Looking Back on Fiscal 2018 as Puerto Rico Starts a New Fiscal Year

Sales tax revenues have recovered. Fiscal year 2019, which started in July, should be a good year thanks to Federal disaster aid. The real question though is what happens when Federal aid starts to fall.

There is no real doubt that the Federal government—and for that matter, Puerto Rico’s own government—didn’t respond effectively to the devastation wrought by Hurricane Maria. I certainly hope preparations now are underway for the coming hurricane season.

But the initial devastation has now largely been cleaned up, and power has been restored to most of the island.

There is also relatively strong evidence that Puerto Rico’s economy has started to recover from Maria’s shock.

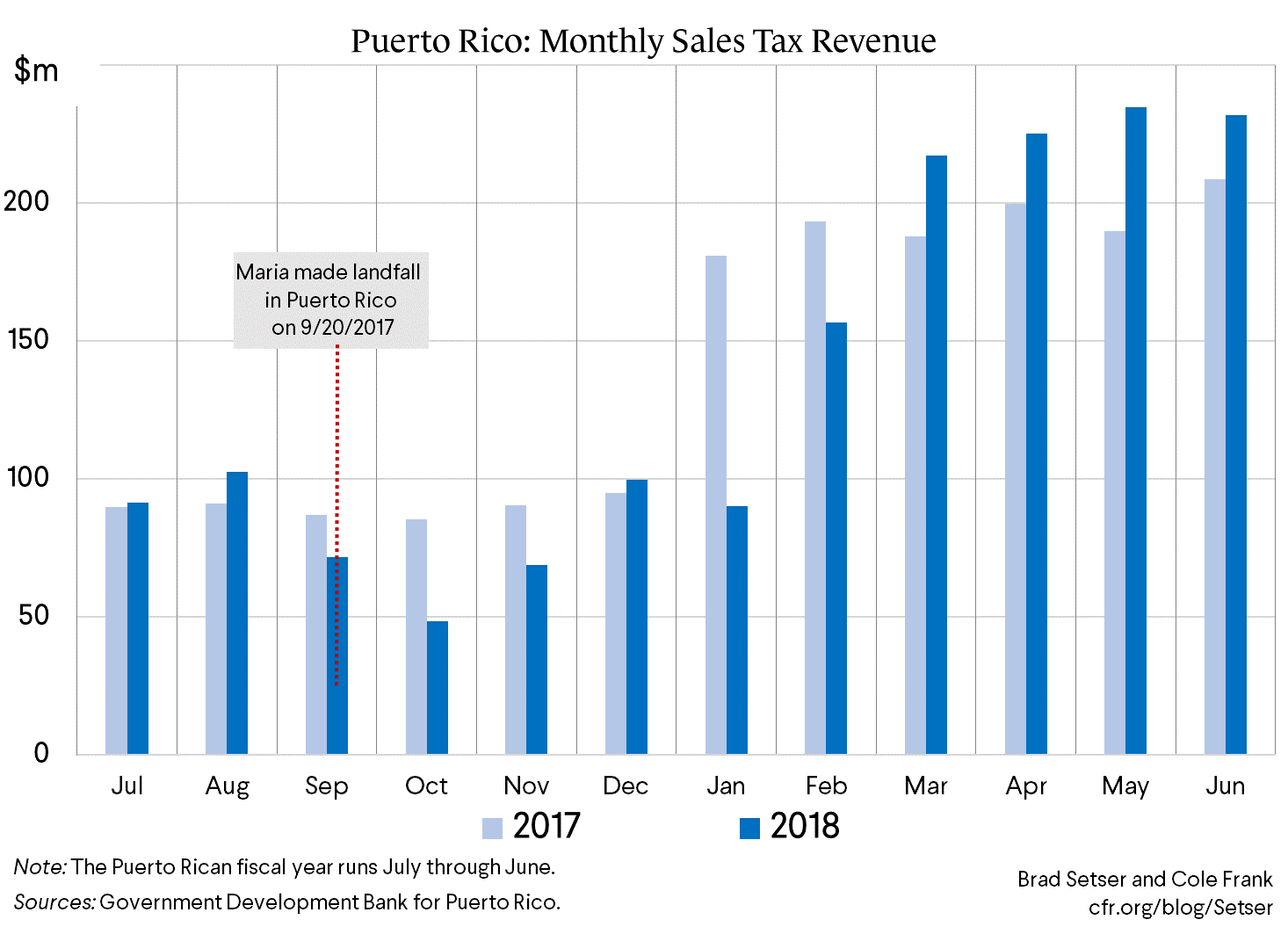

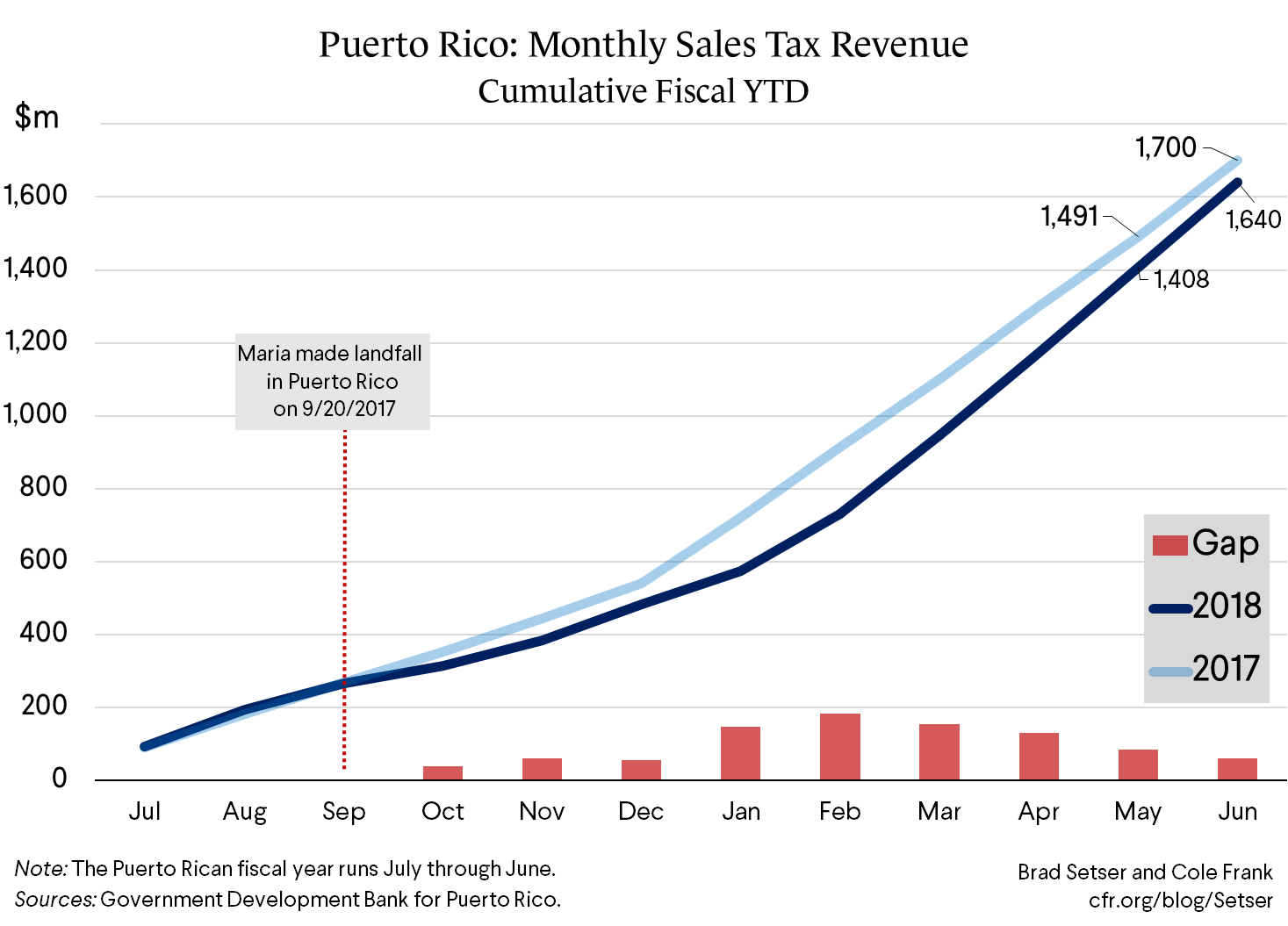

Puerto Rico’s economic numbers are notoriously bad, and the numbers on output are only available with a long lag. But sales tax revenues should be a reasonable proxy of economic activity. * And for the past few months, sales tax revenues have exceeded their pre-Maria numbers.

Indeed, the strength of sales tax collections in recent months looks to have allowed Puerto Rico to make up most of the deficit in Puerto Rico’s sales tax collections (relative to the pre-Maria baseline). The sales tax collections are thus consistent with other data indicating that Puerto Rico’s economy is now recovering (for example, cell phone data shows that some Puerto Ricans who temporarily relocated after Maria have now returned).

