Puerto Rico Before Maria

My new discussion paper with Greg Makoff on economic and demographic trends in Puerto Rico.

Even before Maria, Greg Makoff and I worried that Puerto Rico’s fiscal plans were built on overly optimistic assumptions.

Overly optimistic assumptions about the ability of an already weak economy to handle a wave of austerity after the pensions are depleted and the ACA funds are exhausted.

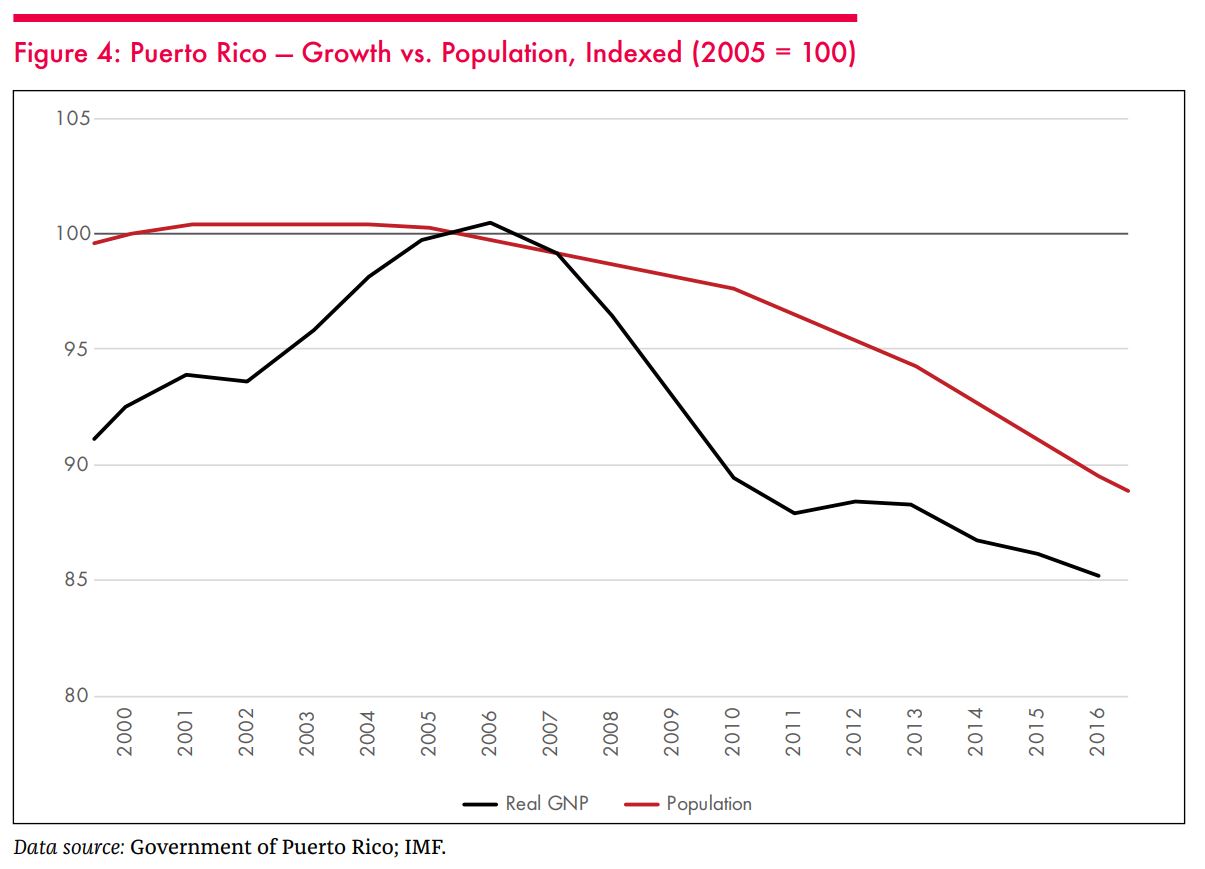

And overly optimistic assumptions about the willingness of Puerto Ricans to stay on-island while Puerto Rico’s economy continued to decline. The island’s pre-Maria fiscal plan assumed, implausibly, that outmigration would stop even as the economy shrunk.

