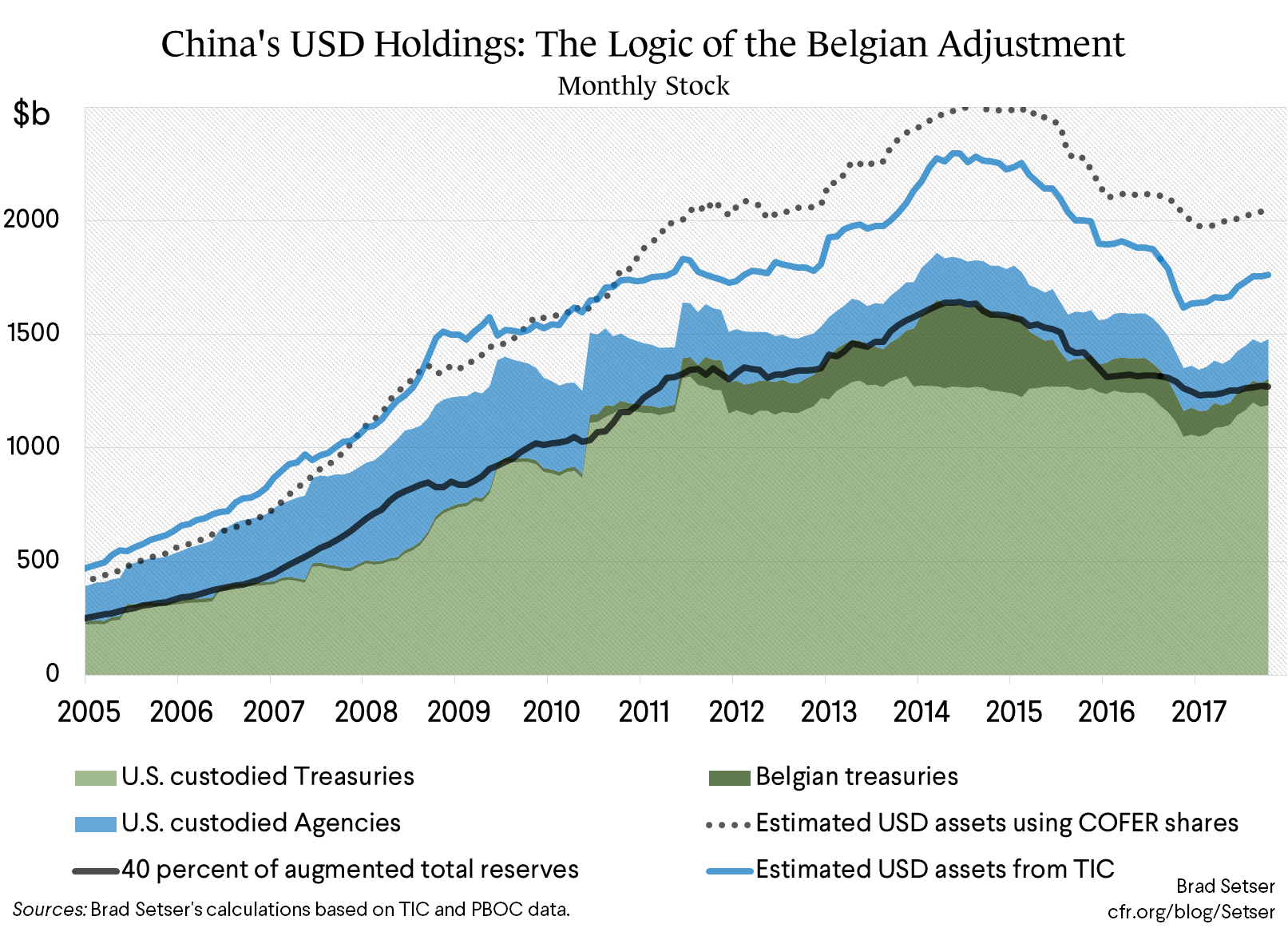

2) China’s Treasury holdings are also a bit higher than formally reported.

The U.S. major foreign holders table (which is the data everyone uses) shows Treasuries that Chinese institutions hold in U.S. custodians. But starting in 2011, China seems to have started using a Belgian custodian for a portion of its holdings—Belgium’s holdings surged then, and again in 2013-2014.

