Looking Back at the Impact of Real Exchange Rate Moves on Exports

G-3 exchange rate moves over the past four years have had expected impacts on trade flows

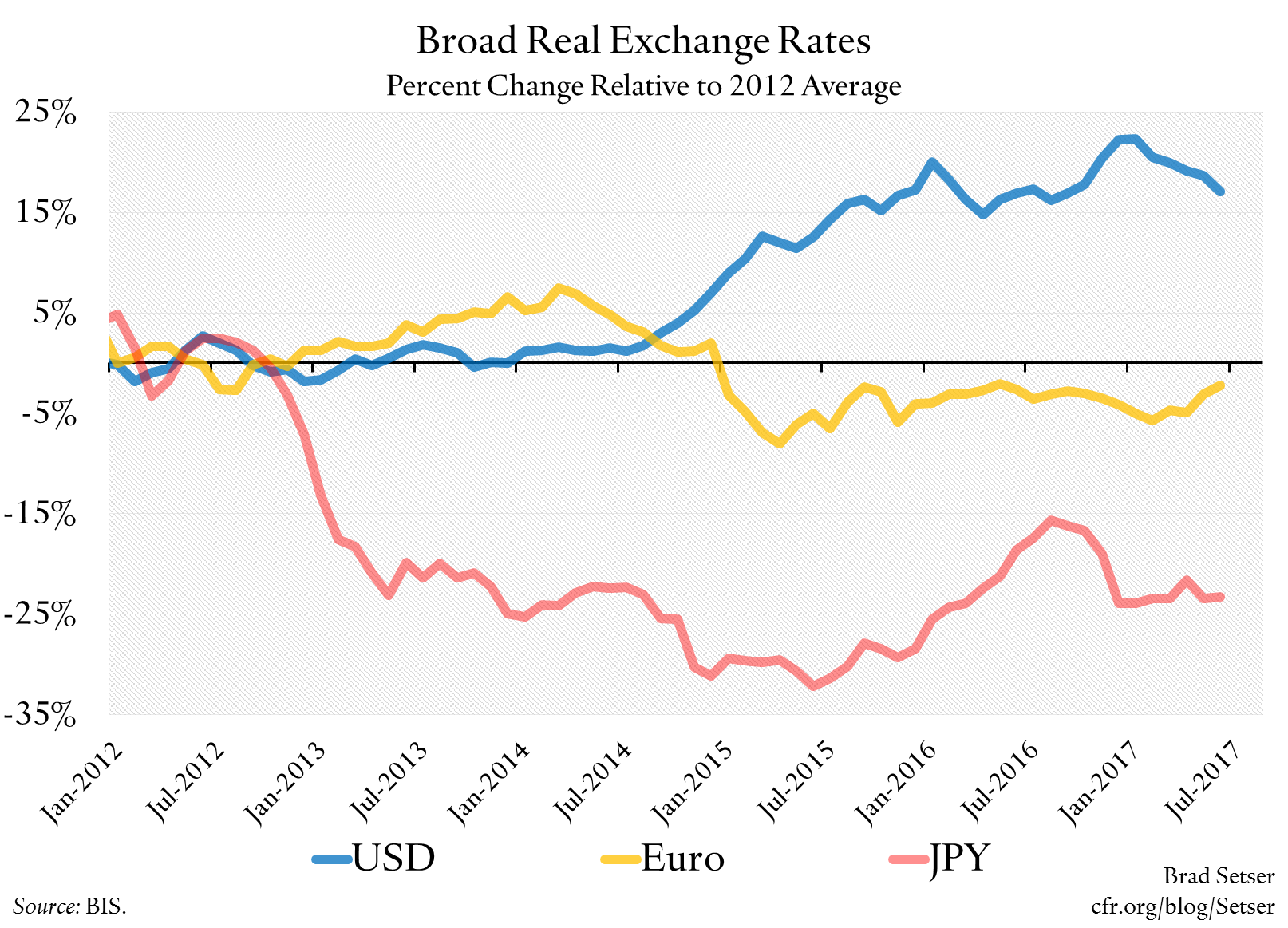

The big news—on the foreign exchange front—this year has been the rebound in the euro.

