China’s Balance of Payments Data Does Not Add Up

China’s current balance of payments data doesn’t quite make sense. Significant and poorly explained gaps exist between the reported BoP data and the underlying source data. China’s economy is so big that data gaps really matter.

The IMF’s surveillance cycle for China is wrapping up, and at least judging from the press release, China’s balance of payments was not a focus of the conversation.

That is unfortunate.

I, of course, believe that the balance of payments is always central to understanding how any economy is interacting with the rest of the world economy, particularly for an economy whose visible trade surplus now approaches $1 trillion (a percent of world GDP).

But even setting that general point aside, there are a growing set of questions about China’s external data that are of fundamental importance to both China’s economy and the world economy.

Put simply, China’s external numbers just aren’t lining up. And they don’t really add up either. Often, the reported balance of payments is slightly at odds with the underlying source data.

Four discrepancies stand out.

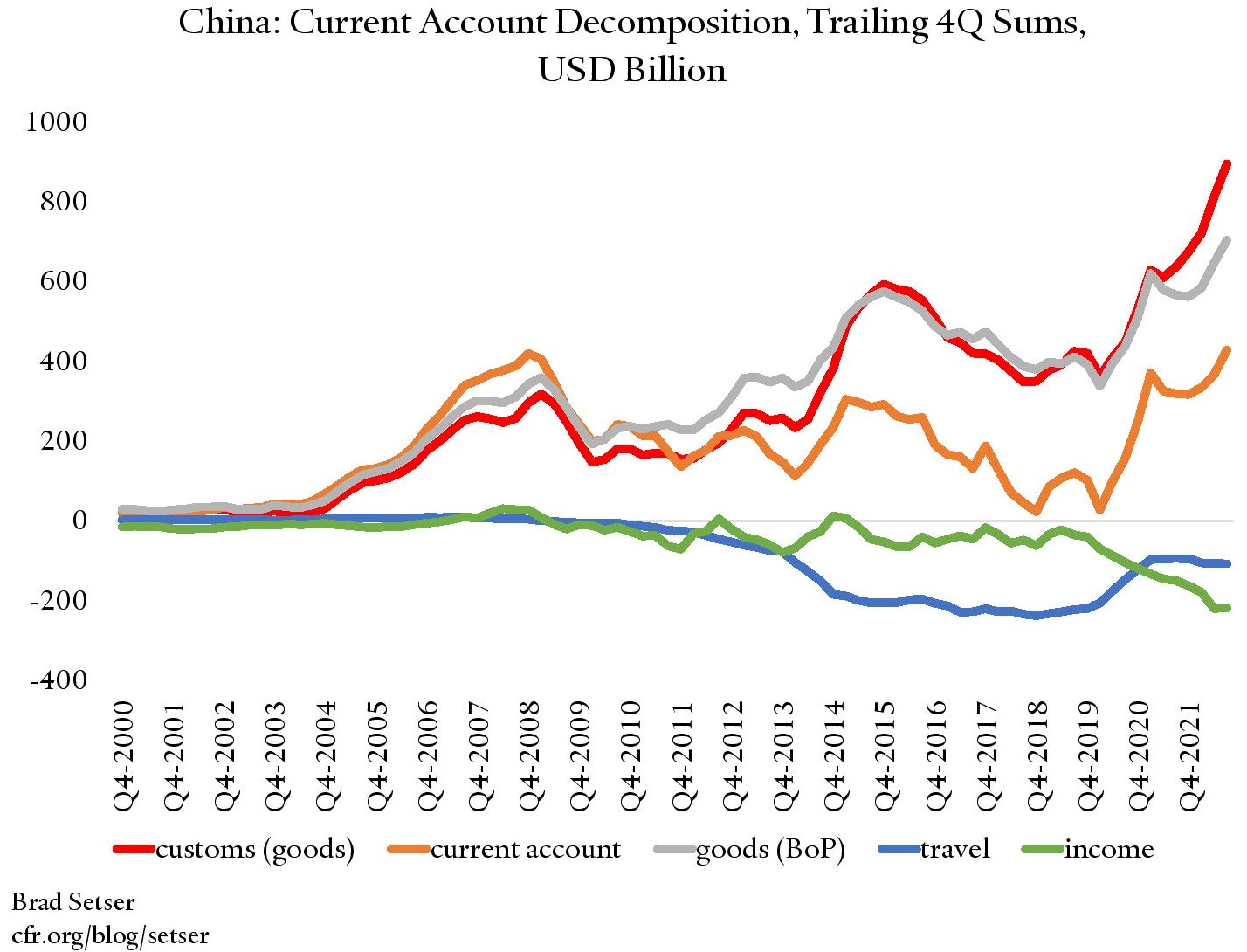

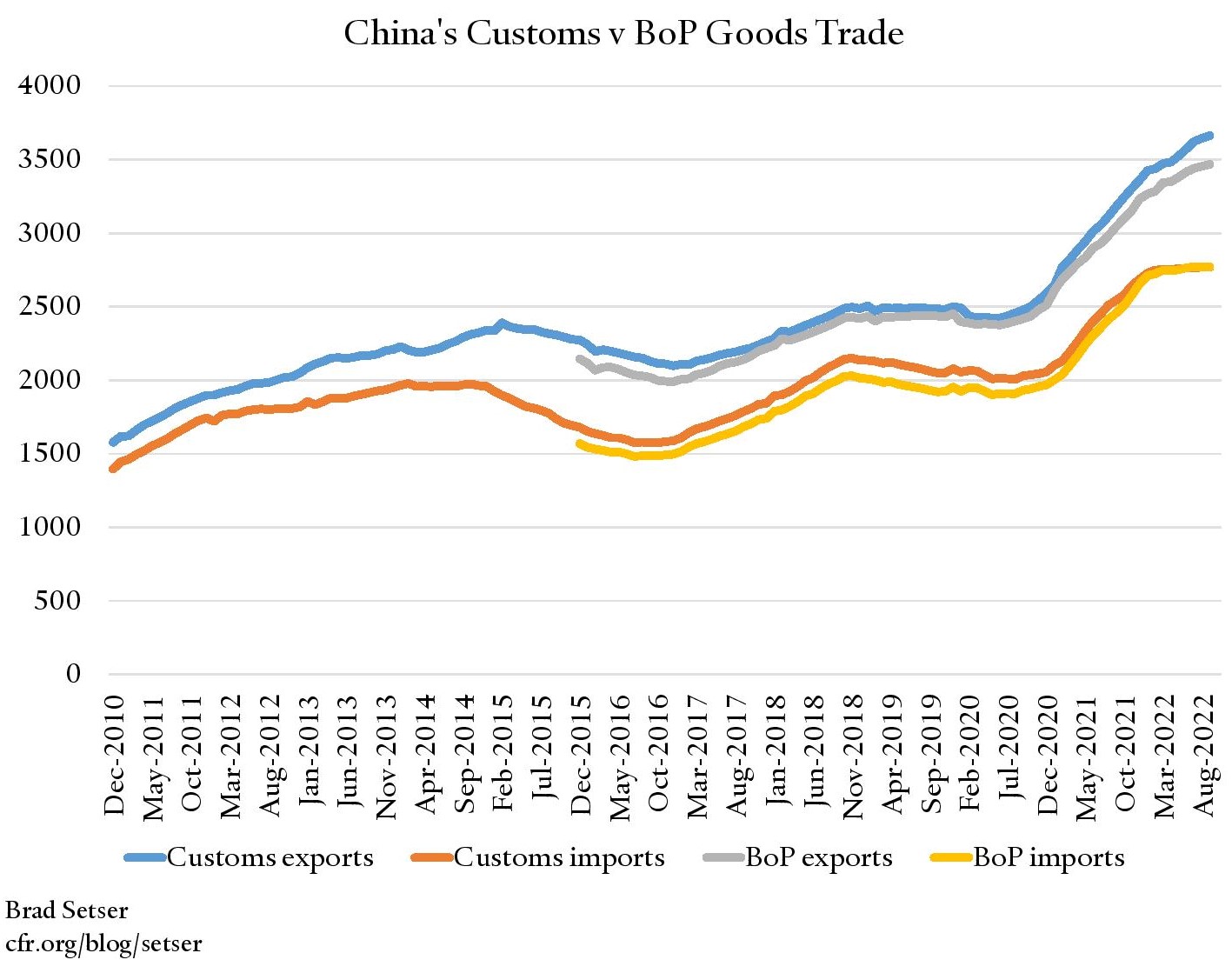

1. China’s reported goods trade surplus doesn’t line up with … China’s reported goods trade surplus.

There is a roughly $200 billion gap between the goods surplus China reports in the balance of payments and the goods surplus Chinese customs reports to the world. This amount accounts for over a percent of Chinese GDP.

Now, there are reasons why the balance of payments data can differ from the customs data. Notably, the charges on imported freight are included as goods imports in the customs data but moved over to the services data in balance of payments.

And so-called merchanting profits are included in the definition of trade in the balance of payments but not in the customs data. Basically, if a Chinese company has contracted for US liquefied natural gas (LNG) and sells that gas to a European company, it enters in the balance of payment data as a Chinese resident (the company, bought and sold the gas) but not into the customs trade data (the gas never entered a Chinese port). I learned about this after Apple became a balance of payments resident of Ireland back in 2014.*

But there is no obvious reason why these adjustments started to reduce China’s balance of payments trade surplus in a significant way only in 2020.

For example, it is hard to explain why China’s exports in the balance of payments data are now $200 billion below China’s reported exports in the customs data. Certain imports and exports into legally offshore customs zones are netted out of the balance of payments data. But this adjustment should be symmetric, and it didn’t obviously start during the pandemic. The “merchanting” adjustment, if anything, should increase China’s surplus, as Chinese state oil companies have bought U.S. LNG on long-term contracts and sold it to Europe at a nice markup. (For more, see Adam Wolfe’s comments on twitter)

