Can China Reduce Its Internal Balances Without Renewed External Imbalances?

The rest of the world has a big stake in whether China responds to the demand drag from its construction and real estate slump with looser monetary policy or with direct stimulus to households.

Differing Views

Adam Tooze has drawn attention to two broad ways of interpreting China’s current slowdown.

One interpretation focuses on shifts in the balance between the state, the party, and the market under Xi. The recent politicization of China’s economy is the basis of the “authoritarian impasse” thesis put forward in Adam Posen’s well-known “economic long COVID” Foreign Affairs article. During the COVID lockdowns, China turned to a more authoritarian form of nationalism.

This thesis also is apparent in Eswar Prasad’s argument that China’s problems start at the top:

“Mr. Xi’s government has prioritized state enterprises, which hew closely to the Chinese Communist Party line and are under direct government control, over the private sector.”

In these accounts, Xi’s basic mistake has been a turn away from the market in his effort to assert the primacy of the party. In the process, he lost the trust of private investors both in China and abroad, as China now suffers from a crisis of confidence among its previously dynamic business class. And his authoritarian impulse, according to Posen, has made Chinese households more reluctant to spend even when China provided various forms of (modest) stimulus.

The other interpretation focuses on China’s deep structural challenges – notably its reliance on high levels of investment (especially property investment) to propel its high-saving economy forward. In this view – most strongly associated with Michael Pettis but also a long-standing theme of the Financial Times‘ Martin Wolf – China’s fundamental problem stems from relying on leveraged investment in residential property and infrastructure to mask underlying weakness in household demand. Wolf has noted:

“[China’s] gross national savings peaked at 52 percent of GDP in 2008. It was still at 44 percent in 2019, before COVID hit. Prior to 2008, nearly a fifth of these huge savings went into China’s current account surplus. After the crisis, such surpluses became politically and economically unacceptable. The alternative turned out to be even higher investment, much of it in property. Gross investment rose from 40 to 46 percent of GDP from 2007 to 2012.”

