Mobilizing Russia’s Immobilized Reserves

A quick note on the debate over the use of Russia’s frozen reserves.

Concerns over the impact of making full use of Russia’s immobilized reserves, on the reserve status of the dollar and, more importantly, the reserve status euro, always seemed a bit overstated to me.

Reserves-related flows haven’t been driving the dollar or euro for a while now. Most countries that could add to their existing reserves have concluded that they already have plenty and are making more adventurous use of them. The global stocks of foreign exchange reserves are big, true, but current flows are much more modest.

More importantly, the big decision was the initial move to immobilize Russia’s reserves. That action was taken quickly, over a weekend. But I suspect that it mattered more than the current debate over formally seizing the reserves. It made it clear that the reserves of even big countries can be frozen. From the sanctioned country’s point of view, frozen reserves are already gone. President Putin knows he won’t get access to them without backing down.

The big surprise of 2022 wasn’t that the United States froze Russia’s reserves – Russia had already anticipated that risk and diversified out of the dollar.* Rather, the big surprise was that Europe joined the U.S. in applying muscular sanctions, and thus holding euro reserves didn’t offer any additional safety. I have noted (in private conversations) that so long as the countries of the G7 acts together, countries that diversify out of dollars into euros in an effort to reduce their sanction vulnerability effectively give up both yield and liquidity for no additional protection.

When the G7 countries (and the G10 countries, for that matter) act collectively, options for reserve diversification are limited. Holding reserves in Chinese yuan isn’t true protection from “economic coercion” or a full hedge against “weaponized interdependence” – it just creates a different source of vulnerability.

Perhaps most important, though, is the point made elegantly by Colin Weiss in an insightful research paper: if the global reserve pool fractures along geopolitical lines, it probably wouldn’t change much. Would Japan, Korea, Taiwan, and India really want to hold more reserves in yuan given that such reserves could be frozen every bit as easily? Most countries on Europe’s periphery are both aligned with Europe and naturally need to hold euros for their own currency management. China cannot simply diversify its reserves by putting money into China – its real option is holding fewer reserves, not diversification.

The oil-exporting countries of the Gulf are the only big reserve holders with holdings that are somewhat at odds with their geopolitical alignment, and they presumably wouldn’t want to put all their eggs in a Chinese basket. A close examination of the issue points to more modest risks than often implied by breathless headlines around de-dollarization.

But I also understand why European countries are slightly more cautious than the U.S. and Canada. The bulk of Russia’s money is legally trapped in Europe, not the United States. The stakes for Europe are therefore greater.

It is also difficult for the U.S. to tell Europe not to worry about the reserve currency status of the euro when many senior policy makers in the U.S. do cheerlead for the dollar’s global role and sometimes agonize about threats to the dollar’s global position.

But I am also not sure that the G7 has to actually seize the principal to deliver a hefty amount of support for Ukraine.

There are options that don’t require transfer of ownership of existing securities and just use the proceeds from the investment of funds from “frozen” maturing securities, which could yield significant funds for Ukraine.

These options do require legislation, but don’t require formally seizing Russia’s reserves.

According to the Financial Times, the Europeans have already agreed to have the holders of the identified frozen reserves (Euroclear and perhaps other security depositories, including those run by national central banks?) hold the proceeds from Russia’s maturing securities in segregated accounts:

“Under the agreement struck on Monday, profits generated by Euroclear will be booked separately and not be paid out as dividends to shareholders until EU countries unanimously decide to set up a ‘financial contribution to the [EU] budget that shall be raised on these net profits to support Ukraine’”

Russia’s reserves generally were invested in relatively short-term securities, and when the immobilized securities mature, the funds roll into zero- or low-interest deposit accounts. They thus become – absent other guidance – a free source of financing for the institution that previously held the reserves.

We know this because Belgium reported a windfall profit from its ordinary income tax levied on Euroclear’s bank, which saw its profits soar as it made use of this free funding. See Martin Sandbu’s detailed examination of the issue.

To generate real funds for Ukraine without formally seizing the assets, I think Europe needs to do two things:

- Direct institutions with essentially unclaimed funds from the maturing securities held in frozen accounts to invest those proceeds for income, not for liquidity (the funds are, after all, frozen).