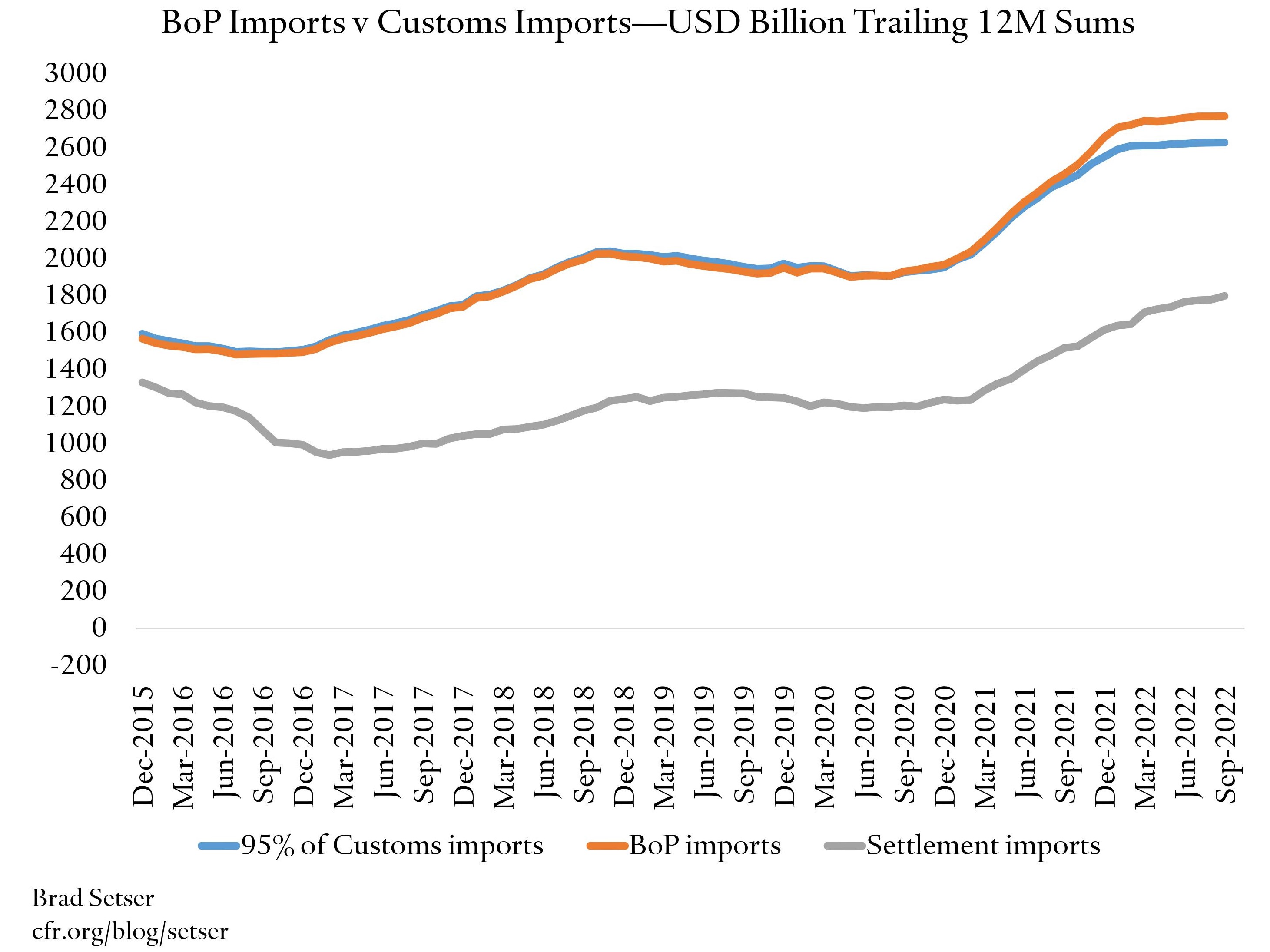

Equally, the convergence of reported goods imports in the balance of payments with goods imports in the customs data is a bit strange.

For a long time, China just mechanically cut measured imports by 5 percent to account for freight (this was spelled out in the fine print of China’s IMF data disclosure; see section 3.1.2), which probably wasn’t accurate but was at least consistent over time. Perhaps the shipping companies were so desperate to get containers back to China that they basically stopped charging for inbound freight? In any case, it is a bit strange.

Why should anyone care?

Well, one reason the surge in China’s external trade surplus hasn’t gotten the attention it deserves because it hasn’t translated over to the current account. As a share of China’s GDP, China’s current account surplus looks fairly stable.

More importantly, the difference between a balance of payments surplus of between 2 and 3 percent and a surplus of between 3 and 4 percent actually matters for a host of assessments of China’s economy. The size of the current account surplus (not the customs surplus) enters into the IMF’s assessment of the appropriate valuation of China’s currency. The reported current account surplus is also used by the U.S. Treasury in its assessment of exchange rate policies under the criteria set out in the 2015 Trade Enforcement Act. Both might need to reevaluate their choice of variables if questions about the quality of the reported current account data are not resolved.

