Chasing Shadows in China’s Balance of Payments Data

China’s second quarter balance of payments data points to a significant increase in the foreign asset accumulation of the state banking system. That at least raises the question of whether China’s authorities are resisting pressure on the yuan to appreciate.

For better or for worse, I have been trying to track the evolution of the foreign currency balance sheet of China’s state banks for a very long time.

Remember the use of foreign currency reserves to recapitalize China’s state commercial banks back in 2003 and 2005? I have a view on how that appears in China’s balance of payments data and why. I even suspect that—at least for the Bank of China—it was actually a more modest change than it seemed, as the Bank of China was likely already managing a portion of China’s reserve before 2003.*

Remember the surge in private bond purchases from China back in 2005 and 2006? I have a view on that too—as those purchases rather clearly were financed by swaps from the People’s Bank of China (PBOC). Those swaps and the resulting rise in private capital outflows from China fooled many (the IMF at the time wrote about how balanced private capital flows in Asia were that year).

Remember the rise in the banks’ holding of dollar reserves against their yuan deposits back in 2007 and 2008, which showed up on the PBOC’s balance sheet as “other foreign assets”? I do. Most central banks count dollar deposits from their own banks as part of their reserves (ask the Central Bank of the Republic of Turkey). But China at the time didn’t want to disclose how rapidly its foreign assets were rising, so when it asked the banks to hold dollar reserves as part of their required reserves, which were large at the time, they didn’t count those dollars as part of the PBOC’s reserves (I still don’t know if the funds put on deposit were managed by the banks, or by SAFE).**

Remember the foreign exchange shifted over to China’s rather neglected sovereign wealth fund, the China Investment Corporation (CIC)? I have a view on the timing of that transfer, and how it impacted China’s balance of payments data. The CIC, incidentally, also took over the equity stake that the PBOC acquired in the state banks in exchange for the injection of its foreign exchange reserves in 2003 and again in 2005 (re-read Red Capitalism for all the gory details).***

Everyone chases a great white whale—China’s reserves and the foreign assets of the state banks have long been mine.

Suffice to say that over time I have gained a great deal of respect for China’s ability to shift funds between the PBOC and the state banks. I think I have patched together much of the story, but I also know what I don’t know (for example, the precise mechanics of the recapitalization of the China Development Bank and the Exim Bank of China).

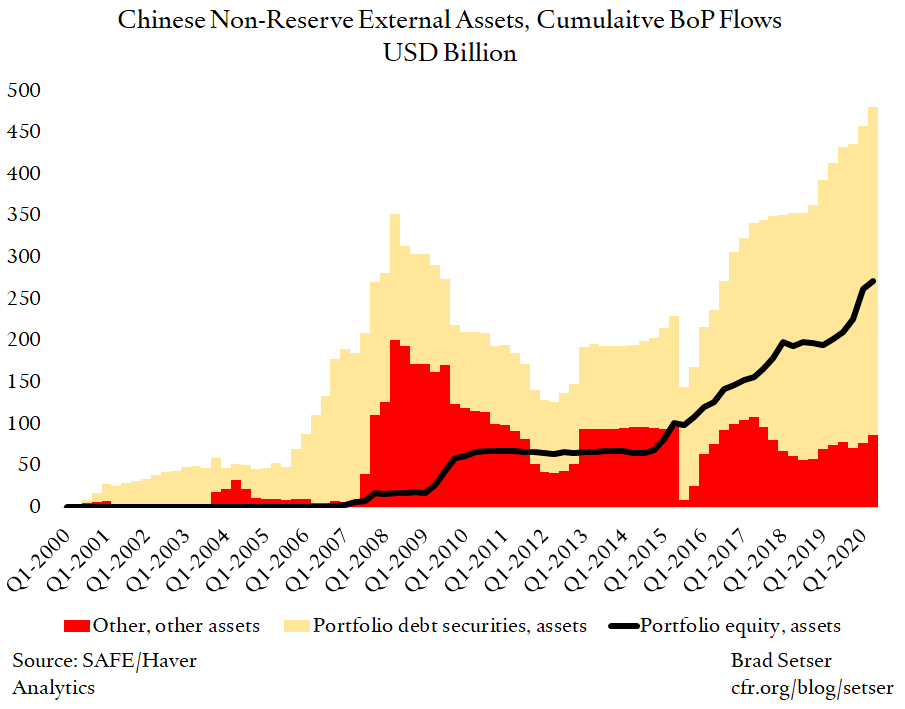

After all, China’s centrally-controlled state commercial banks—a grouping that reportedly includes the China Development Bank but not the Exim Bank of China, even though both are policy banks—have a disclosed foreign currency balance sheet of over $1 trillion dollars, with close to $750 billion disclosed external foreign currency assets. The China Development Bank and the Exim Bank of China combined aren’t just bigger than the World Bank; their external portfolio (over $500 billion) likely puts them in the top ranks of sovereign wealth funds by assets.

That is a long windup to be sure.

But I hope it gives me a bit of credibility when I say this: something significant shifted in China’s balance of payments in the second quarter of 2020.