- Introduce a very high (say 99.9 percent) tax on the interest income of all frozen reserves held in segregated accounts for immobilized reserves.

The size of the frozen reserves hasn’t been authoritatively determined. $300 billion is a sum that is often tossed around; Martin Sandbu says the right number is $350 billion at the time of the seizure, though that will be a bit lower now thanks to currency moves. The Financial Times reports the European Union is using a slightly smaller number – €260 billion, with €190 billion of that held in Euroclear (a rather stunning fact in itself). That number, ironically, will include a portion of Russia’s reported dollars, as Russia held around $16 billion of its dollar securities in a Euroclear custodial account.

But for the sake of argument, let’s assume the real number across the G7 is around $300 billion. That portfolio, conservatively managed, should generate interest income of at least $10 billion a year. The dollar portfolio can be held in bills (5.25 percent), or higher yields can be locked in by investing in Agencies (6 percent plus). The euro portfolio would be invested in the interbank market (at close to 4 percent now), or in Spanish government bonds at 3.15 percent. A portfolio that includes a mix of Spain, Italy (why not), and the euro-denominated bonds of the European supra-nationals and multilaterals like African Development Bank (AfDB) would easily lock in a 3 percent return over time. The blended yield, including the proceeds on the dollar portfolio, should be a bit over 3 percent.**

This hypothetical portfolio also only includes assets that would normally be part of the investment tranche of a standard reserve portfolio: emerging market and corporate bonds would generate a higher yield. Remember, this portfolio doesn’t need to be managed for liquidity.

The €4 billion sum that the European Commission has suggested could be generated off the proceeds of the frozen reserves (per the Wall Street Journal) seems substantially too small; I consequently hope that the G7 countries are pushing the Europeans on this.***

$10 billion a year over multiple years is real money – so treating the frozen reserves as an endowment and only using in effect the income on the estate’s frozen assets generates a guaranteed $50 billion over 5 years. Ukraine needs more, but it is a start – and all this can be done in a way that only uses the windfall that would currently accrue largely to the institution that happens to be holding the frozen security when it matures. It should be all legally pretty straightforward.****

The frozen assets themselves wouldn’t actually ever be seized – the principal would remain frozen, notionally owned by Russia and available to sweeten any eventual settlement. And the interest income would technically be taxed away rather than seized. Large taxes on intangible income have ample precedent, so prohibitively high taxes on the intangible income from frozen accounts actually seem fairly easy.

Bottom line: there should be real money on the table even if the principal on Russia’s immobilized reserves isn’t seized. $10 billion a year is, in reality, probably a bit conservative… and $10 billion a year is over 5 percent of Ukraine’s GDP.

That isn’t a small sum – especially when any negotiated settlement likely would include liberating additional funds to pay for Ukraine’s reconstruction. And the option of doing more remains.

