MeetingA New Wave of Foreign Assistance: Innovative Financing and the Power of Commercial DiplomacyApril 16, 2026

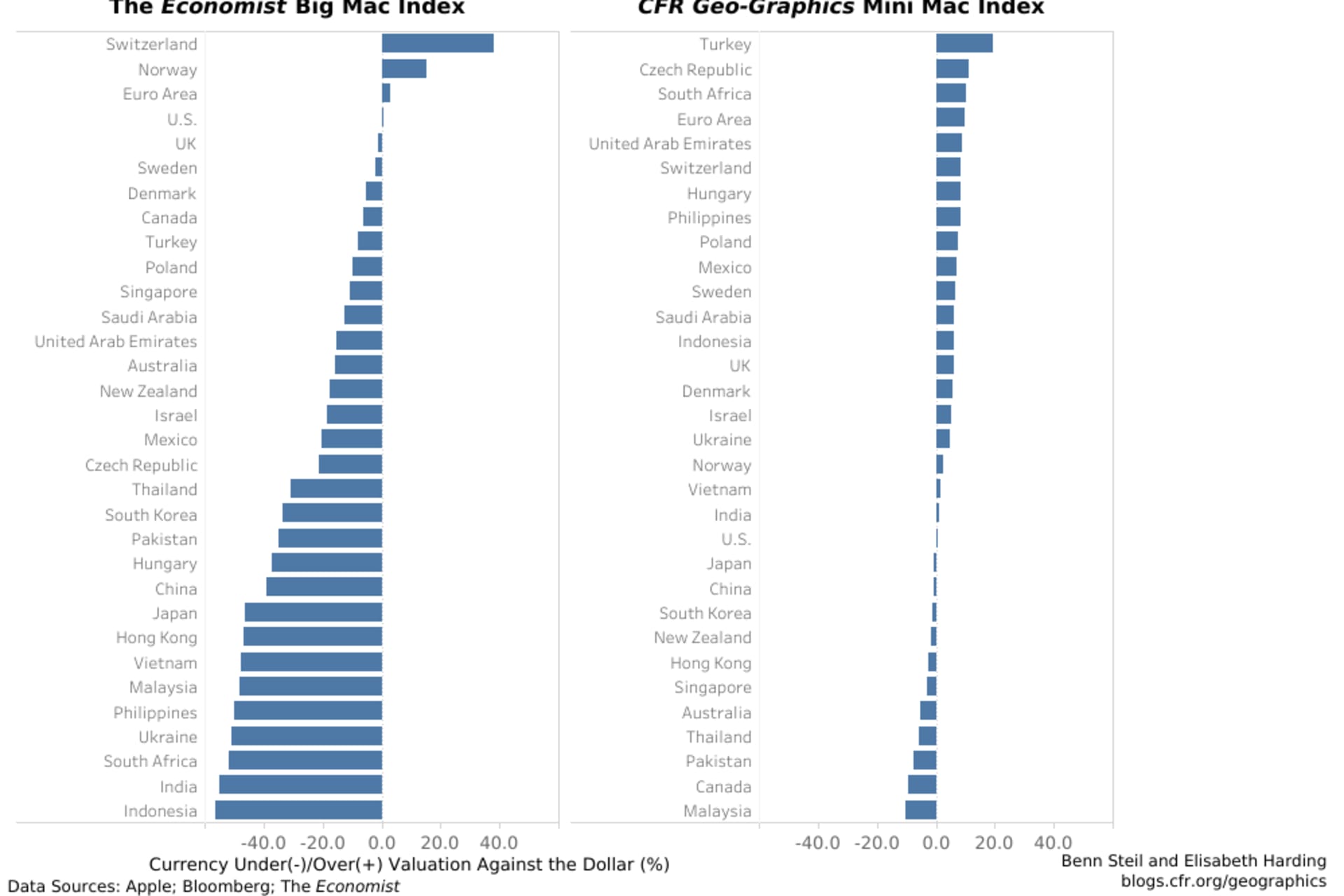