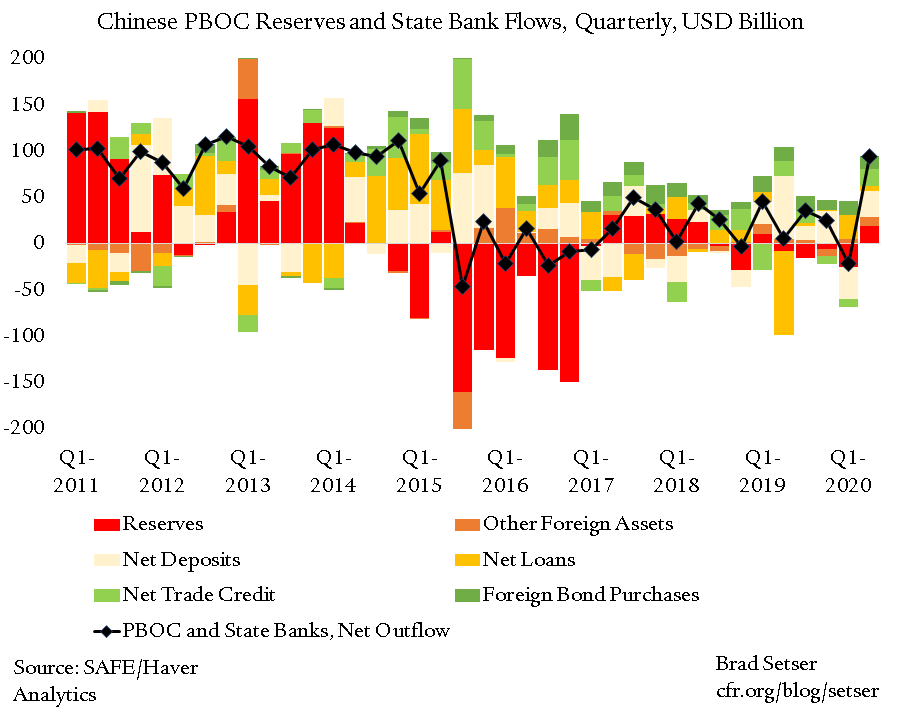

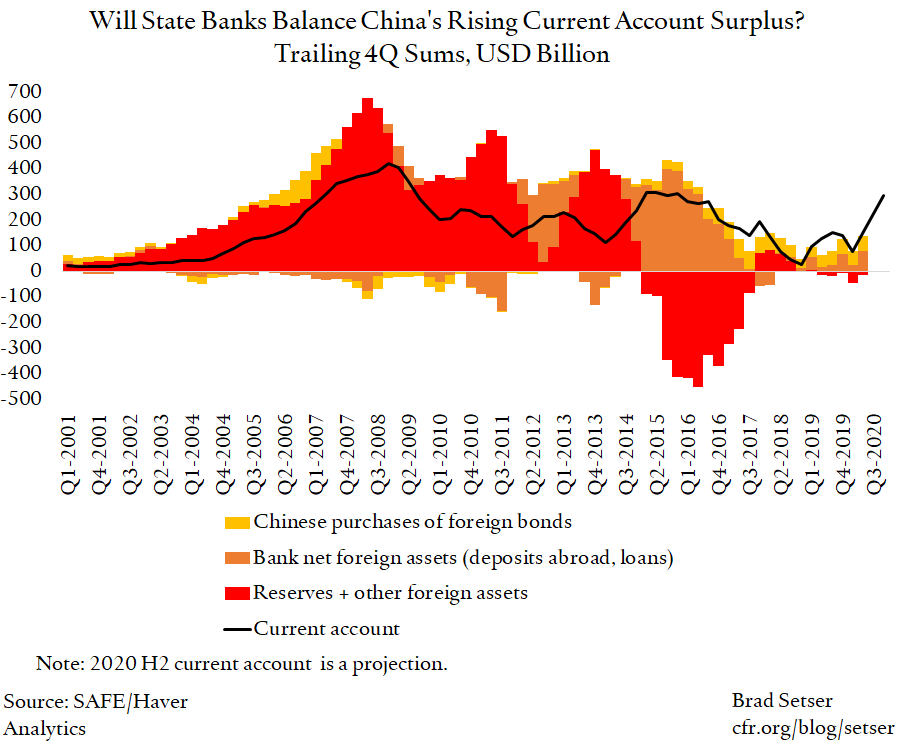

For most of the past five years, China’s government hasn’t added huge sums to its reserves, and there has been only a modest—by Chinese standards—rise in the net foreign assets of its state banks. Yes, there have been swings (I have long noted that part of the fall in the PBOC’s reserves in 2015 and 2016 is explained by the fact that the state banks paid down their external debts without reducing their external assets, so their net foreign asset position rose even as the PBOC’s reserves fell). Yes, there has been more underlying flow volatility than has showed up in the PBOC’s foreign exchange reserves. But there hasn’t been the kind of rapid accumulation of foreign reserves (including the required reserves left in the state banking system for the state banks to manage) that was typical from 2003 to 2013.

