Foreign central banks aren’t going to finance much of the 2009 US fiscal deficit; their reserves aren’t growing any more (the q4 2008 COFER data)

The latest COFER data doesn’t show much change in the dollar’s share of global reserves: the dollar accounted for 64% of the reserves of countries that report data to the IMF at the end of 2008, exactly the same share as at the end of 2007. The dollar’s share of the reserves of advanced economies rose just bit, going from 66.9% at the end of 2007 to 68.1% at the end of 2008. And the dollar’s share of reporting emerging economies -- a set that importantly excludes China -- fell from 61.3% to 59.7% over the course of 2008.

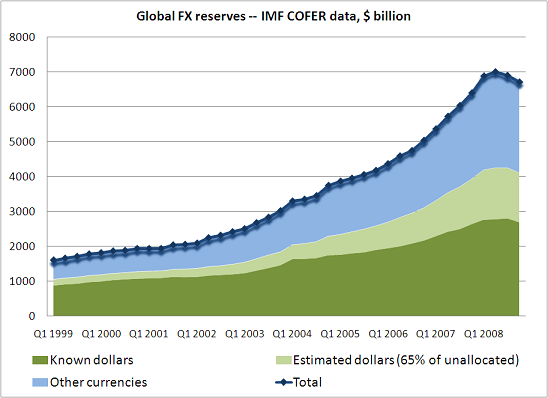

Those small changes though aren’t the real story. The real story is that global reserve growth -- and thus dollar reserve growth -- has slowed. Look at the following chart. To estimate the stock of dollar reserves, I assumed that the countries that do not report data to the IMF held a constant 65% of their reserves in dollars (this is effectively an assumption about the dollar share of China’s reserves*). And to keep things simple, I didn’t add in the growth in the non-reserve foreign assets of China’s central bank or the growth in non-reserve foreign assets of the Saudi Monetary Agency. This is very easily replicable graph.

The obvious implication of the recent downturn in total reserve holdings -- and the $180 billion fall in q4 wasn’t driven by currency moves -- is that the pace of growth in the world’s dollar reserves has slowed dramatically.

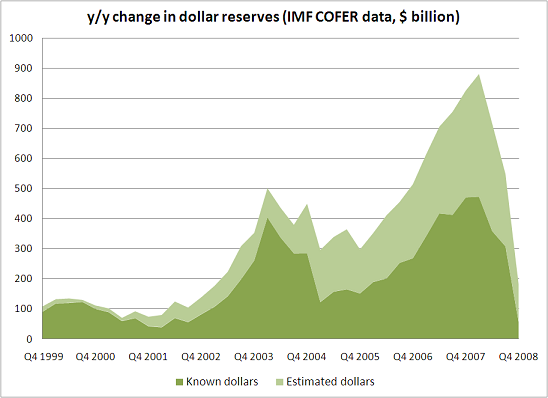

In the fourth quarter, the IMF data shows a $110 billion fall in the dollar holdings of countries that report detailed data to the IMF. That all came from emerging economies -- who had to sell their reserves to finance massive capital outflows. The reserves of the countries that don’t report data to the IMF also fell by $55 billion. They likely reduced their dollar holdings proportionately.

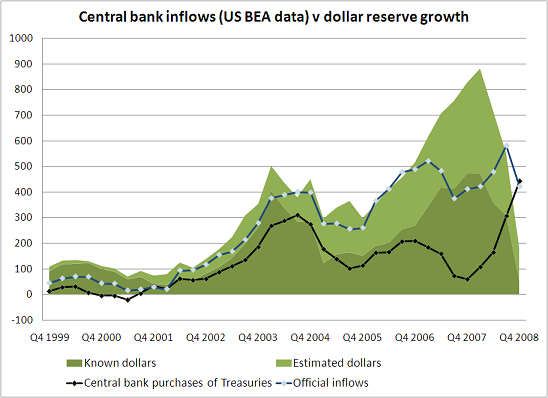

The US data didn’t show comparable sales from central banks. Central bank inflows slowed to a crawl, but the US data doesn’t show large sales. That implies, I think, that the world’s central banks pulled a lot of large dollar deposits from the “eurodollar” market. They weren’t in the mood to take chances after Lehman. Big uninsured deposits were risky. Some of that money -- along with the money that was withdrawn from the agency market -- found its way into Treasuries.

A chart of central bank purchases of Treasuries against reserve growth shows that central bank purchases of Treasuries soared even as dollar reserve growth fell.** That can only go on for so long.

Over time -- setting big shifts in the composition of reserves -- central bank demand for Treasuries tends to track reserve growth.

The obvious implication: most of the 2009 US fiscal deficit will need to be financed domestically. The Fed’s custodial data indicates central banks are still buying Treasuries, though at a somewhat slower pace than in late 2008. But their demand hasn’t kept up with issuance.

That isn’t necessarily a bad thing either. If a large fiscal deficit was driving an expansion of the US current account deficit -- and a rise in say China’s surplus that was being recycled back into the US -- I would worry a lot more about the United States external position than I do now. The US should want the rest of the world to take policy steps to support demand for goods -- not to restrict demand growth, run current account surpluses and have more money available to lend to the US.

* This is lower than I have used in the past; the latest survey data suggests China did diversify its reserves from mid-2007 to mid-2008, and it is quite clear that China accounts for most of the $2177b in unallocated reserves. The fall in unallocated reserves in q4 likely reflects the fall in the reserves of countries like the Emirates.

** The BEA’s data hasn’t been revised to reflect the latest survey; that explains the fall off in inflows from q2 2007 to q2 2008.