The IMF’s China Problem

Giving macroeconomic policy advice to a country that saves 46 percent of its GDP is hard. Imprudent domestic policies help limit large external (trade) imbalances, and more prudent domestic policies could result in a return to large external imbalances. Policy changes to reduce national savings are critical.

(Really, the world’s China problem)

The IMF, more or less, thinks that a country with China’s characteristics should be running a massive current account deficit.

That’s what the IMF’s workhorse model says, if you plug in the IMF’s assessment of China’s policies.

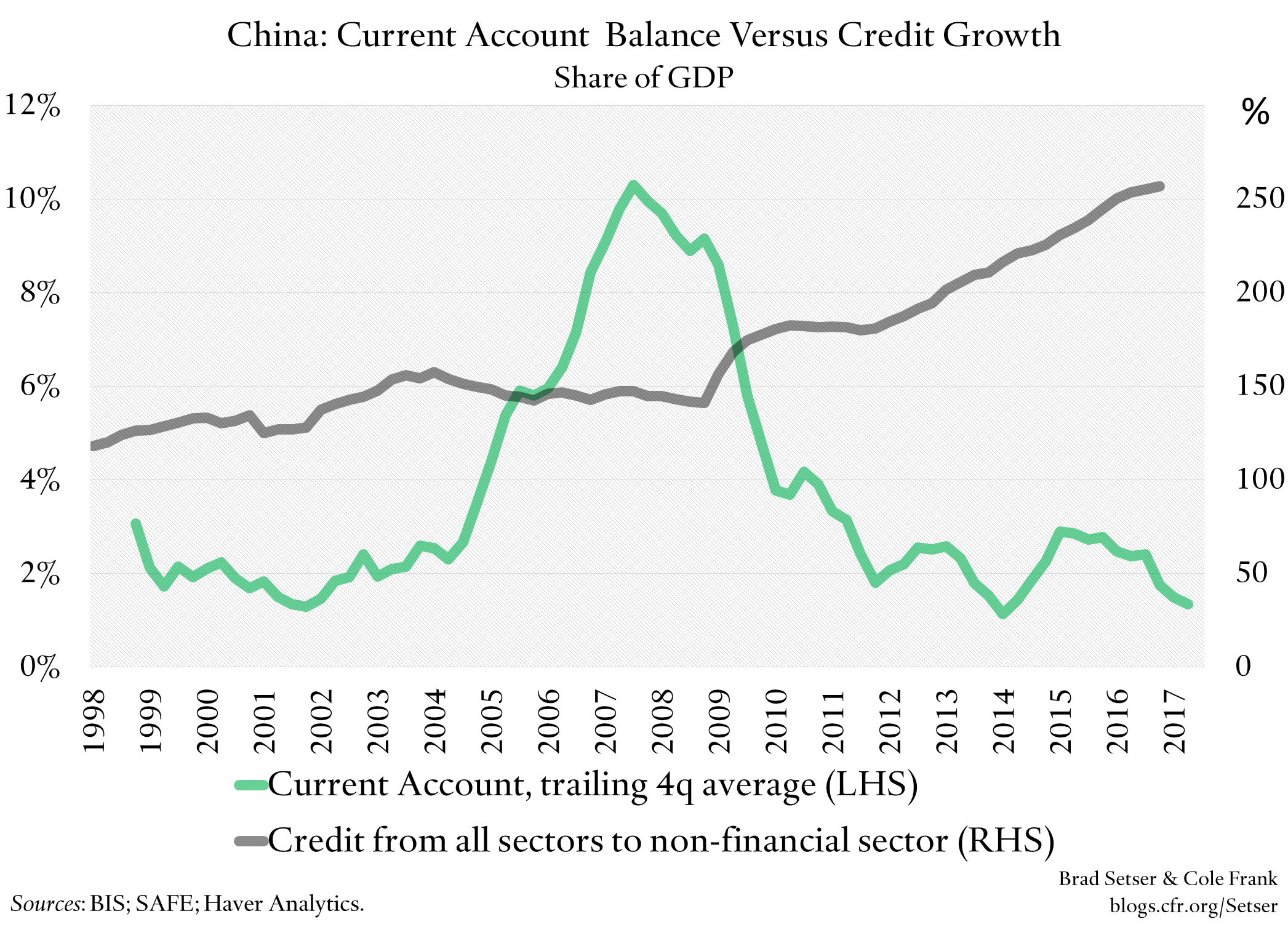

Excessive credit growth. Check. Leads to current account deficits.

