Getting Debt Restructuring Terms Right

State contingent instruments can play a role in debt restructuring agreements, but they shouldn’t be a give-away to investors. There is a compelling case for their use in Zambia—but not in Sri Lanka.

After months of delay, the debt restructuring process for low income countries that borrowed excessively from both China and the bond market is starting to grind forward. For all the talk of a need for a new institutional architecture for sovereign debt restructuring, real progress generally comes from innovations introduced to solve complex cases.

And the key cases right now are Zambia and Sri Lanka. Zambia is above all the key case for restructuring Chinese policy bank loans; the face value of recognized Chinese bilateral loans is about two times the face value of Zambia’s bonds.* Sri Lanka, by contrast, is fundamentally a bond restructuring story, though the Export-Import Bank of China, India, Japan and the China‘ Development Bank all have significant exposure.

But rather than focus on the challenge of coordinating the restructuring of Chinese policy banks, I want to focus narrowly on the challenge of securing agreement with commercial bond holders.

The actual negotiations with the bond holders haven’t formally started. Zambia is reported to have made a concrete offer to its official creditors, including the Export-Import Bank of China.* An offer to its bond holders is only expected once the terms of the official restructuring are clear. Sri Lanka is also initially focusing on its external official creditors—who aren’t negotiating as a single committee but rather than have split into two groupings, one led by China’s Export-Import bank and another that represents both India and the traditional “Paris Club” creditors. Negotiations with external bond holders aren’t likely to start until this fall—in part because the bond holders have insisted that Sri Lanka “optimize” or reschedule a portion of its domestic debt (I personally believe this is a mistake, but it is a demand that the International Monetary Fund’s debt sustainability framework for market access countries implicitly encourages through its focus on the total stock of public debt; the low income country debt sustainability framework, by contrast, only covers external public debt).

As always, finding a solution means finding a package of new bonds that can be exchanged for the existing set of bonds in default. That means talking about actual cash flows and the valuation of the new bonds. It also means thinking about the role contingent instruments can play in the restructuring. Sri Lanka’s bond holders reportedly are seeking GDP-linked bond payments. Zambia’s advisors are thinking about ways to help close the gap between the cash flows implied by the IMF’s debt sustainability analysis and the current market value of Zambia’s bonds (see Lazard’s February White Paper).

And in both cases, there are contingent options that in my view make sense, and frankly, those that don’t.

This discussion matters for those with a stake in the specific cases, but also to all those who care about finding ways to make debt restructurings faster and more efficient. Zambia, Sri Lanka, and Ghana (a case where China is not front and center) are unlikely to be the only restructuring cases of this cycle.