That, more or less, is the elevator summary of my new paper with Greg Makoff of the Center for International Governance Innovation (CIGI).

It was written before warm waters in the Atlantic spawned a series of category 4 and 5 storms, and before one of them crossed through Puerto Rico with devastating force. It looks backward far more than it looks forward. It isn’t a guide to most of the policy issues that the Trump Administration, the Congress, the Governor, and the Oversight Board will need to work through as they try to chart a path forward for Puerto Rico.

It does though offer a data-based review of what has happened to the island’s economy and population in the past ten years.

A few points of interest:

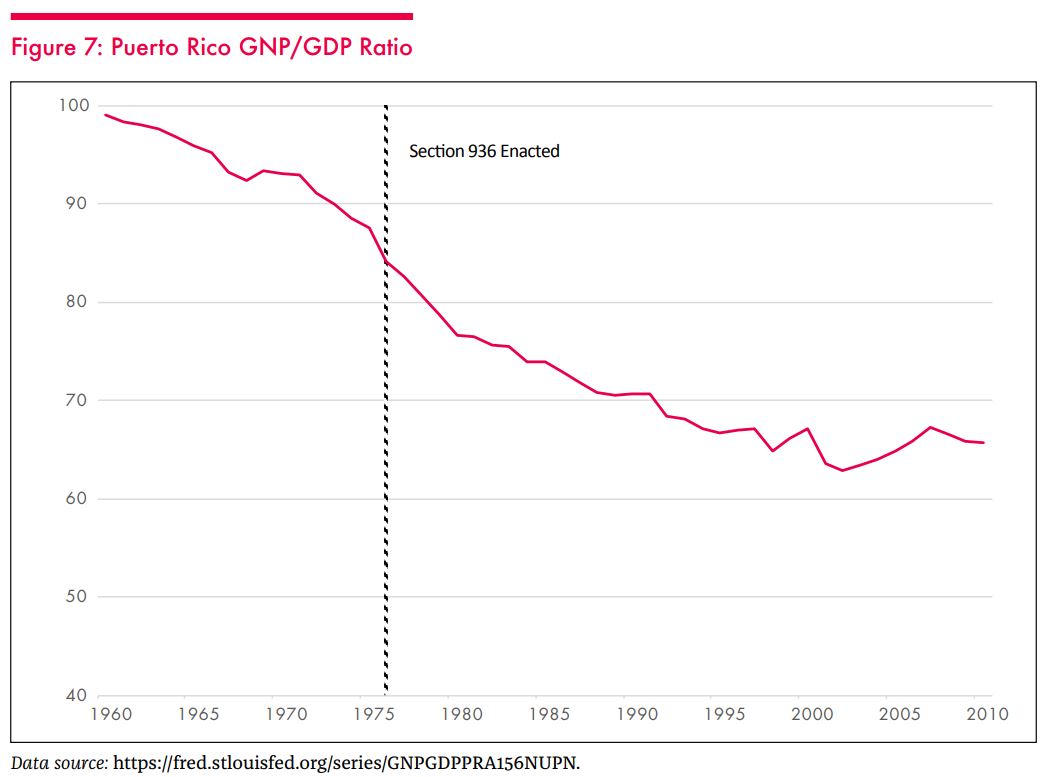

1) The correlation between the final expiration of section 936 of the tax code (an infamous tax break that encouraged pharmaceutical production in Puerto Rico by providing firms an even better tax deal than they now get in Ireland, or for that matter, still get in Puerto Rico) and the start of Puerto Rico’s slump may be a bit deceptive. The pharmaceutical sector in Puerto Rico may be less dynamic than it was previously, but the industry didn’t pick up and leave Puerto Rico after the end of “936.” Profits “earned” in Puerto Rico are still legally offshore, and thus tax on them can be deferred. If you want a super technical indicator that suggests the ongoing presence of the Pharma sector, take a look at look at the gap between Puerto Rico’s GDP and GNP: the difference is correlated with the transfer pricing that helps the pharmaceutical sector and Microsoft move a portion of their profits offshore.*

