The Oversight Board’s Latest Fiscal Plan for Puerto Rico is Still Too Optimistic

The power is off in Puerto Rico, again. It may not be restored for a day or two.

Puerto Rico obviously has yet to fully recover from Maria’s devastation. Tax revenues this fiscal year are off by over $800 million—or about 10 percent. Sales tax revenues are about 30 percent below forecast (pg. 7, line 3).

The fall overstates the underlying fall in activity—as a group of bondholders (for now) has first claim on a portion of the sales tax (until the funds needed to cover payment on the bond are set aside). As a result, the risk of any shortfall in sales tax proceeds is born almost entirely by Puerto Rico’s Treasury. The impact of that pledge shows how Puerto Rico’s debt still complicates Puerto Rico’s recovery.

Tax revenues for Puerto Rico’s fiscal year will be something like $1 billion less than forecast—perhaps a bit less than some feared immediately after Maria, but still a substantial shortfall. It is all, more or less, consistent with an economy expected to fall by a bit more than ten percentage points (in real terms) this year.

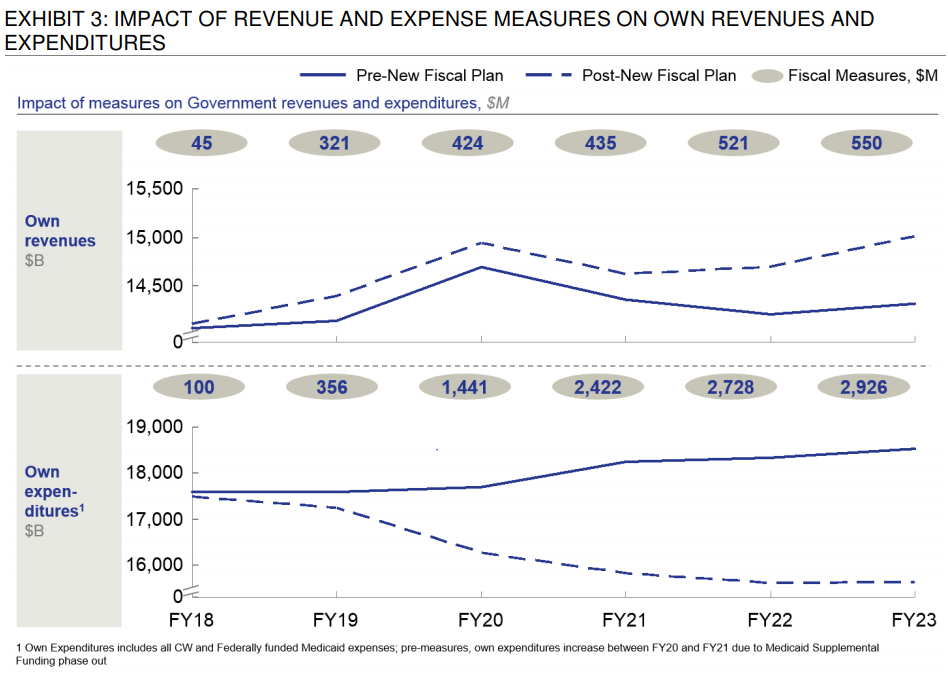

And, well, in July, according to the new fiscal plan put forward by the Oversight board, a new round of fiscal austerity kicks in. Puerto Rico’s fiscal year runs from July to June. The proposed fiscal tightening “measures” are about a percentage point of GNP in fiscal 2019. The board expects this tightening to push down output (relative to baseline) by about 1.25 percent of GNP. Not all of the tightening in fiscal 2019 comes from spending cuts—about half the 2019 measures are designed to raise revenues. But in 2020 and 2021 the austerity really kicks in, with spending cuts (versus baseline) of well over a percentage point of GNP in both years (see exhibit 3 on p. 4).

That austerity is needed in no small part because Puerto Rico is surviving for now off a one-off supplemental increase in Medical funding from the federal government that will run out in 2020.

Before the hurricane, Puerto Rico’s economy was in structural decline—with output (and population) falling by at least a percentage point a year. And its tax favored medical manufacturing sector (Puerto Rico is outside of the United States for income tax purposes, so firms operating in Puerto Rico need not pay U.S. corporate income tax) will be a bit less tax favored after the tax reform,* so it faces a new structural headwind.

It all is rather bleak.

And it make the optimism about Puerto Rico’s near term economic path that is embedded in the latest fiscal plan put forward by the oversight board all the more risky.

