The Impact of Tax Arbitrage on the U.S. Balance of Payments

I sat down with the FT’s Matt Klein for an Alphachat podcast on the international provisions in the December tax reform.

In the last month, the market’s focus has been on the impact of a rising fiscal deficit on Treasury yields—and the reasons for the dollar’s decline. The global impact of the reforms to the treatment of the global profits in the December tax reform is no longer front and center.

Tax, though, has a profound impact on the pattern of global trade.

It influences both where firms report their global profits on intangibles (like intellectual property rights), as well as the location of actual physical assets. The desire to shift profits around influences multinationals’ production decisions on things like concentrate for colas—or, more significantly, active pharmaceutical ingredients.

I don’t think that there is any doubt now that tax has influenced the U.S. balance of payments in significant ways (tax shifting also likely has reduced measured GDP a bit). But there is a real debate about the impact of the tax reform on incentives to shift profits out of the United States.

I talked to the FT’s Matt Klein about these topics in the latest edition of Alphachat.

My bottom line: the tax on GILTI (the global minimum tax that applies to intangibles income abroad) is too low to create an incentive for most firms to book profits in the U.S. rather than in their tax haven of choice, and the way intangible income is calculated creates a perverse incentive to shift tangible assets abroad. The income on tangible assets abroad won’t be taxed by the U.S. under the new (mostly) territorial system.*

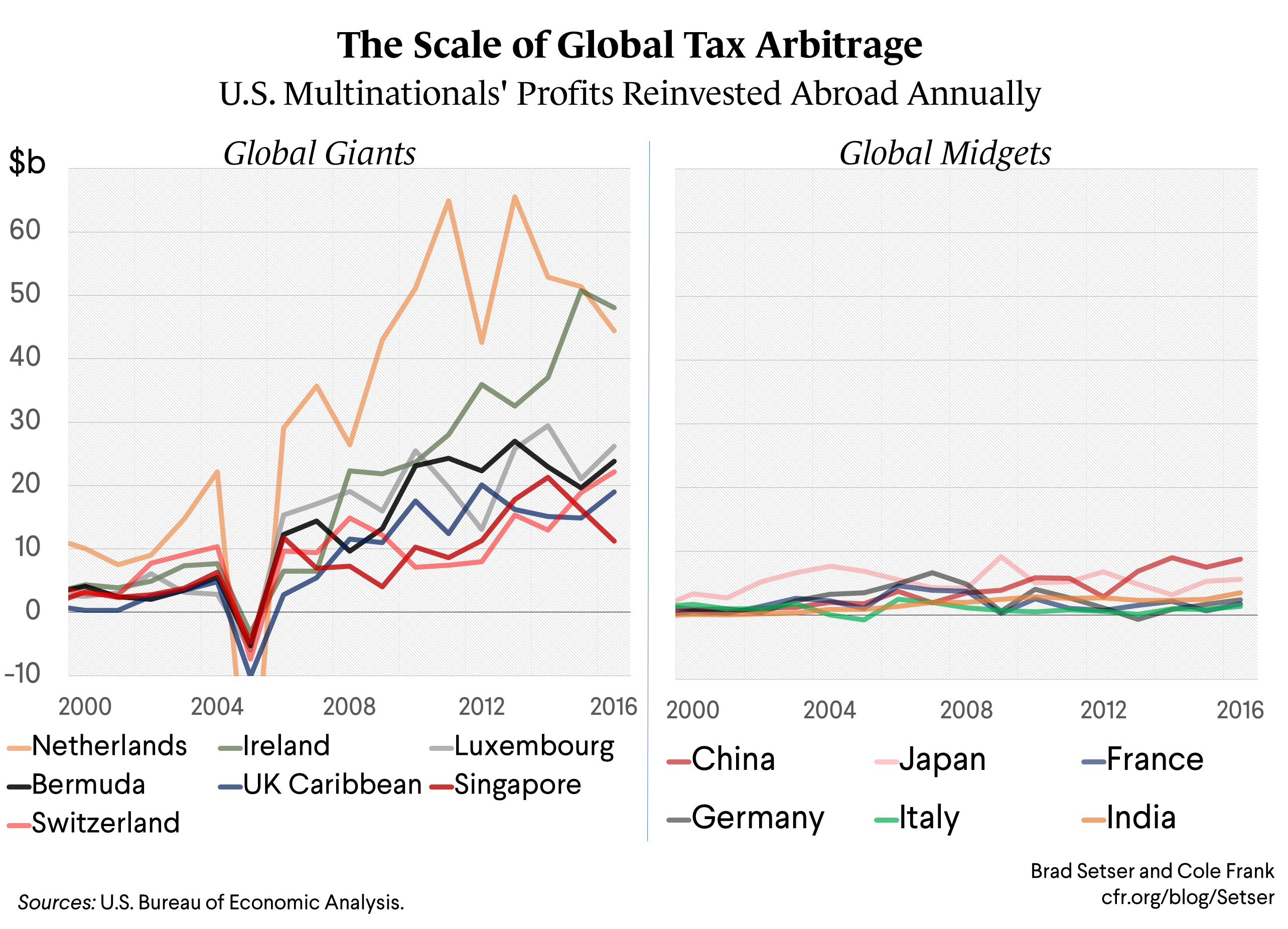

There is I hope now basic agreement that tax has distorted where firms report profits (and thus export revenues) in significant ways. If you look in the balance of payments data at the reported locations of “reinvested” earnings (e.g. funds that stayed abroad and were not repatriated, so they remained tax-deferred), countries like Ireland, Bermuda, and the Netherlands are giants. While the world’s biggest economies—countries like Germany, France, Japan, and China—hardly register at all.

“Gravity” stopped working in a big way.

The same, incidentally, holds for the numbers on services trade, at least that portion of the services data that isn’t a reflection of the physical movement of goods and people. In those categories of services trade that reflect trade in “intangibles,” countries like Ireland and Switzerland loom quite large. And that too, of course, is almost certainly a function of tax-related distortions.* But that is a subject for another time.

* Martin Sullivan has a more positive overall take on the overall effect of the corporate tax reform than I do, as he believes that the “BEAT” tax will limit the ability of foreign firms (including firms that moved offshore through inversions) to shift U.S. profits abroad. But he also believes that the reform increases the incentive to shift tangible production abroad. Robert Pozen’s take is closer to mine. I have learned a lot from the tremendous paper written by 13 tax experts last December outlining ways to game the new tax reform. I also recommend Richard Waters reporting on this topic; he doesn’t think the reforms will get rid of the incentive for the technology industry to shift profits offshore. Finally, Zoltan Pozsar of Credit Suisse has been investigating how the end of deferment will impact global financial markets, as tech and other companies will no longer end up running offshore credit hedge funds with their tax-deferred profits.

** Look at Tables 2.2 and 2.3 of the BEA’s interactive tables for services, particularly categories showing the geographic distribution of export of software, research and development services and business and management consulting services.