Puerto Rico was, for a set of complicated reasons, expecting a bit more revenue from the sales tax than it will receive in FY2018 (it was expecting to use some of the COFINA pledge to support the budget). So even with strong monthly numbers recently, sales tax revenues still came in $300 million less than the budget assumed. But on a year-over-year basis, they were close to flat, which is a bit better than I had expected.

The fiscal agency’s release also provides a bit of insight into how Puerto Rico, in a budgetary sense, coped with Maria—

In the end, it didn’t draw on the special credit line Congress authorized FEMA and Treasury to provide for emergency budget support.

But that was in large part because Congress was generous in other ways:

- The supplementary Medicaid funding passed with the disaster relief package provided a little over $400m in budget support

- Special Temporary Assistance for Needy Families (TANF, e.g. food stamps) appropriations provided almost $300m (see p. 7 of the June 29 release)

And well, Federal disaster aid looks to have helped the budget indirectly as well. Gasoline tax revenue (shows up under the “highways” clawback) is up something like $150m (p. 9, line 13 of the June 29 fiscal release). That’s because of all the heavy trucks rumbling around removing debris and the like, and also some of the fuel purchased to run generators. Insurance money fueled a rise in new car sales, and thus auto tax receipts (up $100 million). And Puerto Rico benefited from the extension of the rum tax “cover-over”* too (background); Puerto Rico’s share of U.S. rum tax collections thus exceeded the budget forecast by $80 million (p. 8, line 8).

All in all, tax revenue held up better than I would have expected. And the provision of federal budget aid for health care spending and nutrition—in a context where most debts are not being paid—left the commonwealth government with a comfortable cash cushion.**

That said, Puerto Rico’s short-term recovery wasn’t really in doubt after the Federal disaster aid package passed. And fiscal 2019—which just started—should also be strong (absent another natural disaster). Economies tend to rebound from natural disasters in the short-run, especially with federal disaster aid.

The fiscal plan projects almost $9 billion in recovery spending in fiscal 2019 ($7 billion from the federal government and over $1.5 billion from private insurance, see Exhibit 8), a material sum for a $70 billion or so economy (pre-Maria). And the supplemental Medicaid funding, which directly supports the budget, helped push the consolidation of Puerto Rico’s own budget out into the future.

Basically, if Puerto Rico doesn’t experience strong growth in fiscal 2019 it never will.

The debate around Puerto Rico’s economic trajectory though isn’t really about what will happen this year. It is about what happens when the impulse from federal relief spending fades as federal disaster funding starts to winds down.