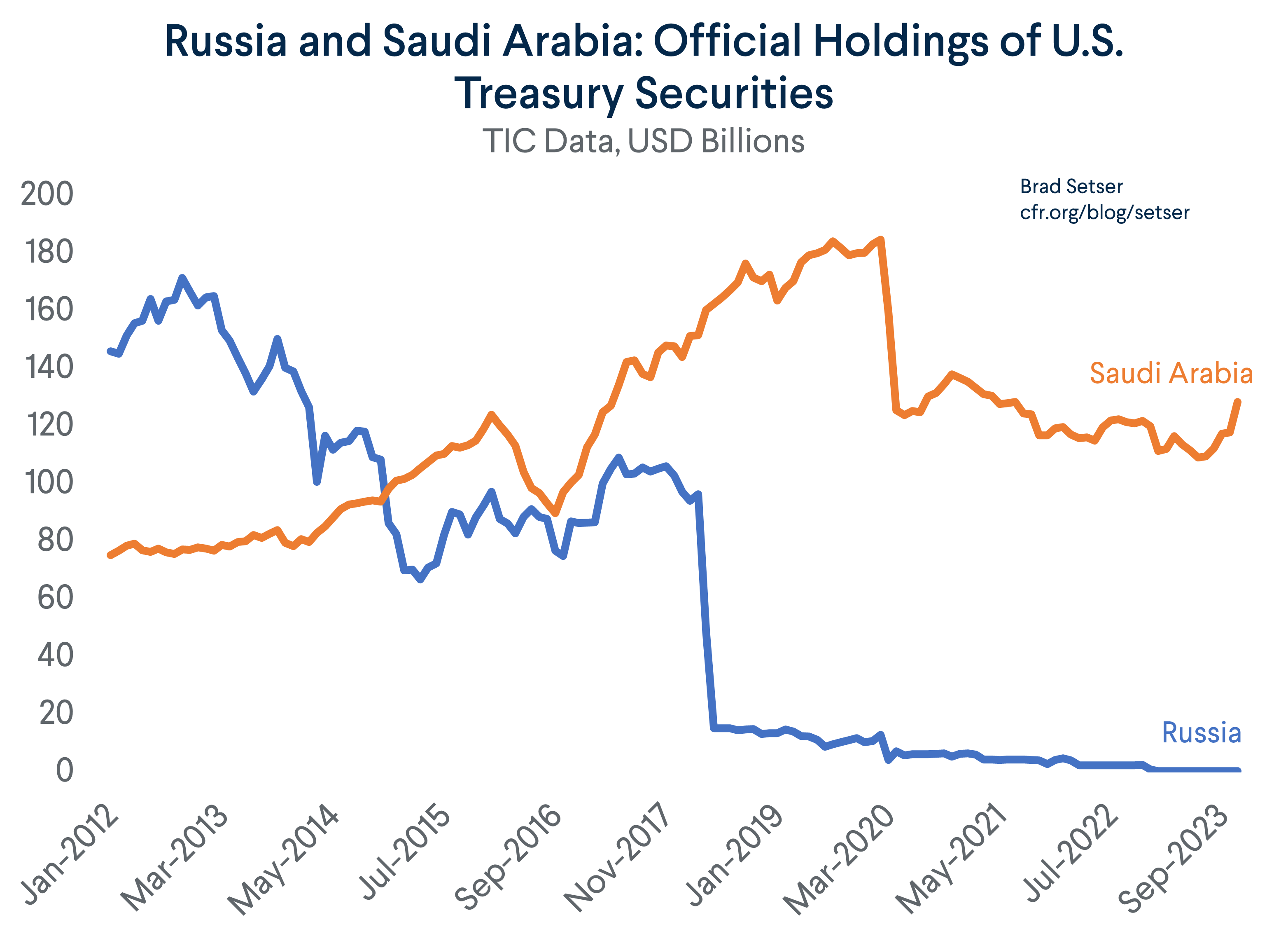

* Russia’s reported holdings of Treasuries with U.S. custodians fell sharply in spring of 2018, dropping from $96 billion to $15 billion. That coincided with a fall in the dollar share of Russia’s reserves from around 40 percent to around 15 percent.

** Several very safe Euro-denominated ten-year bonds yield just under 3 percent: AfDB (2.58 percent), European Stability Mechanism (2.69 percent), European Investment Bank (2.73 percent), NextGeneration EU (2.6 percent). To get an overall yield of over 3 percent the mix would need to include Spanish (3.15 percent) and Italian sovereign bonds (4.43 percent).

*** The €4 billion sum seems to stem from Euroclear’s 2023 windfall profit on the €191 billion of frozen Russian reserves (“Euroclear’s overall net interest earnings jumped to €5.5bn in 2023 from €1.17bn in 2022, according to its yearly results, with the bulk of it related to Russian assets”). That profit should automatically rise as more and more of Russia’s frozen securities mature and roll over into zero interest deposit accounts -- and it also helps that European rates increased over the course of 2023. Euroclear though is only 2/3rds of the total stock of Russia’s reserves, so their should be additional funds -- and, as I noted in the blog, there is no reason why the funds in these deposit accounts couldn’t be invested in ways to lock in a bit more income over time.

**** I am not a lawyer of course, but I think I have a reasonable sense of what is possible from some past work on related issues.