Turkey Shows the Value of Balance Sheet Analysis

Selling reserves borrowed from the banks ultimately puts the health of Turkey’s banks at risk.

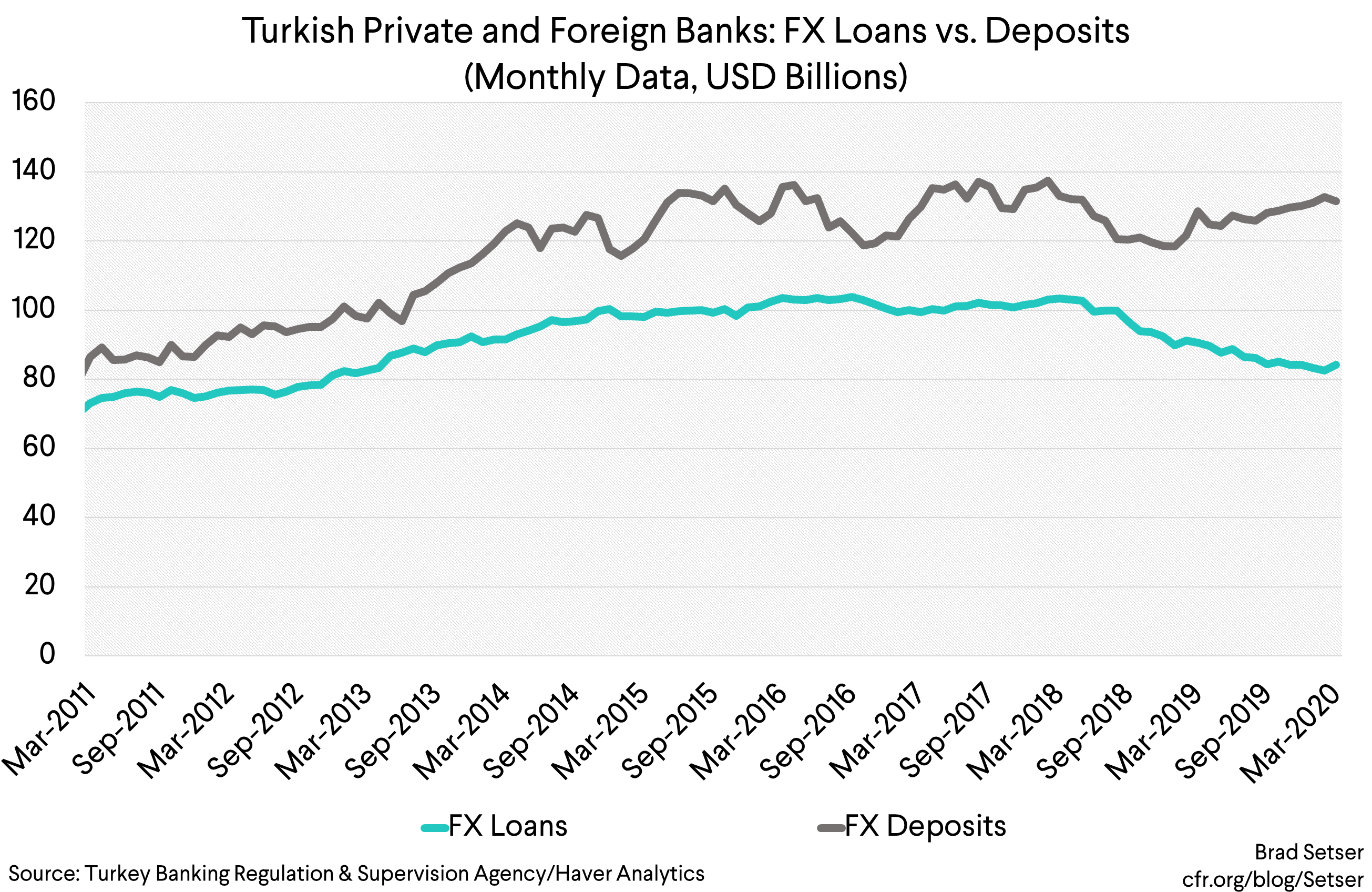

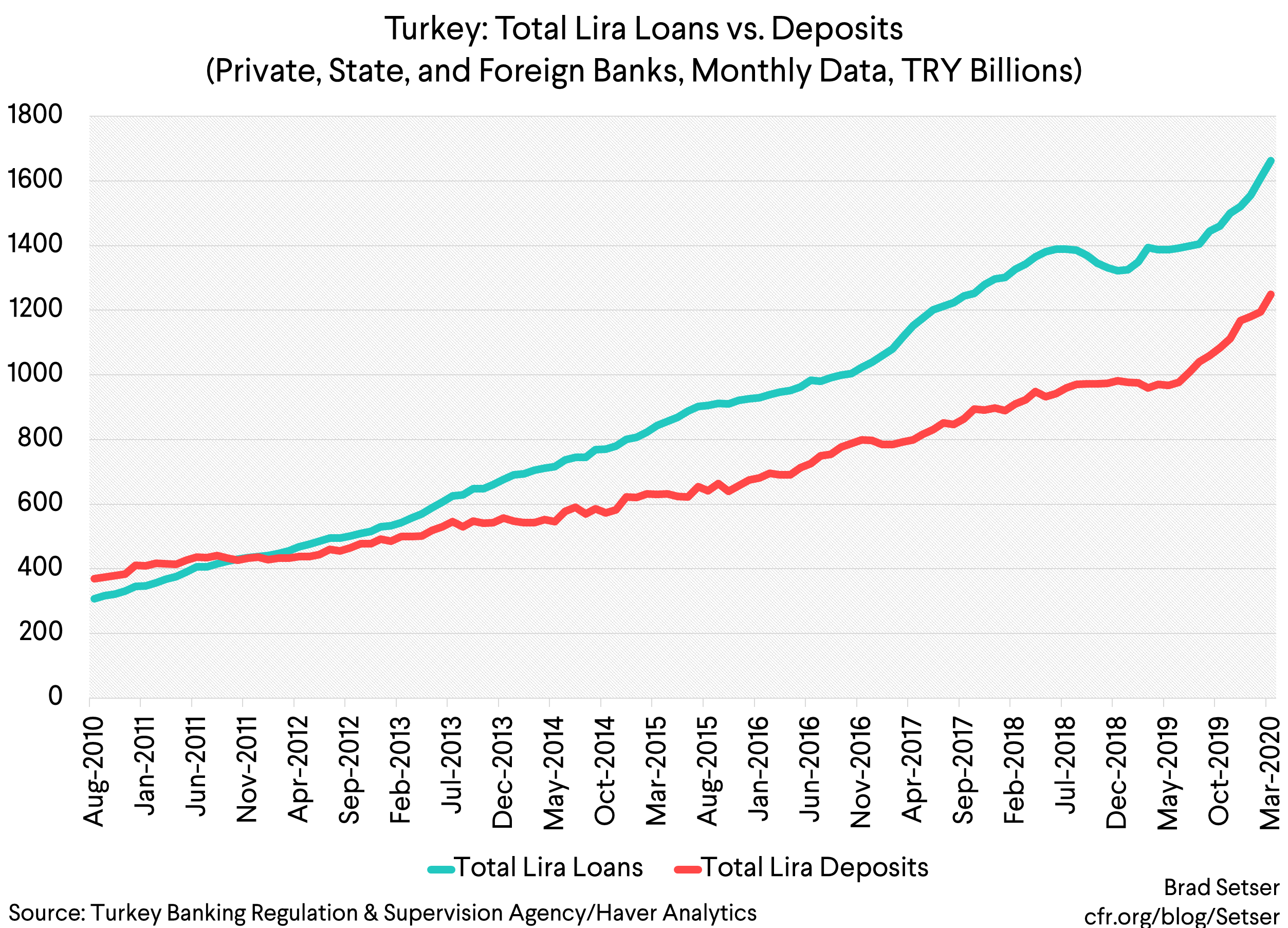

Turkey’s banks have long had more foreign currency deposits than foreign currency loans.

That’s only become more true during the past year and a half of stress.

Domestic residents have shifted toward foreign currency deposits, while domestic foreign currency lending has trended down. The private (and foreign owned) banks have $47 billion more in foreign currency deposits than foreign currency loans. The state banks have $20 billion more.