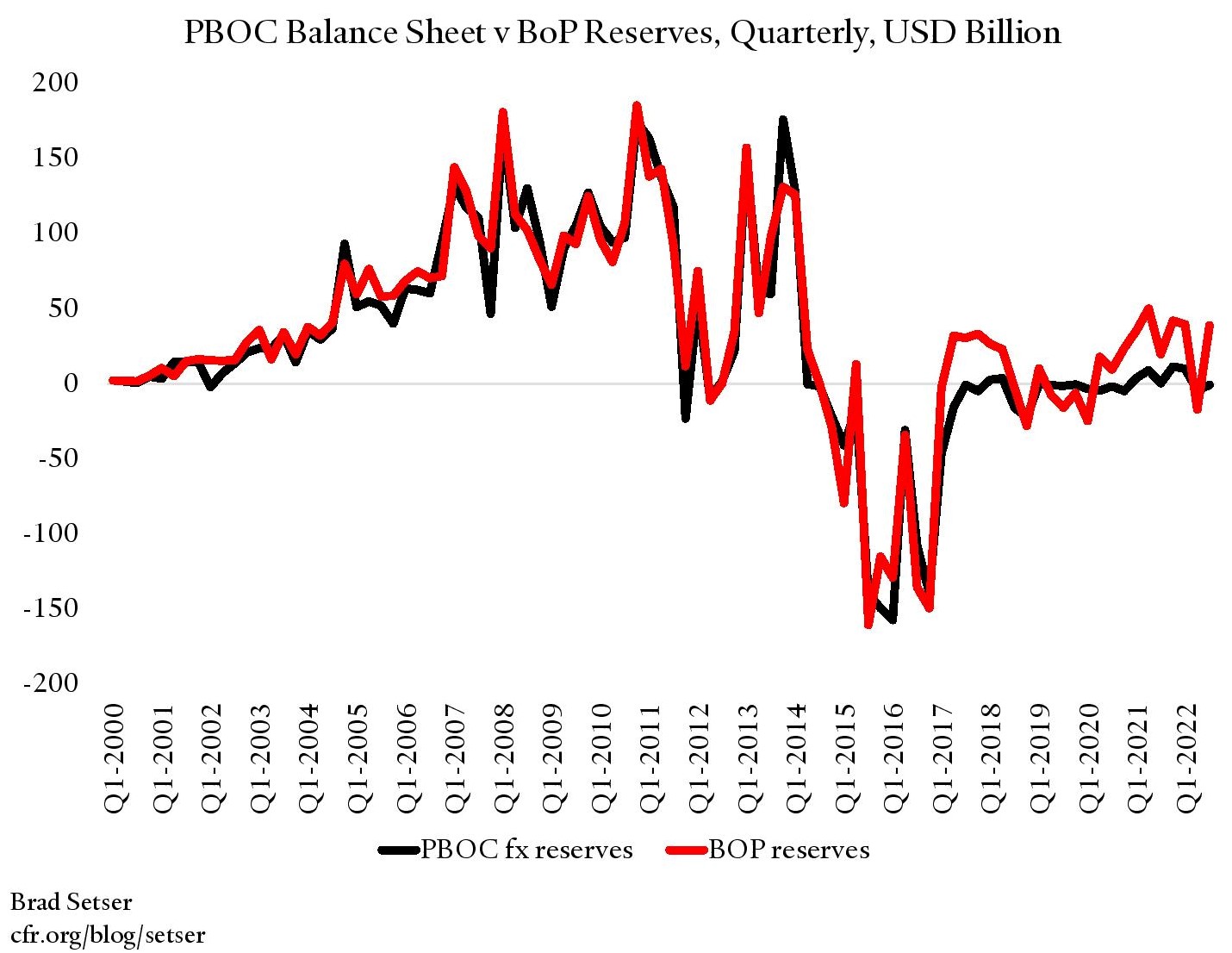

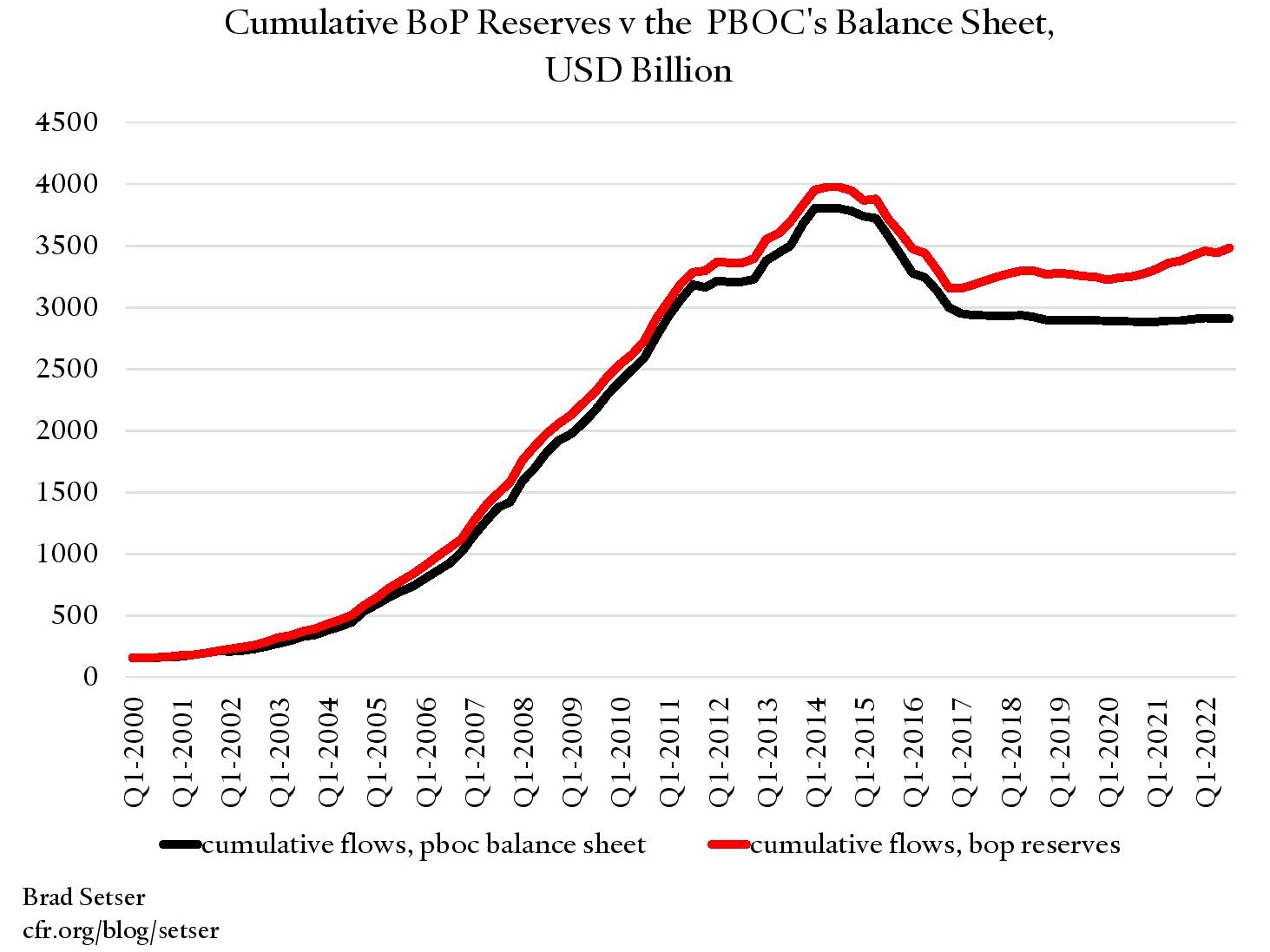

2. China’s foreign exchange reserve growth on the balance sheet of the People’s Bank of China (PBOC) doesn’t match China’s reported foreign exchange reserves in the balance of payments data.

