Can Anyone Other than the U.S. Fund a Current Account Deficit These Days?

Almost all oil-importing emerging economies with current account deficits are under market pressure to adjust …

The question is a bit rhetorical.

Some other advanced economies still are running current account deficits. And I don’t think China is really in current account deficit, and if it was, I personally don’t think a small deficit would pose any real problem. China in theory could fund a modest deficit with the interest income on its still substantial reserves ...

But there is no doubt that almost all the oil-importing emerging economies that ran external deficits last year are facing pressure to adjust.

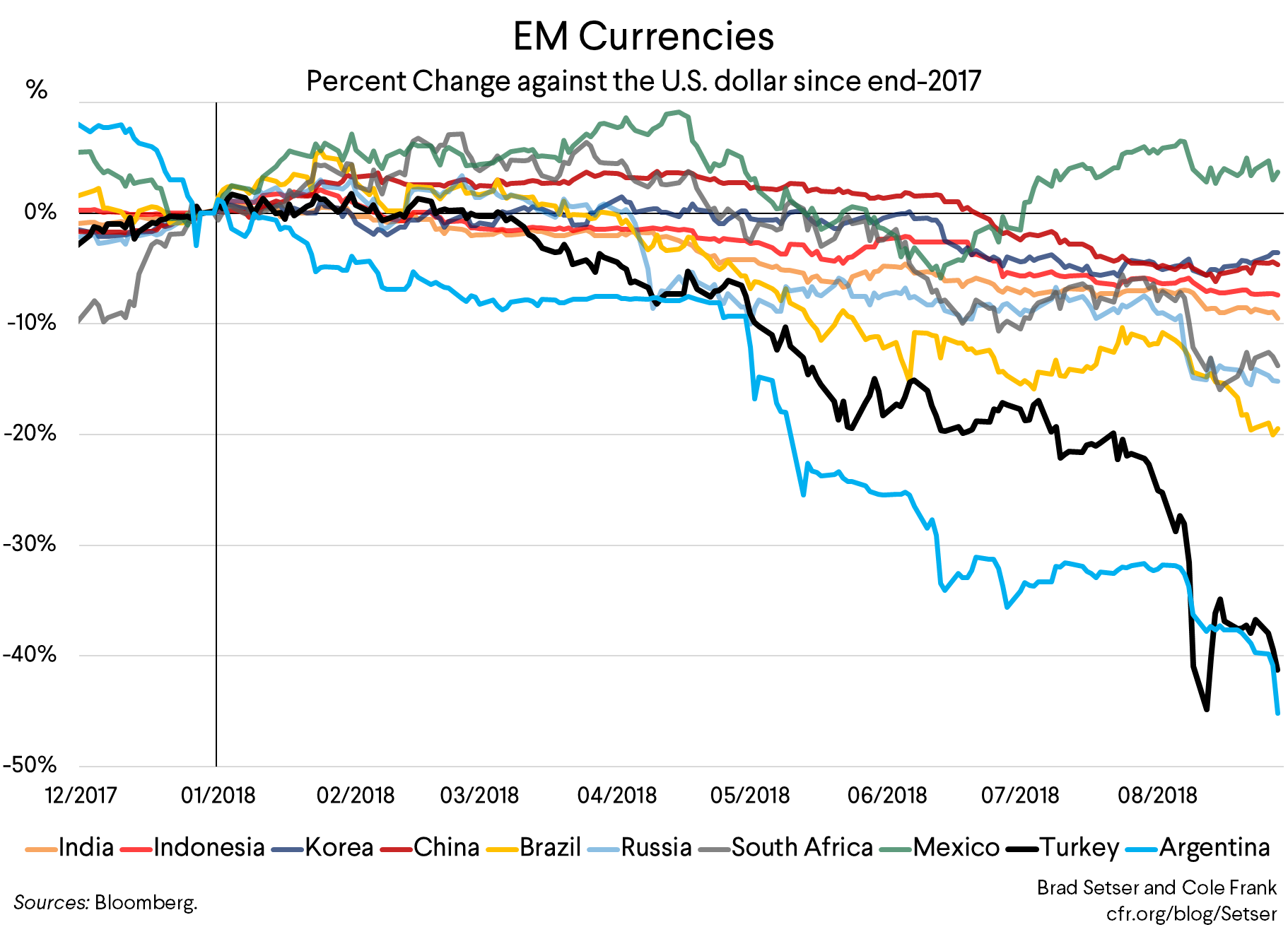

Argentina, obviously.