But exchange rates affect trade flows with a lag. The trade data is still being shaped by the big event of three years ago: the dollar’s 2014 rally.

The euro weakened then—and broadly speaking stayed weak (at least against the dollar) until earlier this year.

And the yen saw a second down leg, after weakening in late 2012 and early 2013.

Most of the impact of an exchange rate move should be apparent after three years. So this seems like a good time to assess whether the exchange rate moves of 2014 had an impact on trade flows (especially as the euro has largely reversed its 2014-16 weakness).

Guess what? The 2014 exchange rate changes seem to have had more or less the expected impact: countries that saw their exchange rates depreciate in 2014 have done better than their peers.

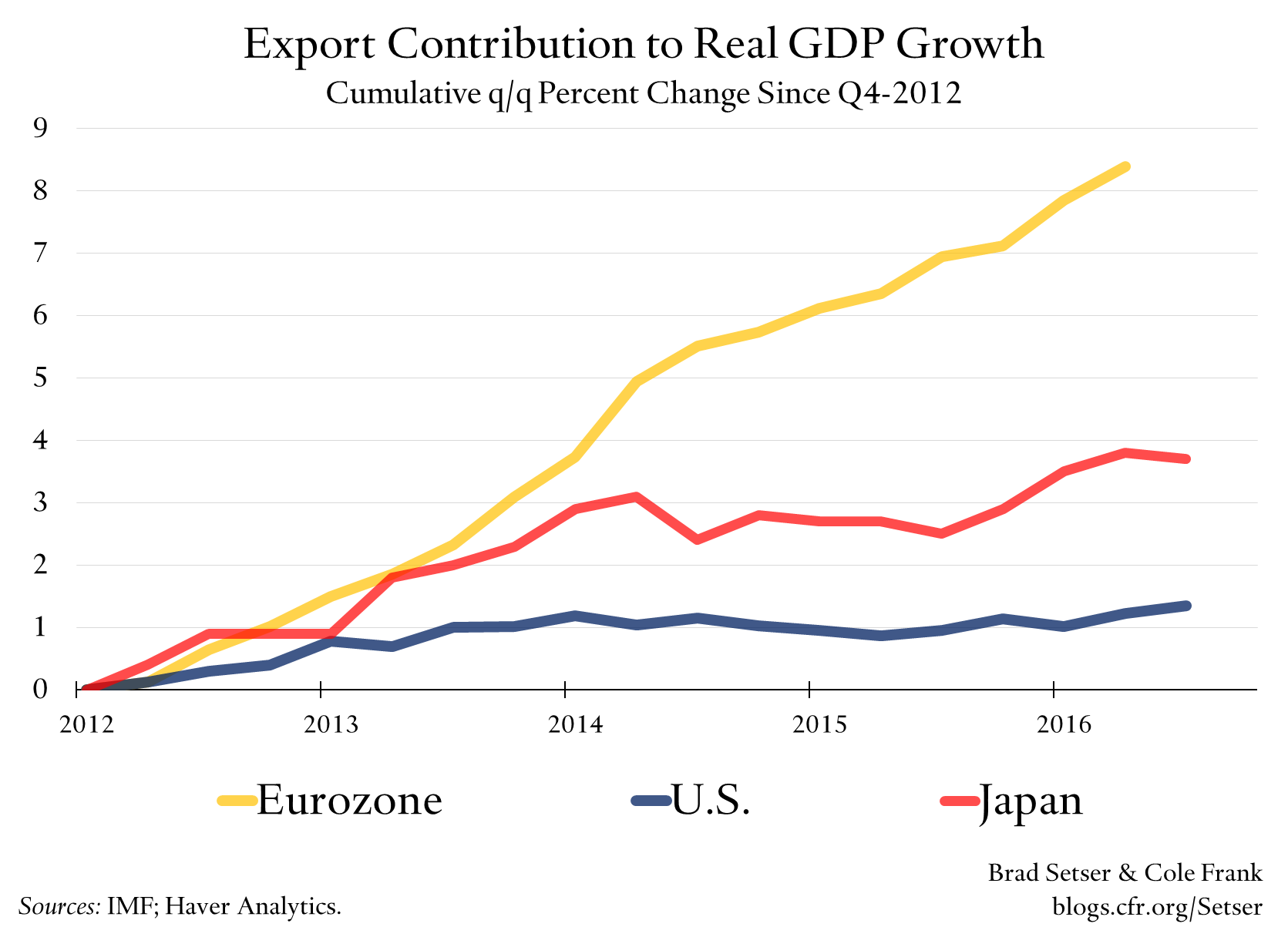

Look at the growth of real exports (measured by the cumulative contribution of real exports to GDP growth) in the U.S., Japan, and the eurozone.

I have no doubt that the oil price shock of 2014 cut into the exports of all three, as oil exporters had to cut their imports (quite significantly). But it is equally clear that Japan and the eurozone have outperformed the U.S. over this period. As a standard model would predict given the dollar’s strength after 2014.