The case that these should be attributed to China is very strong. They certainly aren’t really “Belgian.” And, well, the sum of Belgium’s (long-term) holdings and Chinese holdings fits better with China’s reserves than the China line alone. China’s holdings were flat when China’s reserves were rising from 2011 to the end of 2014. And, well, China’s holdings likely fell by more then reported in 2015 and 2016 when China’s reserves were falling (back in 2015 and early 2016 the counterpart to the fall in China’s reserves was a reduction in China’s holdings of U.S. stocks and a fall in Belgium’s treasury holdings… hmmm).

This adjustment pushes China’s current Treasury portfolio up from $1190 billion to just over $1250 billion—it isn’t huge.

3) China doesn’t just hold U.S. Treasuries! China’s reserve managers at the State Administration of Foreign Exchange (SAFE) have long had a significant Agency portfolio, and a decently sized U.S. equity book.

There is a tendency to take China’s holdings of U.S. Treasuries (in the major foreign holdings table) as the proxy for China’s holdings of all U.S. bonds.

That’s clearly off.

The Treasury helpfully now produces monthly survey data on China’s holdings of Agencies (and U.S. equities). So we know China has almost $200 billion in agencies.

China likely holds some U.S. corporate debt. But, well, those holdings have—for some reason—never appeared in the U.S. custodial surveys. China’s holdings here blend in with the large custodial holdings of corporate debt of “Luxembourg” and “Belgium”—in other words, the custodial data for corporate bonds just tells us that a lot of these bonds are held in global custodial centers. So there are reasons to think China’s total U.S. bond portfolio exceeds the $1.45 trillion implied by summing up China’s custodial holdings of Treasuries and Agencies, and then adding in the Belgian portfolio. But there is no doubt in my mind that China’s total U.S. bond holdings are closer to $1.5 trillion than $1.2 trillion.

And SAFE also likely accounts for the significant fraction of China’s $200 billion or so in holdings of U.S. equities that registers in the custodial data.**

Why does this all matter?