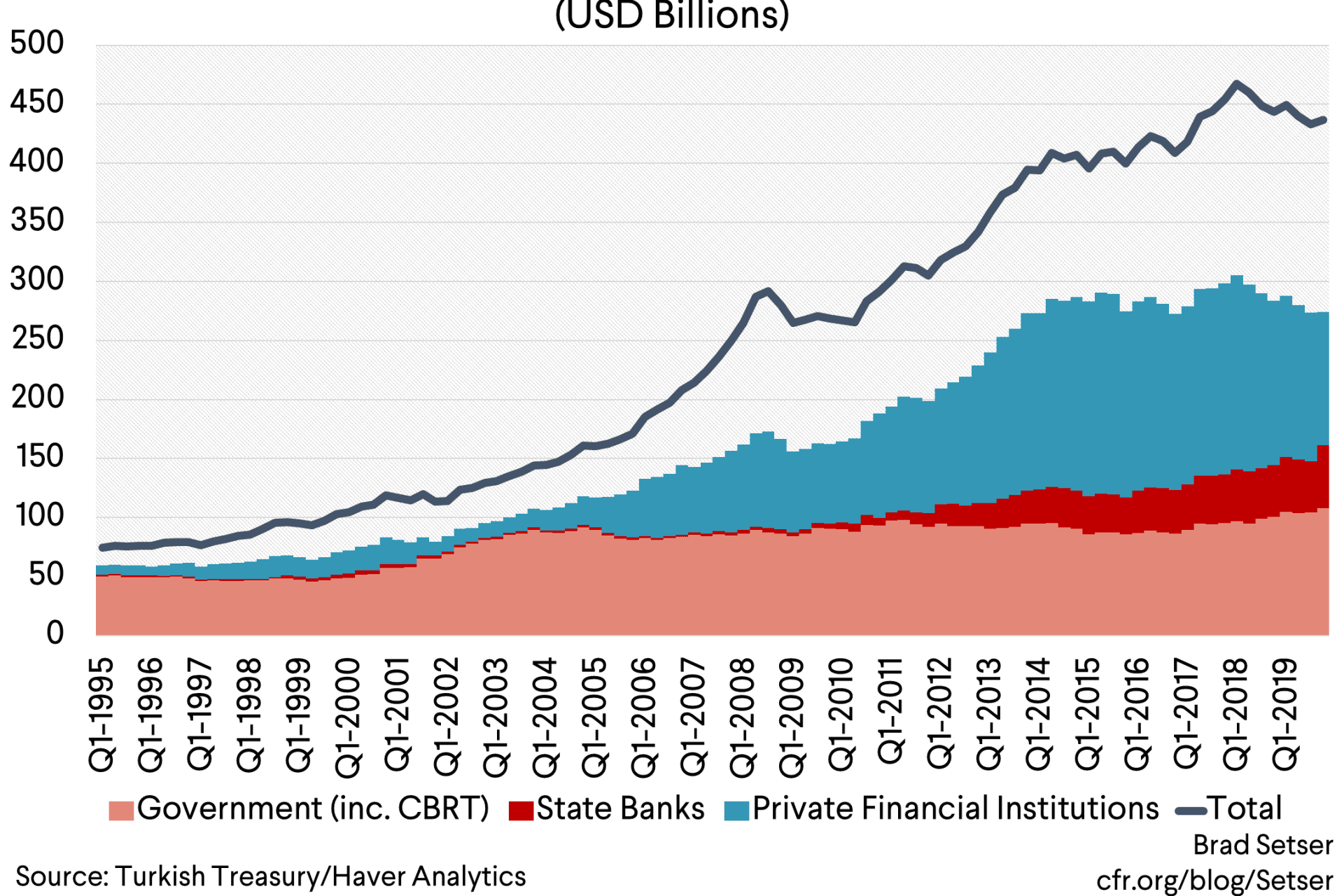

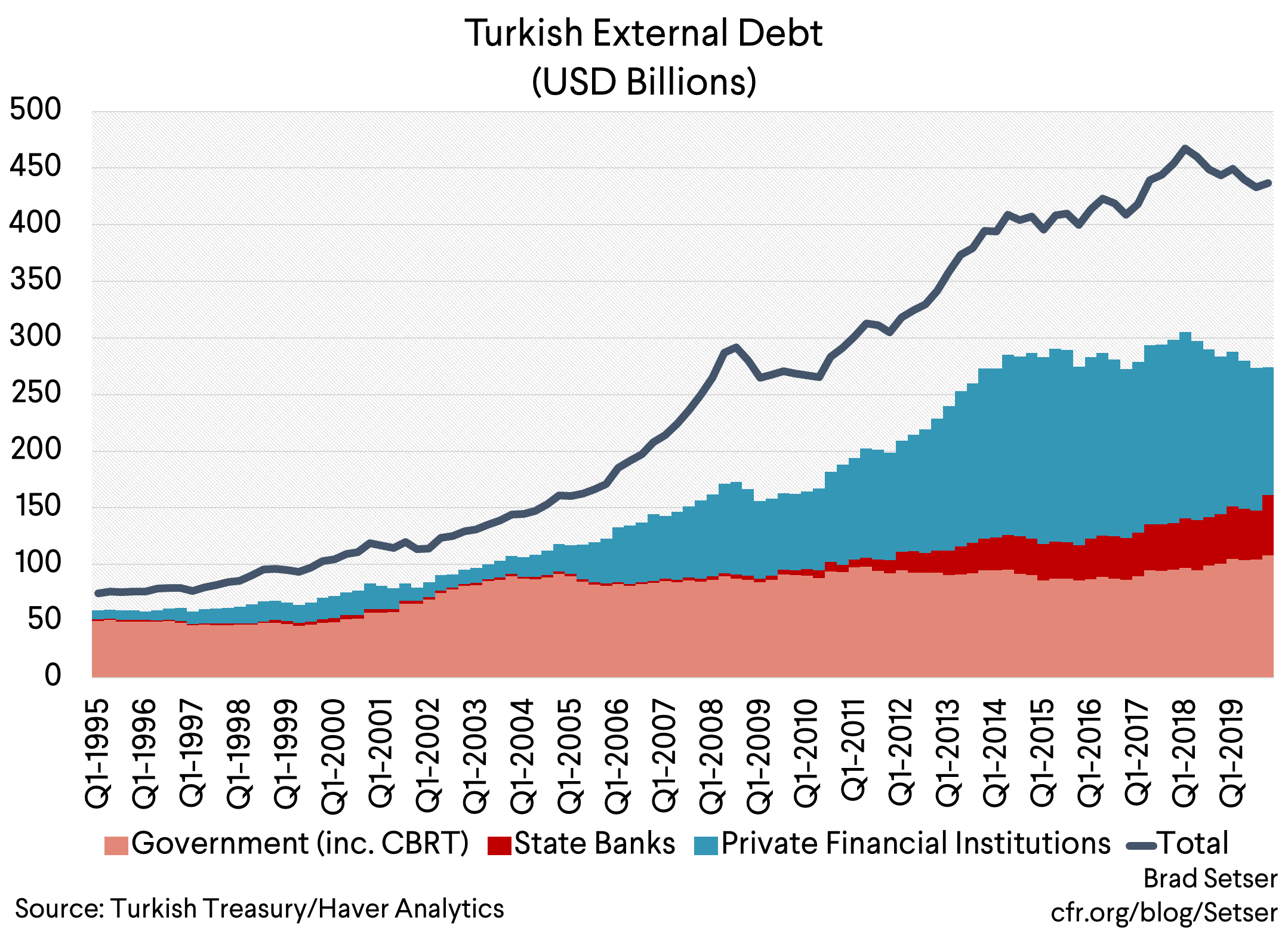

The great financial puzzle posed by Turkey is why, given the strong domestic foreign currency deposit base of Turkey’s banks, they nonetheless went out and borrowed a lot of foreign currency. The banks account for around $150 billion of Turkey’s $450 billion in external debt.

