Official Investors and the Eurozone Debt Market

The share of Treasuries held by official investors—foreign central bank reserve managers as well as the Fed—has been going down in recent years. But the share of Eurozone bonds held by official investors is soaring, and could now be approaching 50 percent of central government debt. With the ECB holding a rising share of a shrinking stock, there aren’t enough German bunds around to meet reserve demand.

Back before the financial crisis, “official” investors—meaning the reserve managers of foreign central banks—played a big role in the Treasury market. There were years when dollar reserve growth far exceeded net new Treasury issuance. Ben Bernanke, among others, thought this had an impact on the term premium, and thus helped hold down the yield on long-term Treasuries. Others argued that these inflows freed up U.S. funds to search for yield in riskier fixed income assets—Americans sold short-term bills to a foreign central bank and placed the funds in a money market fund that lent to a European bank that bought riskier long-term paper; American fixed income fund managers moved out of Treasuries and Agencies and into riskier private label mortgage backed securities.

The role of official investors in European government bond markets during the era of super-strong global reserve growth never attracted as much attention, in part because there is no real European equivalent to the detailed U.S. TIC data. But it should get a bit more attention. The combination of ECB buying, higher global reserve holdings (and an associated need for reserve managers to hold more euros), and relatively restrained Eurozone government bond supply could be having an important impact on the Euro-denominated bond markets.

Prompted by a question from Jamie McGeever, I tried to estimate just how many Eurozone bonds are now in the hands of the ECB and global reserve managers.

