The Foreign Asset Position of Chinese Banks

Some thoughts on how China’s state banks may have funded their growing external loan portfolio

One of the known unknowns of the financial world is the combined forward (and swaps) book of China’s “core” global financial institutions: the People’s Bank of China (PBOC) obviously, but also the Bank of China, the Industrial and Commercial Bank of China, China Construction, the China Development Bank (CDB), China Exim and maybe a few other.

When China joined the IMF’s Special Drawing Rights (SDR) basket it also committed, in principle, to disclose the PBOC’s forward book—forward purchases and sales are part of the IMF’s reserve disclosure standard. But, well, the disclosed forward book never really has convinced. Too stable at the start (The disclosed position was stuck at $29 billion for a long time. It then jumped to $45 billion in late 2016 before falling to around $10 billion this year). And it didn’t map easily to the forward position implied by the foreign exchange settlement data (which should cover the entire banking system, including the PBOC).*

And in some important ways China has become less not more transparent over the last two years. In the fall of 2015, China stopped publishing two data series that had in the past perhaps provided some information about the banks’ foreign exchange position: the foreign exchange position of the banking system, and state banks foreign currency funding from the purchase and sale of foreign exchange (which seemed to include funding from forward purchases/ sales).

This is a long-winded way of saying that it is, to my knowledge, impossible either to prove or disprove Christopher Balding’s argument that the rapid growth in the foreign assets (and net foreign assets) of China’s state banks over the last several years reflects the banks’ willingness to allow wealthy Chinese residents with yuan trapped onshore to swap their yuan for foreign exchange, and it thus represents ongoing capital flight.

Swapping Theories

There is no doubt that demand for such swaps existed at a time when the yuan was widely expected to depreciate.

But, generally speaking, commercial banks aren’t in the business of running an unmatched foreign exchange book—they are in the FX “flow” business, not in the business of warehousing and holding FX risk. In the absence of a regulatory blind eye to an unmatched book, a commercial bank would only swap onshore yuan for offshore dollars if an offshore actor wanted to swap dollars for yuan.

And it isn’t obvious who wanted to swap into a depreciating yuan. Exporters who want to lock in a future price for their dollar proceeds are one answer, but with the dollar expected to appreciate, it isn’t obvious why they would want to hedge by selling their dollars forward. The other answer is a Chinese actor who already has lots of previously unhedged foreign assets and who might want to lock in a price for converting back to yuan. The China Investment Corporation (CIC) is the most obvious candidate I think, as it historically hasn’t hedged its foreign assets – though it also isn’t clear why it would want to give up the potential profit from a weaker yuan.

Now a bank can set up an opposing position if the forward flows do not match up—if a client swaps out of yuan and into dollars, the bank would need to borrow dollars (say from the central bank), sell them, and hold yuan to be matched. But if that was happening the PBOC also might start asking a few questions…

So I am not convinced the buildup of foreign assets represents state banks meeting the demand for foreign currency from Chinese firms and households through off-balance sheet swaps. Not unless there is an opposing flow that keeps the banks’ books balanced—