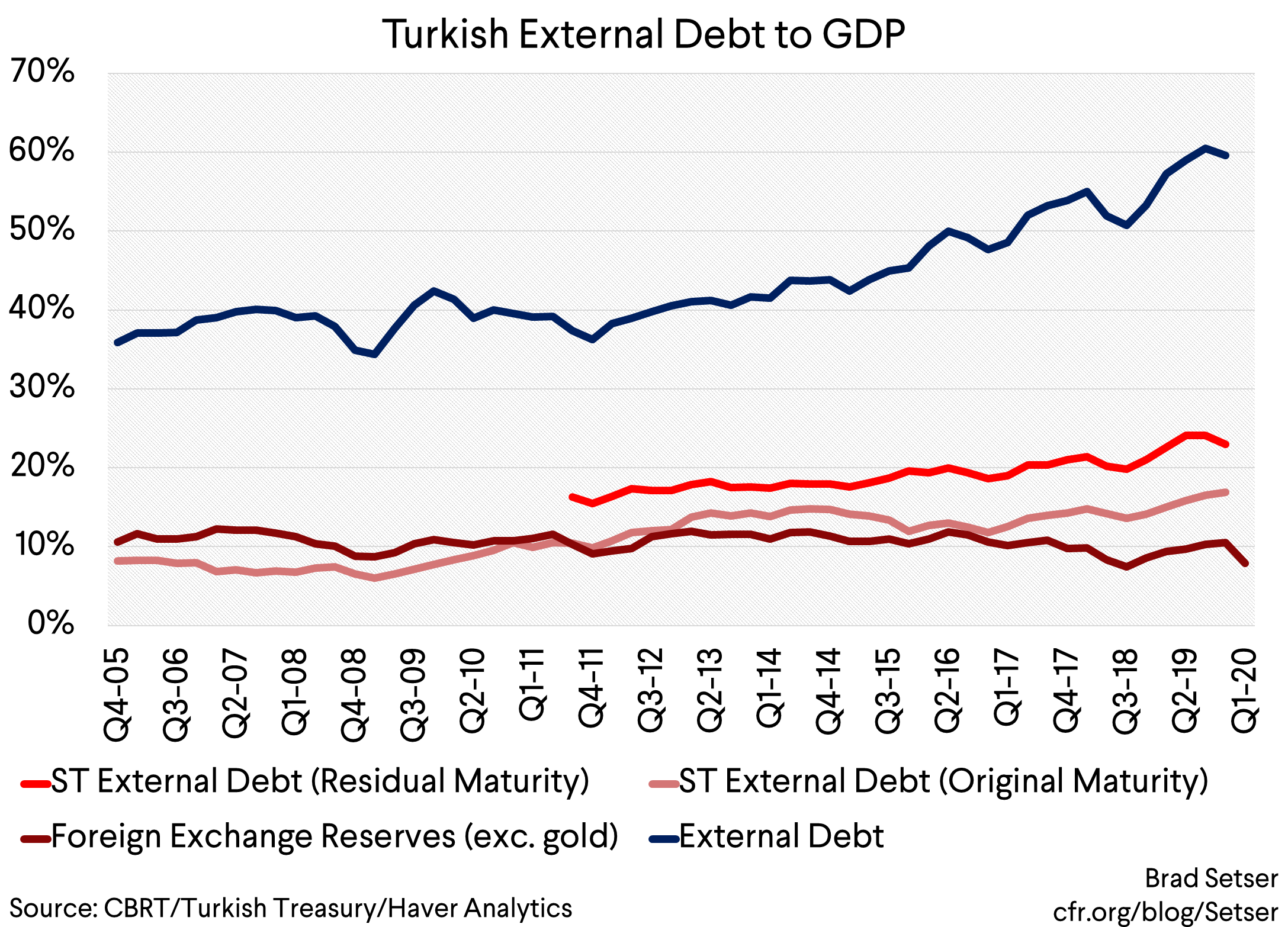

The banks are thus a big reason why Turkey has a lot more foreign currency denominated external debt than it has reserves. And, best I can tell, the banks also have more short-term external debt coming due over the next year than they have liquid foreign currency assets (counting the foreign currency that the banks have on deposit at the central bank, but excluding their Turkish eurobonds).

The magic that makes Turkey’s financial system work has long been the foreign currency swap market.

The availability of swaps basically explains why the banks borrowed foreign currency abroad that they didn’t appear to need to cover their domestic foreign currency lending (The financial stability report put out by the central bank is actually pretty good on this topic).

Turkey’s banks have long had difficulty getting long-term deposits from domestic depositor residents. But by borrowing foreign currency for longer tenors abroad and swapping it into lira, the banks created (synthetic) long-term lira financing to help match their longer-term lira lending. And the CBRT also helped the banks lend more in lira when it allowed the banks to meet a portion of their Turkish lira reserve requirement by holding foreign currency at the central bank. More lira lending raised the banks profits back when times were good. And the reserve option mechanism helped the central bank out too, as the foreign exchange the banks put on deposit at the CBRT counted toward Turkey’s reported foreign exchange reserves.