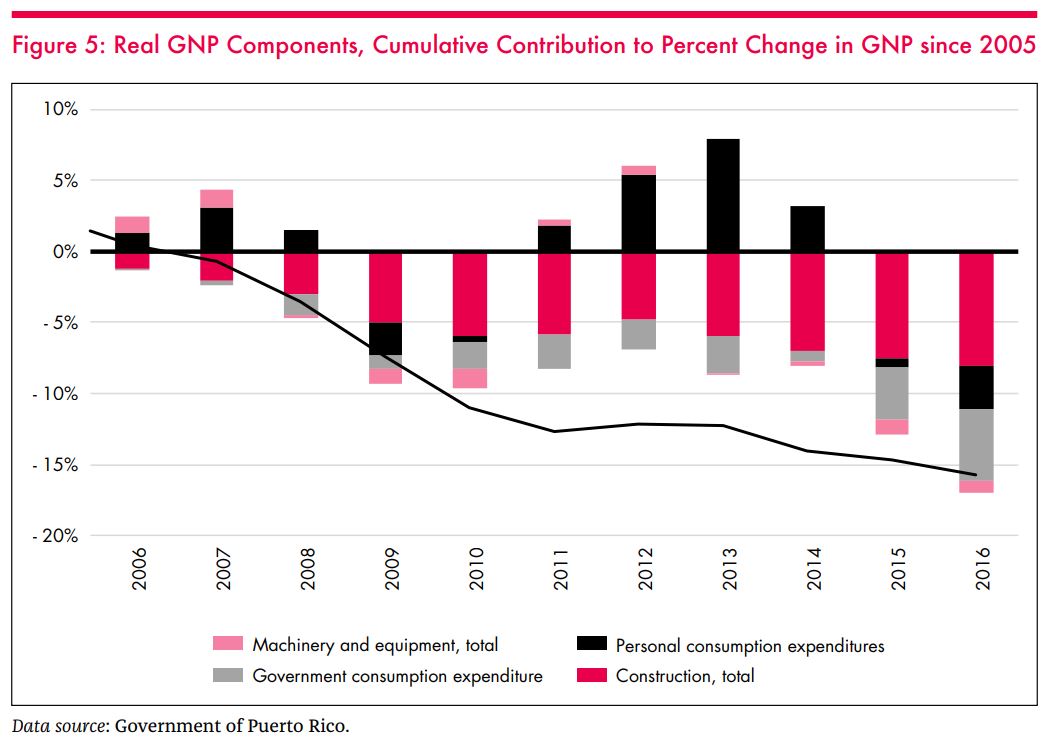

The proximate cause of the 2006 slump was the bursting of a property bubble, which devastated the local banks and led to a very large fall in construction employment. I think Daniel Gros of CEPS got this right. Puerto Rico experienced an intensified version of Florida’s housing and real estate driven crisis, but unlike Florida, it never recovered.

If you look at the real GNP data, the downturn in property investment (construction) explains far more of Puerto Rico’s slump than a downturn in business investment in plant and equipment, which captures the capital-intensive pharmaceutical sector to a significant degree.

2) While “936” didn’t cause the post 2006 slump on its own, Puerto Rico is a manufacturing intensive-economy and it has been hit by many of the same factors that led to trouble in other manufacturing heavy parts of the U.S. economy.** Construction initially helped make up for jobs that were being shed in the traditional manufacturing sectors (electronics assembly for example) in the first part of the 2000s, but when the property boom turned to a deep bust, there wasn’t much to fall back on. Puerto Rico in some sense can be thought of as part of the manufacturing belt in the American Southeast. It experienced a pre-globalization manufacturing boom in the 1960s—as Puerto Rico is inside the U.S. for trade purposes but not for tax purposes, more or less, and it offered the lowest labor costs inside the U.S. And like other manufacturing heavy regions, it has struggled to manage the shocks that have come both from technological progress that generates an ongoing reduction of the need for labor (in the pharmaceutical sector) and greater global competition.