Over the last five years, the reported foreign exchange reserves of China’s central bank (the PBOC) have not increased. The central bank reports its reserves are at their historical purchase price, and the sum of monthly changes since the start of 2018 is negative $20 billion (basically nothing).

On the other hand, the sum of changes in the balance of payments is positive, at around $200 billion.

And even setting aside the gap between the two measures, the recent stability in the foreign exchange on the PBOC’s reported balance sheet is also strange.

Are interest payments constantly repatriated so they don’t add to reserves? It doesn’t seem so, given that the PBOC supposedly made a large transfer to the budget this year.** Yet the buildup in interest income in the PBOC’s reported reserves prior to the transfer isn’t at all obvious.

The recent evolution of reserves in the balance of payments has been particularly confusing. The PBOC’s reported balance sheet has been remarkably stable this year—suggesting (cough) that China is the one country in Asia that has engaged in a relatively clean float and allowed the market to determine its exchange rate without any intervention. Yet in the balance of payments data, the PBOC added close to $40 billion to its foreign exchange reserves in the third quarter. That, at face value, implies that China’s central bank was buying dollars at a time when the yuan was depreciating and pretty much every other oil-importing emerging economy was selling reserves. It is, at a minimum, a bit strange.

This gap really should be clarified by the IMF among others. The cumulative gap between the flows implied by the balance of payments data and the flows implied by changes in the PBOC’s balance sheet is now larger than the reserves of most countries.

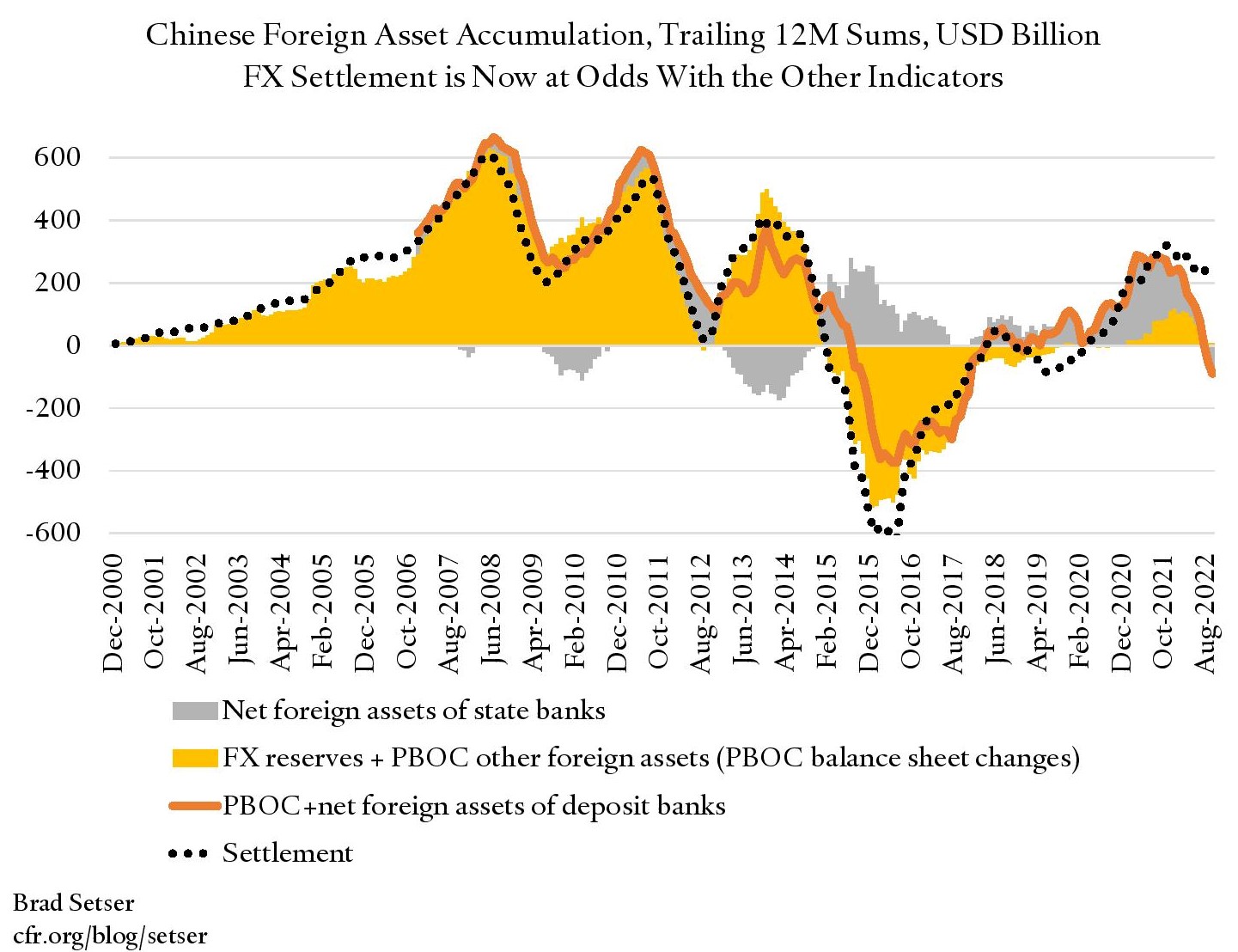

3. The foreign exchange settlement data doesn’t match the state banking data.

Foreign exchange settlement is one of those uniquely Chinese data sets—it reports the combined foreign exchange purchased by the state banks and the central bank. It dates back to the time when China’s capital account was really walled off, and exporters were expected to sell all of their foreign exchange earnings to the state.

For most of China’s post-WTO history, the bulk of the foreign exchange bought by Chinese financial institutions was bought by the central bank. In fact, gaps between the settlement data and the PBOC’s balance sheet generally stemmed from a policy decision by the PBOC to transfer foreign exchange over to the state banks.