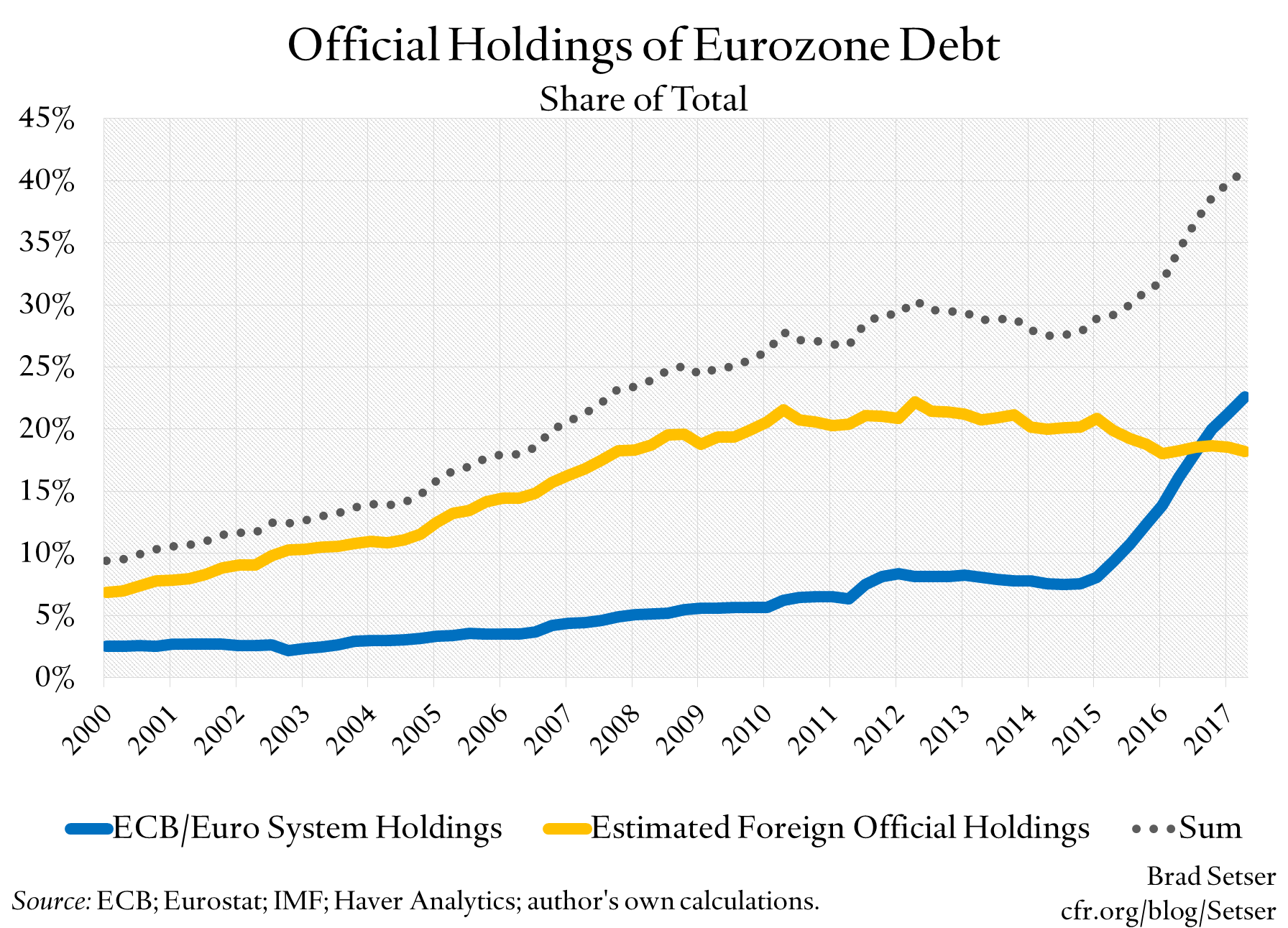

To cut through the chase, the answer is probably well over 40 percent of the stock of general government debt. That’s comparable to the total share of Treasuries now held by the Fed and foreign reserve managers. And, well, there has been far more of a change in Europe than the United States.