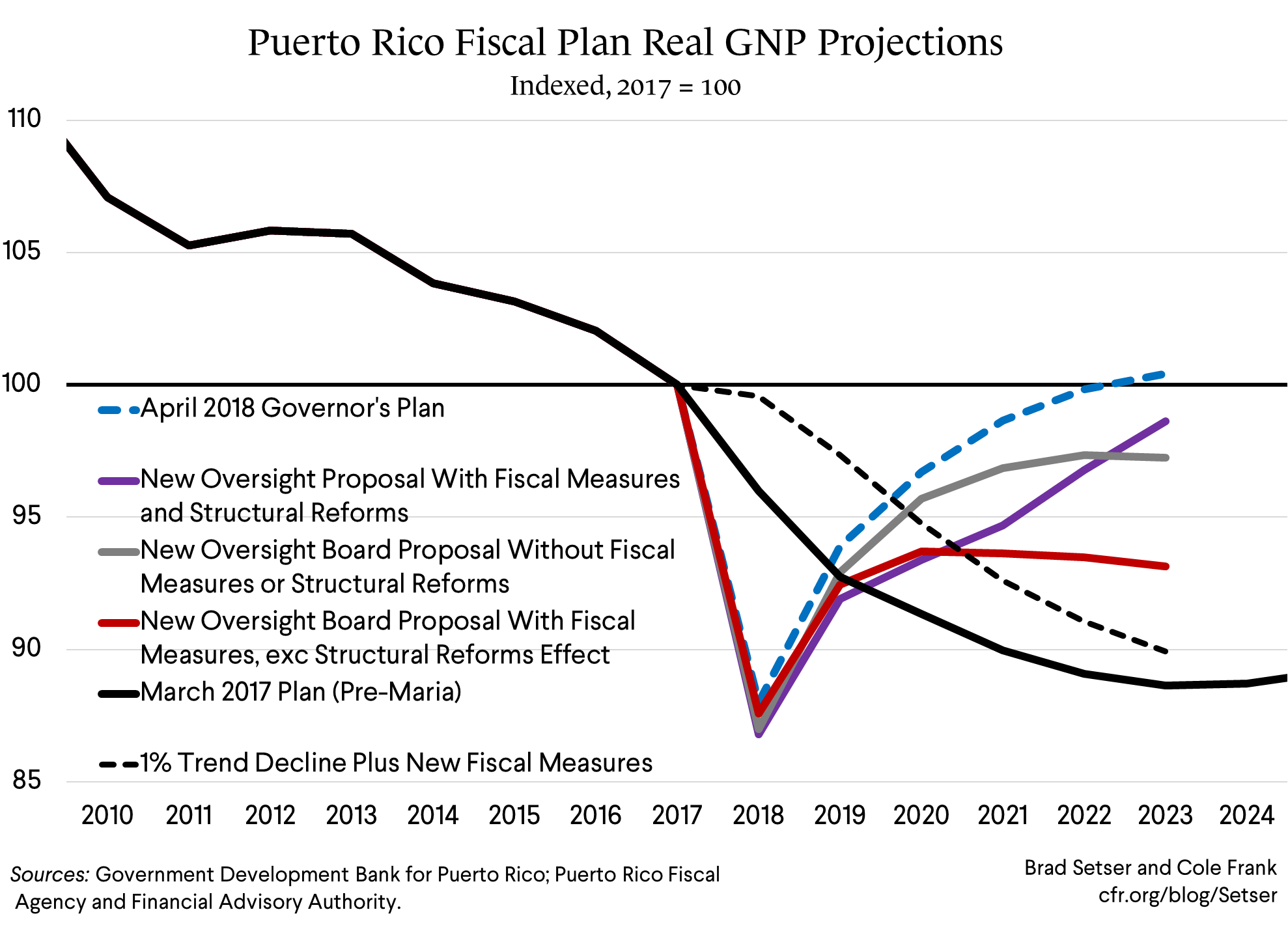

The board has essentially embraced Governor Rosello’s argument that Maria will prove to be a positive growth shock (see my Bloomberg View column with Antonio Weiss and Desmond Lachman). The board isn’t quite as rosy as the governor. But it basically gets close to Rosello’s forecast by 2023—it just gets there through explicitly forecasting very large gains from its proposed structural reforms in the last three years of its fiscal plan (see exhibit 6 on p. 9 of the proposed fiscal plan).

The board’s forecast would put output about 10 percentage points above its forecast the in last year’s fiscal plan in 2023, and only just a bit below its pre-Maria level. And that comes even in the face of a quite strong fiscal consolidation.

Larry Summers aptly described the associated risk: “Puerto Rico’s oversight board will countenance too much debt service and too much austerity because of rosy scenario economics and excessive faith in structural reform.”

Let me try to outline, best I can, the key assumptions behind the baseline growth numbers embedded in the oversight board’s fiscal plan.