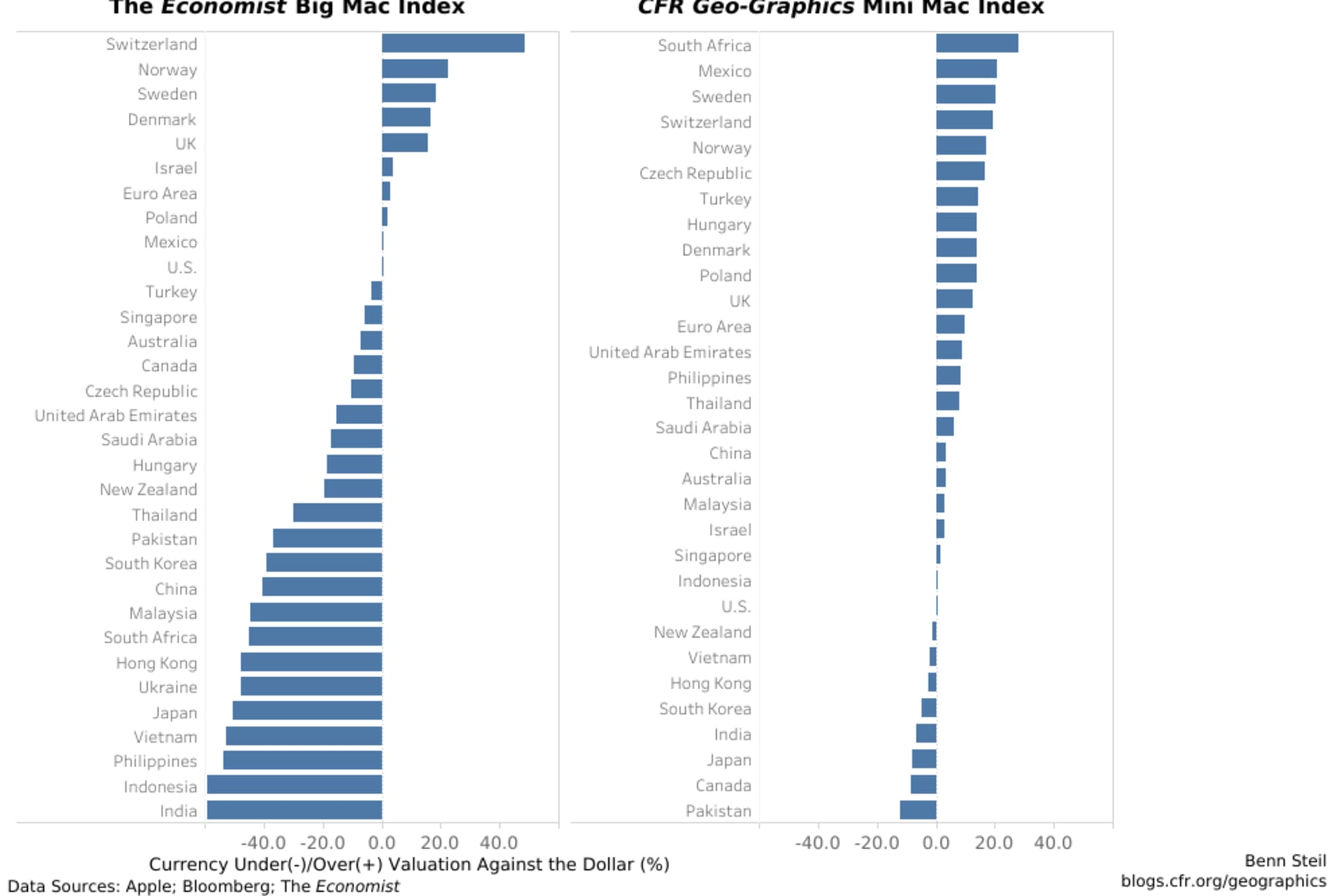

CFR Mini Mac Index Shows Dollar Weakening in Trump's First YearMarch 11, 2026By Benn Steil and Yuma Schuster