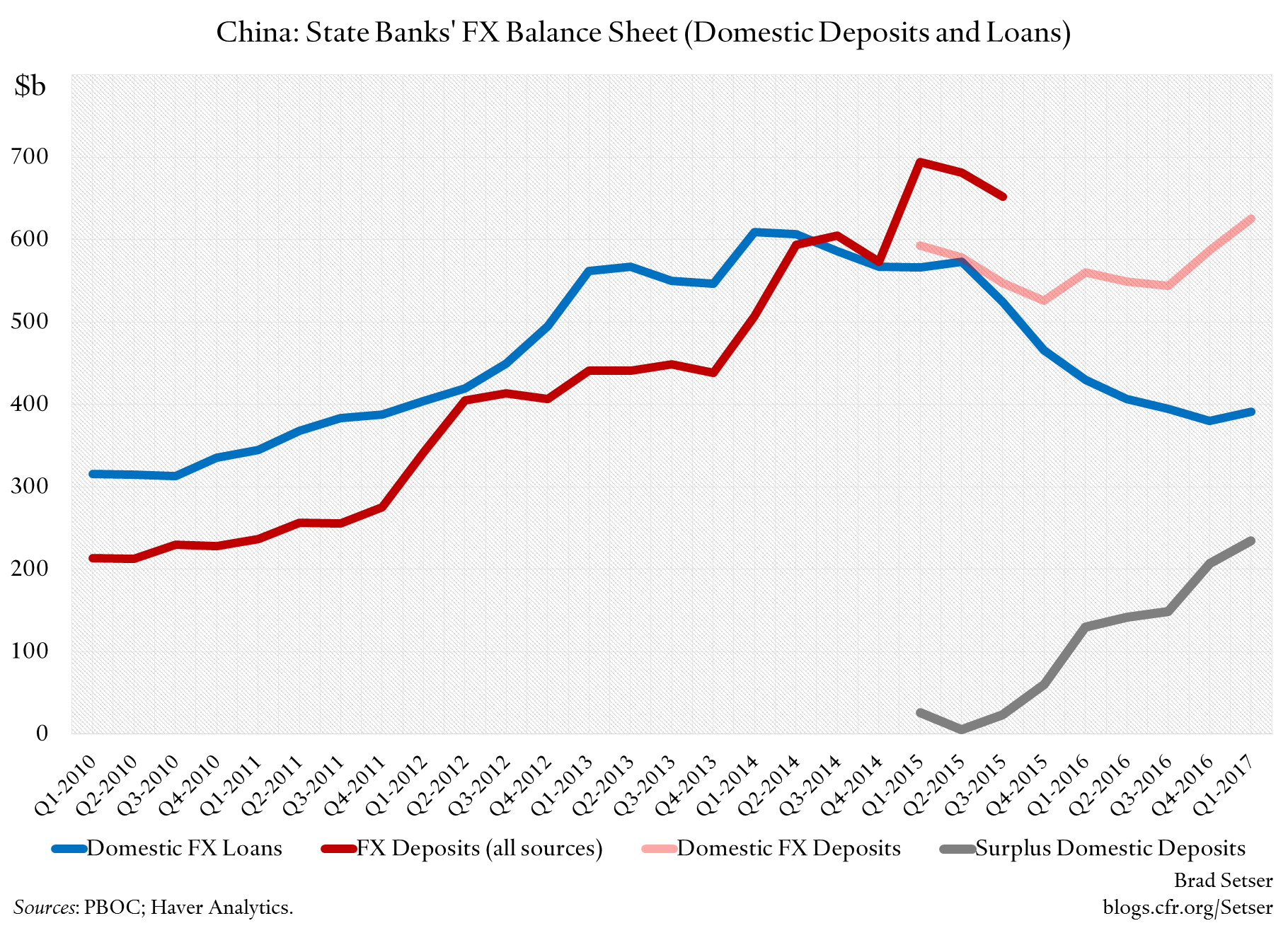

Domestic Dollar Deposits No Longer Balanced by Domestic Dollar Loans

The available evidence suggests a more prosaic source of funding for much of the banks’ rising foreign asset position: domestic foreign currency dollar deposits. Or really domestic foreign currency deposits, net of domestic foreign currency lending.

The net position of the banks in foreign currency vis a vis Chinese residents has shifted significantly since the middle of 2015. In early 2015, domestic dollar loans were roughly equal to domestic dollar deposits. At the end of q1, domestic dollar deposits exceeded domestic dollar loans by about $250 billion.

So increasingly residents’ dollar deposits are being matched by foreign currency lending to non-residents.