- The board’s baseline—which has embedded in it an assumption about the impact of federal disaster relief aid—implies that the pace of underlying economic decline will slow a bit post-Maria. The no (further) fiscal consolidation, no structural economic reform baseline has output down about three percentage points from its pre-Maria levels in 2023. There is a 12-13 percent fall this year, and then solid recovery. This is a tad optimistic in my view. Remember that the underlying pace of decline was about a percentage point a year before Maria, and federal tax law is now at the margin less favorable to Puerto Rico. But there is no doubt that federal disaster spending will help. I am less concerned about the level than the path: federal disaster aid and private insurance funding is projected to decline from fiscal 2021 on, and it isn’t clear that this fall off is having much impact.

- The board forecasts that fiscal consolidation from fiscal 2019 on will knock about five percentage points off output (see exhibit 9 of the fiscal plan on p. 13; I applaud the board for making this transparent). If that was all that was in the board’s forecast, output in 2023 would be about eight points below its pre-Maria level—and not that far off from the level of output embedded in the previous fiscal plan. That’s realistic in my view: if an economy in decline has to do significant austerity, output is forced down. And Congress hasn’t made the fundamental policy choices that would be needed to allow Puerto Rico to avoid a new round of austerity.

- But with disaster spending falling (see exhibit 8) and ongoing austerity, the board is forecasting quite positive growth in fiscal 2021, 2022 and 202 That is because of the projected impact of structural reforms. They appear—based on the growth forecasts in the face of austerity—to be adding about two percentage points to growth in all three years. That seems quite high, given the nature of the reforms. I can see a modest impact from reforms even in an economy that is likely more demand than supply constrained—but would think that a cumulative increase in output (versus baseline) of two percentage points (e.g. a bit over 50 basis points year) would be on the optimistic side. I am suspicious that structural reforms will have a bigger impact than the austerity and fall-off in projected disaster spending (even if the impact of the infusion and then withdrawal of disaster spending on the local economy is modest thanks to a high level of imported content). Remember that before Maria trend growth was negative 1 percent per annum, so getting positive 2 percent growth in the face of austerity takes a really big assumed payoff from reform. (See the difference between the previous board forecast for growth in the out years in exhibit 91, p. 139).

![PR Exhibit 91]()

- The strong projected increase in growth in fiscal 2021, 2022 and 2023 avoids any second round impacts of austerity: revenues go up, not down even with all the fiscal tightening thanks to the projected increase in nominal and real GNP. And that increase in revenue is strong enough to more than offset a forecasted fall in the revenue Puerto Rico is able to collect through a special tax that it now imposes on the “offshore” (for tax purposes) pharmaceutical manufacturing sector (I do give the board credit for forcing Puerto Rico to incorporate a fall in this revenue in its forecast—though in a sense the combination of Maria and tax reform has forced the board’s hand as Act 154 revenue is now falling). Exhibit 80 on p. 126 has the details of the fiscal side of the fiscal plan)

- As a result of these technical assumptions (big and fairly rapid payoff from structural labor market reforms that often are painful in the short-run, a quick payoff from reforms to an electrical system which unquestionably needs fundamental changes and no second round impacts of austerity) Puerto Rico is forecast to run a primary surplus of around 2 percent of GNP in 2023 ($1.4 billion) and sustain that kind of surplus for several years (see exhibit 20 and 21 on p. 27). That’s why the proposed fiscal plan shows more capacity to pay debt than before Maria—which is no doubt both the most politically salient and the most market relevant point.**

That forecast primary surplus is big enough—for a time—to allow Puerto Rico to pay the current coupon on the two groups of tax supported bonds that believe they have the strongest claim (the “constitutional” GOs and the sales tax backed “COFINA” bonds). The forecast primary surplus path thus seems to be at odds with the board’s debt sustainability analysis. It suggests Puerto Rico could sustain a higher level of debt than a typical state even though it is much poorer than a typical state.

Remember, median household income in Puerto Rico is about ½ that of Alabama or Mississippi, and about 1/3 the level of the U.S. If nothing else, an implied debt level that would effectively preclude any realistic path to statehood should get a bit of attention from Governor Rosello.

The real risk though is more fundamental. Forecasting a sustained boom (by Puerto Rican standards) after Maria means Puerto Rico may end up committing to an unrealistic level of debt service. And that would leave a debt overhang that blocks any sustained return to market access—and would make a second debt restructuring likely. Puerto Rico’s disastrous demographics only add to this risk.

The board’s current forecast effectively assumes that Puerto Rico can grow even with a structural fall-off in federal support (as Puerto Rico loses federal medical funding eventually), a fall-off in disaster spending, a shrinking population, and a 2 percent of GNP gap between what Puerto Ricans pay in tax and what they get back in local spending (a burden that Puerto Ricans can escape should they migrate, as no state runs a comparable primary surplus). That seems too optimistic to me—the technical assumptions basically forecast away the downside risk.

And I think that downside risk is substantial. A simple model that keeps trend growth unchanged and adds in the forecast impact from fiscal consolidation gives results similar to last year’s fiscal plan—e.g. another 10 percent or so fall in real GNP, which brings the cumulative fall in output from 2006 to close to 25 percent.

