China’s Rising Holdings of U.S. Agency Bonds

China has discovered, once again, that the best alternative to a U.S. Treasury bond is a U.S. Agency bond…

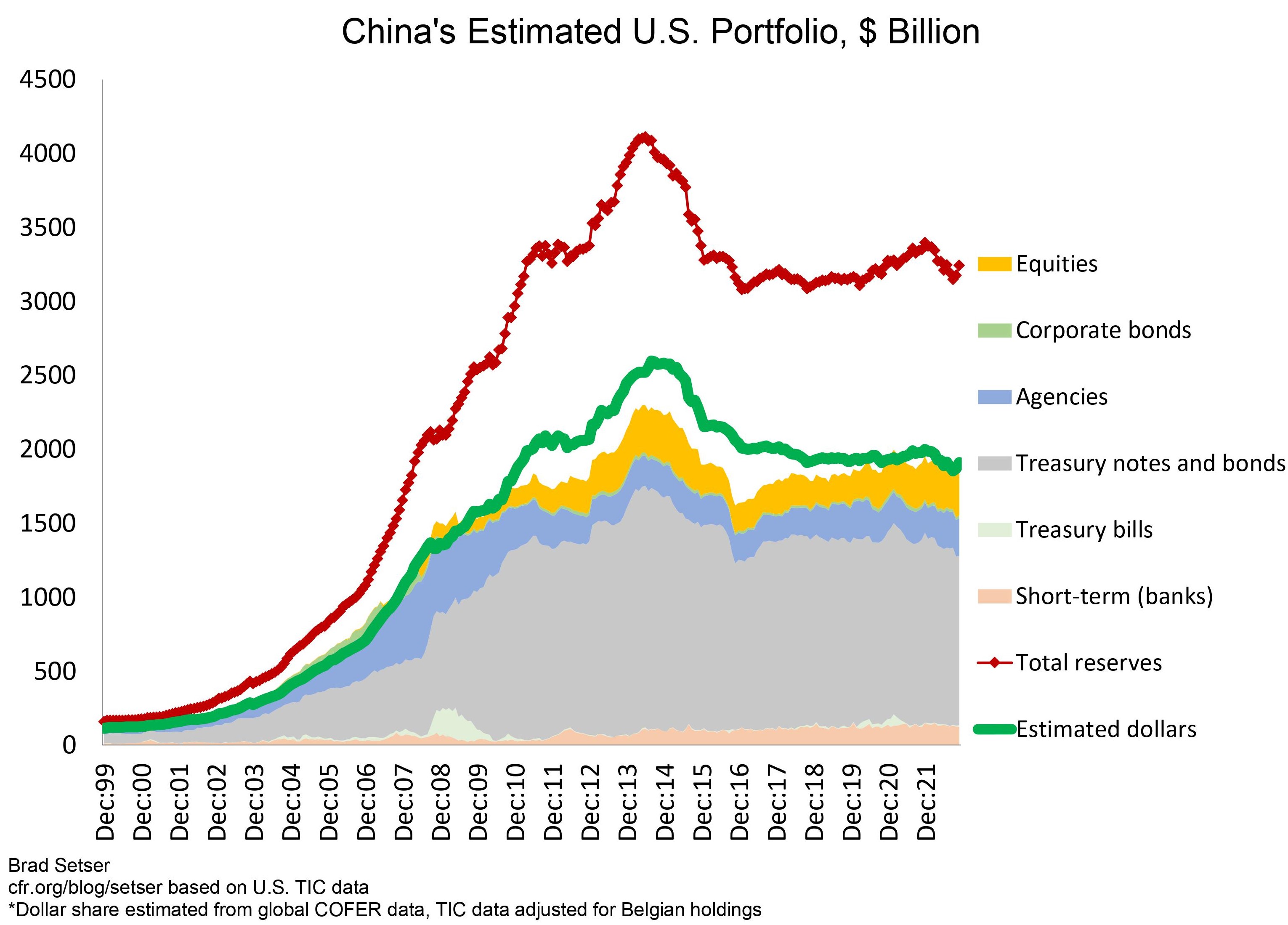

China’s holdings of Treasuries have attracted a fair amount of attention over the years.

