The Changing Nature of Turkey’s Balance Sheet Risks

Pay attention to banking system’s foreign currency exposure to the government …

The lira was under a fair amount of pressure today. Bloomberg reports the state banks were selling $400 million to try to limit the lira’s depreciation. Even so, the lira fell through 8 Turkish lira to the dollar. The central bank’s decision last week to hold the headline policy rate constant looks to have been a mistake.

A few years back, the big balance sheet risk in Turkey that worried outside analysts was the foreign currency exposure of Turkey’s corporate sector, as Turkish firms had significant external borrowing and had, in many cases, taken out large foreign currency denominated loans from the domestic banks. A weaker lira means, obviously, that any existing foreign currency debt is harder to pay back.

Those exposures are by and large still there—some external loans have been paid back, and some domestic foreign currency debt has been restructured. But, to the best of my knowledge, the domestic banks are still sitting on close to $50 billion in loans to the energy companies (some of which has been restructured) and something like $30 billion or so in loans to the real estate sector (at least $10 billion of which may be troubled).

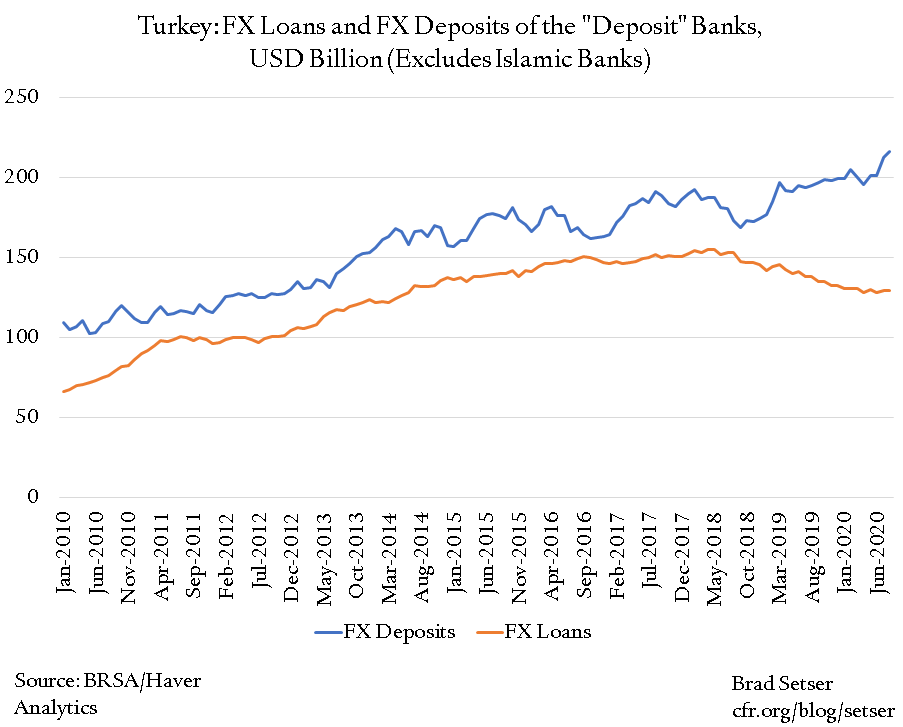

But the banks‘ foreign currency exposure to Turkey’s firms is in a sense a legacy problem. The recent lending boom has almost all been in lira. Foreign currency loans have been declining absolutely, and relatively to the banking system’s foreign currency deposits.

Right now, the banks have around $220 billion in domestic foreign currency deposits and less than $130 billion in domestic loans.

In various ways, those domestic deposits have been lent to the government, creating a substantial new direct exposure to the government.*