There is another argument that may resonate with more international readers. The board’s technical assumptions from fiscal 2021 onward run contrary to many of the lessons the IMF thinks it learns from the eurozone crisis. The IMF put out a formal lesson learned paper (here’s the summary blog) in 2016 (based on work done in 2015, but formal publications have lags). The analogy is of course imperfect, as the eurozone’s fiscal and banking union differ from the American fiscal and banking union (as applied to the unique case of Puerto Rico). But Puerto Rico is like most eurozone member states an economic unit that has (some) fiscal autonomy (before its debt crisis) while lacking monetary autonomy.

Three of the IMF’s lessons learned seem particularly relevant:

- Recovery inside a monetary union takes time. The oversight board has recognized this. It isn’t assuming that Puerto Rico is going to be able to access markets any time soon, all financing gaps are covered out of revenues (assuming the revenues materialize).

- Fiscal consolidation lowers output and often raises the debt burden in the short-run. It isn’t clear that this lesson has been internalized. The fiscal adjustment is offset in the first few years by disaster spending and then by projected payoff from structural reforms (that Puerto Rico is resisting)—growth is forecast to stay quite positive over the “program” period (e.g. through fiscal 2023). Unrealistically so in my view.

- “Painful” structural reforms are in fact “painful” and don’t yield a quick payoff—they cannot realistically offset the impact of fiscal austerity. This isn’t to say reforms don’t matter—Puerto Rico cannot continue as is, and fundamentally reforming the electrical grid, raising the standard for fiscal transparency, creating a mini-EITC, and ultimately bringing Puerto Rican labor law into closer alignment with U.S. labor law all strike me as necessary even if the labor market reform will be painful. But projecting a big short-term payoff from such reforms that fully offsets the drag from large scale austerity is dangerous—the available precedents suggests that such supply side reforms cannot offset the demand impact of fiscal consolidation.***

To be blunt, the board’s baseline runs the risk of repeating some of the IMF’s initial mistakes in Greece—though the drama may play out more slowly. In Greece the IMF initially made the mistake of thinking that Greece would be able to return to market borrowing quickly, and the mistake of predicting that massive austerity wouldn’t have a big negative impact on output. In Puerto Rico there is no assumption of a quick return to the markets, but there is an assumption that a period of fairly intense austerity won’t drag down growth.

* The impact of the tax reform on Puerto Rico is complicated, but likely to be negative thanks to the BEAT, and the partial deductibility of foreign tax against the GITLI. Puerto Rico historically has been used to move profits on pharmaceutical and medical device sales out of the U.S.—it thus differs a bit structurally from tax havens that largely served to allow American firms to avoid paying U.S. tax on profits from their global sales. Consequently it is likely hit harder than some other tax centers by the “base erosion” measures that are designed to protect the integrity of a territorial system.

** The exact amount of debt that the primary surplus outlined in the fiscal plan can support can and should be debated. It would fall if the board insists on a standard amortizing structure, and insists that the available resources for debt service fall after 2028 (as is in their latest forecast). It also would fall if the board insists that debt payments reflect uncertainty about Puerto Rico’s ability to achieve the optimistic path laid out in the fiscal plan for the next ten years means that Puerto Rico can only commit a fraction of the forecast primary balance to cover contractually fixed debt payments (“the base bond” if there is both a base bond and a growth bond). The fiscal plan for the commonwealth now covers about $40 billion in bonds—as the Highway debt and the Government Development Bank (GDB) debt fall under separate fiscal plans (as of course does the debt of the main utilities PREPA and PRASA). $1.5 to $2b in forecast primary surplus from 2023 to 2028 thus comes reasonably close to covering most of the interest on these bonds. That is why I think it is at odds with the more modest levels of debt proposed in the debt sustainability analysis. Puerto Rico’s underlying level of tax revenue is actually quite modest—it gets $3.5 billion from personal and corporate income tax (a number that would fall to $2.5 billion if it matched the federal EITC), something like $2.5 billion from sales tax, and something like $1 billion from various taxes on crude oil, gasoline, cigarettes, and the like, so something like 10 percent of GNP in tax revenue out of Puerto Rico’s own economy (in no small part because Puerto Rico is poor, and thus the income tax yields less). Without the extra income it gets from the potentially footloose pharma sector, its underlying tax base is small—and I think that is at least relevant for thinking about its capacity to support a high primary surplus.

*** I think there is a strong argument that Puerto Rico cannot achieve the sustained growth the oversight board forecasts without help from the U.S. Congress—it may not be able to do it on its own. Extending the federal EITC would have a tremendous long-run impact in my view—but it would require in effect agreeing to treat Puerto Rico better than a state, as it would get the “reward for low-paid work” now provided through the federal income tax code without paying federal income tax (e.g. all gain, no pain).