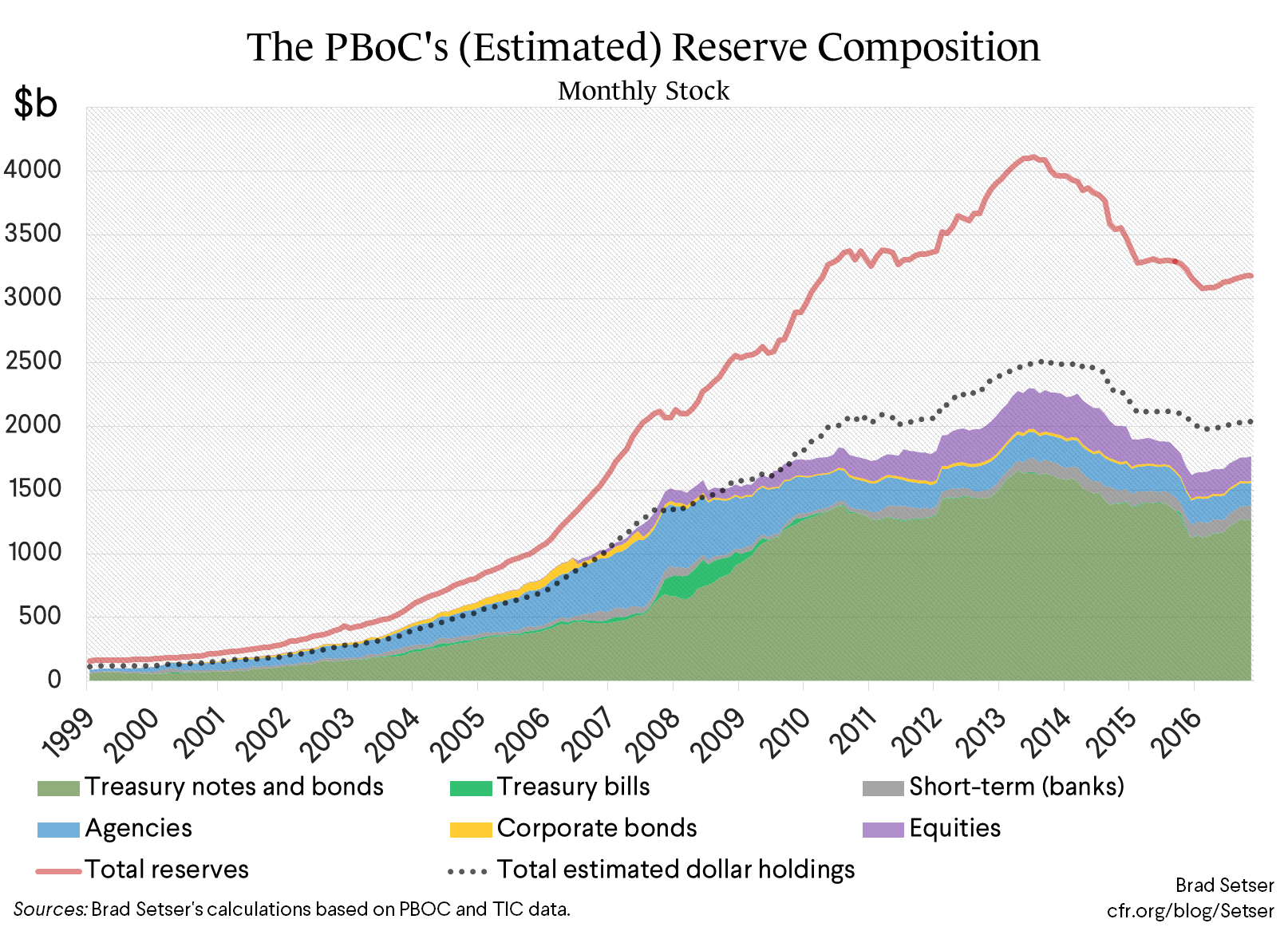

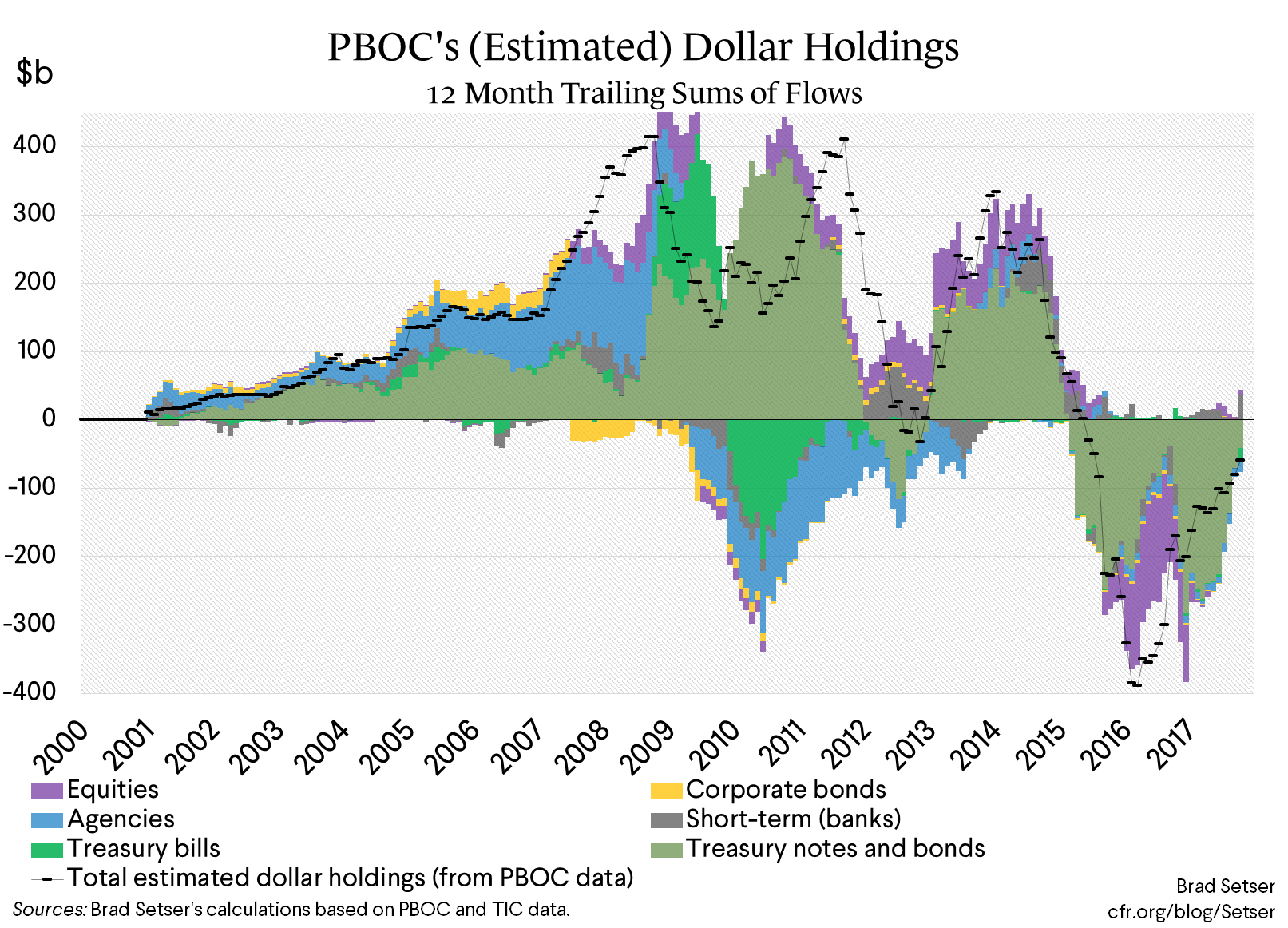

Well, in the pre-crisis period, the bulk of China’s flow actually was going into Agencies—looking only at the Treasury data significantly understated China’s impact on the U.S. fixed income market.***

And, well, the global data indicates that the big distortions associated with China’s flow into the U.S. fixed income market came from 2004 to say 2010, or maybe 2012 (the euro crisis in the summer of 2011 led to a general risk sell off that impacted all emerging economies and reduced China’s reserve accumulation in 2012). There was a last hurrah in 2013 and 2014—but the bonds bought then were sold when China’s currency came under pressure in 2015 and 2016.

What accounts for China’s reduced impact?

Three things in my view:

1) China did a big stimulus after the global crisis, and allowed a boom in domestic lending—which reduced its current account surplus as a share of its GDP (less so as a share of global GDP). Some other countries and regions didn’t. Korea never did a stimulus for example. And the eurozone’s structural fiscal position today is better than it was in 2007. The fixed income inflow into the U.S. has broadly migrated to the countries that have run tighter fiscal and credit policies post-crisis than China (and to Japan)

2) China moved away from Agencies after the global crisis—while the Treasury share of China’s reserve portfolio has been remarkably constant, the overall U.S. fixed income share of China’s reserve portfolio has fallen. And China’s share of the overall Treasury and Agency market has really fallen.

3) China consciously increased the external lending of its state banks (notably China ExIm and the China Development Bank) in order to reduce its reserve accumulation, and in the process, reduced its buying of U.S. and European fixed income reserve assets. From 2002 to 2010 or 2011, reserve growth matched China’s current account surplus (actually it was a bit above it if you add the PBOC’s other foreign assets). After 2010, lending to the rest of the world from China’s banks has increased rapidly, and mechanically now has offset much of China’s current account surplus.