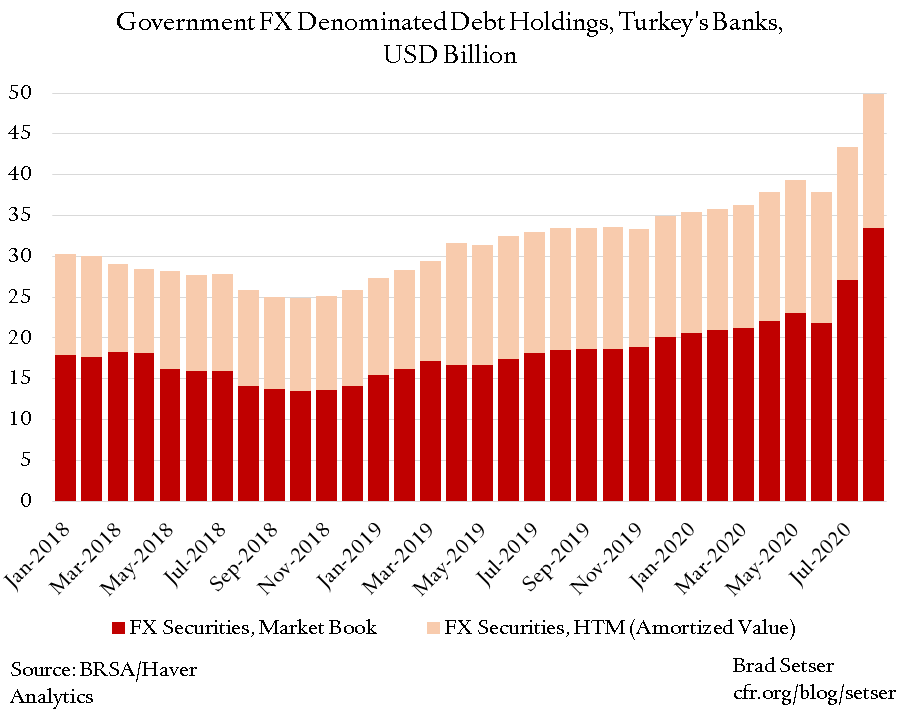

The government has now issued nearly $30 billion local law but foreign-currency denominated instruments—almost all held by the domestic banks. And of course the banks still have a substantial portfolio of the Government of Turkey’s Eurobonds, supposedly close to $30 billion counting the eurobonds held in the banks‘ offshore branches (including, I would assume, some of the $2.5 billion five-year bond issued in October).

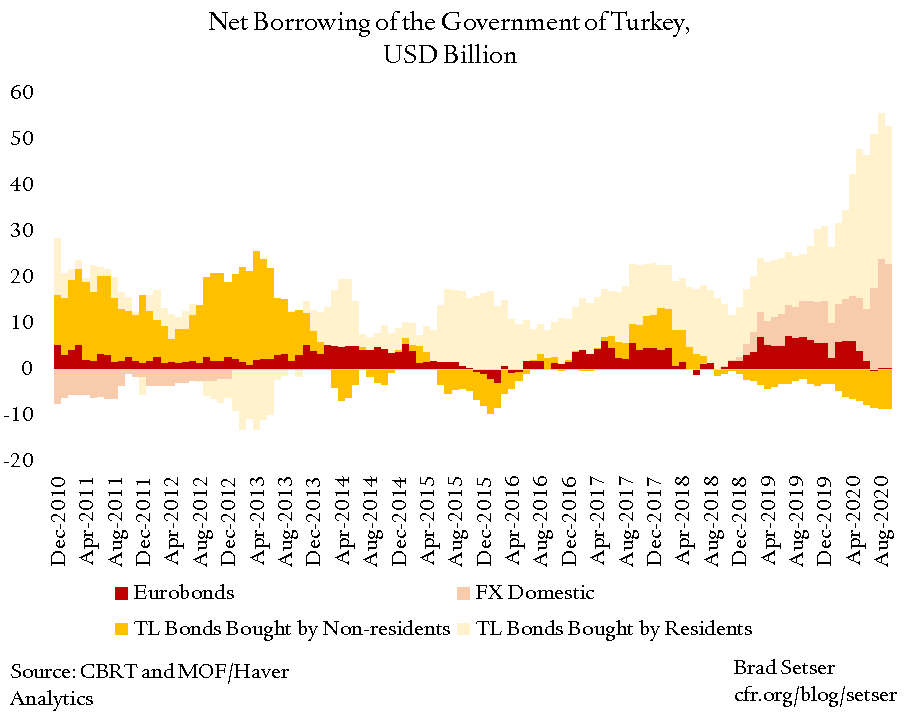

Basically, a large share of Turkey’s fiscal deficit is currently being financed in foreign currency by the domestic banking system. That’s a big shift from the past, when the government’s borrowing need was often met by yield-seeking foreign creditors buying Turkey’s local law currency bonds.

The banks also have credit exposure to the government now as a result of all the dollars they have lent to the central bank. What used to be the safest of safe assets—dollars held on deposit at the central bank or dollars swapped with the central bank to obtain lira financing—is now quite risky as the Central Bank of the Republic of Turkey’s (CBRT) net foreign currency reserves are negative. The CBRT has sold a fair amount of what in effect is borrowed foreign currency into the market to defend the lira. Laura Pitel of the Financial Times reports, “that effort [to support the lira] has taken a heavy toll on the country’s foreign currency reserves, prompting the rating agency Moody’s to warn last month that Ankara had “almost depleted the buffers that would allow it stave off a potential balance-of-payments crisis.”

