The Belt and Road Initiative Didn’t Quite Live up to its Hype in 2017

China’s balance of payments data doesn’t show any material increase in the pace of offshore lending.

I admire the public relations push that China has marshaled around the Belt and Road Initiative.

It isn’t yet clear if the Belt and Road has any geographic coherence*—or is simply a phrase that China’s bureaucracy has latched onto because of its flexibility. I suspect that the historic Chinese connection to the Artic is rather thin for example.

The Belt and Road isn’t (for now) a trading block. The Regional Comprehensive Economic Partnership (RCEP)—China’s big trade initiative—is smaller in scope. It rather is a set of infrastructure projects that will be financed by Chinese money. Or global money mobilized thanks to a backstop provided by Chinese risk capital.

Which means that the balance of payments data provides at least some insight into the Belt and Road Initiative.

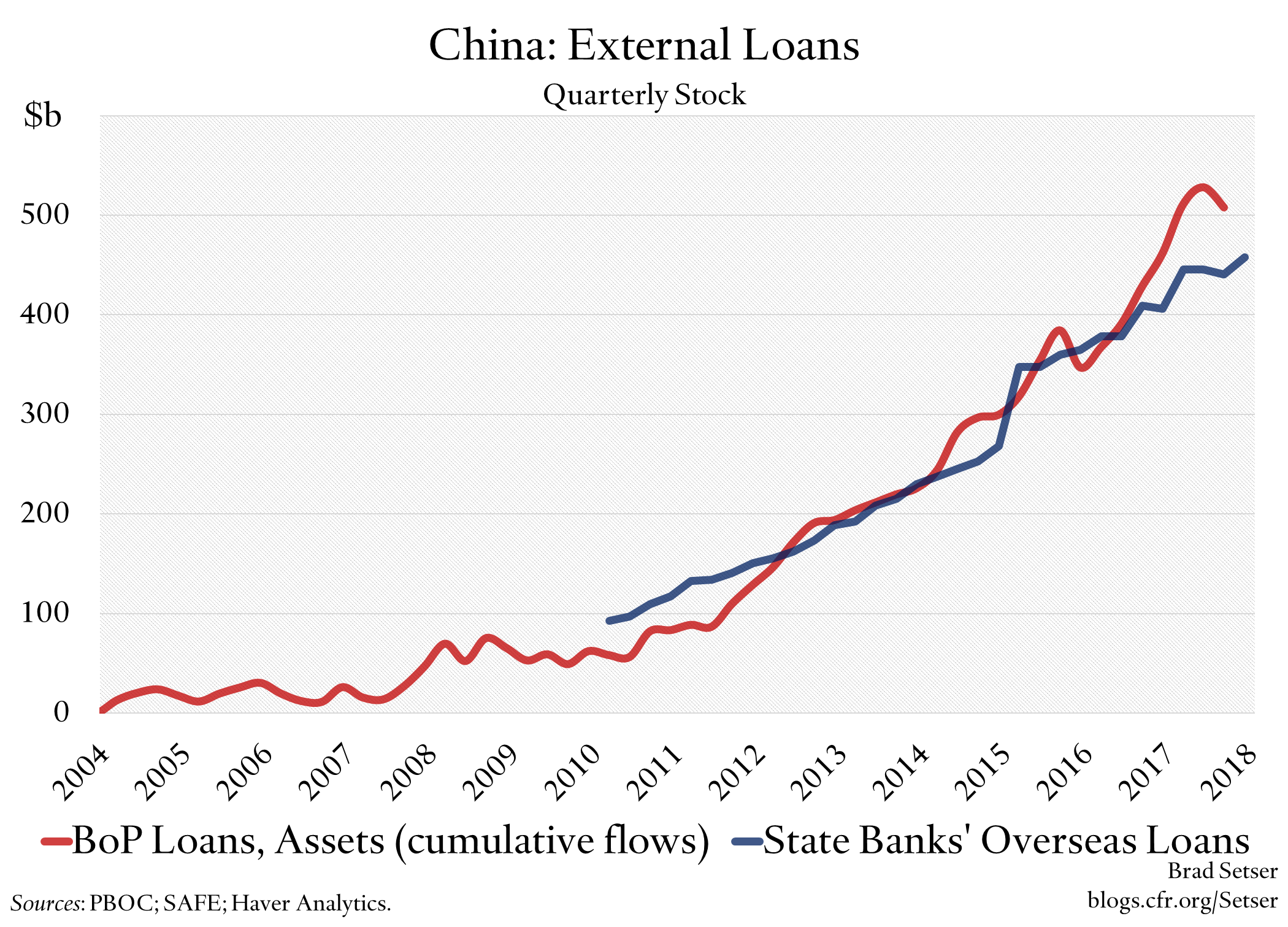

The external lending of China’s policy banks—and the big state commercial banks, who often still seem to serve as policy banks—shows up in China’s balance of payments pretty clearly I think.

And, well, the relevant balance of payments categories suggest that China’s policy lending slowed a bit in 2017.

Not the standard story I know.

But one that is well founded in the relevant “hard” data points. The aggregate overseas lending in foreign currency of China’s state banks (a category which could include the China Development Bank—it isn’t totally clear to my knowledge) also slowed a bit.

The balance of payments data—I am using “other, loans”—suggests that the rise in policy lending preceded the Belt and Road. It started back in 2011, picked up pace in 2012, and continued at a fairly steady clip since.

That lending had different branding. It was part of the broader “go out” policy that supported the international expansion of Chinese state firms. And at the time it was focused more on investment in energy and mining assets—though of course there was still plenty of funding for the construction of railways and highways and ports and the like (China has never really been resource constrained, and in many cases, improved infrastructure is needed to facilitate the physical flow of commodities). No matter, the flow was rather significant.

By 2012 external lending by the Chinese banks was rising by about $50 billion a year. And in 2016, the total external lending of the main state banks topped $100 billion.

I sort of expected the Belt and Road initiative, given its hype, to increase that sum.

So far, though, it hasn’t.

We don’t have the complete numbers for 2017 yet. But based on the data for the first three quarters and the banking data that has been released for q4, I am confident that the pace of offshore lending by China’s banks slowed a bit in 2017. The scale of lending probably picked up from the $50 billion over four years that Keith Bradsher and Jane Perlez reported last May. But some fraction of the new Belt and Road lending seems to came come from redirecting lending away from other projects —energy lending, for example — rather than an increase in the overall pace of lending by the state banks.