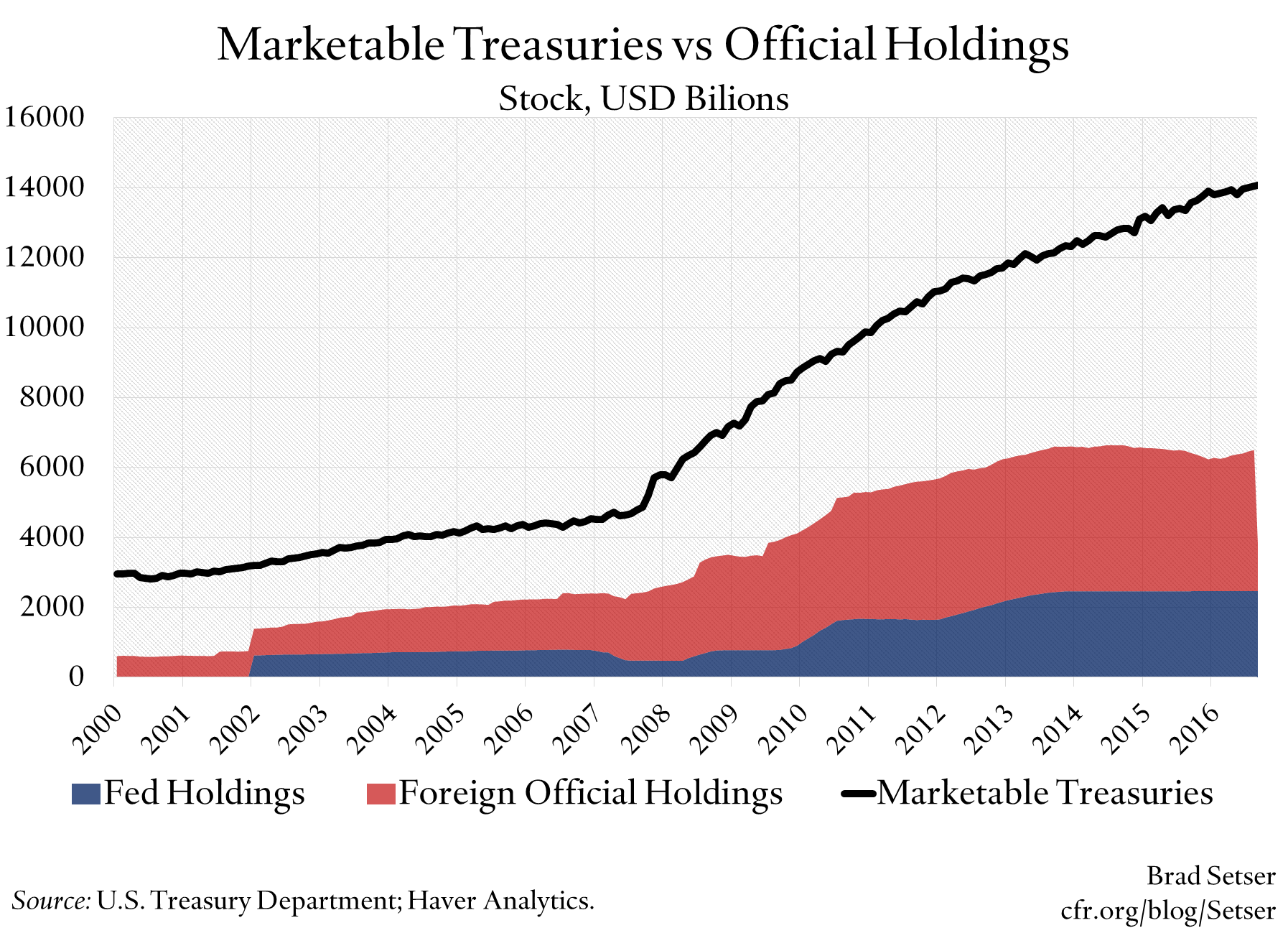

Here is a plot of “official” holdings of Treasuries—both the Fed’s holdings and the holdings of foreign central banks—relative to the total stock of marketable Treasuries.

As a share of the stock, official holdings are now at a ten year low (sort of surprising)—thanks to a growing stock of Treasuries and a levelling off of demand from foreign central banks in the last few years. And now the Fed is poised to start reducing its holdings (for a great summary of the estimated impact of the Fed’s rolldown, see Joe Gagnon in the Wall Street Journal, or this Fed note).

The Europeans don’t produce an estimate of official holdings of Eurozone government bonds, at least not one that I have found (foreigners are reported to hold around euro 2 trillion of euro-denominated government bonds, but I didn’t see a private/ official split in the net international investment position).

And the IMF’s data on the currency composition of global reserves still has some important gaps (not everyone reports the currency composition of their reserves). But on the assumption that the currency composition of the reserves of the countries that do not report their currency composition to the IMF matches the currency composition of those who do*, and on the assumption that about 75 percent of euro-denominated reserves are invested in the government bond market, one can roughly estimate official holdings.