I will have more on the state banks later. Something interesting happened in 2017. Rather than funding, in a deep sense, their external lending out of China’s current account surplus (during the good years) or out of reserves (in the bad years), they funded their external lending last year by raising their external borrowing. That shift explains a decent part of the stabilization of China’s reserves in 2017.

* My broader measure of China’s official assets is bigger yet, as the state banks account for the bulk of China’s holdings of portfolio debt (this was used to disguise China’s intervention back in 2006) and the China Investment Corporation (CIC) accounts for a large share of China’s holdings of portfolio equity—so a meaningful fraction of China’s $450 billion in portfolio assets is held by state actors (and those state actors added to their foreign portfolios in the past in order to take pressure off the PBOC and limit China’s reserve growth). And, well, China’s banks (including ExIm and the China Development Bank) have made about $640 billion in loans to the rest of the world. The decision to encourage the banks to go out also was initially a function of a desire to limit China’s reserve accumulation.

** Balance of payments math also allows us to confirm that China’s U.S. equity holdings aren’t private, and for that matter, aren’t all from the CIC. The U.S. doesn’t split out official and private holdings for individual countries. But China’s total holdings in the TIC data long exceeded the total global equity holdings of “private” Chinese investors in the NIIP (“private” here includes the CIC, it is everything that isn’t considered a reserve asset). The institutional history here is well known in China and reserve watching circles: SAFE set up “SAFE investments” to manage a risk portfolio and expanded its funding to ward off competition from the CIC to manage China’s reserves in the 2000s, and it clearly bought a lot of equity (it showed up in the TIC flow data as a spike in purchases from Hong Kong) in late 2007 and early 2008.

*** The usual references for China’s impact are Warnock and Warnock; Bernanke, Bertaut, DeMarco and. Kamin; and Beltran, Kretchmer, Marquez, and Thomas. But this Christopher Martin paper also seems interesting!