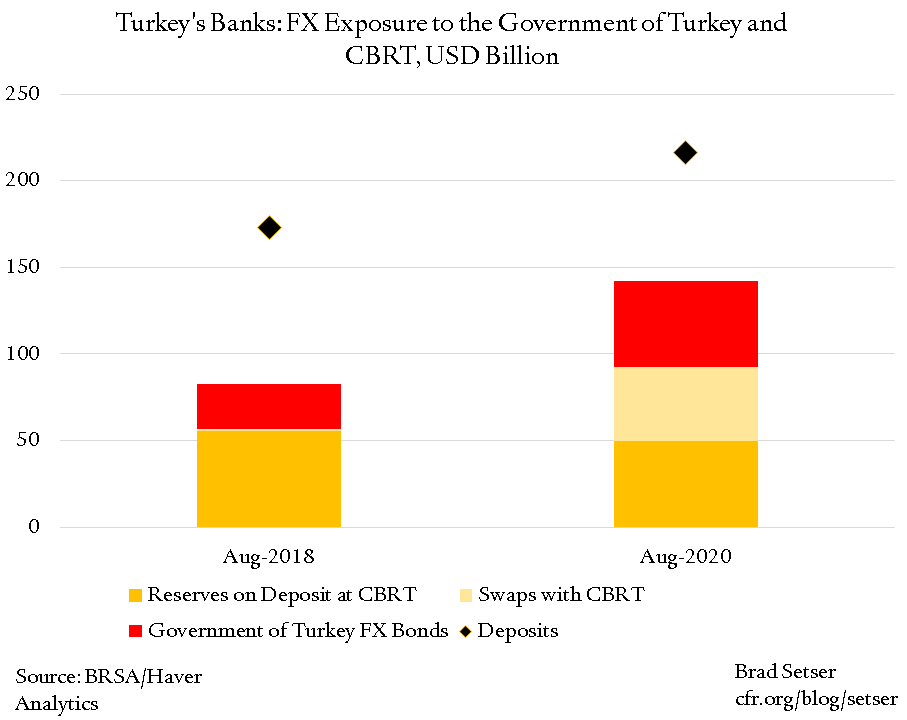

Between the banks‘ foreign exchange on deposit at the CBRT (as part of their reserve requirement) and the banks’ approximately $40 billion in swaps with the CBRT, the banks have effectively lent about $100 billion to the CBRT. The CBRT, though, has less than $40 billion in foreign currency assets (it also holds some gold of course), and over $15 billion of those foreign currency assets appear to be in Qatari rial rather than euros or dollars (see the detailed disclosure of Turkey’s end August reserves).

That makes the banks’ exposure to the CBRT a potential risk, not a source of strength.

In very ballpark terms, a few years back the banking system had $150 billion in domestic deposits and $150 billion in external funding (mostly loans and bonds, but some deposits) on the liability side, $150 billion in domestic loans on the asset side plus $20 billion or so of Eurobonds, $20 billion or more of offshore foreign exchange deposit, over $50 billion of foreign currency at the CBRT, and say $30 to 40 billion of market swaps (providing foreign investors with exposure to the lira). The banks had exposure to credit risk on their foreign currency book and absent access to the CBRT, they were taking on some funding risk of their lira swap book. But those risks were balanced by a large portfolio of undeniably liquid foreign currency assets.

Today the banking system looks different. While $50 billion in foreign currency funding has fled over the past two years, domestic residents have moved that much into their foreign currency deposit accounts. As a result, the total foreign currency balance sheet remains large (~$300 billion). On the asset side, the banks still have exposure to Turkey’s firms (including some exposures implicitly or explicitly backed by the government). But increasingly the banks biggest foreign currency exposure now is to a single borrower—the Government of Turkey.

Sum up the banks‘ exposure to the central bank, the banks’ exposure to government’s local dollar debt, and the banks‘ holdings of Eurobonds, and close to $150 billion (about half) asset side of the banks’ foreign currency balance sheet is Turkish sovereign risk. More really, given that some of the foreign currency lending to various projects is implicitly backed by the government...

What does all this mean? Well, the fate of Turkey’s banks is increasingly tied to the fate of Turkey’s government—and the stability of the government’s finances equally depends on the stability of the banks’ foreign currency funding base. So far, Turkish deposits have retained confidence in the Turkish banks, which has allowed Turkey to muddle through. But not without some important changes: the dollarization of the deposit base has led to the dollarization of the government’s domestic liability structure as well.

*/ The banks also have indirect exposure to the government through the loans provided to back various mega-projects (the new airport, the third bridge, and the like) which have government revenue guarantees.