India—whose current account deficit looks to have widened to just over 2 percent of GDP.

South Africa.

Pakistan, though it is a much smaller economy than the others on this list.

Indonesia (no longer an oil exporter).

Brazil (though it doesn’t have much of a current account deficit).

Even Chile.

All have seen their currencies fall significantly this year.

I don’t expect Turkey’s troubles will prove contagious in the same way as Asia in 1997— India and Brazil have substantial reserves, and thus there is no real risk that a weaker currency will cause them trouble in repaying their external debt. South Africa and Indonesia don’t have access to comparable reserve stockpiles, but they are doing the right thing by letting their currencies adjust. Turkey and Argentina really did stand out as the two emerging economies with the most obvious vulnerabilities going into 2017—they had the largest current account deficits going into 2018, and insufficient reserves on standard debt-based metrics. The others are in a stronger position to manage the crisis through currency adjustment alone, without needing to borrow reserves to avoid a sovereign or bank default.*

But that doesn’t mean the pressure on oil-importers to adjust—meaning tighten policies, slow growth, and look more to exports to reduce their current account deficits—won’t have a global effect.

No deficits in oil-importing emerging economies and a higher surplus among the oil-exporters (who generally adjusted their imports down after the 2014 oil price shock and now “break-even” with prices in the 50s) means, mechanically, that there need to be adjustments elsewhere.

Broadly speaking, that could happen in two ways—

The large oil importing surplus countries could run lower surpluses. Germany, Korea, Japan, and the like could see their surpluses fall as emerging economies cut back …

Or one of the big advanced economies now running a substantial external deficit could run an even bigger deficit.

