Asian Intervention in the Foreign Exchange Market is Back. Bigly.

Joe Gagnon and Fred Bergsten have called the years from 2003 to 2013 the decade of manipulation, as a host of Asian countries protected their competitive position of their exporters by intervening massively in the foreign exchange market. Is a new decade of manipulation about to start, as Asian exporters once again try to keep their currencies from rising?

There is a sense, I think especially in foreign policy circles, that currency manipulation is yesterday’s issue.

That sense is largely driven by China.

China hasn’t been adding to its reserves for a while—and it used up a lot of them in 2015 and 2016 as the carry trade unwound and Chinese banks repaid their short-term debt. Plus, Trump made China’s ‘manipulation” a political issue at a time when there just wasn’t a strong case that China was a manipulator. Manipulation started to be viewed, I suspect, through a Trump-shaded lens. But the times they are a-changing.

With lower oil prices and China’s strong export rebound, the global current account surplus is once again located largely in Asia.

And a lot of Asian economies are intervening to keep their currencies from rising even as their trade surpluses are—at least in some cases—heading up.

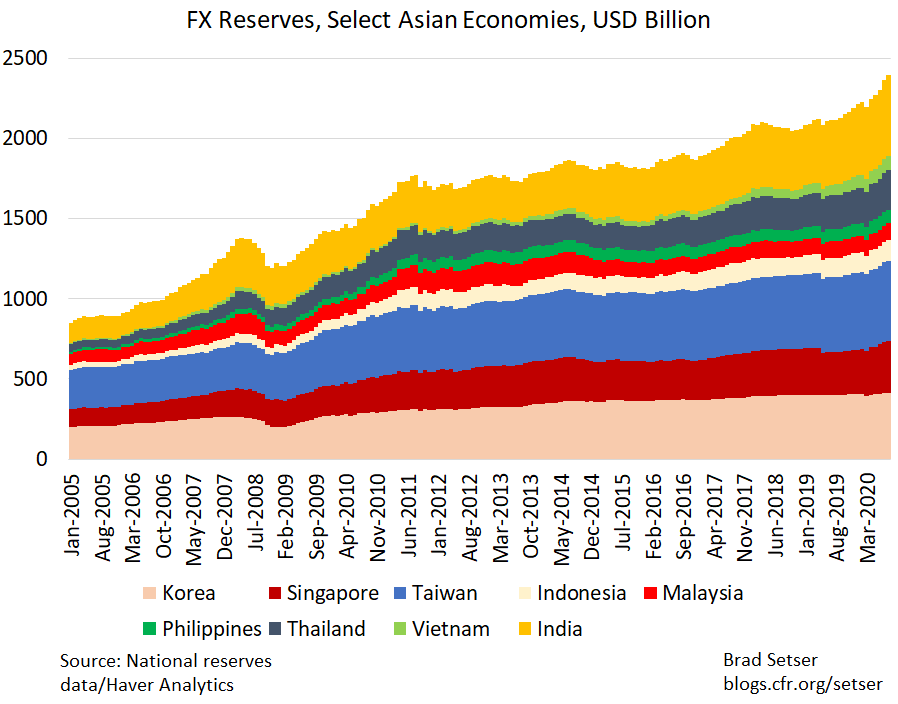

That is clear from a simple plot of Asia’s foreign currency reserves. There is, rather surprisingly, not much (if any) of a COVID-19 shock in the data—in part because Korea and Singapore used the Fed’s swap line to avoid dipping heavily into their reserves. And now those reserves are rising at a rapid clip.

A quick glance at the markets suggests that a number of countries are trying to keep their currencies from rising through key levels.

Thailand’s central bank, for example, has been trying to keep the baht from rising through 31 baht to the dollar.

The Reserve Bank of India didn’t want the rupee to rise much beyond 75 rupees to the dollar for most of the summer (it has allowed a bit of appreciation in September).

Vietnam has a peg —but one set at a level that keeps its currency weak and supports its exports. Reserves now top $90 billion, and are on their way to $100 billion (up from $80 billion at the end of last year). Nguyen Duc Thanh, the Director of the Vietnam Institute for Economic and Policy Research, said “the central bank’s purchase of foreign currencies helped prevent the strengthening of the Vietnamese đồng.”

Taiwan’s central bank has been doing its best to keep the Taiwan dollar from rising through 29 or so while also trying to avoid the attention of the U.S. Treasury, often by intervening late in the day.*

And Singapore, of course, continues to intervene as well. Nothing new there though.

These countries generally run significant current account surpluses (India is the exception) and thus can only keep their currencies from appreciating by adding to their reserves.

Or perhaps I should say by either adding to the reported reserve or their “shadow” reserves.

Even if Japan (with the Government Pension Investment Fund, which now has almost half of its assets abroad) and China (with a big state banking system as well as the China Investment Corporation) are set aside, all the big reserve holders in Asia have additional pools of government assets that are often used, at least in my view, to help achieve exchange rate goals.