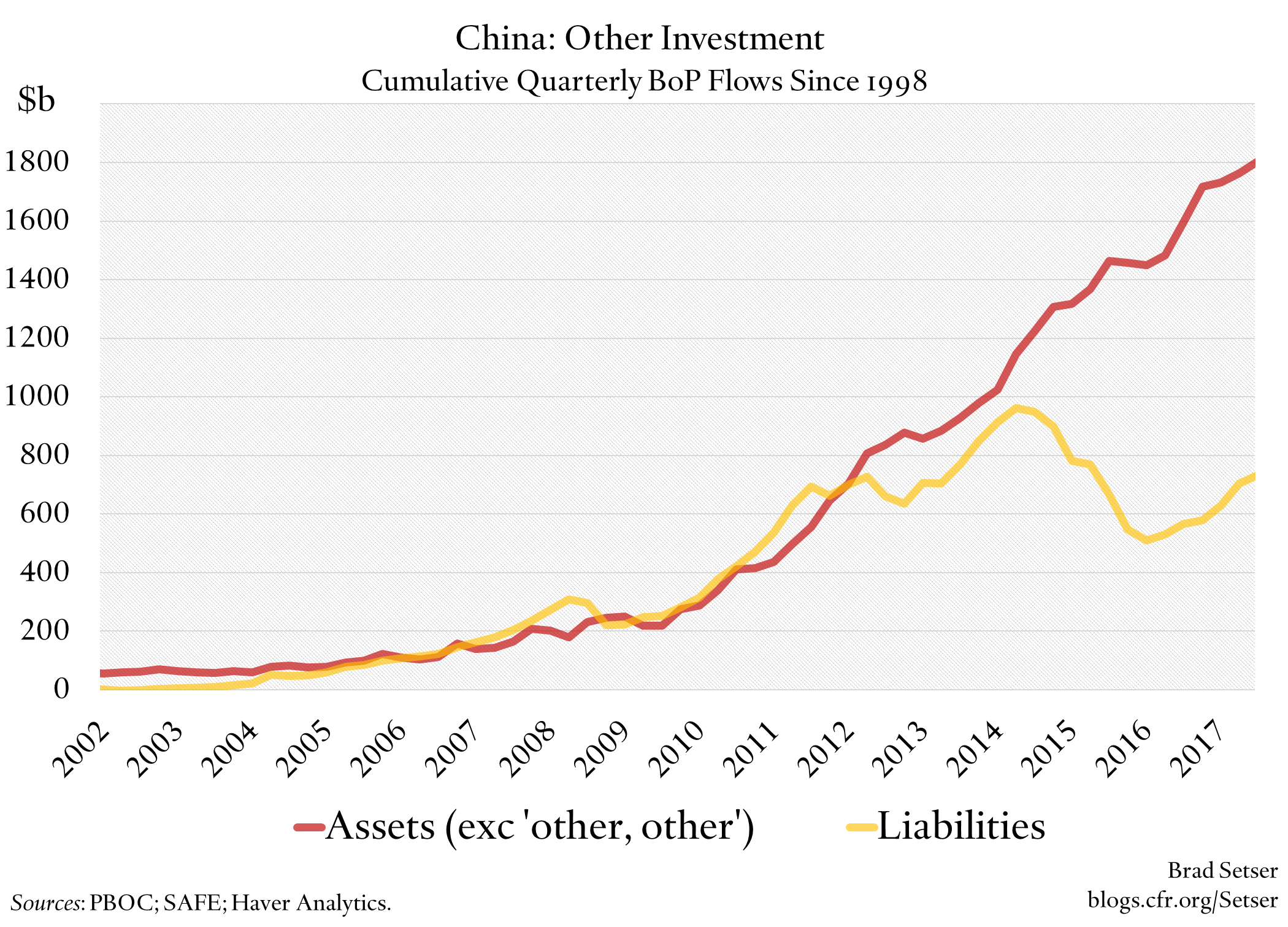

Not only did the pace of lending slow a bit, the Chinese banks were able to finance their external lending with external borrowing—so the need to draw on reserves to support policy lending abroad fell. The chart below shows the broadest possible measure of banking flows, one that captures short-term flows as well as long-term flows. But a chart showing only “loans” would tell the same story: the net outflow through the banking system fell in 2017.

I have been tracking this because I am interested in the sustainability of China’s currency peg, and more generally, the role that foreign exchange reserves and the state-guided channels for moving Asia’s savings abroad have played in sustaining Asia’s ongoing current account surplus.

There is a broader point here too, one that looks forward not just backward: even if the Belt and Road for now largely seems like rebranding of the policy lending that previously supported Chinese firms as they went out, it clearly has a lot of top-level support. That likely explains why the lending continued in 2016 even when the yuan was under significant pressure and China’s reserves were falling.

Now that the direction of the pressure on the yuan has changed and China is (likely) intervening again (if only modestly) to limit its appreciation,** China could decide to ramp up its policy lending. Part of the original motivation for encouraging Chinese banks to lend more abroad back in 2010 was that it kept China’s reserve growth down.

And it is also possible that China may now be looking to turn its state banks to do more than just lend some of China’s spare foreign exchange to the rest of the world.

In 2017, Chinese banks increased their external borrowing, and in a sense, started borrowing from the world to lend to the world. They were doing more than intermediating Chinese savings. They were mobilizing some of the world’s savings to back China’s strategic goals—taking a page from the United States‘ old global playbook.

* If it has geographic coherence, the key projects would provide stronger land linkages between China and Central Asia and Southeast Asia—and, through central Asia, a connection to South and Southwest Asia as well.

** The balance of payments data for 2017 shows a $90 billion reserve increase. The PBOC’s balance sheet data (which shows reserves at their historical cost) though doesn’t show a parallel rise. It isn’t entirely clear what explains the discrepancy. My best guess is that interest income is counted in the balance of payments data but doesn’t—for some reason—enter into the PBOC’s yuan balance sheet data.