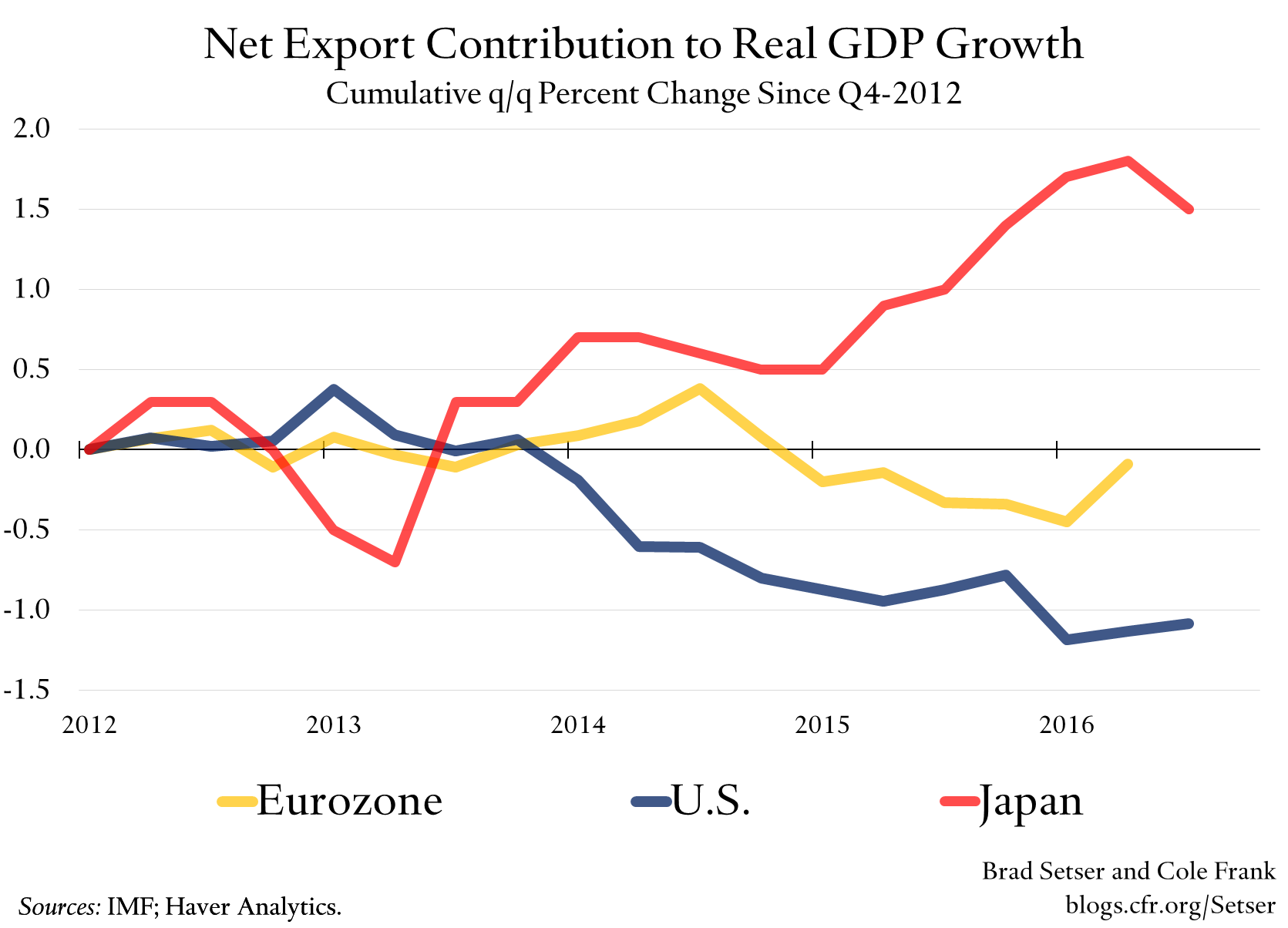

Now look at net exports—exports less imports.

Japan has received quite a significant contribution to its overall growth from net exports since 2014. In part because the sharp rise in the consumption tax in 2014 cut into Japanese demand growth, and thus into the path of imports.