A big fiscal deficit. Check. Also leads to big current account deficits.

China’s general government deficit, which counts recognized provincial borrowing, is about 4 percent of GDP. But the IMF thinks the real fiscal deficit is bigger. Much bigger: 12 percent of GDP, after a more than 2.5 percent of GDP fiscal expansion in 2015 and 2016 (see paragraph 4 of the staff report)

That’s because the IMF argues, contrary to the view of China’s government, that a lot of the borrowing by provincial and local state enterprises is really government borrowing. In the parlance of Chinese policy, the “front-door” was opened when the central government allowed provincial and local bond issuance well before the “backdoor” was closed.

Yet a country with a 12 percent of GDP fiscal deficit (10 percent of GDP if you exclude the portion of the augmented fiscal deficit financed through land and asset sales) and rapid credit growth still has a substantial trade and current account surplus. An external surplus of about two percent of GDP after the last fiscal expansion, once you adjust for the IMF’s estimate of financial flows disguised in the tourism deficit *

Think about what that means for a minute.

The IMF’s best guess—based on evidence amassed across a broad sample of countries—is that a 1 percent of GDP fiscal deficit generally leads to a current account deficit of between 0.4 and 0.5 percent of a country’s GDP. And it isn’t just the IMF. Menzie Chinn also found that fiscal policy has a large impact on the current account in his Jackson Hole paper.

So, more or less, the IMF thinks that a country with a 10 to 12 percent of GDP fiscal deficit should be generating a current account deficit of between 4 and 6 percent of GDP. **

Ok, to be super technical, this is only true if the “norm” is a current account of about zero, which just happens to be the case for China.

And excessive credit growth—even after adjusting for credit to SoEs that the IMF considers part of the disguised fiscal deficit, which should be netted out to avoid double counting—also is directionally working to bring China’s surplus down. The IMF estimates that excessive credit growth on average added about two percentage points to China’s growth over the last five years, so the effect on the current account could be substantial—especially as investment has a higher import intensity than consumption.

In other words China saves so much—about 45 percent of its GDP—that it runs a sizeable trade surplus even with what would otherwise be considered wildly irresponsible domestic policies

That’s a problem for the IMF.

The policies that the IMF—and many others—generally recommend for China are broadly speaking the policies that would typically be recommended to a country with a large external deficit: tighter credit, a smaller fiscal deficit, and the like.

They are also precisely the kind of policies that would be expected to increase the external surplus of a surplus country.

The IMF goes to lengths to note that it isn’t advocating China go cold turkey and bring its augmented fiscal balance down to zero or anything like that, and to note that China should adjust gradually (by 0.5 percent of a year, see paragraph 37 of the staff report). But even if the IMF thinks China can stabilize its fiscal debt-to-GDP with an augmented fiscal deficit of six to eight percent of GDP, that’s still a big change from the current 12 percent of GDP fiscal deficit.** A four percentage point fiscal adjustment might raise China’s external surplus by two percentage points, a six percentage point consolidation would be expected to raise China’s external surplus by about three percentage points—and tightening credit also would have an impact on the external surplus.

So broadly speaking, the IMF’s fiscal policy advice seems consistent with China eventually running a 4 to 5 percent of GDP external surplus.

At a time when China’s GDP could well approach $18 trillion (that’s the IMF’s forecast for China’s 2022 GDP—and it will only rise as you go forward), that translates into an external surplus that could approach a trillion dollars.

And since China’s economy is so much bigger than it was back in 2006 and 2007, even a 5 percent of GDP current account surplus would be record big when scaled against world GDP. It easily could approach one percent on global GDP.