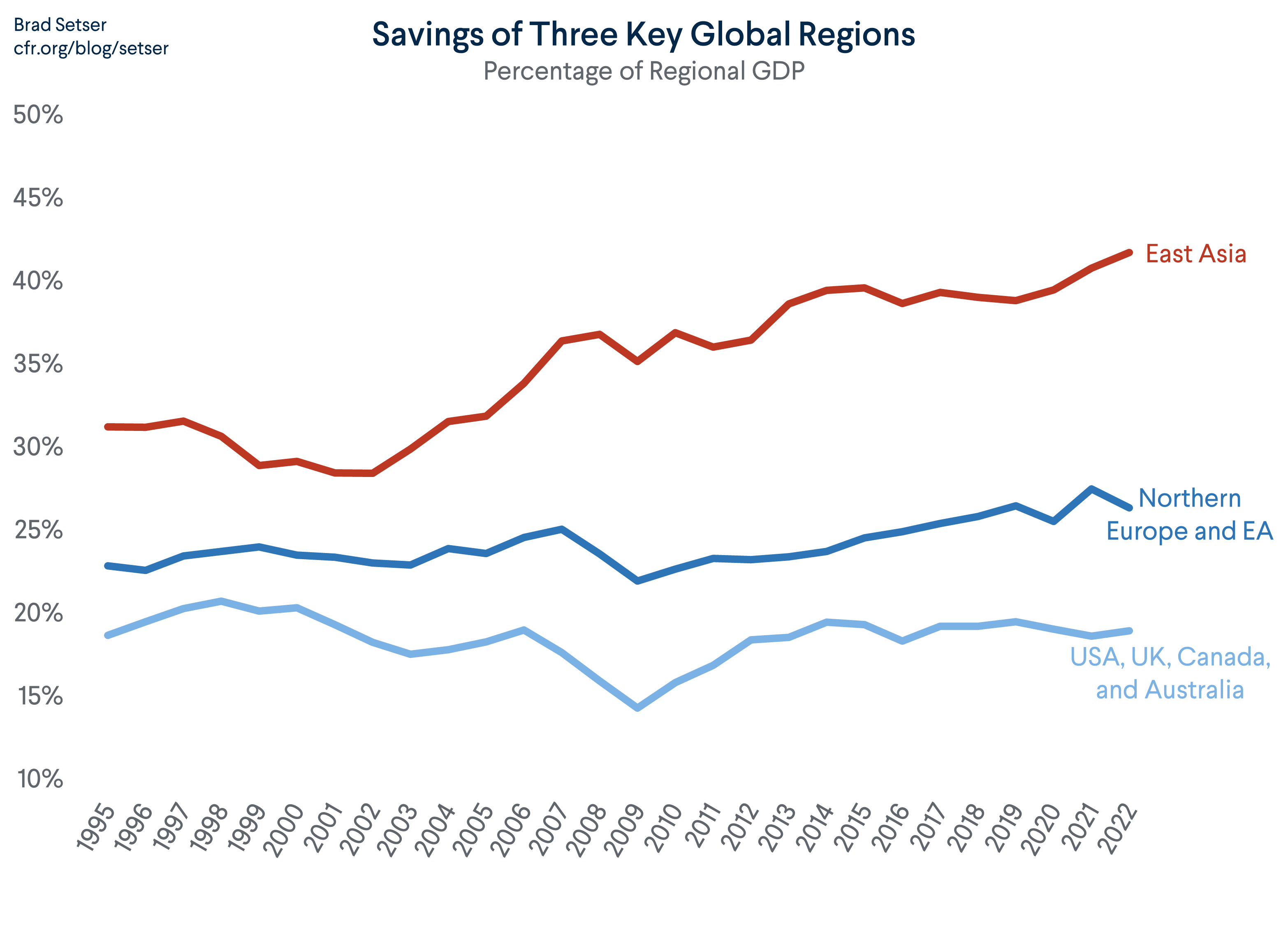

China’s national savings rate actually has increased in the past few years, contrary to widespread expectations that it would slowly fall. As a result, East Asia’s aggregate savings rate (the Asian savings glut, which has kept inflation in East Asia down) has increased in the last few years: China’s savings rate is rising, and China accounts for an ever bigger share of regional GDP.

In this interpretation, the underlying structural weaknesses in China’s economy predate Xi’s politicization of the economy, COVID, and – for that matter – Trump’s trade war.

China’s strong growth amid a structural glut of savings and limited household demand always depended on its ability to sustain turbo-charged rates investment. But investment now appears to be falling back toward more reasonable levels – the recent crisis among China’s property developers illustrated clearly that China has too many apartments relative to underlying demand. Household construction is expected to fall to 50 or 60 percent of its previous levels. Absent an alternative growth engine, China’s economy inevitably will slow, and potentially slow sharply. Xi’s policies haven’t helped, but China was headed towards a slowdown linked to a correction in excessively high levels of investment in real estate even if Xi had shown more interest in the old reform and opening up agenda.

I am personally associated with the structural view. I highlighted the risks posed by a high savings/high investment model in a 2016 working paper that I at least think has held up well, and again in Foreign Affairs in 2022:

“China’s banks, trusts, and other financial institutions have lent huge sums to China’s property developers, to households looking to buy apartments, and to local governments building public infrastructure even as China’s big policy banks financed construction projects around the world as part of its Belt and Road Initiative. China’s financial system could do both kinds of lending without borrowing large sums from the rest of the world, thanks to the country’s enormously high domestic savings rate, which has averaged about 45 percent of its GDP over the last 20 years … Saving is often considered a virtue and the absence of significant external debt gives China more options for managing the current property slump ... But too much saving helped create China’s current financial difficulties, as it fostered an economic environment where China’s rapid growth effectively required increasing domestic debt.”