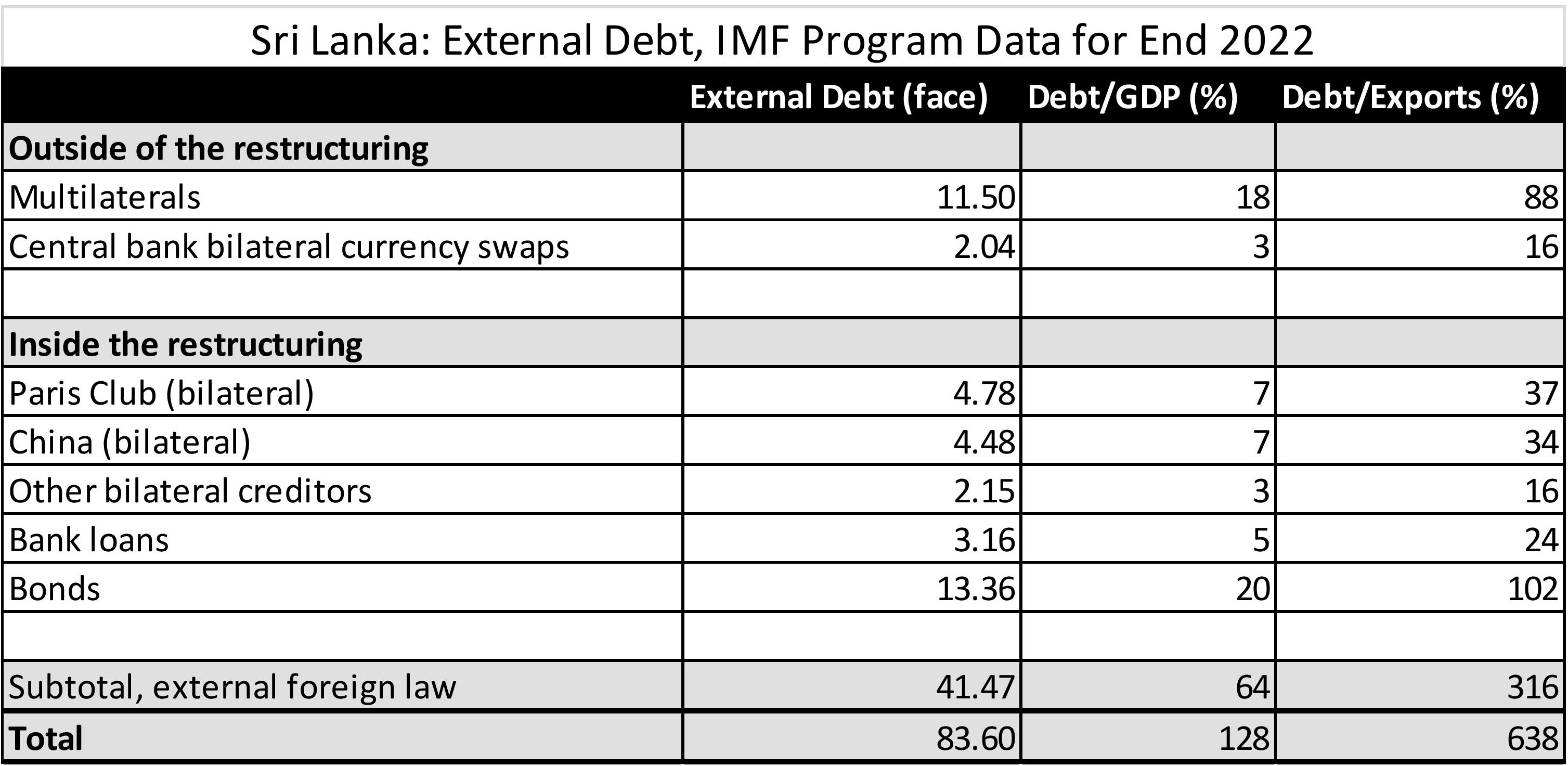

Sri Lanka

Sri Lanka should be an easy restructuring.

The IMF’s criteria are frankly not very constraining.

In fact, I think the IMF made a mistake by setting out criteria that imply Sri Lanka’s debt sustainability can be judged largely based on its gross financing need, and thus Sri Lanka can support a significantly higher public debt stock going forward than it was able to manage in the past so long as the gross financing need is reduced.

The IMF program only requires a bond restructuring that, in conjunction with the bilateral debt restructuring, keeps total debt under 95 percent of GDP in 2032. It also requires that Sri Lanka keep hard currency payments under 4.5 percent of GDP between 2028 and 2032.

A bit of math. The external foreign currency debt of Sri Lanka’s government is currently around $40 billion. Even with an increase in foreign currency debt from multilateral development bank (MDB) fiscal financing during the program period, external foreign currency debt is expected to fall to 50 percent of GDP at the end of the program period in 2027 as GDP recovers (it currently is around 65% of GDP). To my way of thinking, a net present value (NPV) neutral coupon would easily fit within this parameter, as an exit instrument that yields 5 percent (the NPV neutral rate for low income countries) would only use 2.5 percent of the 4.5 percent of GDP foreign currency payment envelop. MDB and IMF amortizations are around 1 percent of GDP a year. Thus, there is even a bit of room for early amortization of some bilateral or market debts.**

These requirements, together with the current market pricing of the bonds, set the stage for a straightforward exchange. Even with the recent rally, Sri Lanka’s roughly $13 billion in external foreign currency bonds trade at around 40 cents on the dollar. The market cap of Sri Lanka’s bonds, so to speak, is a bit over $5 billion.