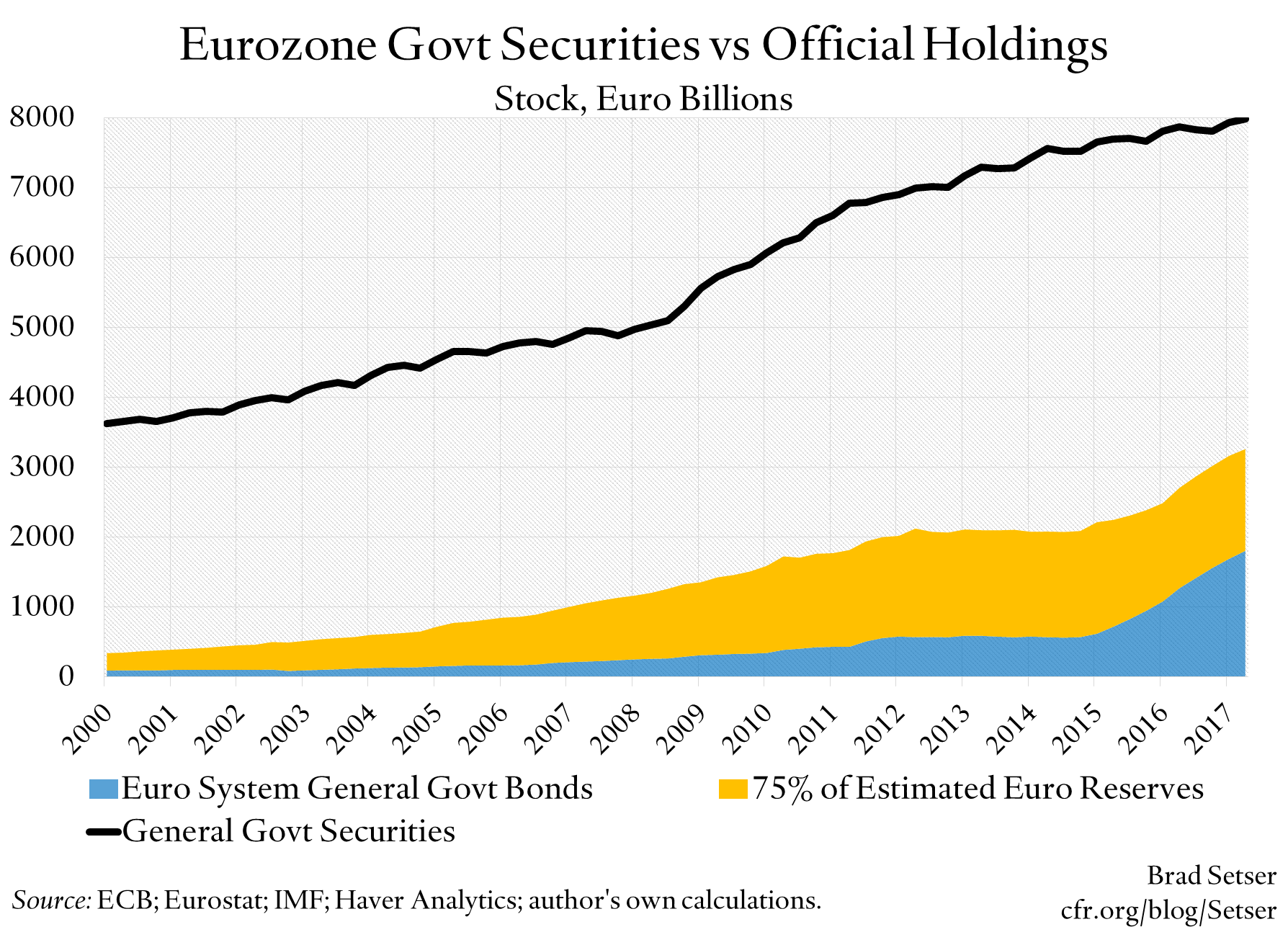

Total reserves globally aren’t going up that fast anymore, so estimated euro reserve holdings aren’t rising. But ECB purchases are rising fast—so the stock of bonds left for the private market is falling.

Official holdings are now over 40 percent of the outstanding stock of the stock of all eurozone government debt, and would be closer to 45 percent of the stock of all central government debt. That’s sort of normal for the U.S. Treasury market, but something new for the Eurozone bond market.