Turkey’s banks are thus simultaneously a source of short-term strength for Turkey, as they are still in a position where they can lend some of their excess domestic foreign currency deposits to the central bank to help the central bank out, and a medium term vulnerability—as the banks will eventually need some of their surplus foreign currency to pay back their external creditors.

All this matters now, as the CBRT has been intervening (selling dollars through the state banks) very heavily in the foreign exchange market. See Reuters, among others.

“This (state bank action) is the most important factor preventing the rise in dollar/lira, but question marks regarding its sustainability have created fresh selling pressure on the lira in the last few days,” said a forex trader who requested anonymity. The trader estimated that some $13 billion was sold in each of February and March.“

And it is increasingly intervening with foreign exchange borrowed from the banks.

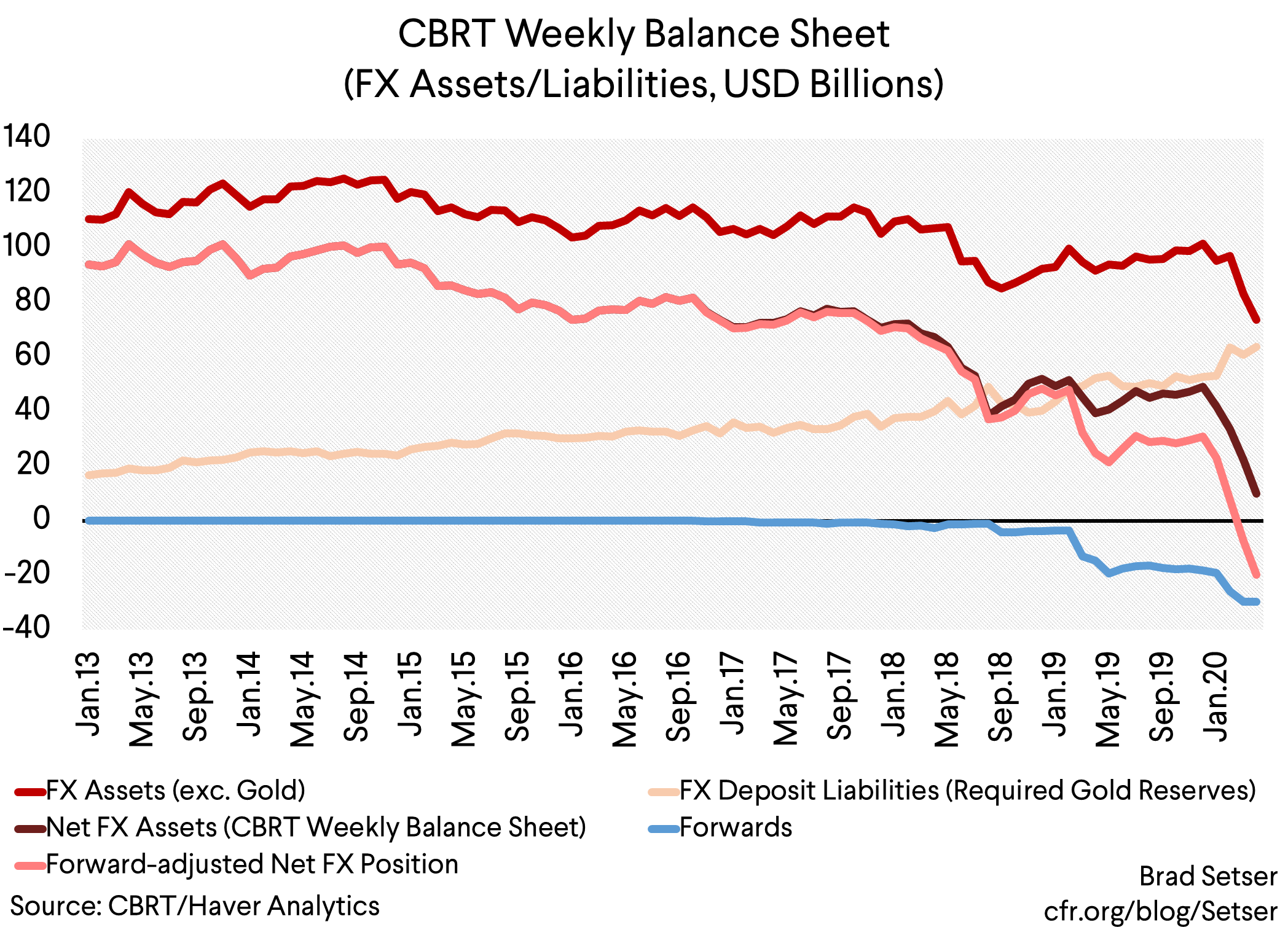

We know this because the central bank reports its net reserves, and those have been falling.

And we know this because the central bank reports its “swaps” position—swaps in this case are the mechanism through which the banks get lira from the central bank and the central bank gets foreign exchange from the banks. Those swaps boost the central bank’s reported reserves, but they don’t have to enter into the accounting as borrowed reserves (see this BIS paper).

Those swaps reached just under $30 billion at the end of March. And that in turn implies that all of the central bank’s reported net reserves at the end of March are in effect borrowed reserves, as the swap are an off balance sheet form of borrowing. And the central bank has continued to sell —and in all probability, has only increased the amount it borrows from the banks via the swaps.

The central bank unleashed a wave of regulatory changes that more or less forces the banks to provide more foreign currency to the central bank in April. Swaps with offshore counter-parties have more or less been prohibited (they are now limited to 1 percent of the bank’s capital base). And the regulatory limit on the banks‘ swaps with the central bank was just increased.

What’s the risk here?

Well, Turkey’s banks should still be liquid in foreign currency as they have way more foreign currency deposits than they have domestic foreign currency loans (a lot of those loans are bad, but that’s another story*). Some of that excess foreign currency funding has been invested in Turkey’s foreign currency denominated bonds, but a lot should be in liquid foreign exchange deposits—both abroad and at the central bank.