A bit of advanced balance of payments math. A dollar loan to a resident doesn’t necessarily generate a balance of payments outflow. It depends on whether the company borrowing the dollar holds onto it and puts it on deposit abroad (it which case it should show up as an increase in China’s total foreign assets), or sells for yuan. A dollar loan to a non-resident (a long-term loan by the CDB for example) by contrast is a balance of payments outflow. **

Broadly speaking, over the past few years Chinese companies stopped borrowing in dollars (why borrow in a currency that is expected to appreciate?) and paid down their internal and external dollar loans. As a result, the banks could no longer match domestic dollar deposits with domestic dollar denominated loans, and started to build up their foreign assets (there is a rise in overseas loans in the state banks foreign currency balance sheet, and a rise in their holdings of foreign currency denominated securities).

That at least is the story in the state banks’ foreign currency balance sheet.

Trying to Make Different Data Sources Match Up

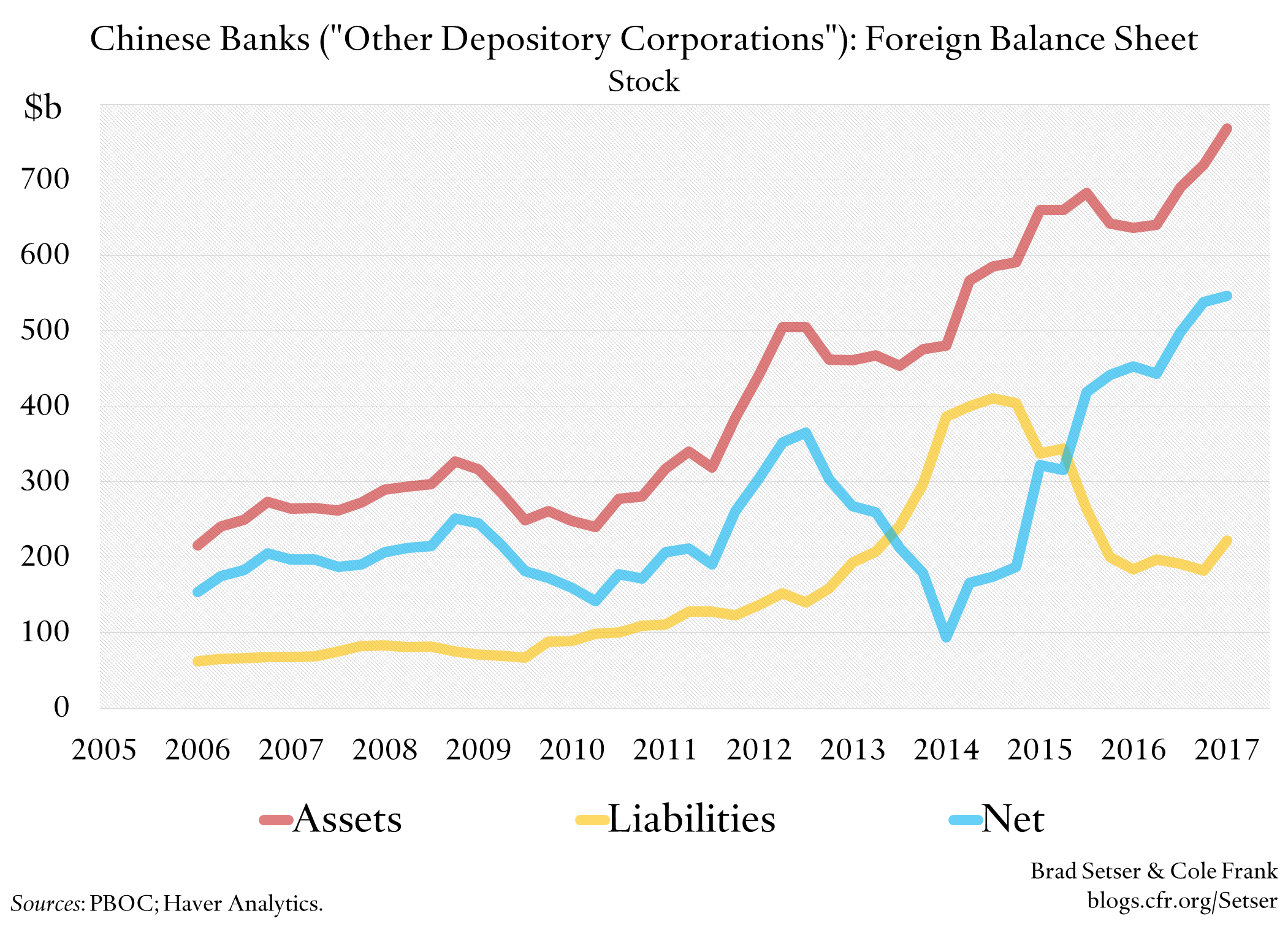

Of course, with China not everything lines up perfectly. The foreign currency balance sheet of the state banks, for example, reports some data on the banks‘ overseas assets, and more can be inferred by the gap between the banks domestic deposit loans and domestic foreign currency loans. So even though the foreign currency balance sheet is not done entirely on a balance of payments basis, it does contain balance of payments relevant information. Yet it isn’t the full story: the reported foreign (in a balance of payments sense) asset position of the banks (depository corporations) exceeds the gap between the state banks’ domestic foreign currency deposits and their domestic foreign currency lending.