More recently, it seems the banks started to account for the bulk of the foreign exchange bought or sold in the settlement data. The PBOC officially (see its balance sheet data) hasn’t been buying foreign exchange, yet the settlement balance still showed net purchases.

There is a bit of a puzzle there too, as the banks—intermediaries, fundamentally—shouldn’t really be net buyers of foreign exchange. That’s typically done by the central bank or institutions that naturally take foreign exchange risk. No matter—the data used to at least fit together. The buildup of foreign assets in the state banks basically matched the gap between the reported purchases in the settlement data and the PBOC’s balance sheet (after accounting for the foreign exchange held by the state banks at the PBOC as part of their reserve requirement, which isn’t consolidated into the PBOC’s reported reserves).

That correlation has now broken down—the “settlement” data shows ongoing … umm … purchases of foreign exchange in 2022: $116 billion YTD, with forward adjusted settlement up $73B.

The PBOC’s reported reserves are flat. The foreign exchange held at the PBOC as part of the banks required reserves is down -- total foreign assets held by the PBOC are down $25 billion. The foreign assets of the state banks are down $35 billion. The rise in settlement simply doesn’t line up with the numbers coming out for the PBOC and the state banks.

Now, it is possible that the old correlation was just a false correlation, but something is happening.

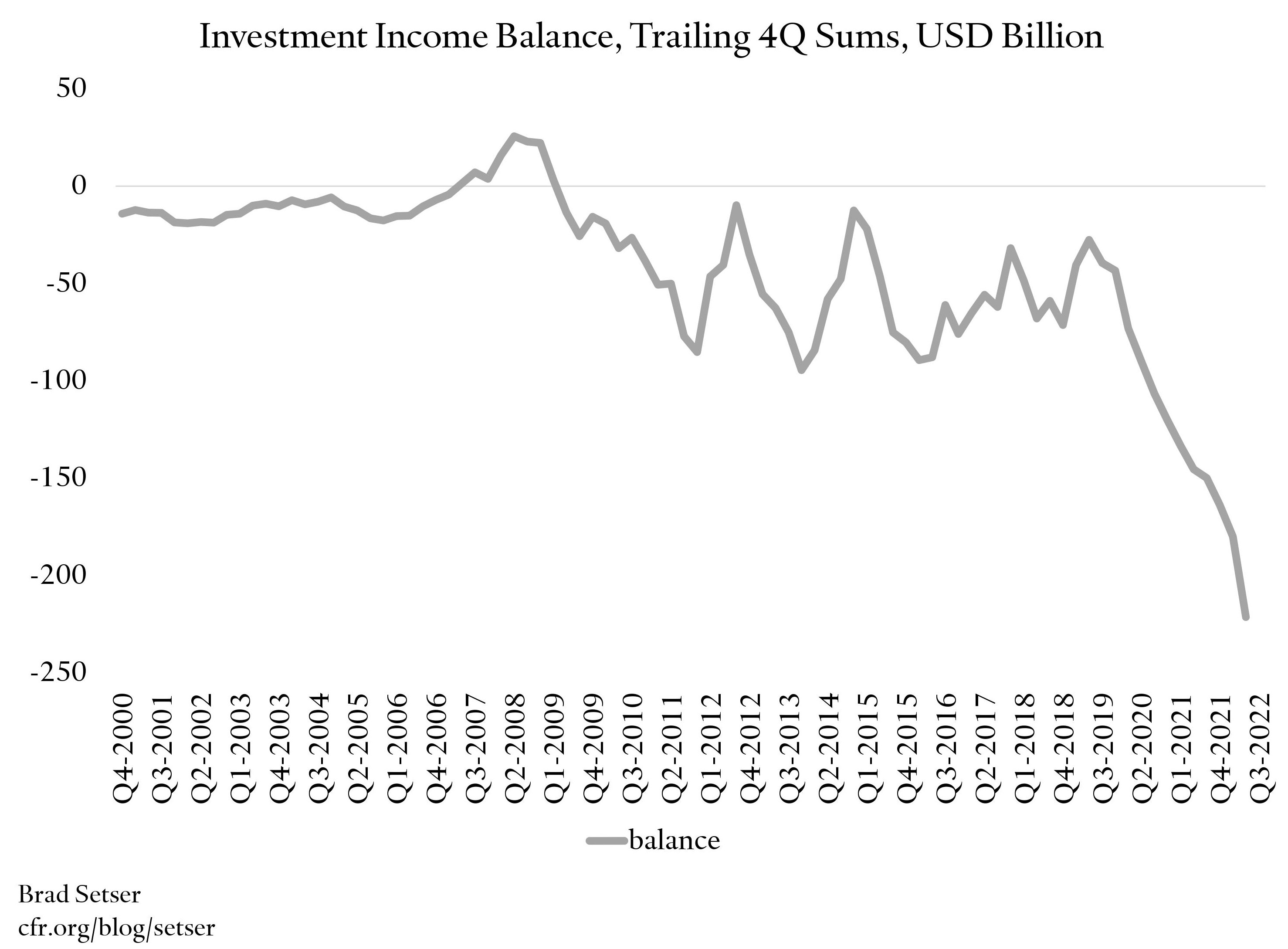

4. The income balance has been running contrary to changes in both global interest rates and developments in the Chinese economy.

After the COVID shock, China suddenly started running large deficits in its income balance. The income balance is the gap between the interest China pays on foreign holdings of its debt and the interest China receives on its lending/foreign exchange reserves together with the gap between the earnings of foreign equity investors in China and the earnings of Chinese firms abroad.

