Thailand is Really, and I Mean Really, Close to Meeting the Treasury’s Manipulation Criteria

The Treasury’s April foreign exchange report should be interesting.

Thailand hasn’t been included in past foreign exchange reports. Yet it is likely to meet all three of the criteria set out in the Bennet Amendment for a finding of “manipulation.”

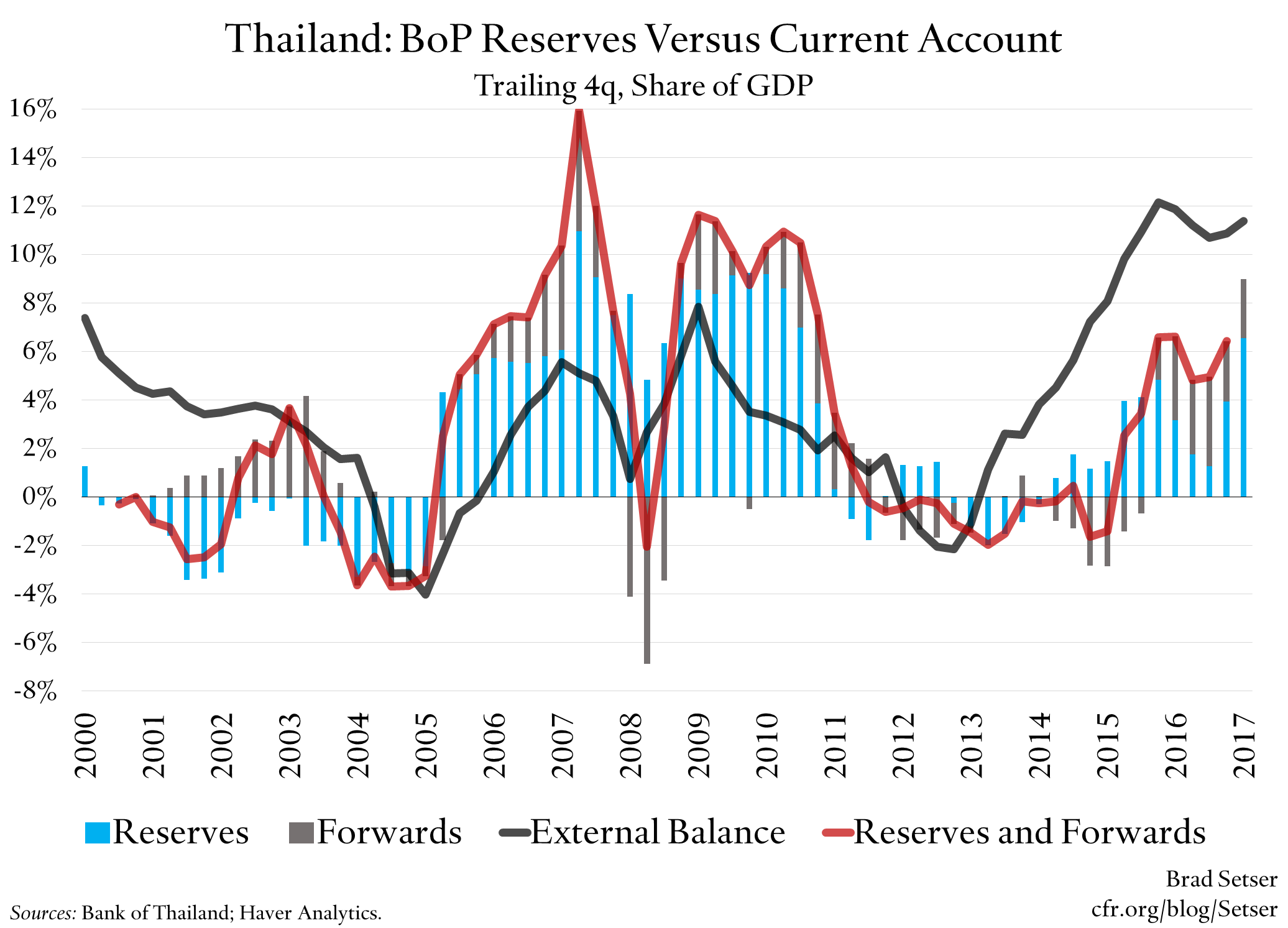

Thailand has long met the current account surplus and intervention criteria monitored in the Treasury’s semi-annual FX report.

Its current account surplus and its intervention both jumped in the third quarter of 2017, and little changed in the fourth quarter. The central bank’s forward book rose $5.5 billion in the fourth quarter, and the BoP data for the first two months of q4 shows a $4.4 billion increase in on-balance sheet reserve assets.