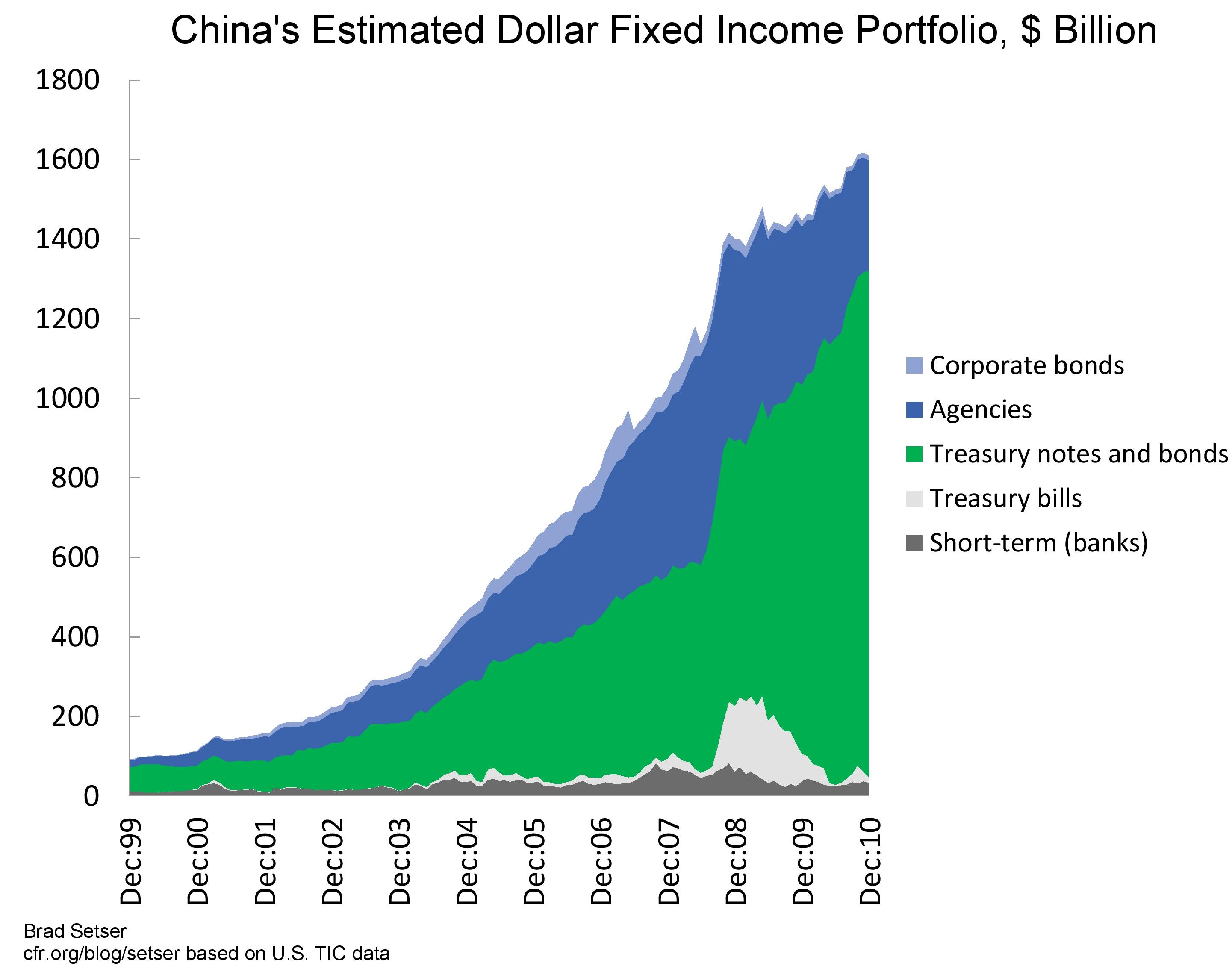

China’s holdings of Agencies—the bonds backed by Fannie Mae, Freddie Mac, and a few government agencies and government sponsored enterprises—much less so.

The U.S. Treasury doesn’t put out a table showing the “Major Foreign Holders“ of Agencies. China, no doubt, prefers that its Agency holdings remain under the radar. *

But the story of China’s Agency holdings is in some ways as important as the story of China’s Treasury holdings.

A bit of history:

In the years before the global financial crisis, global reserves were growing so fast that reserve managers could hardly find enough Treasuries to buy. The United States reduced its issuance of Treasuries from 2005 on, as the fiscal deficit fell to under 2 percent of GDP in 2006 and 2007. At the same time, global reserve accumulation was soaring, and central bank demand for dollar reserves eventually reached around 8 percent of U.S. GDP.