The size of the increase was a bit puzzling but it broadly made sense. Chinese interest rates were above U.S. interest rates in 2020 and 2021. Foreign investors were piling into China’s local bond market, so they naturally would be getting more interest payments. China’s relatively rapid recovery from the initial COVID shock supported the earnings of foreign firms operating in China. And Chinese firms that are nationally owned by foreign investors (whether in Hong Kong or the Caymans) started paying bigger dividends (reverse dark matter, so to speak).

But the rise in the income deficit in the second quarter of 2022 is much harder to explain.

Chinese interest rates fell below U.S. dollar interest rates, and foreign holdings of Chinese bonds were falling fast. China was locked down and its economy shrank—not an ideal environment for foreign firms to make large profits.

This could turn out to just be quarterly variation.

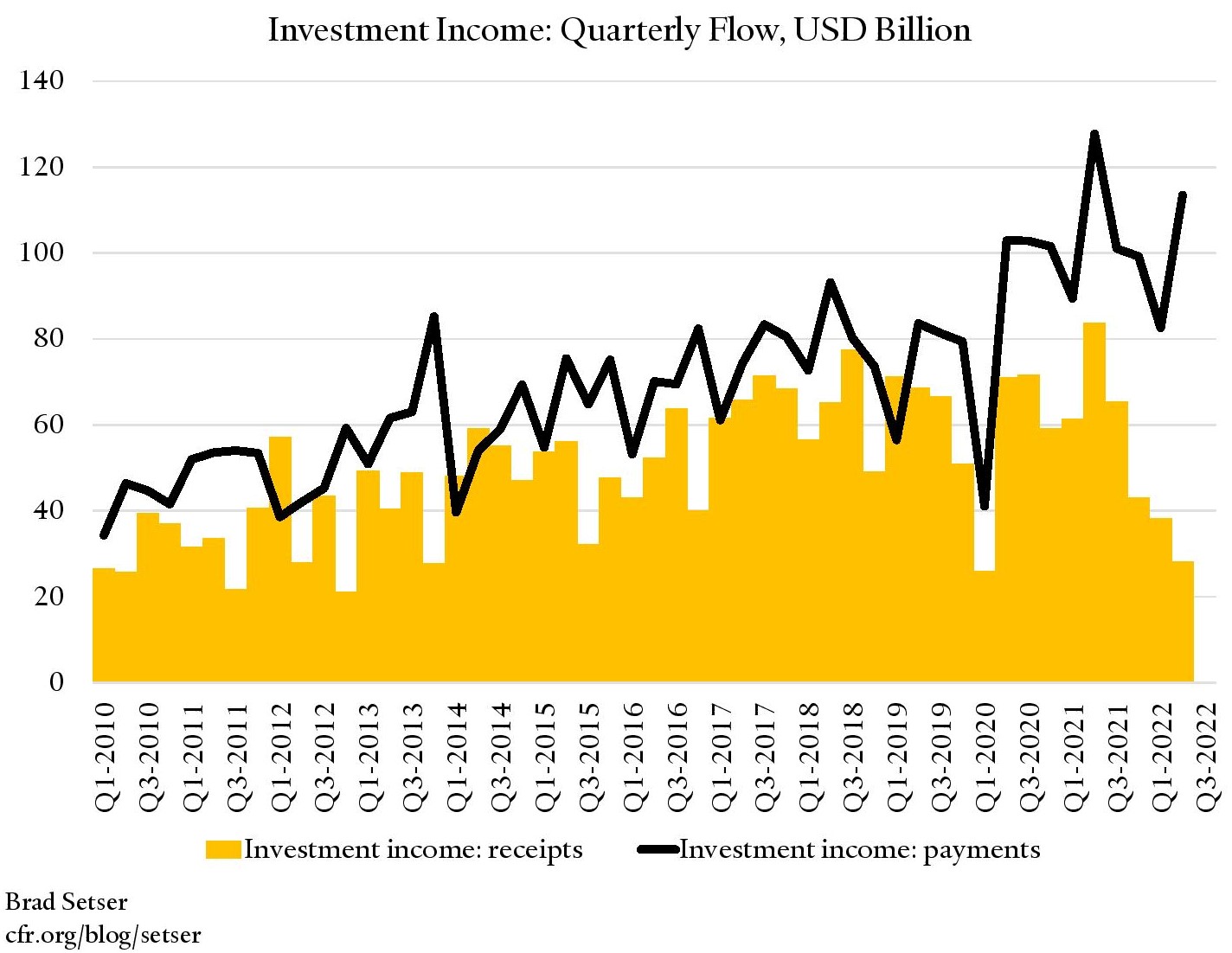

But it draws attention to a much bigger issue: China doesn’t release a detailed breakdown of its income balance, so it is impossible to trace the recent swing in the income balance back to the underlying payment flows. Why, for example, has China’s recorded receipts on its holdings of foreign assets (mostly bonds and loans) collapsed just as dollar interest rates started to rise?

This also matters for the IMF’s overall assessment of China’s economy—the income deficit and the goods discrepancy together account for the full $400 billion gap between China’s goods surplus and its balance of payments surplus. Tourism no longer is driving the gap.

---

There are a couple of other puzzles in the Chinese data that don’t directly affect measures of the current account balance or measures of China’s intervention in the foreign exchange market, but that are still of global interest.