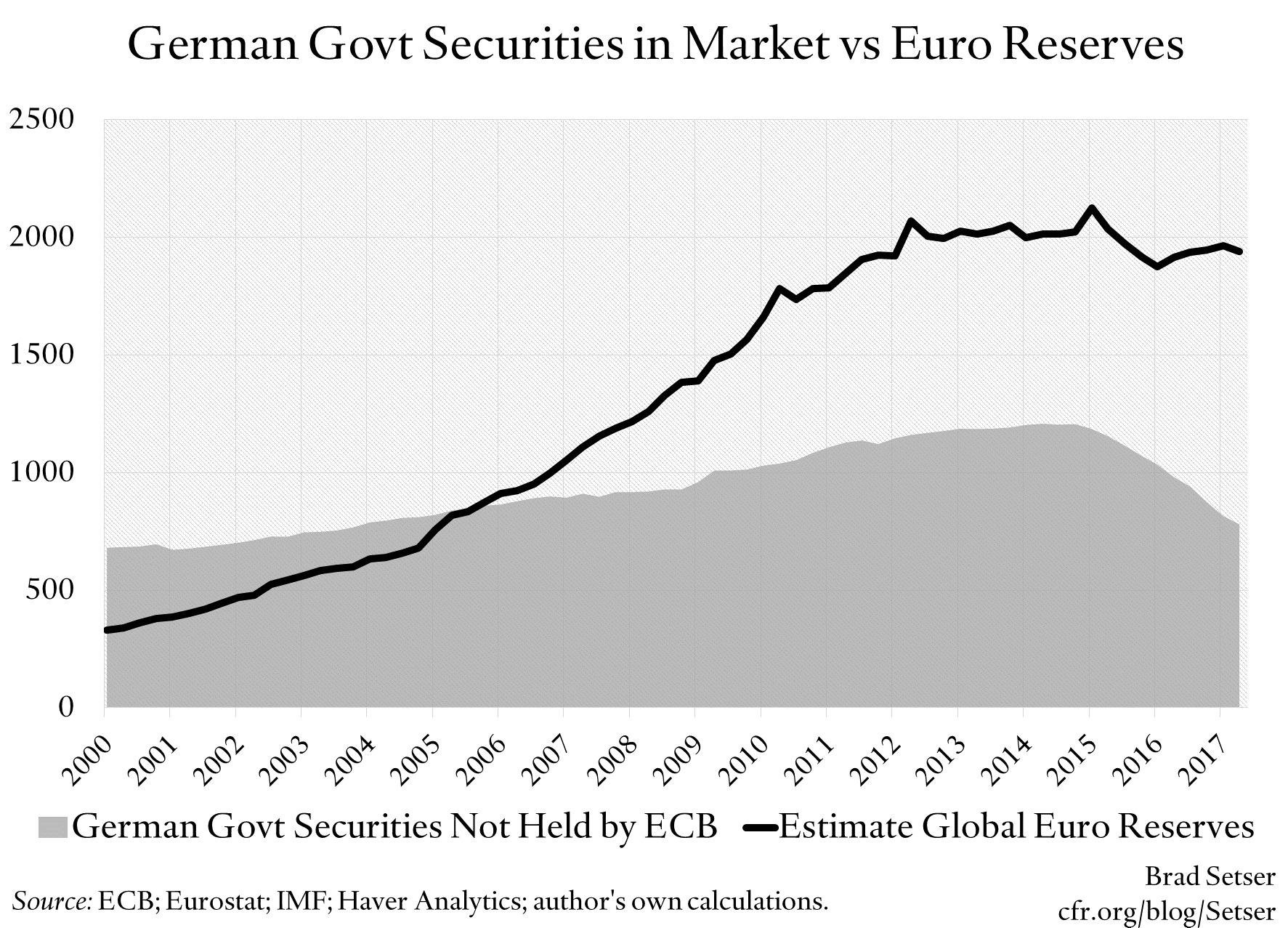

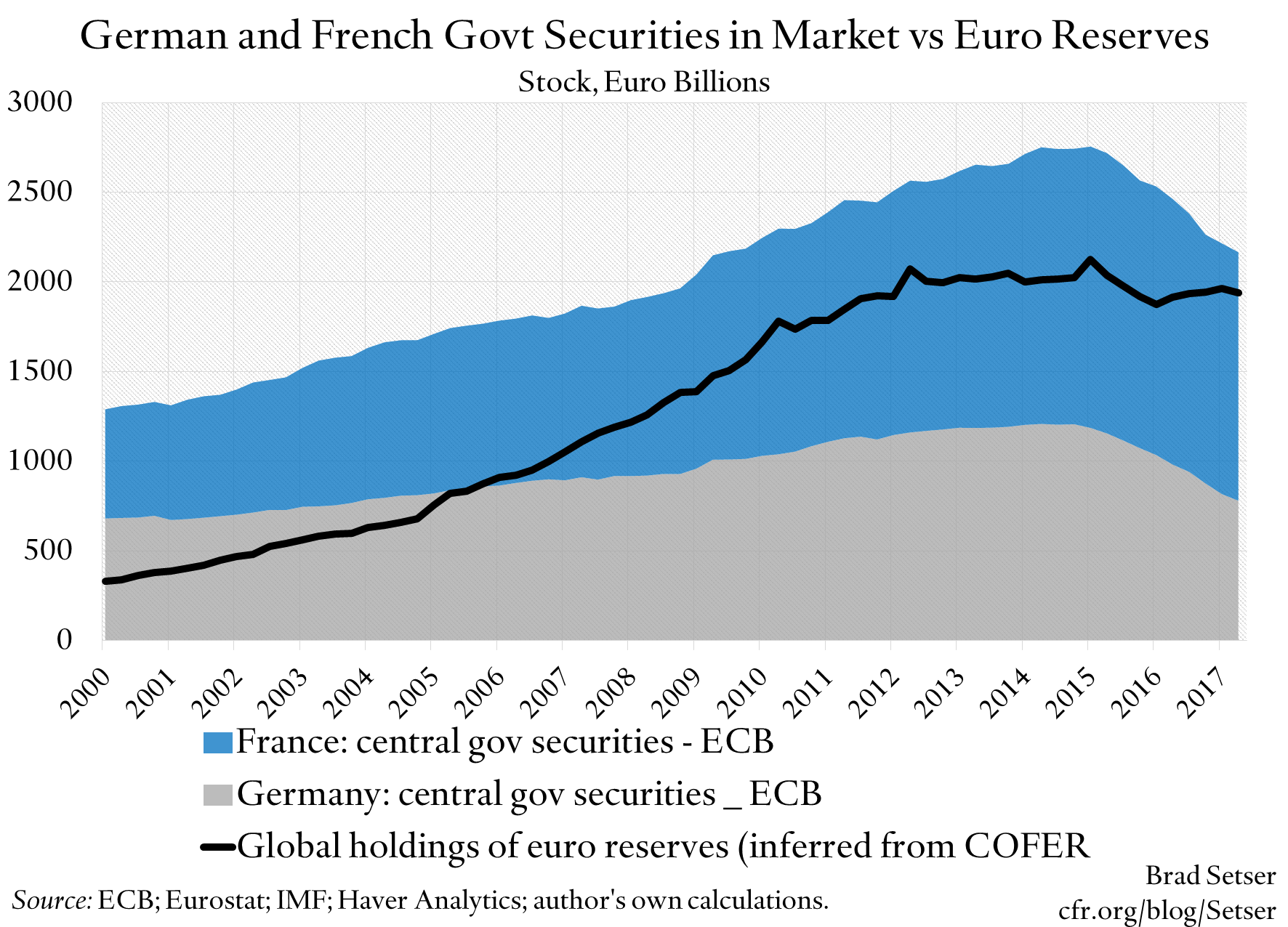

And there is another interesting angle on all of this: compare the stock of German central government bonds that are not held by the ECB to the estimated stock of Eurozone reserves. The supply of Bunds doesn’t come close to meeting reserve demand.

Foreign reserve managers that have a fixed allocation to the euro are almost always forced to hold other countries’ government bonds as reserve assets.

Or to put it differently, by failing to supply enough safe Eurozone reserve assets, the Germans have effectively encouraged reserve managers to hold more French government bonds!

p.s. It would be fun to see how Eurozone reserve portfolios are allocated across Germany, the Netherlands, France, Italy, and Spain—maybe that’s possible with nationally disclosed data? I haven’t tried. A challenge for The General Theorist?

* China reports the currency composition of a part -- but not yet all -- of its reserves to the IMF. It is phasing in full reporting so as to avoid revealing too much information about the currency content of its reserves. Unfortunately, as part of its deal with China, the IMF stopped reporting the split between emerging economy and advanced reserves, which radically reduced the information value of the COFER data. It was actually more useful when China wasn’t reporting, as it didn’t take too much work to infer the portfolio of the non-reporting emerging economies (China and Saudi Arabia were the most important).