For the sake of argument, let’s assume that the restructuring reduces the face value of the bonds by 40 percent. Thus, Sri Lanka would issue new bonds with a face value of just under $8 billion in the restructuring. Let’s also assume the bonds have a 4 percent initial coupon (or $312 million a year in cash flow) that steps up 8 percent in 2028.*** This translates to $620 million a year in cash flow, which would be in the range of 0.6 percent of projected GDP. I also assume this bond fully amortizes in 2033, which is an intentional over-simplification.

At a 10 percent exit yield, this bond should trade up. A holder of the bonds now in default would get a new bond that should trade at about 80 percent of its new face value, or at almost 50 cents on the current face value of bonds now in default. If Sri Lanka’s GDP outperforms the IMF’s projections—as many bond holders believe is likely—the new bond should rally to par, which would raise the recovery on the old bonds to around 60 cents on the dollar.

Of course, bond holders want a bit more. But I suspect, given that the bonds have traded at prices in the thirties for some time, they ultimately would accept a deal along roughly these terms. Evaluated at a 5 percent discount rate, this offer incidentally has a 30 percent NPV reduction (a bit more than in the offer that Sri Lanka has made to its bilateral creditors, which supposed has an NPV reduction of 23-28 percent). Thus, it more or less achieves the amount of debt reduction that I think the IMF should have required.

The bond holders supposedly want a GDP-linked option that would let them recover all lost principal if Sri Lanka’s GDP is higher than the IMF projects: a warrant for the $5 billion in forgiven principal.

I understand the demand but giving such an option, in addition to a bond that should trade up if Sri Lanka outperforms the IMF forecast, simply isn’t a good deal for Sri Lanka. The bond holders don’t need to be made whole for the deal to work given current market pricing. If Sri Lanka wants to give the bonds more upside, Sri Lanka would be better off by offering a slightly bigger nominal bond than by creating a complex GDP-linked instrument. GDP-linked instruments have historically not been highly valued by the market, so the country often ends up promising a lot of cash flow for very little gain.****

That said, if some bond holders really want a GDP-linked instrument, then it would make sense to provide a GDP-linked instrument with more upside and downside as a choice alongside a plain vanilla nominal bond.

For example, bond holders could be given a choice between taking either a 40 percent face value debt reduction and obtaining a new fixed rate instrument or taking a 60 percent reduction in face value and getting the associated fixed cash flows together with a GDP warrant. The warrant would be designed to provide a cash flow stream equal to 20 percent of the current face value of the defaulted bonds if GDP performed in line with the IMF’s forecasts—and more if GDP outperformed projections, less if it underperformed. If Sri Lanka’s GDP growth matches the IMF’s expectations, the two instruments would by design have roughly equal cash flows. Such a choice would force investors who believe the IMF is wildly understating GDP performance back their conviction with real money, giving up assured cash flow to get the optionality.

As an aside, Suriname is providing oil linked warrants in its restructuring that would provide investors a sum equal to the debt that it currently being written off; Sri Lanka though doesn’t have an obvious commodity export stream that would provide a natural anchor for a contingent instrument.