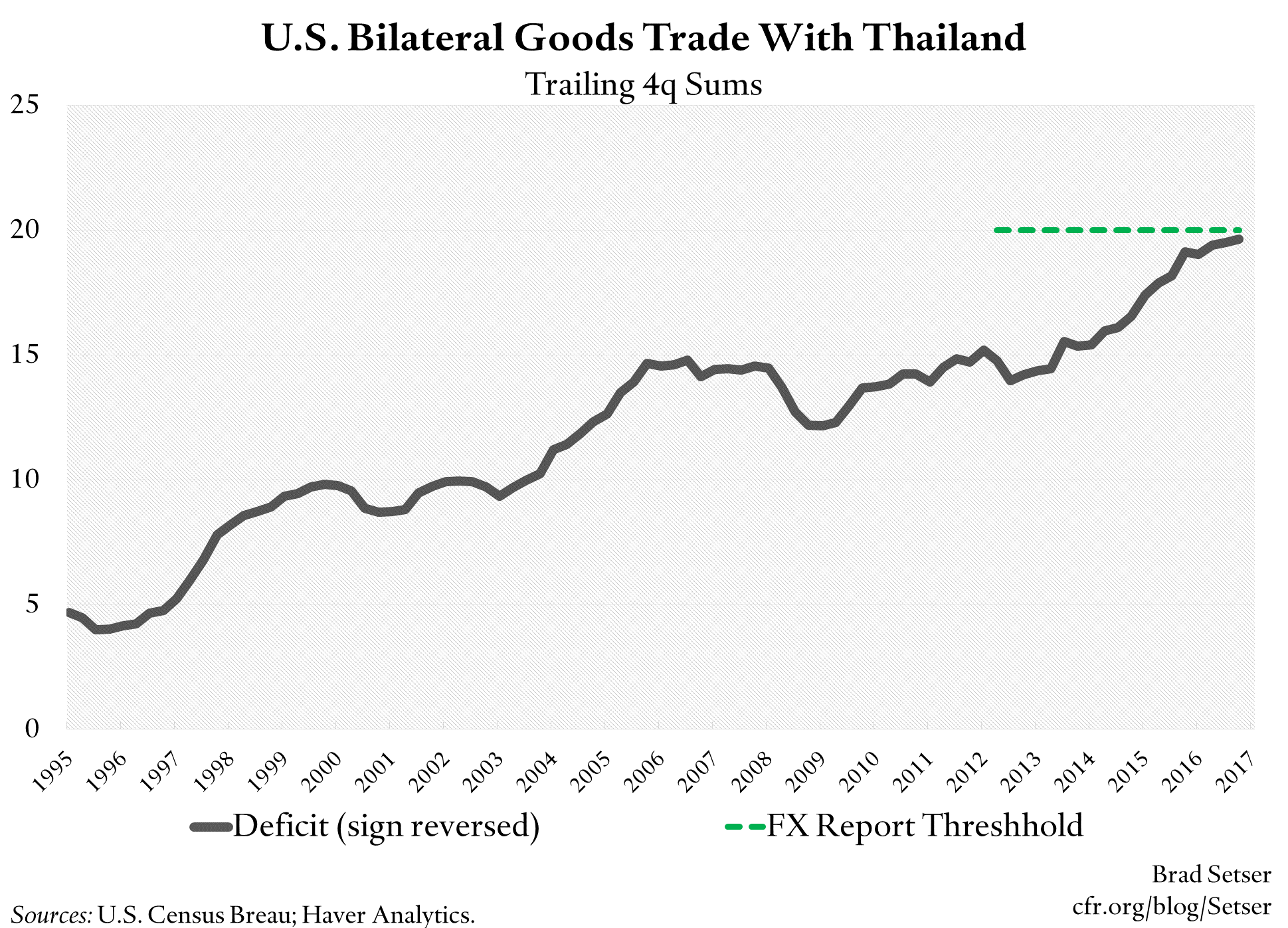

Thailand has gotten off in the past, because, well, it wasn’t judged a major trading partner and thus wasn’t covered by the Treasury report. And because its bilateral trade surplus with the United States fell just short of the Treasury’s $20 billion threshold.

But wow is it getting close.

Thailand’s bilateral surplus (e.g. the U.S. bilateral deficit) in the last 12 months of data (through November) was $19.86 billion. So, barring a change in trend, Thailand’s bilateral surplus will top $20 billion before the next foreign exchange report is released.*

The ticker for the first 11 months of 2017 shows a bilateral surplus of $18.49 billion (table 14). A $1.52 billion surplus in December would put Thailand over the top. The monthly surpluses in October and November were each $1.8 billion…

Thus it is likely that Thailand will meet all three of the Bennet amendment criteria in about a month.

Just saying.

In some ways Thailand would be an ideal test case for the Bennet designation process. It isn’t a borderline case: Thailand has a very large external surplus, and there is no doubt that it has intervened significantly in the market.** It isn’t next door to North Korea, so there isn’t a strong geo-strategic case for letting Thailand off. And the consequences of a designation are, by design, relatively mild, as Congress wanted the designation process to be used. Designation results in a year of enhanced bilateral engagement, and if no solution is found at the end of the year, the Treasury Secretary has to choose at least one of the listed possible sanctions. But the sanctions themselves aren’t all that onerous: see section 701 of the 2015 Trade Enforcement Act for the details.

Yet my guess is that the Treasury (at least the staff) is hoping that Thailand doesn’t formally cross the threshold until early next year. The April report technically only covers the period through December. And I am sure there will be pressure to give Thailand a bit of time on the watch list before declaring it a manipulator.

* The Treasury, for data availability reasons, uses the goods balance. But adding in services wouldn’t really change the number for Thailand. The United States imports a lot of tourism services (e.g. it is a popular vacation destination) from Thailand, so the services account tends to be close to balance. In 2016, in fact, the United States ran a services deficit with Thailand of just over $0.5 billion (see the interactive tables)

** The Thai baht did appreciate in 2017, and appreciated by a bit more in early 2018. This shouldn’t be surprising. Most countries that intervene do so to limit the pace of appreciation, not to drive the currency down—e.g. they tolerate market pressure to depreciate, but not market pressure to appreciate. In the first part of 2017, Thailand’s central bank looks to have intervened to keep the baht from appreciating through 34 before shifting to defending 33 (against the dollar). With the dollar’s broad weakness in 2018, they are now possibly defending the 32 mark.