China’s Response

These two interpretations of China’s economic woes – one that emphasizes the heavy hand of the state and party, and another that emphasizes the challenge of sustaining demand in an economy that saves close to half of its income – are not mutually exclusive. Most people think that a shift toward greater party control augmented the downturn in the property market that initially manifested itself in distress at highly-leveraged Evergrande and eventually resulted in cash flow difficulties even at the more conservatively managed Country Garden and most other major developers. However, the different readings of the cause of the current slump do tend to favor different views on the steps China should now take to revive its economy.

Those most worried about renewed authoritarianism and the reassertion of “Mao” (or Xi) over “markets” tend to prioritize policies that would signal decisive shift away from state guidance of the economy. That sometimes includes relaxing China’s current capital controls, and allowing the market to set China’s exchange rate. Posen explicitly argues that the U.S. should welcome Chinese flight capital and a weaker yuan.

The other view puts much more emphasis on implementing reforms that reduce structurally high rates of saving and that support domestic sources of growth, notably through policies that strengthen China’s underdeveloped social safety net and that support stretched local government balance sheets. There are concerns about the risk from local governments carrying out pro-cyclical fiscal tightening to make up for shortfalls in land sales as well as about Xi’s relationship with the businessmen whose created China’s top technology companies.

These views aren’t necessarily mutually exclusive either – many advanced market economies let markets allocate most capital while providing fulsome guarantees of access to healthcare and retirement security – but they do rub against each other uncomfortably at times.

Proponents of the need to show a strong commitment to markets would likely criticize policies to, say, raise Jack Ma’s income tax bill, while those focused on bringing down the high savings rate think China’s state absolutely needs to collect more personal income tax revenue.

Monetary Policy

There is a related debate – visible in the IMF’s analysis of China – over the macroeconomic policies that China should use to respond to the current slowdown.

One side of this debate emphasizes the need for China to use classic monetary policy tools and thus cut interest rates quickly and decisively to help spur the economy. The IMF’s latest Article IV includes a section (Box 3) on the benefits of interest rate cuts and a price-based monetary policy (emphasis added):

“China’s monetary policy framework has recently increased its emphasis on quantity-based monetary policy tools. These policies, which induce banks to increase net lending through non-interest rate means, have long featured in China’s policy toolkit. Their use has recently expanded given their promise of more precisely controlling credit growth and avoiding financial risk-taking. Adjustments to policy interest rates have become less frequent, both relative to China’s recent past and to other emerging markets. Evidence suggests these quantity-based policy tools should not substitute for traditional interest rate-based monetary policy.”

The IMF’s top leadership has reinforced this argument. First Deputy Managing Director Gita Gopinath recommended that “monetary policy should remain accommodative and rely more on interest-rate based measures.”

Using interest rates as a tool of macroeconomic stabilization is the norm globally, and there is little doubt that China deciding to use interest rates as the main tool of macroeconomic stabilization would be a significant policy shift, and a major reform.

Historically, China has relied on more targeted support for credit (and even, at times, direct regulation of the quantity of credit) than on moves in the policy rate. In a speech at the China Financial Forum in April, former PBOC Governor Yi Gang celebrated China’s commitment to what he called “monetary stability,” and highlighted the advantages of avoiding the extremes of G7 monetary policy:

“In terms of interest rates, we have likewise remained prudent and refrained from going to extremes, thereby keeping the fluctuations of policy interest rates within a relatively small range.”

Yi Gang also often talked about the advantages of structural monetary policies that targeted specific sectors rather than flooding the economy with cheap credit. He highlighted, for example, the special central bank facilities to support lending to small enterprises and the green transition. The PBOC also recently created a special facility to support the troubled property developers (with ambiguous results, it seems).

There consequently should be little doubt that China has, as the IMF noted, often used its policy levers to induce changes in bank lending without any overt change in the headline interest rate. Stepping back, cutting interest rates and letting the market allocate credit would be a real reform (though it isn’t quite clear how a market composed of large state banks would allocate credit in the absence of state guidance).