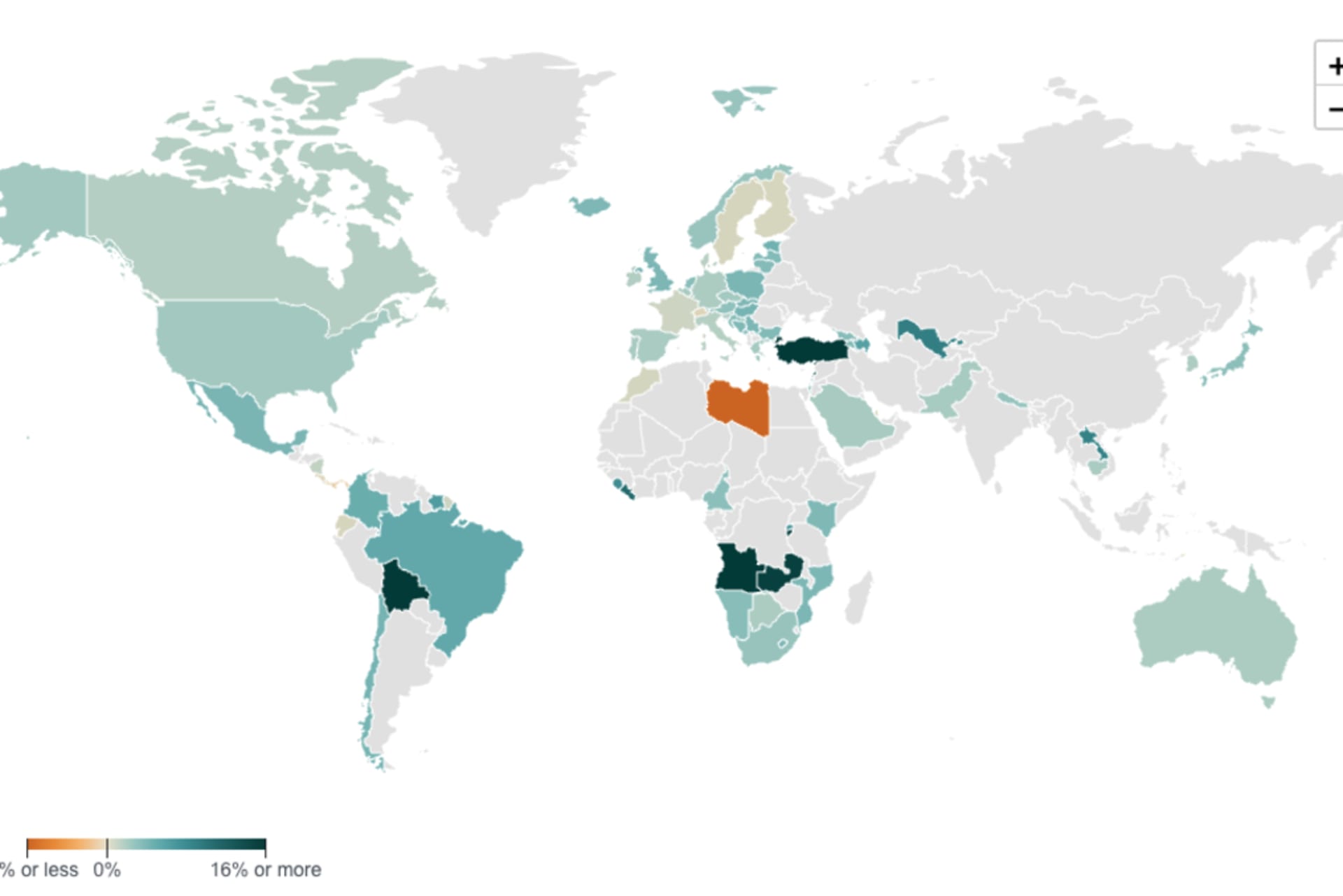

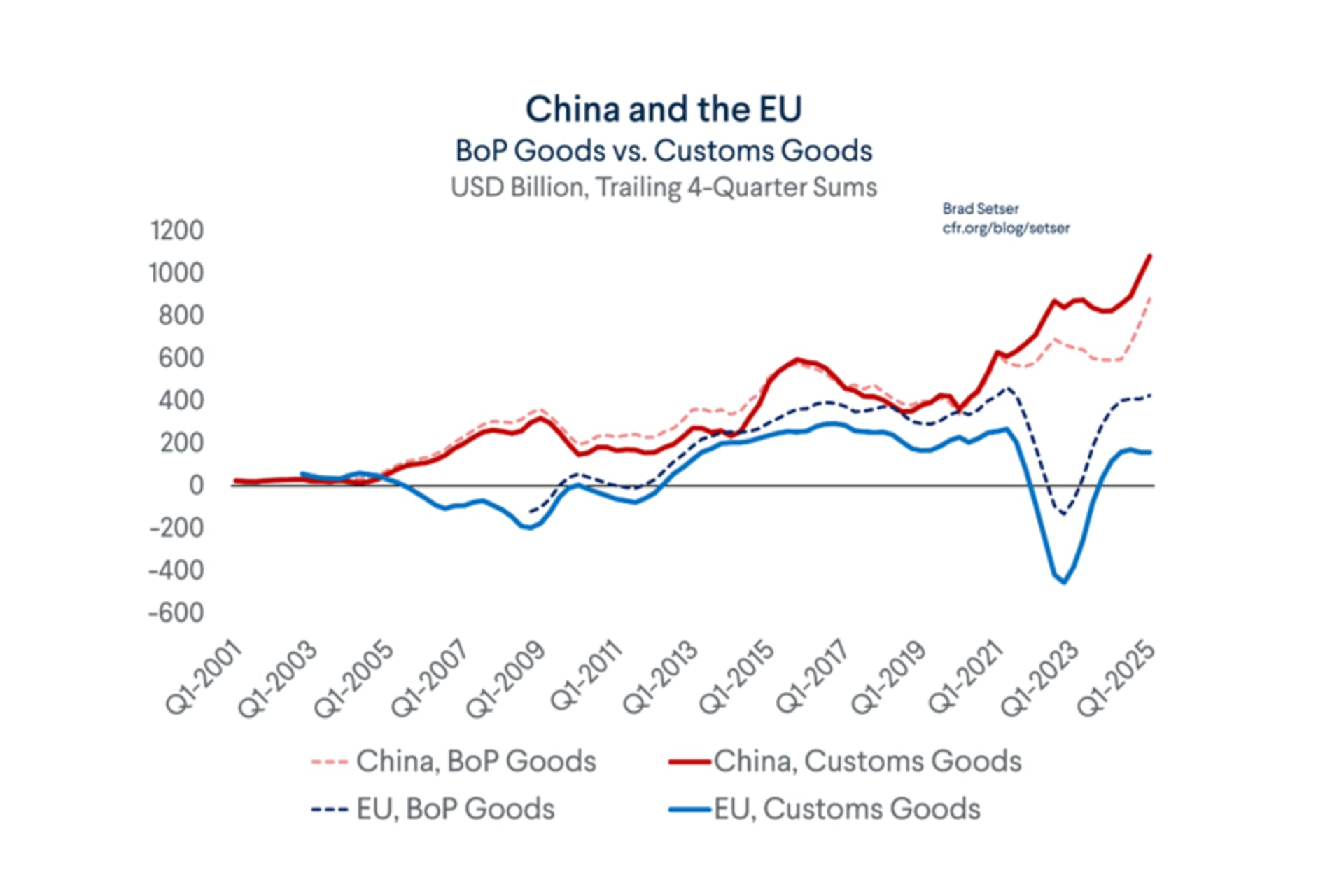

China’s Massive Surplus is Everywhere (Yet The IMF Still Has Trouble Seeing It Clearly)November 12, 2025By Brad W. Setser

Rebalancing China’s Economy: Stimulus, Confidence, and Self-SufficiencyJanuary 23, 2025By Zongyuan Zoe Liu

Expert Take

Expert Take

Meeting

Meeting

Video

Video