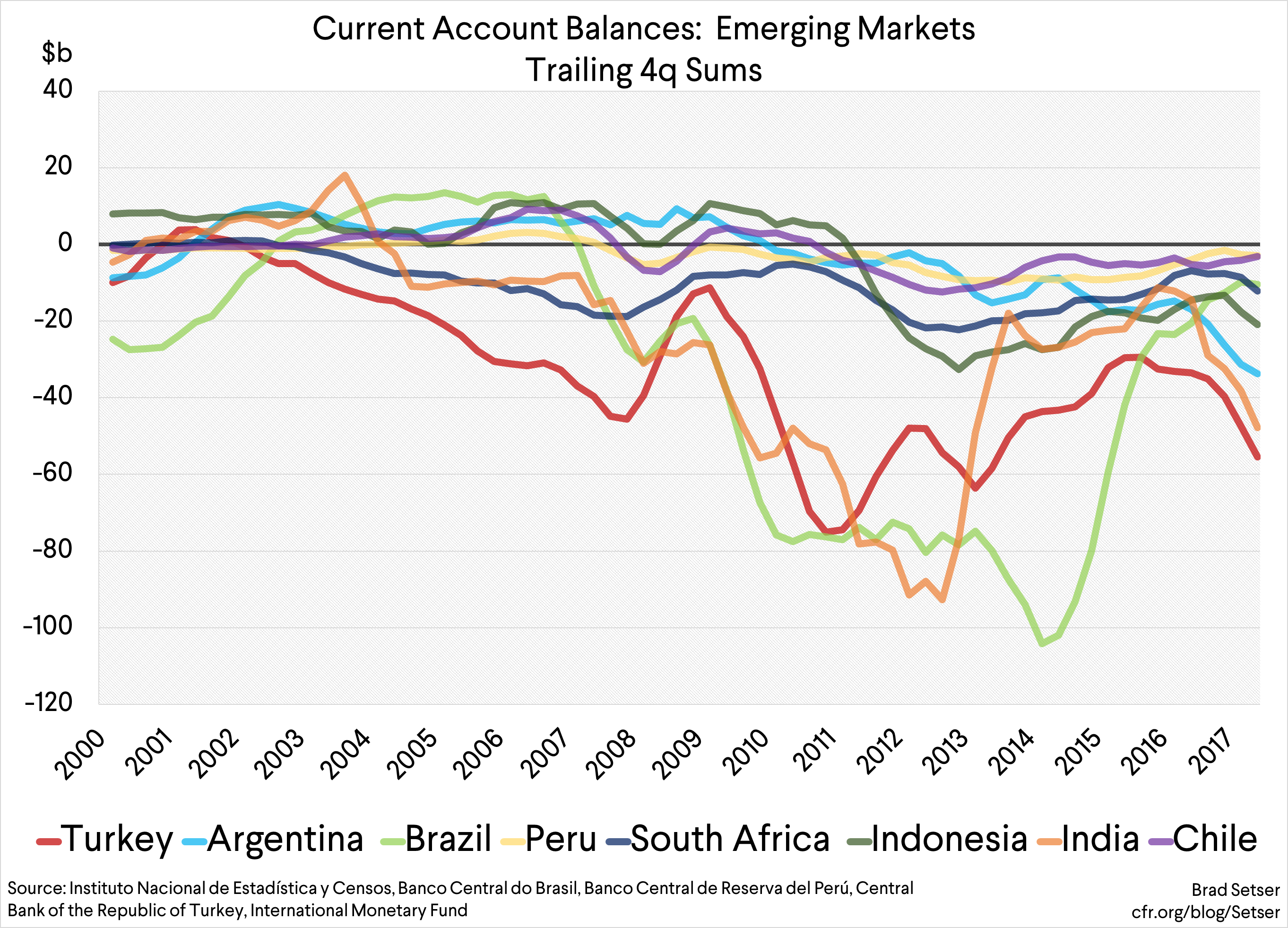

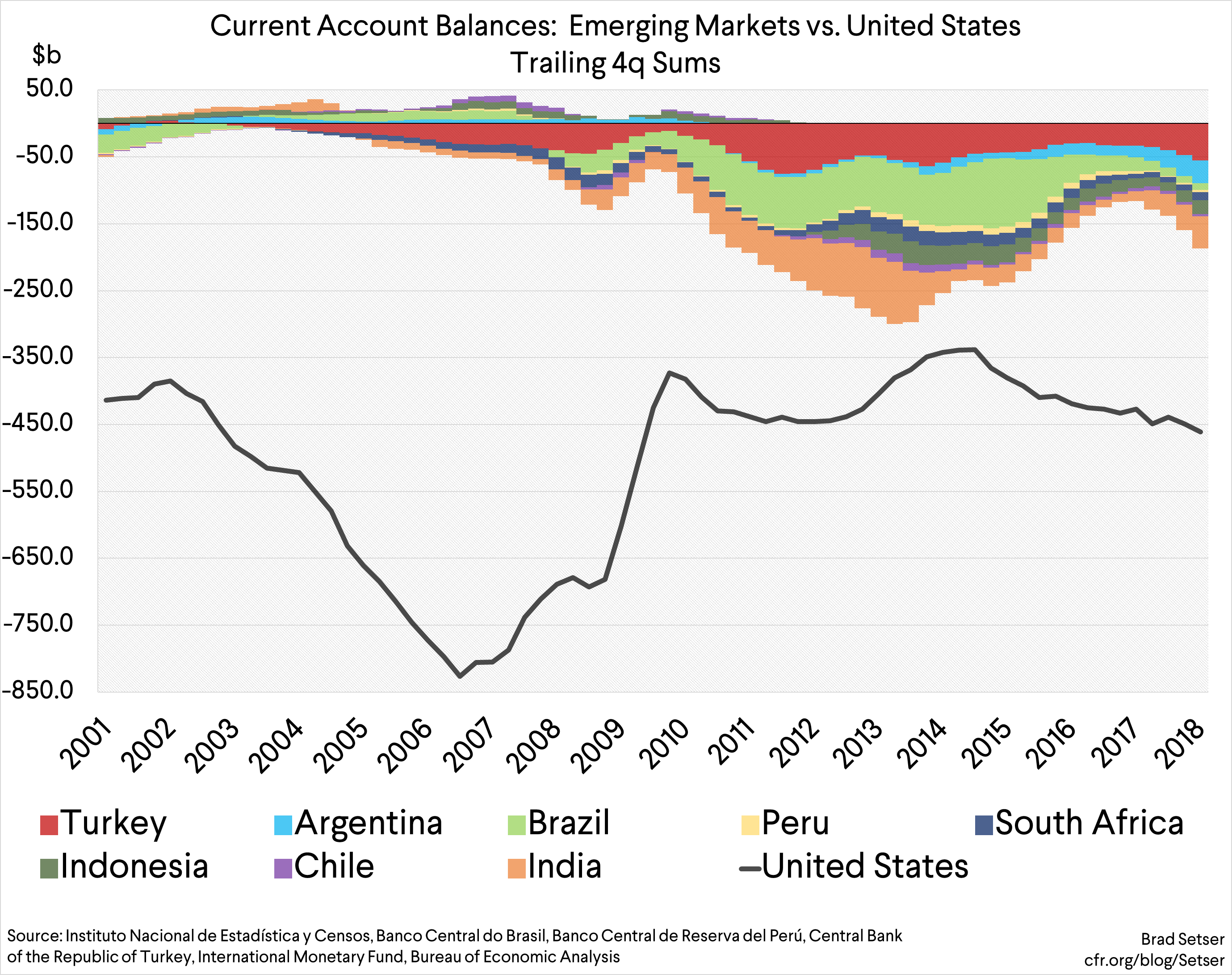

The overall deficit of a set of eight relatively large oil-importing emerging economies rose to about $200 billion in the last four quarters of data. The overall deficit of these countries is still smaller than it was in 2013, when the “taper tantrum” forced a significant adjustment. But the swing in the current account balance required to stabilize markets might be about as big as back in 2013 and 2014.

And despite Trump’s deeply held view that trade deficits are bad and a sign of “losing”, if “deficit” emerging economies are under market pressure to cut back, the odds are that the United States will end up with a larger deficit.

That’s what the foreign exchange market is signaling—the strong dollar means U.S. exports should fall (or grow less rapidly) than the exports of the euro area, Japan, Korea, and China. Plus, U.S. domestic policies are strongly supporting internal U.S. demand growth—while Germany, the Netherlands, Korea, and others maintain tight fiscal policies.**

To exaggerate a bit, the world may soon only have one borrower—

In some sense that’s a safe equilibrium: the United States borrows in dollars, so it is less exposed to the risks created by the Fed’s monetary tightening and a rising dollar than others. Exorbitant privilege and all.

In another sense though it is a disappointment: the United States already has a lot of external debt, it doesn’t really need any more. And it would be globally healthier if the savings of aging Europe and aging Japan and aging Korea and slow growing Taiwan flowed to the world’s young and potentially rapid growing emerging economies, not to fund inequality increasing tax cuts in the United States…

* Asia’s crisis led to a slump in demand for commodities, which put pressure on all commodity exporters in 1998. Oil was incredibly cheap in 1998. That isn’t the case now. The oil exporters are now experiencing a bit of a reprieve after several lean years.

** President Moon of South Korea does seem to be moving in the right direction. But with a 2% of GDP general government fiscal surplus in 2017 (according to the latest IMF WEO data) he needs to go even further. In the first half of 2018, it looks like tax revenue expanded faster than government spending. Both Korea and Germany have a ton of unused fiscal space.