Changes in interest rates typically work through the more interest-sensitive sectors of the economy – real estate being one – as well as through the exchange rate – so they aren’t totally neutral across sectors. The fact that “market-based” interest rates reductions would typically work through encouraging an already investment and export-heavy economy to recover through more property investment and even more exports is a potential concern. Interest rate cuts on their own won’t magically shift income to low income households, or resolve long-standing fiscal tension between local governments and the central government in Beijing.

Fiscal Policy

The other option, of course, is classic fiscal policy.

More specifically in this case, central government borrowing to provide direct fiscal support for household demand.

A word of clarification: in China, “stimulus” generally has not meant borrowing by the government in Beijing to cut checks for China’s workers and households. China’s analogue to U.S. Treasuries – the bonds issued directly by China’s Finance Ministry and backed by the central government’s taxing authority – are only 15 percent of China’s GDP (there are other central government debts, but total central government debt is only 25 percent of GDP).** This aversion to centrally-financed fiscal stimulus has had a clear impact on China’s finances.

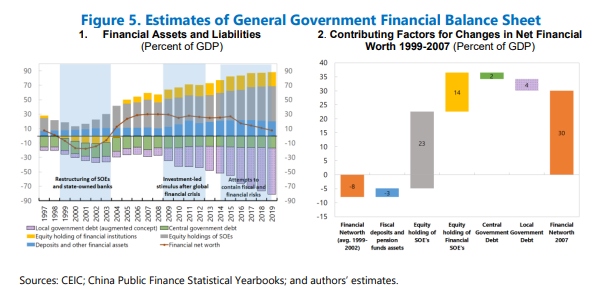

The formal balance sheet of China’s central government is remarkably strong in many ways. A recent IMF working paper highlighted how the combination of limited central government direct borrowing and the central government’s ownership of some of the most valuable companies in China through the State-owned Assets Supervision and Administration Commission of the State Council (SASAC) has left the central government with a positive net financial worth (SASAC’s vast portfolio includes the railways, the airlines, the telcos, the electricity grid, the petroleum companies, the biggest grain importing company, the biggest shipping company, and the big banks).

Stimulus in China generally has meant allowing local governments to borrow heavily (off-balance sheet, then on-balance sheet, then on- and off-balance sheet) to invest in infrastructure and industrial development.*** It also has typically involved allowing bank credit to flow more easily into the property market – and at times it clearly has meant liberalizing financial regulations, including by allowing credit to flow to the economy outside the formal banking system (China’s unregulated shadow banks that offered what looked like high-yielding deposits that weren’t backed by regulatory capital and weren’t subject to reserve requirements; Logan Wright has all the details on China’s post-crisis deregulation and the subsequent deleveraging campaign).

Thus, stimulus took a form that made it seem a bit like monetary policy and a bit like a decentralized fiscal expansion– but without a lot of central government borrowing or much direct support for Chinese households.

Some – including President Xi according to the Wall Street Journal’s excellent China team – think direct support for household demand is a Western policy tool that China should avoid. Xi reportedly believes that household checks are wasteful, as the increase in government spending raises the level of debt but doesn’t create any hard assets. China’s leaders also worry that a stronger social safety net – more substantial unemployment insurance payments for example – would encourage “welfarism.” As a result, China has supported business income through tax cuts during the pandemic without really ever providing much direct support for households.

A household-focused stimulus also faces structural challenges, as China’s policy infrastructure isn’t designed to support households through the national budget. The IMF had a very good series of papers (links can be found this blog) looking at these issues back in 2017 and 2018. But there are steps Chinese policymakers could take if they really wanted to do so. Rebating a portion of mandatory social contributions (China’s payroll tax), for example, is technically feasible.