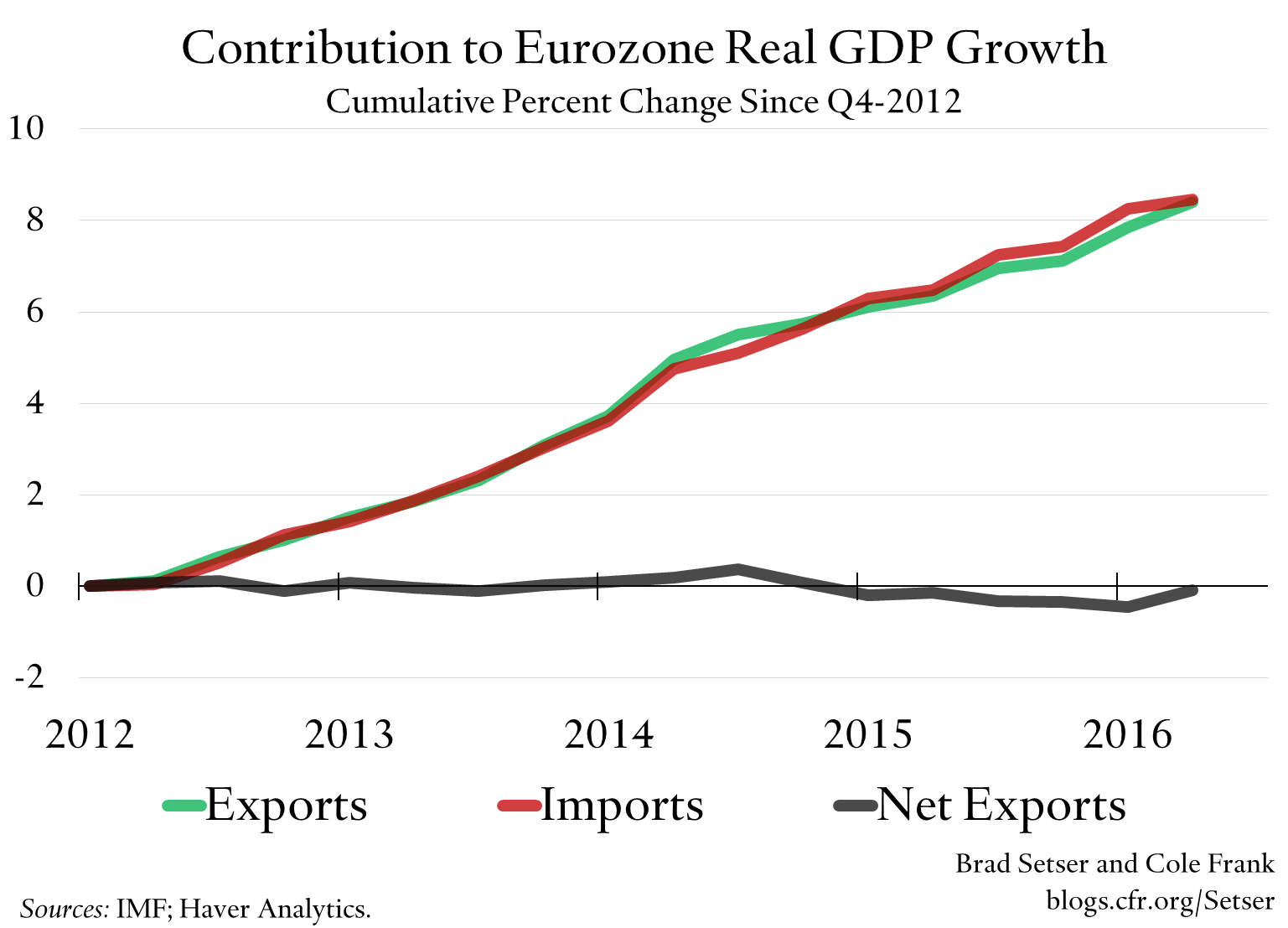

The eurozone hasn’t gotten a big boost from net exports. Exports are up but the revival in demand has pushed imports up too (as Couere noted).

The rise in the eurozone’s external surplus came in 2011 and 2012 , as rising risk premia in the periphery and a wave of fiscal consolidation cut into demand (charts are here). I do though think the euro’s 2014 depreciation had an impact: without the euro’s weakness, the fall in emerging market import demand that followed the commodity shock would likely have had been a drag on eurozone growth.

And the U.S. has experienced a significant (roughly one percentage point of GDP) drag from net exports over this period, thanks to a broad-based fall in exports (nicely illustrated by Jospeh Parilla and Nick Marchio of Brookings)

More formal techniques are needed to estimate whether the magnitude of the trade response to exchange rate changes is in line with the past (in the U.S. it seems to be, at least on the export side). But directionally, exchange rate moves are having the expected impact.

I would love to have included China in this data by the way—the yuan initially followed the dollar, and then it reversed course and depreciated against its basket in 2016, before stabilizing in 2017. But China—alone among the big economies—doesn’t provide a detailed quarterly GDP series and thus it is not possible to calculate quarterly contributions from real exports and imports.