3) Austerity probably hasn’t been the main reason why Puerto Rico failed to recover from its construction boom and bust. This sort of surprised me to be honest, as Puerto Rico’s downturn was both large and persistent and I sort of thought austerity helped it along. But it is the conclusion that I think emerges from the numbers.

So why wasn’t there initially a self-reinforcing cycle of decline and austerity, which led to more decline and then more austerity?

- Puerto Rico was able to borrow in the traditional municipal bond market until 2012, and then raised one last slug of expensive financing in 2014 from a consortium of non-traditional investors. It also supplemented the financing generated by borrowing by drawing on the assets of the pension fund to pay current benefits in an unsustainable way (the pensions are now out of assets, and have substantial future liabilities). That dug Puerto Rico in a deeper hole financially—but helped it defer cutting back on public spending or raising taxes from 2007 to 2014.

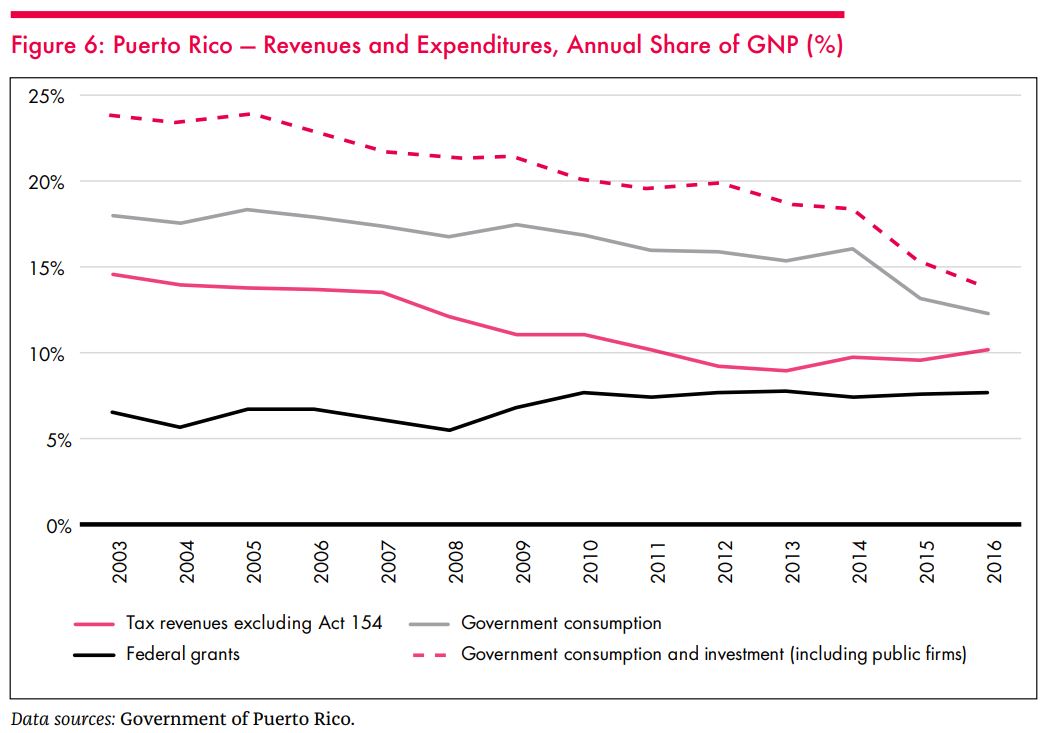

- Puerto Rico received significant new funds from the Obama Administration. The “stimulus” of course. And even more so funds from “Obamacare” (the Affordable Care Act). This is easy to document statistically: federal transfers jump absolutely, and as a share of Puerto Rico’s GNP (chart below).