China’s reserve accumulation peaked at $600 billion a year (measured from the middle of 2007 to the middle of 2008), including funds that the state banks held as part of their required (prudential) reserves to reduce the reported foreign exchange reserves of the People’s Bank of China (PBOC). China has a long history of using the state banks to help the PBOC out.** China’s reserve managers thus could have absorbed all of the Treasury’s net issuance on its own.

Different central banks found different solutions to the challenges created by the world where the growth of Treasury supply lagged the growth in global reserves. Some put more funds on deposit in the global banking system. Others, led by the PBOC, bought a ton of Agencies.

I pointed this out in 2007 and 2008, which didn’t make me very popular in China. The composition of China’s reserves was treated as a state secret. For what it is worth, I relied on the data that the United States releases with a lag as part of the process of compiling its balance of payments data—and that data (presented in the annual survey of foreign portfolio investment in the United States) showed that China held just over $525 billion of Agencies at its peak in June 2008, a sum that narrowly topped its holdings of long-term Treasuries.***

These holdings played a role in the high diplomacy of the global financial crisis too. China famously told Treasury Secretary Paulson at the Beijing Olympics that they were worried about the safety of their investments in Agencies. Paulson’s accounts of the crisis make it clear that he was concerned that China would unload its Agencies and he spent considerable time on the phone personally reassuring China’s top financial leaders—something that seems hard to imagine now.

But diplomacy alone didn’t solve the core problem of the Agencies (or GSEs, effectively national housing policy banks). The U.S. Treasury ultimately had to inject a significant amount of capital into the Agencies in the fall of 2008, which helped assure their ability to weather the crisis.

However, this injection wasn’t enough to reassure the big central bank holders of Agencies. They didn’t want to take any risk and they either continued to sell their bonds or allowed their portfolio to run off very rapidly. The Federal Reserve had to step in and start buying Agencies and Agency MBS to stabilize the market (“QE1”).

China’s initial foray into Agencies thus put Chinese creditors on the line in the early stages of the financial crisis and helped spur the introduction of a policy (“QE”) that China then criticized. I think that all the demand for safe assets back in 2006 and 2007 helped push the banks into manufacturing assets that could be marketed as safe even when they really were not, and thus contributed to the overall environment that led to the great North Atlantic financial panic of the fall of 2008.

China didn’t face much pressure to return to the Agency market in the years immediately after the financial crisis. Treasury issuance soared, and expanded supply helped accommodate increased demand for safe Treasuries from central banks that previously had dabbled in Agencies or bank deposits. To manage the optics of the massive size of its Treasury holdings, China worked to make its Treasury portfolio slightly less visible (for example, using a custodian in Belgium), rather than actually shifting out of Treasuries.