But broadly speaking, the yuan’s 2014 real appreciation seems to have had the expected impact on China’s export growth. Export volume growth was weak in 2015 and 2016. Chinese goods exports rose on average by about 1 percent in 2015, and by between 2 and 3 percent in 2016.* And its 2016 depreciation is having the expected impact on 2017 volume growth too—on average, goods export volumes are up close to 9 percent this year. China’s exports are now growing roughly two times faster than the overall expansion in overall global trade. I would attribute that to the lagged impact of the yuan’s depreciation.

British observers often note that the pound’s depreciation has yet to bring down Britain’s current account deficit and infer that exchange rate moves have lost impact (global supply chains, etc). That though overgeneralizes based on Britain’s particular experience—in other, larger economies, exchange rate moves have had the expected impact.**

* These numbers are the average of the monthly y/y increases that China reports for goods export volumes. China really should produce better data here, even with the difficulty adjusting for lunar new year seasonality.

** The pound’s weakness has had an impact on Britain’s tourism exports, and also seems to be helping increase goods export volumes (setting aside q3 of last year, when non-EU exports fell for reasons I do not fully understand —see figure 8 of the UK trade data release). But in Britain’s case, the goods-exporting sector is relatively small. That makes adjustment through stronger exports hard—as currency moves tend to have a bigger impact on exports than on imports. “J-curve” (nominal imports rise because of higher prices) effects look to have pushed up British tourism imports. And, well, the fall in household savings in the U.K. kept real spending on imports up and delayed adjustment.