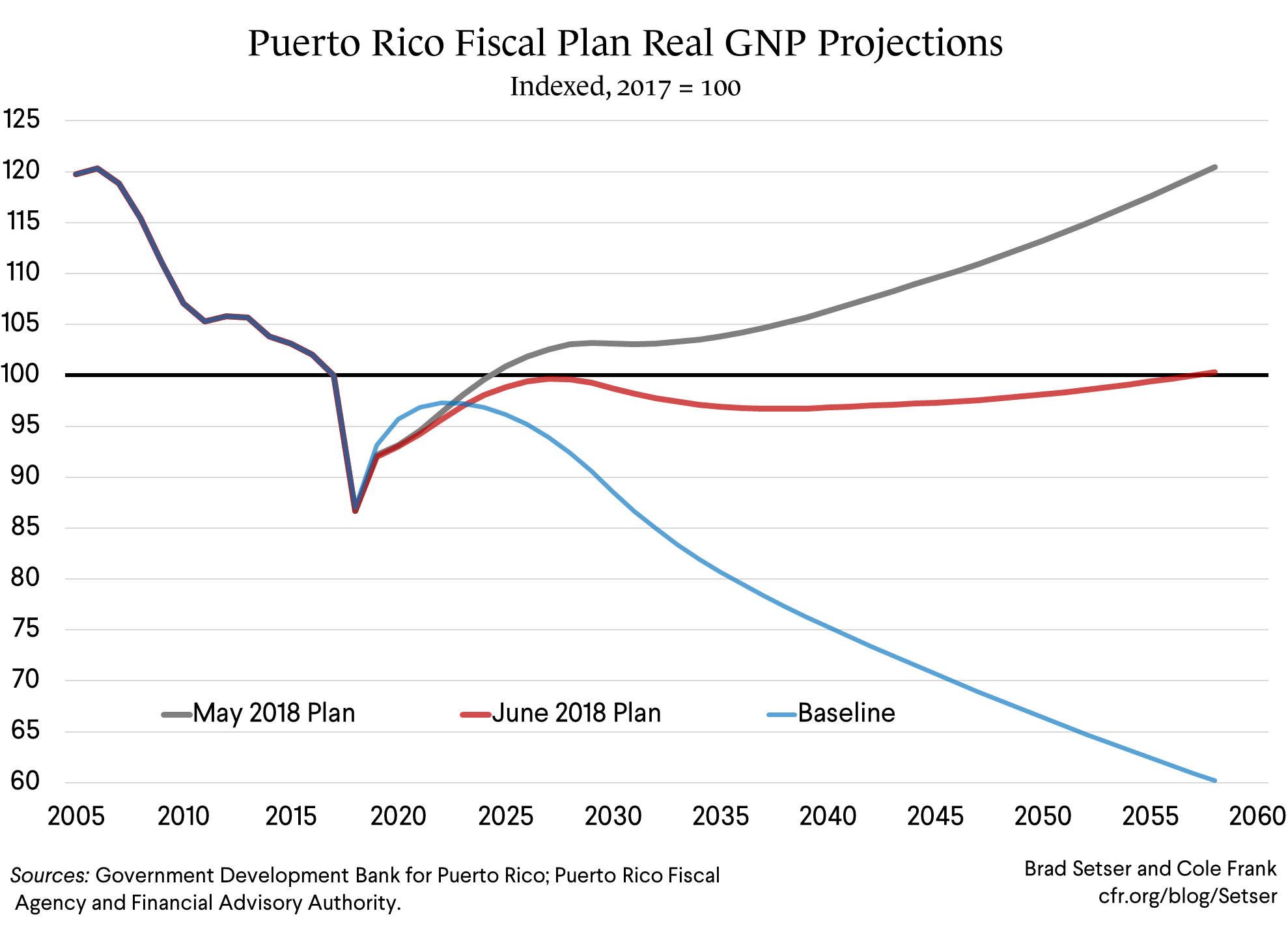

After Puerto Rico’s Senate failed to pass a labor market reform that the board strongly supported, the oversight board has knocked Puerto Rico’s growth forecast for the next few years down—and also lowered Puerto Rico’s projected long-term growth—though it is still forecasting that Puerto Rico will do better than its pre-crisis trend.