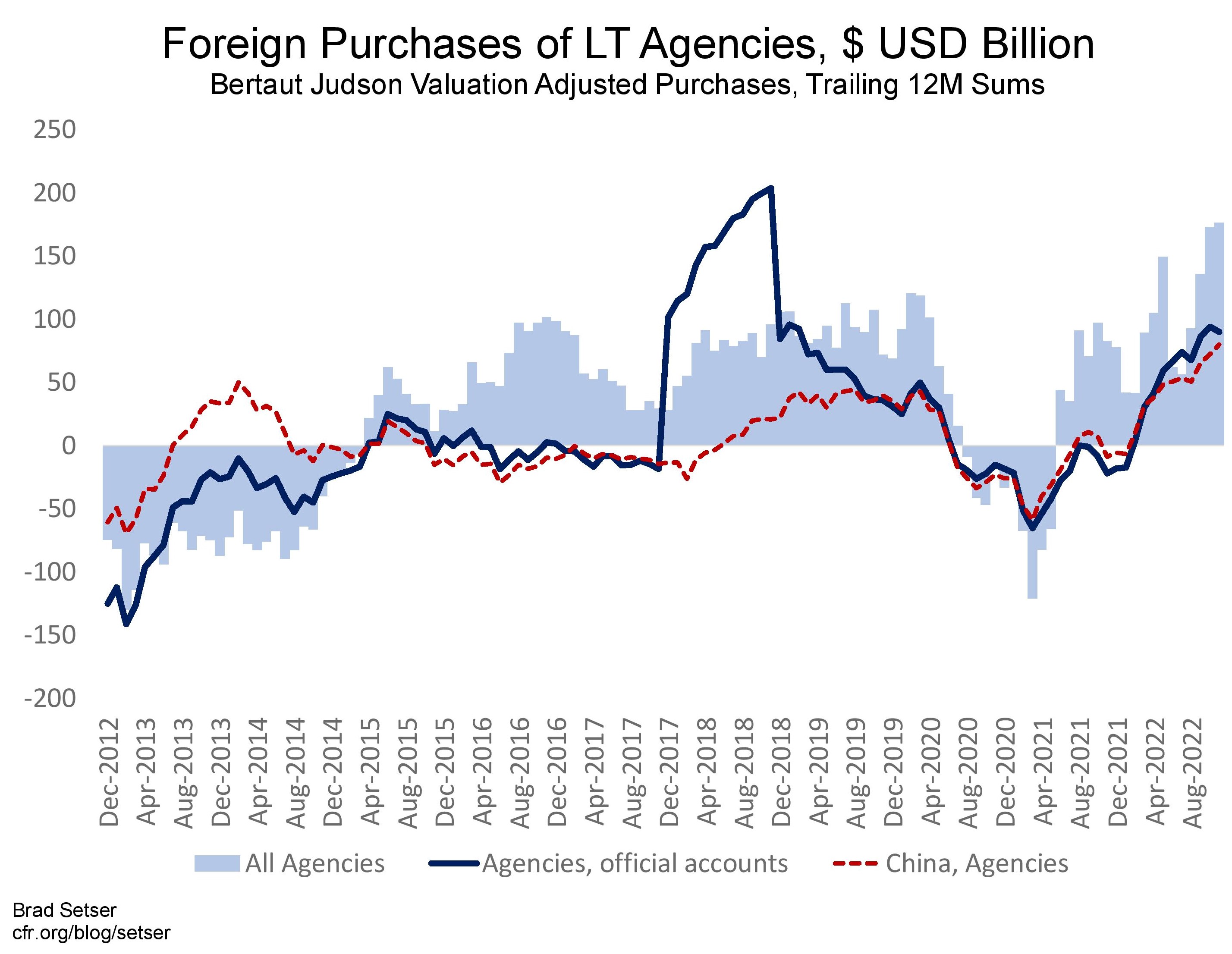

But something has changed in the past few years—this year in particular.

China is on track to buy around $75 billion of Agencies—likely accounting for nearly all central bank demand for Agencies and for about half of all foreign demand for Agencies.

It cannot be known based on the data disclosed by the Treasury (which aggregates private and official holdings) that the Chinese buyer is China’s reserve managers, but the fit in the chart between Chinese purchases and total official purchases is shockingly good. Plus, $75 billion is a bit big even for the Chinese state banks.

China now seems willing to take on a bit more risk to get a bit more yield than it gets on Treasuries. Agency MBS traded quite wide for a while, with a substantial yield pickup over Treasuries. And China never has minded when the true scale of its reserve holdings is obscured a bit.

In some deep sense, the relationship between China, the housing Agencies (U.S. policy banks, in effect), and the Federal Reserve has come full circle. In late 2008 and 2009, China sold Agencies and the Fed stepped in and bought them. Then in 2022, the Fed stopped buying Agencies and now is letting its portfolio run down—and China is buying many of them. A small irony of financial history.

The high coupon that China should be clipping on an Agency book that looks set to rise to over $300 billion soon raises another mystery: namely, how exactly does the PBOC account for the interest income on its foreign reserves?

The PBOC’s flat holdings of foreign exchange suggest the PBOC doesn’t actually keep and reinvest any of its interest income on foreign bonds … which doesn’t seem quite right.

China guards its secrets. There are large parts of China’s balance of payments that do not quite add up right now.

But the U.S. data makes one small point clear: looking only at China’s reported holdings of Treasuries misses a large and growing share of China’s dollar portfolio.

That was true before the global financial crisis, and it ended up mattering.

And it is again true now.

* The data for current holdings can be found here. The annual survey of custodians suggests that China has long held a lot of mortgage backed securities, not just the bonds that the Agencies used to issue to fund their retained portfolio. The size of China’s portfolio has historically been so big—particularly between 2006 and 2008 (See Table 21 in the 2007 report and Table 22 of the 2008 report)—that it is safe to assume that China’s central bank, the People’s Bank of China, and its reserve manager, the State Agency of Foreign Exchange, hold the bulk of the overall total. In June 2008 China held $369 billion of Agency MBS—a sum only slightly below total official holdings of MBS were $435 billion. The rise in Chinese holdings between 2004 and 2008 closely tracks the rise in total reported official holdings.

** See this article for the details of the reserves shifted to the state banks between 2005 and 2008.

*** June 2008 holdings were not reported until April of 2009. But this is a firm data point, as the Treasury survey of custodians at the time only reported mid-year holdings.