The Ripple Effect

There is a clear overlap between the position many take on these macroeconomic issues and their views on China’s underlying structural problems. Many of those who believe that China has suffered from a reassertion of state control over the economy under Xi are sympathetic to a policy stance that currently focuses on lowering interest rates, liberalizing capital controls, and even allowing the yuan to float. They are not especially concerned if that means the yuan would float down far more rapidly that it was ever allowed to float up.

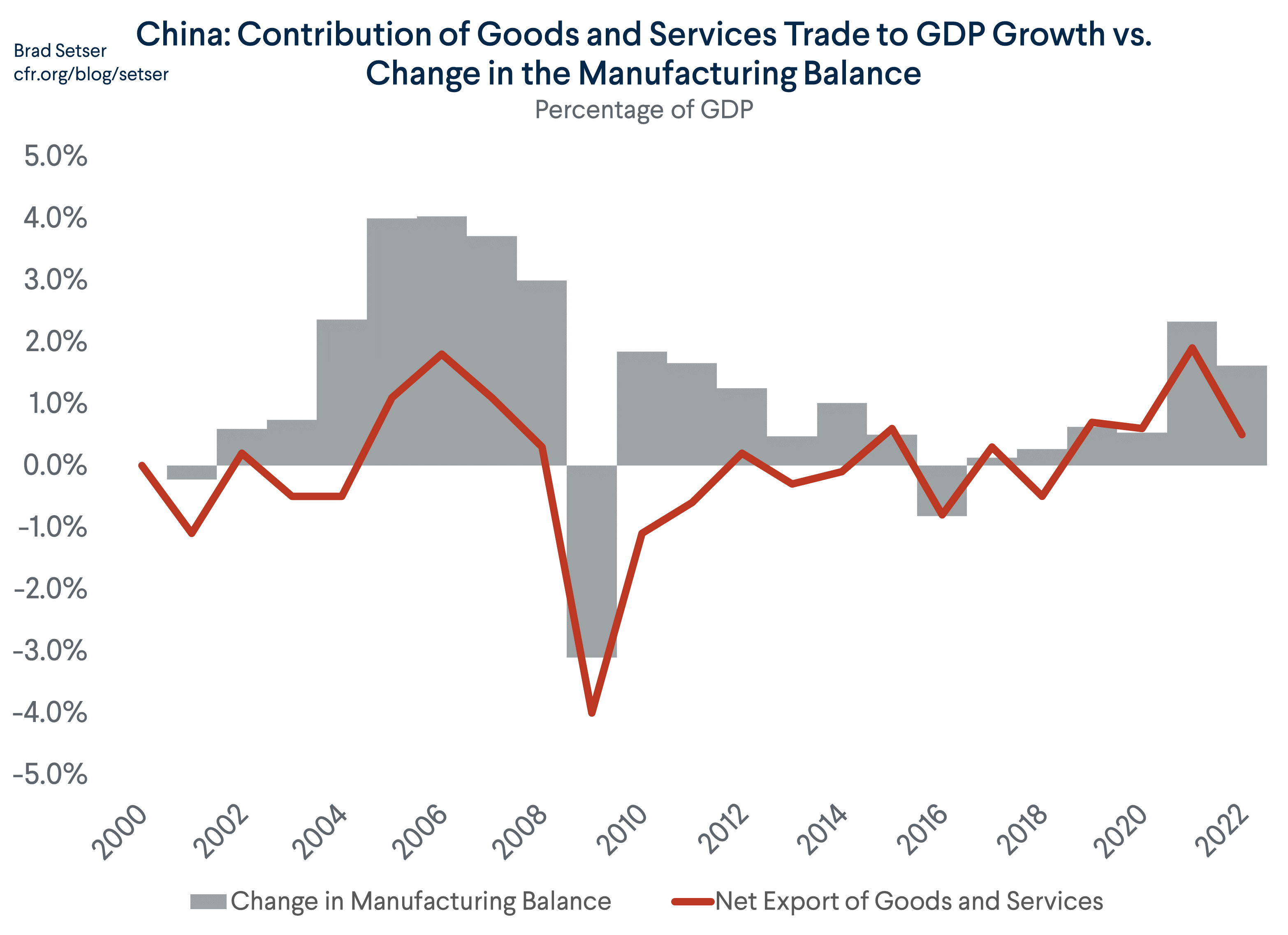

Yet China’s trade surplus is already very large. The headline goods surplus is about 5 percent of China’s GDP, and the underlying surplus in manufacturers is close to 10 percent of GDP.