- Puerto Rico cut domestic taxes significantly in 2011-12, so the net fiscal impulse isn’t obviously negative even with significant cuts in public investment. The domestic tax cut though doesn’t leap out at you if you look only at the aggregate revenue numbers—to understand it, you need to know a fair amount of institutional detail. In 2011, Governor Fortuno cut personal income taxes fairly significantly, which clearly shows up in the income tax revenue numbers. But the fall in revenues was offset by Act 154—a tax on the turnover (a la Macron?) of the big multinationals operating in Puerto Rico. For now, pending final ruling by the IRS, it is fully creditable against U.S. corporate income tax, so it is probably best understood as a backdoor fiscal transfer through the tax system. It certainly isn’t a tax that is born by domestic labor or by domestic firms.

Act 154 and Obama era policies effectively provided Puerto Rico’s government with funding of close to 5 percent of its GNP from 2009 to 2013. That helped offset the fiscal impact of ongoing economic decline.

Puerto Rico’s lack of dependable fiscal numbers—and skill at disguising debt payments to help skirt the constitutional limit on debt service to revenue—makes calculating the real fiscal impulse difficult.

But if my interpretation of the available numbers is right (higher transfers and lower taxes offset the fiscal drag from a fall in public investment so there on net wasn’t much austerity before the 2015 sales tax hike and associated fiscal tightening) it only highlights the difficulties Puerto Rico faces getting its economy going.

Put it this way: even with a decent amount of federal support through both the frontdoor (the ACA) and the backdoor (the federal tax treatment of Act 154), Puerto Rico wasn’t able to pull out of its post-property boom economic decline. That decline continued even with more government-financed health care and lower domestic taxes, including low taxes on investment income (i.e. with the implementation of policy ideas associated with both the Democratic and Republican parties).

Greg and I expected the new fiscal consolidation that was built into the (pre-Maria) budget to trigger a new downturn. And we thought that downturn would lead to more outmigration—which in turn would reduce Puerto Rico’s scope to recover. In the jargon, it would lower Puerto Rico’s economic potential—not just pull output temporarily below potential. Put simply, it means Puerto Rico’s economic plan—and debt restructuring—needs to be built on the assumption that output will be permanently lower.

And the available evidence from hurricanes seems to be that they tend to lower regional output—post hurricane growth tends to be lower than pre-hurricane growth. The short-term boost from rebuilding tends to fade.

The only potential positive is that Maria may catalyze a broad reconsideration of federal policy toward Puerto Rico. PROMESA provides tools to manage Puerto Rico’s legacy debt, tools that in my view are stronger than is commonly realized. But without other policy changes, lifting much of the burden of the legacy debt will not be enough to catalyze a recovery.

* I feel I am at risk of becoming a bit shrill on the topic of tax and trade, but it is very hard—in my view—to understand a lot of the trade data without understanding how heavily a lot of trade is influenced by what might be termed chains of tax arbitrage that have nothing to do with conventional tariffs. The trade flows linked to such tax arbitrage are in my view why the U.S. runs a large trade deficit in pharmaceuticals overall, and why most of the deficit is with places like Ireland and Switzerland. And the U.S. would technically run a trade deficit with Puerto Rico if Puerto Rico were disaggregated from the U.S.—even though the ships that sail from the U.S. to Puerto Rico sail to Puerto Rico full and come back almost empty. Welcome to the world of transfer pricing!

** The dot-com boom was actually pretty good for domestic manufacturing, as at the time electronic capital goods were made in the U.S. and—with low oil prices—U.S. vehicle demand shifted toward heavier U.S. made-SUVs. The bursting of the investment bubble at a time when the dollar was super strong though hit the manufacturing sector hard—the manufacturing job losses in the 2000 recession were exceptionally large, and manufacturing employment never fully recovered.

Note: the last sentence of the second footnote was edited after publishing; I initially left out “never.”

Full Disclosure: I worked on Puerto Rico while at the U.S. Treasury in 2015.