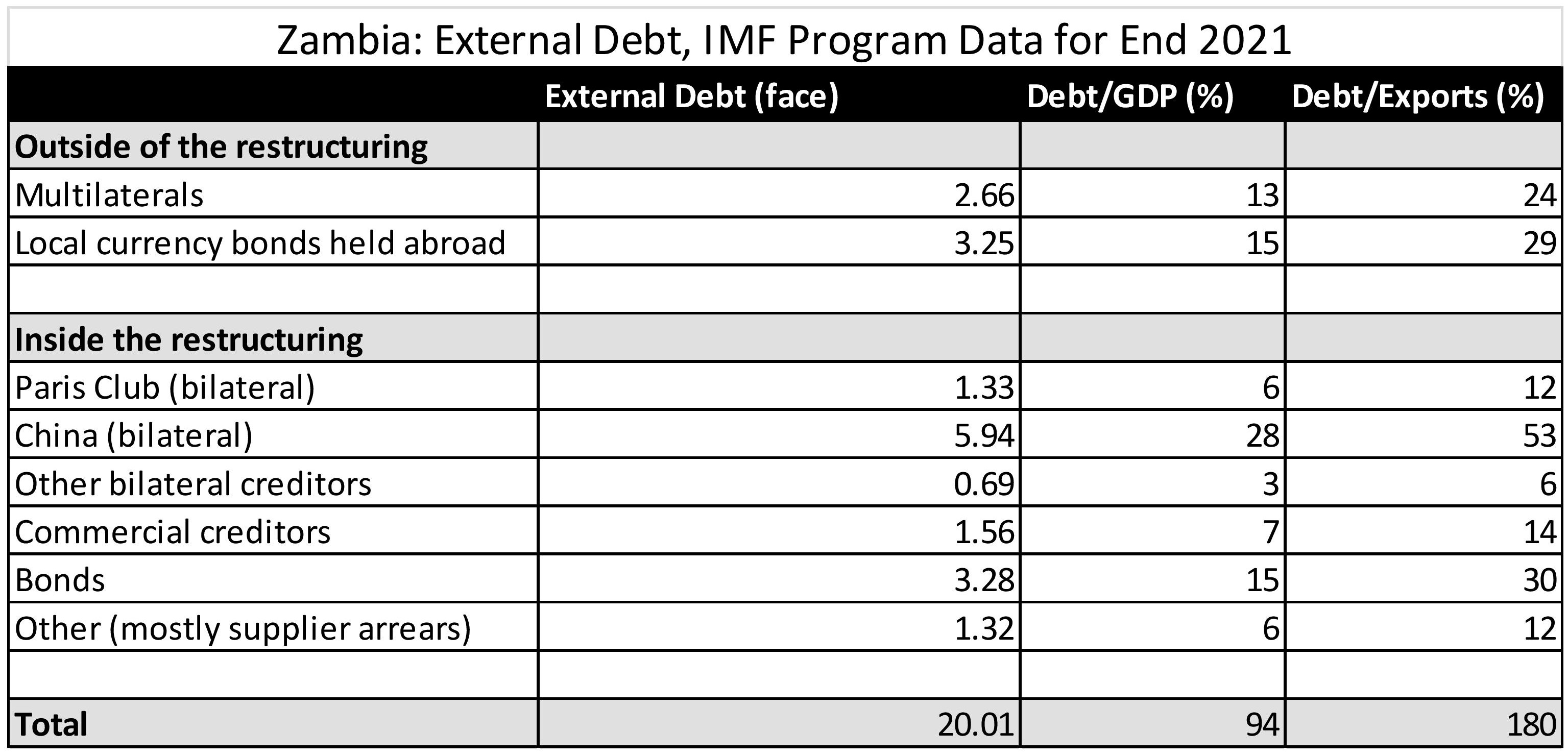

Zambia

Zambia’s bond math is more daunting.

Zambia has $3 billion in bonds, which trade at 40-45 cents on the dollar. The market cap is $1.6-1.7 billion.

Zambia has been in default for several years, resulting in significant accumulated unpaid interest—the total is around $600 million, and it will rise close to $850 million by the end of the year.

For the sake of argument here, let’s assume that Zambia issues a new bond with a face value of $1.8 billion, a 4 percent coupon until 2027, and an 8 percent coupon thereafter. This would result in $70 million of cash payments through 2026 and $140-145 million of annual cash flow thereafter.

This bond would not obviously meet the debt sustainability criteria that the IMF has set out for Zambia. Zambia falls under the low income debt sustainability framework, and the criteria the IMF uses in low income countries are focused entirely on its external debt. The IMF has set out both a target for the total NPV of external public debt in 2027 ($15 billion at a 5 percent discount) and external debt service relative to revenue (external debt service is limited to about $1 billion a year). These criteria, combined with the exclusion of both the MDB debt and local currency debt held by non-residents from the restructuring, are estimated to require a 49 percent NPV reduction from the end 2021 stock. The proposed bond though has an NPV reduction of closer to 33 percent.

The IMF is likely to adjust the needed NPV reduction, thanks to the reduced market value of Zambia’s local currency bonds. However, this will likely mean the needed NPV reduction will fall only a bit, say to 40 percent.