The downward adjustment to the baseline growth in the fiscal plan, though, is in my view good news.

I thought the board was overestimating the gains from the structural labor market reform, and thus was at risk of basing its assessment of Puerto Rico’s long-term debt sustainability on an overly optimistic view about Puerto Rico’s ability to grow in the face of ongoing austerity.

The new fiscal plan has a more pessimistic baseline—which in my view is a more realistic baseline.

I suspect we know less about the impact of any given set of structural reforms on growth than many believe. And after the tailwind from federal relief and recovery spending fades, Puerto Rico faces a set of headwinds that could slow growth:

- Over the next few years, Puerto Rico will be engaged in its own form of austerity, as it cuts spending (relative to baseline, see exhibits 3 and 12 of the Fiscal Plan) in order to create budget room to move the cost of legacy pensions fully on-budget (in the past, pension benefits were financed by selling pension assets—but the assets available for sale are about gone and future assets will be built up in segregated accounts to fund future benefits), to prepare for the exhaustion of one-off slug of Medicaid funding provided in the disaster relief bill, and to adjust to the impact of the projected fall in Act 154 revenues.***

- Puerto Rico’s underlying demography gets more challenging over time, as deaths are projected to exceed births, leading to an aging and shrinking labor force.

- The long-run decline of the pharmaceutical industry seems likely to continue, as the new tax reform didn’t provide any new tax breaks for Puerto Rico and it seems likely that Puerto Rico will continue to lose out to other low tax jurisdictions with better infrastructure and less hurricane risk. (Puerto Rico complains about the loss of section “936” federal tax incentives, but even without 936 the pharmaceutical industry in Puerto Rico is offshore for U.S. tax purposes).

- Even with the Puerto Rican earned income tax credit (EITC), Puerto Ricans with children working in jobs earning $20,000-30,000 a year could get a better deal, tax wise, by migrating to the mainland; Puerto Rico’s EITC will provide maybe a quarter of the benefits of the EITC in the fifty states.**** Wages on the mainland are also rising—a strong labor market in Florida acts as a “pull” that will encourage outmigration (fair enough, but it doesn’t help Puerto Rico’s own tax base).

Sum it all up and, in my view, there are substantial downside risks to Puerto Rico’s outlook over the medium and long-term. That’s why I prefer the new Fiscal Plan baseline to the May baseline. The failure of Puerto Rico’s senate to pass the labor market reform in effect gave the board a reason to move away from what I thought was an overly optimistic economic forecast.

No matter.

In the short-run, all signs point to a real recovery— even with an ongoing fight between the governor and the board over the board’s budget authority. The question now is how long it will last. And whether or not the revised fiscal plan (and the Commonwealth Agent’s settlement with the COFINA Agent on the “constitutionality” of the sales tax pledge) will provide the basis for a restructuring of Puerto Rico’s debt that doesn’t get in the way of the recovery.

More on that latter.

* The lack of electricity in more rural parts of the island may have shut down some small bodegas, and shifted sales toward big box retailers where sales tax collection is more reliable, so it isn’t a perfect indicator.

** Puerto Rico needs a cash cushion to operate, as its tax collections historically have been seasonal. Its cash level was also boosted by one last slug of $350 million in pension asset sales this year. But there is no doubt that the overall cash balance is stronger than forecast a year ago, as creditors like to point out.

*** The Board’s economic plan assumes that fiscal cuts have a short-term negative impact on output, but that the drag is temporary. Thus fiscal consolidation is not projected to have any long run impact on the level of output. I believe that there is likely to be more “hysteresis” — e.g. economic weakness today lowers the level of future output as well. The obvious mechanism that would explain this is increased outmigration, as frustrated workers leave. I am particularly worried about the interaction between Puerto Rico’s own austerity and the wind-down of federal aid in a few years.

**** The projected budget cost of Puerto Rico’s EITC is $200 million. A full federal EITC for Puerto Rico would likely cost about $1 billion.