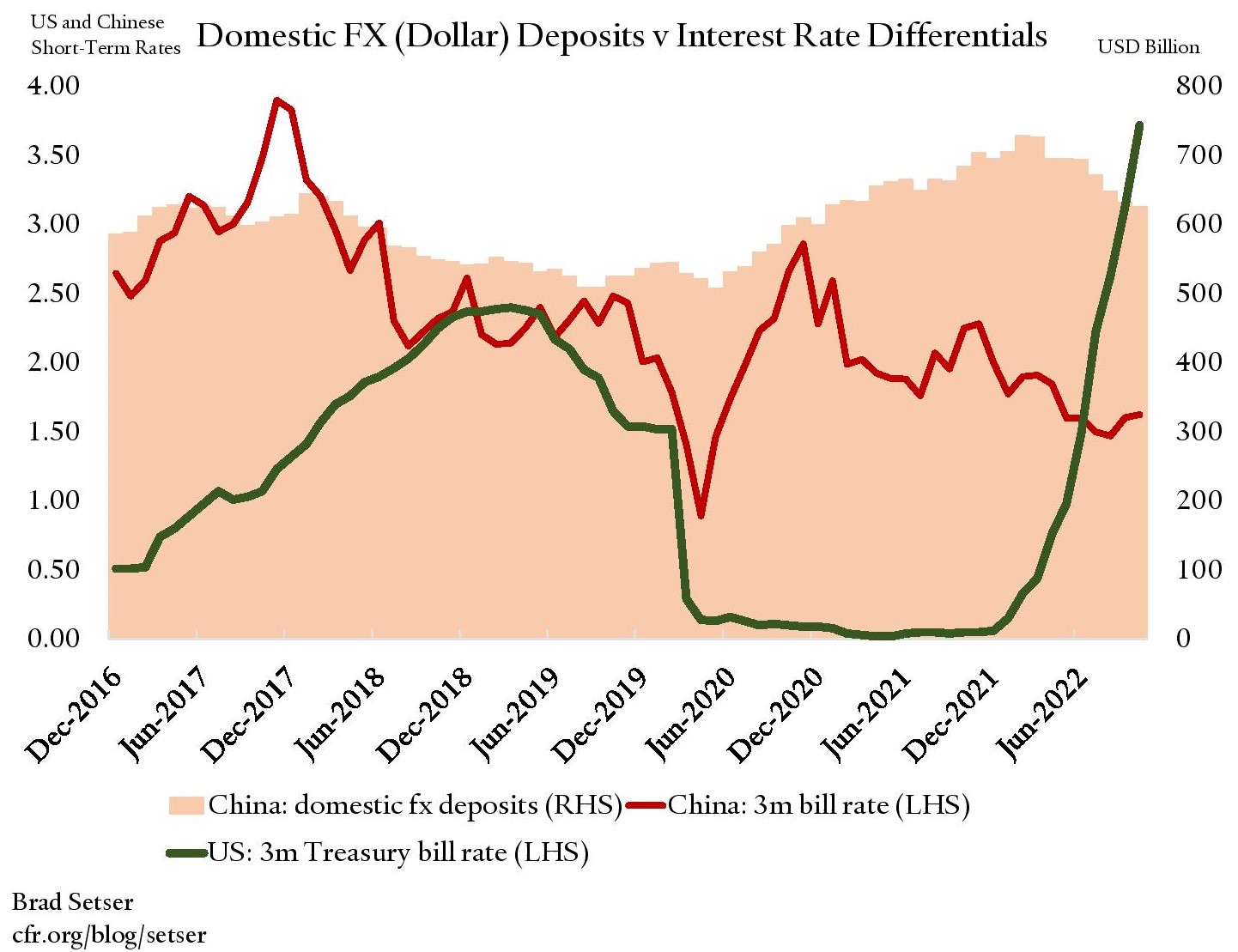

The first is the evolution of onshore foreign exchange deposits. They rose when Chinese interest rates were higher than US interest rates (hmmm) and now are falling when US interest rates are higher than Chinese policy rates (hmmm).

Those onshore deposits have been the main offset to the rise in the foreign assets of the state banking system—the growth in the foreign assets of the state banks was funded domestically. But the economics behind these flows is hard to understand.

The second is the data gap created by the limited disclosure of the foreign currency funding and aggregate foreign lending of the two big policy banks: the China Export-Import Bank (Chexim) and the China Development Bank (CDB).

Neither policy banks are funded by retail deposits—though both could take deposits from other government bodies, including the central bank—and thus neither should appear in the data for the state banking system. Still, both have external balance sheets roughly the size of the World Bank, so they matter globally.

The lack of more detailed data about their external assets and the structure of their, mostly domestic, foreign currency liabilities is shocking. The CDB’s reported foreign currency bond issuance is small relative to its foreign currency lending.

Both do seem to appear in balance of payments data, but that data is highly aggregated—it simply isn’t of the standard one would expect from the world’s second largest economy and one of the world’s biggest creditors.

And that highlights the basic issue with China’s external data right now.

Line items that should line up don’t.

The totals—both for the current account and the PBOC’s asset accumulation—don’t quite make sense relative to the underlying data.

The goods surplus disappears without a trace on the PBOC’s balance sheet even as—by nearly all accounts—the yuan remains heavily managed.

And the domestic foreign exchange funding sources for both the state commercial banks and the policy banks don’t quite make sense either, even though the balance of payments only works with their reported balance sheets if both the commercial banks and the policy banks have substantial sources of domestic foreign exchange funding …

One possible answer to some of these puzzles is that the State Administration of Foreign Exchange has minimized reported errors (outflows that don’t appear in the state banking data) in the balance of payments by making data adjustments that shrink the reported current account surplus.

The other obvious answer to some of these data puzzles is that the PBOC has worked with the commercial banks and policy banks to develop ways to manage the yuan without visibly managing the yuan.

I certainly plan to keep digging.

*Apple’s Irish subsidiary imports phones, notionally, from its subcontractors in a bonded zone in China before notionally re-exporting those phones at a higher price around the world (Apple Ireland has the rights to Apple’s design, software and branding outside of the Americas). The phones never really enter into Ireland and thus don’t enter into the Irish customs data. But the markup on these phones, of course, enters the balance of payments data, as Apple (Ireland) is enormously profitable. The reasons why Apple’s Irish subsidiary engages in theses transaction is of course a mystery, as no large American corporation operates out of Ireland primarily because of tax considerations …