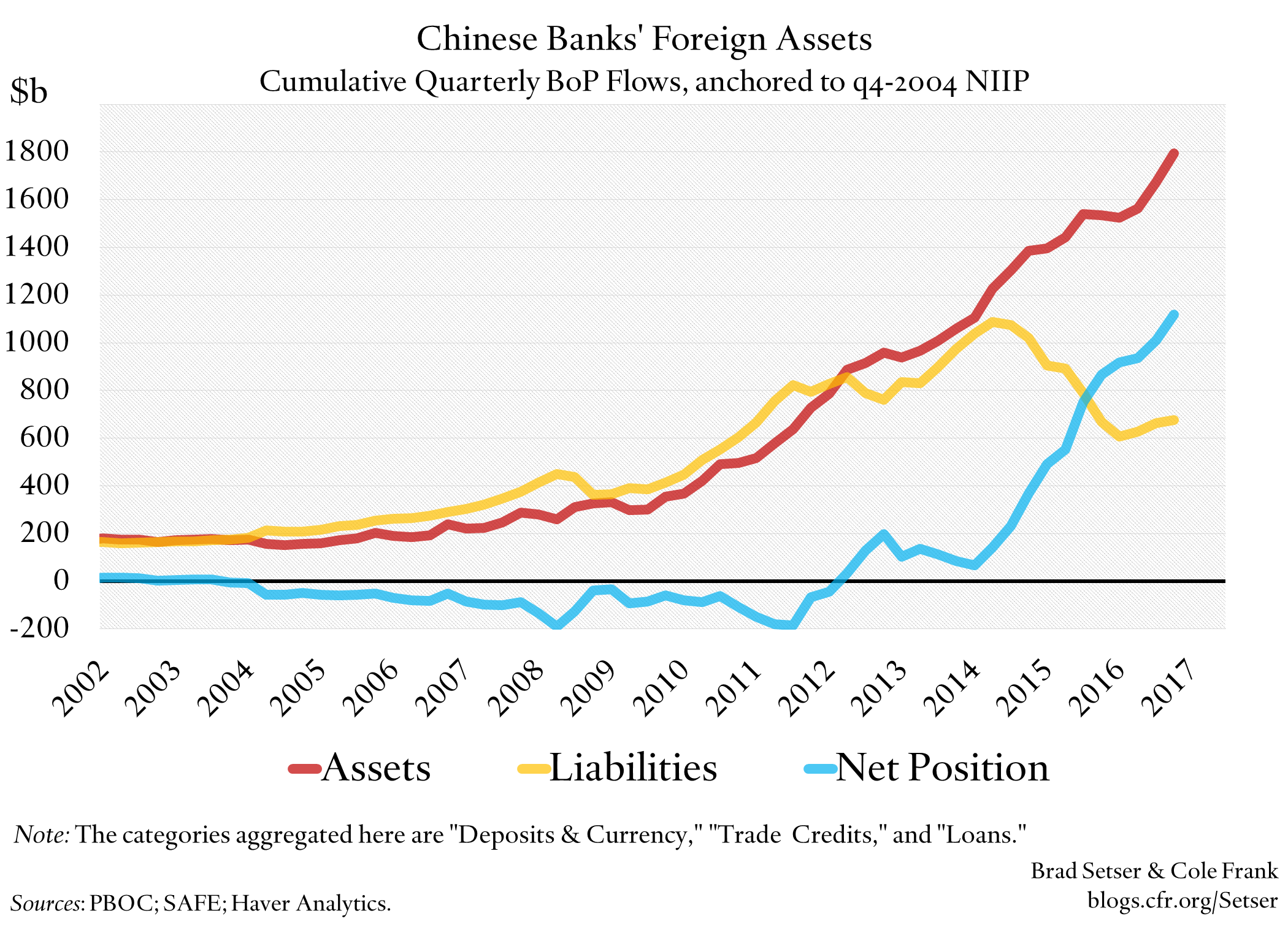

And, well, it turns out there is another gap. The reported net foreign asset position of the banks (other depository corporations in the PBOC’s data set) is much smaller than the net foreign asset position implied by summing up key lines in the balance of payments that tend to correspond with the broad banking system. The net position in the international investment position from these line items now tops $1 trillion. The assets from three key lines in the balance of the payments—deposits abroad, loans abroad, and trade credit—far exceed the associated liabilities (foreign deposits to China, foreign loans to China, and foreign trade credit to Chinese firms).

That is why I suspect some key state institutions (China ExIm? The CDB?) may not be in the “depository corporations” numbers. Or something else is going on. ***

The Big Picture

No matter. The big picture is pretty simple. If Chinese residents are putting dollars on deposit in the Chinese banking system, they aren’t outside of the reach of China’s authorities. China could force the state banks to lend the dollars to the central bank (and count the borrowed dollars as reserves—see Turkey!) if it really was short on foreign exchange. So far, it hasn’t.

Similarly, in a pinch, China could slow the foreign lending of the China Development Bank and the big state banks, and in the process conserve foreign exchange. Of course, that would make it hard for China to deliver on its financial commitments to the Belt and Road Initiative. Having options doesn’t mean there aren’t trade-offs.