Korea generates structural outflows through its National Pension Service and the Korea Investment Corporation. Singapore’s has revealed that its reported reserves are only a fraction of its true foreign assets—that is why reserves were sort of magically able to disappear from the Monetary Authority of Singapore’s balance sheet last year and then reappear this spring as needed (the funds were transferred out of Singapore’s large Government Investment Fund, which doesn’t disclose the size of its assets). And Taiwan’s central bank has revealed that it had a previously undisclosed $100 billion forward book and substantial foreign currency deposits with its local banks.

Add all this up and a substantial number of Asian countries with relatively large trade and current account surpluses are now adding to their disclosed—and in some cases hidden—reserves in order to keep their exports competitive at a time when many Asian economies are outperforming the global economy.

A number either currently meet or are on track to meet the U.S. Treasury’s quantitative thresholds for being named a currency manipulator (intervention of over 2 percent of GDP, a current account surplus of over 2 percent of GDP, and a bilateral surplus with the United States of over $20 billion).

Currency intervention, in other words, isn’t yesterday’s issue. It is today’s issue.

And there are some hints that intervention is more widespread than can be inferred from simply looking at reported reserves.

Taiwan for example has made no secret of the fact that it is resisting the appreciation of the Taiwan dollar—apparently that is a policy that has been decided from on high (“The strong Taiwan dollar has caused concern at the highest levels of government, and the central bank has been intervening to try and prevent it appreciating further”). But the August reserves data (including the forwards data that is now reported in a non-standard format) didn’t show much intervention despite widespread reports that the Central Bank of China (CBC) has been in the market. The CBC hasn’t been disclosing its foreign currency deposits with the local banks—so it could be stashing some foreign exchange there. And the CBC apparently has sought to limit the amount of dollars that can be sold for Taiwanese dollars in order to limit pressure on its reserves while it continues to resist appreciation.**

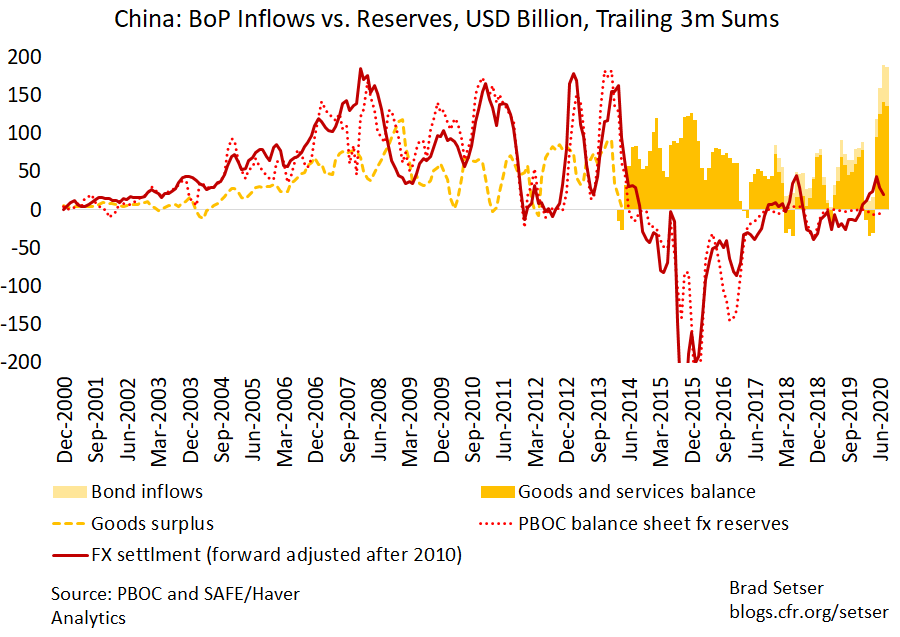

Yet while there are still-to-be resolved questions about the precise size of intervention in some smaller Asian economies, the really big mystery—as always—is China.

A lot of signs point to renewed pressure for the People’s Bank of China (PBOC) to intervene to control the pace of appreciation. China’s goods and services trade surplus has been running at around $50 billion a month ($600 billion a year). Opening its bond market to foreign investors at a time when the other major currencies don’t offer any yield has attracted substantial inflows—around $50 billion over the last 3 months ($200 billion annualized). The yuan is (finally) appreciating (a bit) against the dollar. Chinese investors move money out of China (on the down low) when the yuan is expected to slide, but at least in the past, they have also tended to want their savings at home when the yuan is moving up.

Yet reported reserves—especially reported reserves on the PBOC’s balance sheet—haven’t moved.

As a result, the balance of payments implies some actor or set of actors inside the Chinese economy have been adding to their foreign assets at quite a substantial clip.

If it turns out that asset accumulation is coming from state actors or actors that are borrowing foreign exchange domestically from the PBOC (Taiwan’s trick in the past for keeping the true foreign exchange position of its Central Banks in the shadows), well, currency intervention may become a real rather than a fake issue with China again too…

*/ The CBC’s obvious late-day intervention rather amuses me. A few years back the CBC claimed a blog post from an unnamed blogger of falsely accused them of putting their finger on the market in the last hour of trading… a fact widely recognized in the market.

**/ Are exporters being forced to hold dollar’s offshore by this policy? Inquiring minds want to know…