Until the second quarter: the pace of foreign asset accumulation of the state banking system increased dramatically.

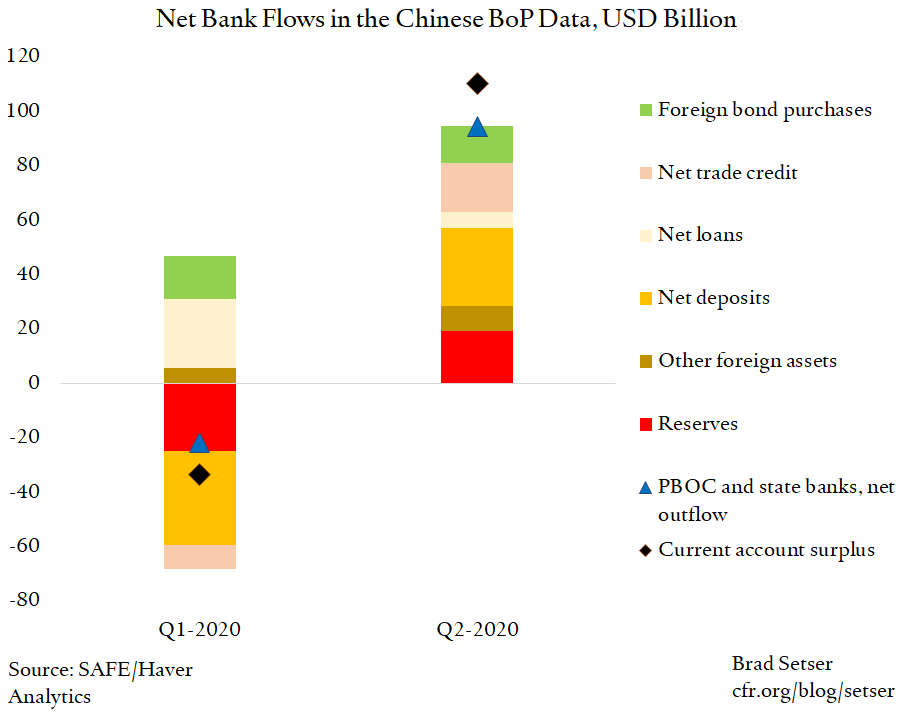

In the second quarter, for the first time, the net foreign asset accumulation of the PBOC and the state banking system looks to have returned to close to $100 billion—a sum roughly equal to the current account surplus. The PBOC added about $20 billion to its reserves (at least in the balance of payments data) and I would add the mysterious “other, other, assets” in the balance of payments data to that total. The net foreign asset position of the state banks increased by about another $50 billion (including trade credit) and the banks also account for the majority of the $14 billion or so in Chinese purchases of foreign bonds.

The scale of the state banks net foreign asset accumulation is significant. The banks did not borrow abroad to lend abroad; they moved a portion of China’s savings to global markets and thus they are responsible for a large share of the net buildup of Chinese assets abroad necessarily associated with a current account surplus.

There was no corresponding surge in domestic foreign currency deposits in the second quarter, so the sources of funding for this increase in the banks external portfolio aren’t entirely clear. Inquiring minds want to know.

Now there are lot of ways of splitting out the balance of payments.

I paired the flows through China’s state financial system with the current account, and thus implicitly netted other financial flows against each other.

But one could equally look at the full set of flows. Net FDI flows were modest in the second quarter, so the combined surplus on the current account and FDI was only around $115 billion. But China also received $65 billion in portfolio inflows, bringing inflows up to $180 billion. On the other side, China added $30 billion to its reserves and the banks added around $50 billion to their external assets and bought another $15 billion of bonds. On top of that, Chinese investors, mostly state investors, bought $10 billion of foreign equity and private Chinese investors moved another $75 billion out of China through ways that the government cannot fully explain. About half of the outflow that offsets the current account surplus and the portfolio inflows come from policy driven accounts—and half comes from other sources.

As a result, the signs of possible hidden intervention are still mostly whispers that speak most loudly only to those who have spent a long time with the data. They don’t (yet) shout out loudly from the headline numbers. But if current trends continue, I would expect that they will start to shout when the data for the full year becomes available—as the both the rising Chinese surplus and ongoing bond inflows will raise the size of the offsetting outflow to a level that is going to be hard to hide.

*/ Look under other, other assets, long-term in the old BPM 5 Chinese balance of payments

**/ Look under other, other, short-term (assets) in the BPM 5 balance of payments data. This is now consolidated in other, other assets with no short-term or long-term breakdown.

***/ Reported portfolio equity outflows in the Chinese balance of payments strongly suggest that the CIC didn’t convert all of the funds it raised back in 2007 and 2008 into foreign exchange prior to 2009, and its purchases of foreign exchange from the PBOC and SAFE in 2009 and 2010 held down reported reserve growth during the immediate post-crisis period (or they would have held down reported reserve growth, but for the fact that some of the other pools of hidden reserves built up before the global crisis were being scaled down).