I certainly worry that if China relied entirely on interest rates cuts, exchange rate liberalization, and a weak yuan to offset the property slump, China’s external trade surplus could increase to record levels relative to the GDP of its trade partners. China, far more than other large economies, relied on net exports to sustain its economy during the pandemic. It would be placing a significant further burden on its trading partners if it ends up relying on an even bigger manufacturing surplus to offset the slack created by its property downturn over the next few years.

Fiscal stimulus (of the classic kind) differs from monetary stimulus (of the classic kind) in one critical respect: it potentially allows China to achieve full employment by producing to meet domestic Chinese demand for goods rather by producing for global consumers.

Thus, China’s choice of policy direction in the face of what is likely to be a sustained slump in its property market will have significant repercussions for the world.

Low inflation in China, together with the yuan’s fall to 7.3 against the dollar, has pushed China’s real effective exchange rate down by about 10 percent over the the last year and a half. If China relied on classic monetary policy tools and let the exchange rate slide, the real effective exchange rate could depreciate by a further 10 percent, if not more. The resulting surge in exports would help China achieve internal balance (full employment) but it would do so in part by moving further away from external balance. Most estimates suggest that a 10 percent swing in China’s real effective exchange rate leans to a swing of 1.5 percent of GDP in net exports.

Of course, China being China, it isn’t likely to make a clear choice between classic monetary stimulus and classic fiscal stimulus. Chinese policy always has Chinese characteristics – China’s fiscal stimulus in 2009 looked in some ways like a regulatory loosening and a monetary easing rather than a classic fiscal stimulus; China’s monetary tightening has often been carried out through regulatory tightening rather than rate hikes. Indeed, China’s underlying policy tools don’t neatly map to standard American textbook macroeconomics.

But even if fully anticipating China’s policy response is difficult, it isn’t hard to forecast that China’s domestic policy choices over the coming years could have large external spillovers.

* China’s saving rate has increased since 2018, contrary to widespread expectations of a trend decline.

** See Table 2 of the IMF’s latest staff report. The substantial debts of the Railway Ministry are a key reason why central government debt is about 25 percent of GDP. Recognized local government debt is much higher, about 35 percent of GDP. There is no agreement on the scale of China’s additional quasi-fiscal debt (from the LGFVs).

*** The Lam and Badia IMF working paper has an excellent explanation on the uniqueness of China’s post-global financial crisis stimulus, highlighting that it was in many ways less a classic stimulus and more a relaxation of regulatory constraints on local governments:

“The stimulus involved only a modest cumulative fiscal expansion of 2 percent of GDP. The rest was mostly financed through the off-budget relaxation of local government financial constraints, which were encouraged implicitly through regulatory changes. Initially, Chinese local governments financed the additional spending through bank loans but when faced with big rollovers in 2012 they resorted to nonbank debt financing ... The relaxation of budget constraints on local governments was very effective in paving the way for the large-scale fiscal stimulus. While local governments were formally prohibited under the 1995 budget law to borrow, typical arrangements would be for a local government to transfer the ownership of land (government asset) to an LGFV, which would use the land as collateral to borrow from banks or capital markets. In this way, local governments were allowed to bypass the 1995 budget law while the central government did not have to show up an increase in debt in its own balance sheet ... About 70 percent of the stimulus was financed off-budget (RMB2.8 trillion out of a total 4 trillion).”