But, well, if the banks have put foreign exchange on deposit at the CBRT and the CBRT has sold the foreign exchange into the market, well, then the foreign exchange isn’t really there—the banks‘ foreign currency exposure to the CBRT thus starts to become a risk.

And that risk will become more acute if, as is likely, the syndicated bank loans that are coming due over the next few months aren’t rolled over—or at least aren’t rolled over at a high rate, and the banking system’s remaining liquid foreign exchange buffer is drawn down.

Right now, the banks and the central bank are basically sharing the same pool of reserves—so the loss of reserves by either banks (as external loans roll-off) or the central bank (through ongoing foreign exchange sales) hurts both. The CBRT’s FX sales thus pose an increasing risk to the banking system. That is what the balance sheet inter-linkages tell us.**

The broader issue though is that President Erdogan wanted an expansion of credit in Turkey to boost the economy. And he wanted lower rates. He certainly has gotten the increase in lending—the CBRT’s financial stability report last fall sent some rather unambiguous signals that the private banks needed to keep pace with the state banks, and those signals have been reinforced by regulatory changes that encouraged lending no matter the risk.

But increased lending in lira at relatively low rates relative to inflation is a policy mix that was consistent with a weaker lira even before the coronavirus shock.

Erdogan though hasn’t been willing to accept the consequences of his domestic policy preferences in the foreign exchange market.

In the process, Turkey has become a growing global financial risk. Neither the CBRT nor the banking system is yet out of foreign exchange. But Turkey will eventually run out on its current trajectory.

* The banks have a lot of foreign currency exposure to Turkey’s energy companies. That large exposure now looks a bit better, as the energy companies may be able to capture some of benefits from lower natural gas prices (they were hurt by a gap between their market inputs and their regulated prices, though now they will be hurt by lower demand). The banks have a lot of foreign currency exposure to the mega-projects, including the new Istanbul airport. The government though should stand behind those loans. The banks though also have a lot of direct exposure to Turkey’s construction companies. Rumor has it that the regulators have allowed a lot of rescheduling and forbearance to keep those loans from going bad, even if the banks did have to provision a bit more at end of last year. And I worry that loans to hotels may start to go bad as well, as Turkey is facing a brutal fall in tourism.

** See this IMF paper, which I think has stood the test of time. I am a bit biased though. It was an early attempt by the Fund to operationalize some of the insights in “The Volatility Machine.”