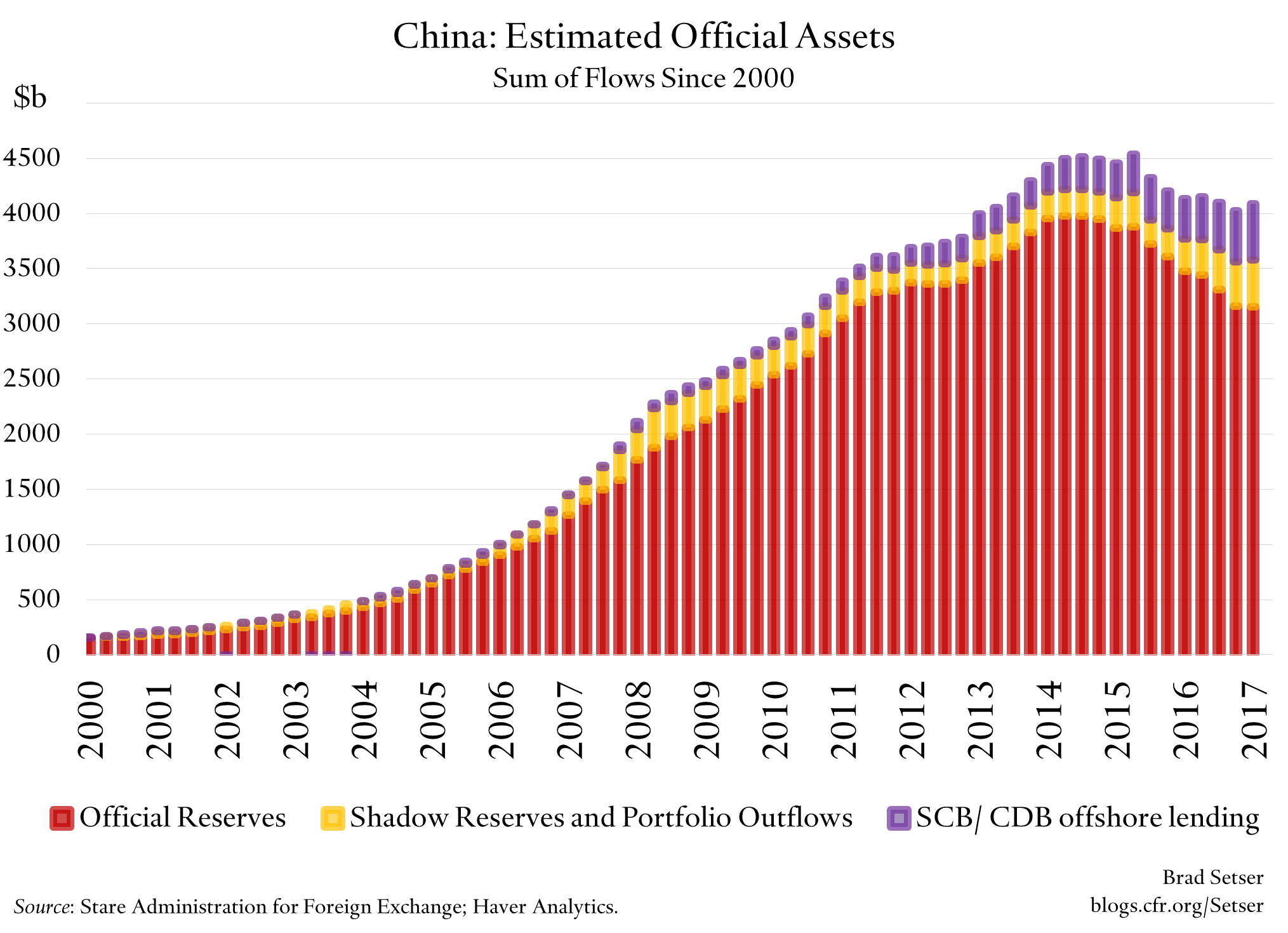

And when you look at the total foreign assets of China’s state—estimated using the balance of payments lines that correspond to the long-term assets of state banks and the China Investment Corporation—they actually have been pretty constant over the last year or so, after unquestionably falling in late 2015. The share of liquid reserves has gone down while the share of illiquid bank loans has increased—but that seems to in part to be a conscious policy choice.

* The forward book implied by the settlement data also has been shrinking in 2017, but the implied starting stock is higher – and the monthly changes have generally not matched.

** The balance of payments accounting. A dollar in cash held by a Chinese resident is a foreign asset—it is a claim on the U.S. central bank. A dollar on deposit in a Chinese bank isn’t a foreign asset—it is a claim on a Chinese bank. A dollar loan from a Chinese bank similarly isn’t a foreign asset—it is a claim on a Chinese resident. A dollar loan to a non-resident abroad though is a foreign asset. The net result of putting a dollar on deposit in a state bank bank, with the state bank then using the domestic deposit to fund a long-term loan abroad is a dollar rise in China’s total foreign assets. During the days of yuan appreciation, Chinese firms who could would borrow dollars and then sell them for yuan—getting a higher interest rate on the yuan (the carry trade) and hoping to pay the bank back by buying dollars back when the loan matured at a better price (e.g. profit from the dollar’s depreciation). The inflow let to a rise in reserves, as Chinese firms borrowed in dollars but didn’t want to actually hold dollars. Obviously that has changed.

*** To make everything more complicated, the CDB has a structural need to swap yuan for dollars as well as it has more foreign currency assets than foreign currency debts given that it funds primarily through the sale of yuan-denominated bonds. I have always been curious who is on the other side of its swaps book. Of course, being a state development institution it need not be matched—it could just borrow in yuan, sell yuan for dollars—reducing reserve growth—and lend the dollars out, taking the associated foreign exchange mismatch.