How can the gap be closed?

I have a simple suggestion.

Assume that the bonds stepped down to a 6 percent coupon if copper prices were below a specified threshold, and then stepped down further to 4 percent if copper prices were back at their 2020 levels.

The IMF might reasonably evaluate the bonds using the stepped down coupon, as the debt criteria were set to ensure Zambia could manage a period of stress. If they did so, that would create an instrument that the market would value based on the stepped up coupon (given current copper prices and forecasts) and the IMF could evaluate on the basis of the stepped down coupon. Chinese creditors could be given a similar deal structure if they so desired.

Technically, the deal is still difficult. It is worth only about 50 cents at the stepped up coupon and the market would assign some risk of a step down. At best, that is only a bit over the current market value of the defaulted bonds and I suspect Zambia’s creditors want an instrument that would initially trade up, not flat, to current market prices.

Still, the proposed structure gets close.

To me, this example is the kind of contingent instrument that should be used much more frequently.

The resulting instrument is a bond, not a warrant, and can easily be held by most bond funds. It offers the country real downside protection, even more so if the instrument has a maturity extension option. And it helps bridge a real gap in criteria that the market and the IMF use to evaluate a deal.

I certainly hope Zambia’s creditors, and its advisors, give some consideration to this structure.

More generally, there are other contingent instruments that clearly remain bonds and could be traded like bonds. A number of bond market investors have proposed, for example, that new bonds should generally be issued with a two year maturity extension option (a contractual standstill). A five year bond could be extended to a seven year bond, and a ten year bond could be extended to a twelve year bond. The market knows how to price such simple options.***** Together with step downs in coupons linked to well defined shocks, they could provide instruments that the IMF might appropriately embrace. And unlike many other, rather academic, proposals for contingent instruments that are unlikely to ever be adopted, this kind of simple, bond based optionality could potentially deliver a real positive shock to the global debt restructuring architecture.

* The Export-Import Bank of China alone has $4 billion of Zambia’s $8 billion in “bilateral” loans, and other Chinese banks have another $2 billion or so.

** I am having a bit of a debate on this point with some parts of the IMF. The IMF asserts that the benchmark restructuring would result in NPV reduction for Sri Lanka (per the Annex in the latest Staff Report). As I understand it, this is entirely because the new bonds that are assumed to emerge from the restructuring start to mature in 2028 at a fairly rapid pace ($1.5 billion matures every year, with Sri Lanka issuing that amount or more in the market). Since the new bonds are assumed to mature right after the overall interest rate on Sri Lanka’s debt is allowed to step up in 2028, the exchange mechanically results in NPV debt reduction. But the NPV of the total debt stock in say 2032 should also include the bonds that are assumed to be issued from 2028 on to refinance the rapid amortization of the bonds issued in the restructuring. In my view, the total NPV of the bonded debt in 2032 will exceed the current face value of Sri Lanka’s bonds. Moreover, I think it would be a serious mistake to have the new bonds largely mature between 2028 and 2033. That exposes Sri Lanka to substantial rollover risk, as Sri Lanka has no history of issuing bonds in the market at the debt-to-GDP levels that are expected in those years. Moreover, the rapid amortization of the new bonds appears to constrain, given the 4.5 percent of GDP cap on projected FX debt service, the scope to make interest payments on the same bonds; it isn’t obvious to me why the bond holders wouldn’t prefer to switch amortization payments to coupon payments between 2028 and 2032 and have a bond that amortizes later. Cash upfront is good, but most bond restructurings are designed to maximize the cash flow that the bonds get over time—not to minimize it.

*** An 8 percent coupon would be consistent with the coupon that emerged out of Suriname’s negotiations with its bond holder committee. It creates an instrument that would be expected to trade at par or even above par in a world where long-term U.S. Treasury rates are between 3 and 4 percent.

**** The IMF, back in 2020: “In some of these cases, payouts may ultimately prove to be quite large in comparison to the instruments’ initial valuations.”

***** Technically, a 10-year bond with a 2-year maturity is a 12-year bond, callable after 10 years. That is something the bond market knows how to price.