The IMF does recognize that this a potential problem. While the press coverage of the Article IV focused on the IMF’s criticism of China’s latest credit binge, the Article IV also included a strong call for China to introduce a set of policies to bring down its high savings rate—and very explicitly noted that the projected impact of aging on savings on its own would not be enough to lower China’s savings rate to much below 40 percent of GDP. And the IMF went well beyond making a generic call for policies to boost consumption—it suggested a very constructive set of policies China should adopt (see paragraph 16 of the report.)

That’s music to my ears of course.

But I don’t yet see much sign Chinese policy makers are prepared to make the needed policy changes quickly enough.

I worry that will leave China in its current high savings trap. A trap that more or less means the economy is structurally short demand and only is in equilibrium when the government or firms borrow too much domestically, or when it borrows too much demand from the world. A trap that means China’s savings surplus either is used inefficiently at home, or dumped on the world. A trap that leaves China perpetually at risk of tightening too much and seeing its economy stall—absent a return to the very large pre-crisis external surplus.***

A better macroeconomic equilibrium—one with less credit and less (but hopefully better quality) investment, and much less savings—is possible. But getting there will be difficult, and take far more aggressive reforms—and by reform, I mean reforms that expand access to social insurance and raise transfers to low-income workers financed through progressive taxes, not just reforms to state banks and state firms—than China’s leaders have considered to date.

I consequently hope the IMF’s recommendations for bringing China’s savings rate down get the same kind of attention as its concerns about China’s credit excesses.

* See paragraph 3 of the staff report, the IMF thinks the tourism deficit is overstated by half a point of GDP; Anna Wong thinks it is more like a full percentage point.

** The IMF’s model got the impulse of China’s 2016 fiscal expansion right: the 2.5 percent of GDP or so fiscal expansion reduced the current account surplus by about a percentage point, roughly what one would expect. So even though the model’s overall fit with China is bad, I do not think there is any reason to expect that a fiscal contraction that lowers domestic demand wouldn’t increase the surplus.

*** The IMF’s precise long-term fiscal stance for China’s isn’t spelled out. The external sector review’s EBA model indicates that the IMF would like the general government deficit to fall from just under 4 percent of GDP to below 1 percent of GDP by 2022 or so (see table 3), but it doesn’t specify a target for the augmented fiscal deficit. The debt sustainability analysis in the IMF’s article IV—which looks at the augmented fiscal deficit as well as the general government balance—clearly indicates that the current augmented deficit is not consistent with a stable debt-to-GDP ratio. At the same time, the IMF recognizes that there isn’t a hard constraint that prevents the public debt-to-GDP ratio from continuing to rise—and thus that China still has fiscal space for a gradual adjustment. The chart on page 56 of the staff report shows the debt-to-GDP ratio stabilizing at around 100 percent with an “augmented” primary fiscal deficit of around 6 percent of GDP—which is 4 percentage points of GDP less than the IMF’s estimate of the current augmented fiscal deficit (10 percent of GDP). However, the translation from the augmented primary fiscal balance to the augmented overall fiscal balance and then to net government borrowing and lending (which is the variable in the EBA analysis) isn’t straightforward. net borrowing includes borrowing to pay interest but that is offset in part by the revenue raised through asset sales. Right now the general government balance is substantially lower than the general government primary balance -- see the fiscal table (table 4) at the end of the staff report. Personally I think a country with China’s favorable debt dynamics (lower nominal interest rates on its borrowing than nominal growth) and high domestic savings can support a general government deficit of substantially more than 1 percent of GDP, so I think the recommendation embedded in the desired general government balance in the EBA report is too conservative (the proposed fiscal consolidation for China is one of the largest in the world). More general government borrowing and less off balance sheet local government borrowing also improves debt sustainability because explicit debt carries a lower interest rate, so a looser general government deficit target would allow less overall fiscal adjustment. I also should confess that I had to get help from the IMF to figure out that their long-run fiscal advice is embedded in the chart on p. 54.

**** China grew very fast without any credit gap—credit to GDP was stable—from 2005 to 2008. But that also was the period when China’s external surplus shot up. The post-crisis surge in credit (with credit here including the credit to local government backed borrowing vehicles and firms that the IMF considers quasi-fiscal) helped China adjust to weaker external demand growth—basically China either has had stable credit and a big external surplus, or fast credit and a more modest external surplus.