Previewing the U.S. Treasury’s April Foreign Exchange Report

The U.S. Treasury Department’s next foreign exchange report is due on April 15—so it should come out soon, maybe even tonight.

Normally the section on China attracts all the attention.

But right now there isn’t any reason to focus the foreign exchange report on China. China has neither been buying or selling large quantities of foreign exchange in the market—and, well, the yuan did appreciate a bit in 2017. China no doubt still manages its currency but it isn’t obviously managing its currency in a way that is adverse to U.S. economic interests. And China’s loose macroeconomic settings have kept its current account surplus down even though China’s industrial policy seeks to displace imports with domestic production. I worry about what may happen if China tightens excessively before it stops saving excessively—but that isn’t an immediate concern.

The real Asian interveners right now are China’s neighbors—Korea, Taiwan, Thailand, and Singapore. All bought foreign exchange on net in 2017, and all also run sizeable current account surpluses. Korea’s surplus is well above 5 percent of its GDP; Taiwan, Thailand, and Singapore all run surpluses of over 10 percent of their GDP. Combined these four countries run a current account surplus of close to $250 billion—bigger, in dollar terms, than either China or Japan. And they all have plenty of fiscal policy space: they could rely more on domestic demand and less on exports.

Singapore isn’t going to be in the report—it is intervening rather massively (also see Gagnon), but it gets an unwarranted free pass as a result of its bilateral trade deficit with the United States (a deficit that likely reflects some tax arbitrage, as firms import into Singapore to re-export).

So I will be most interested in what the Treasury has to say about Korea, Taiwan, and Thailand.

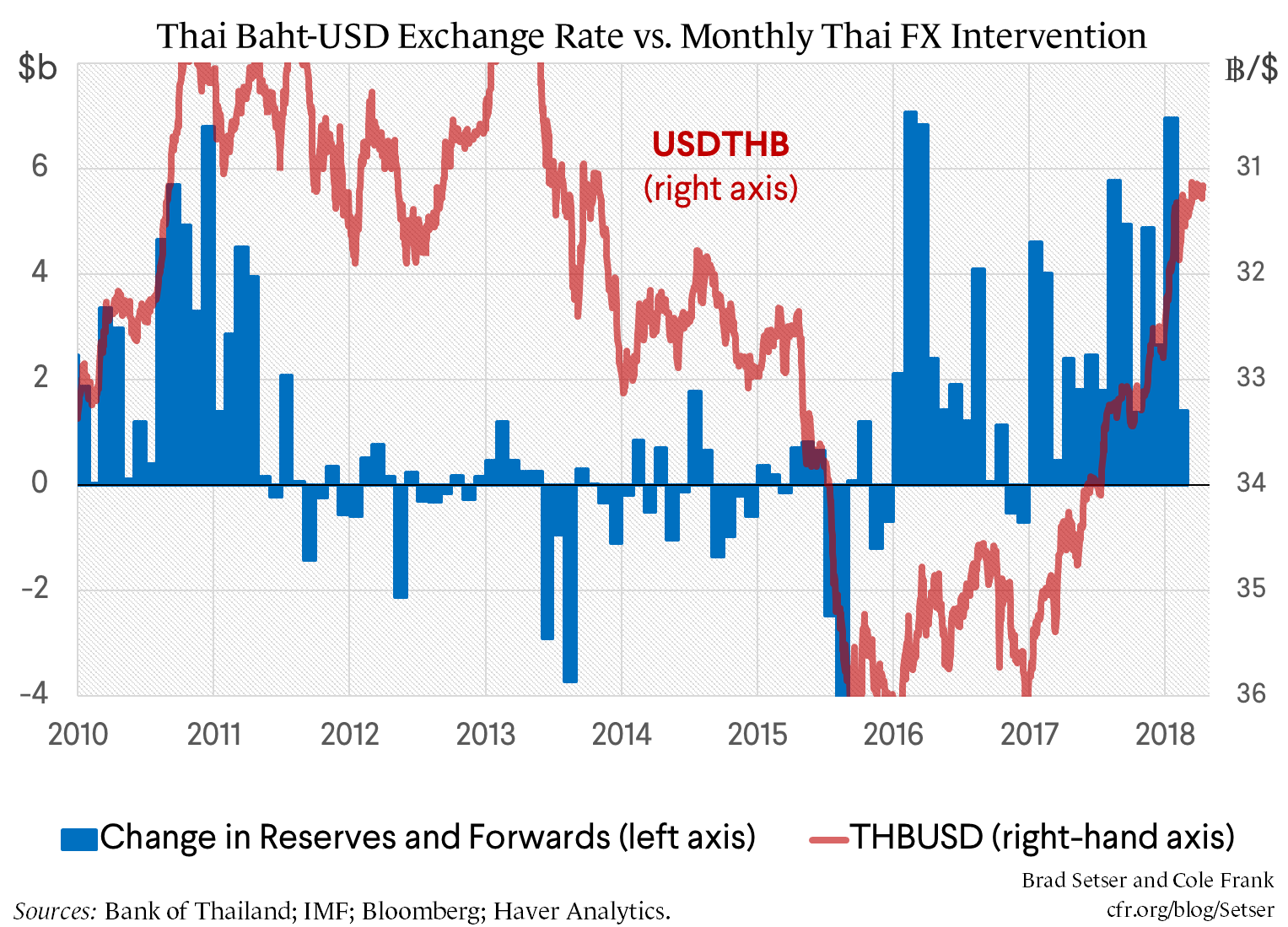

Thailand is the most interesting case.

It hasn’t been traditionally covered in the report as it wasn’t considered a major trading partner.

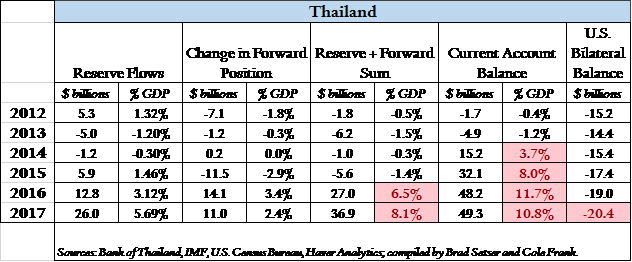

But in 2017 it met all three of the criteria that the Treasury has set out to determine if a country is manipulating: a bilateral surplus of more than $20 billion, a current account surplus of more than 3 percent of GDP, and intervention in excess of 2 percent of GDP. Thailand’s bilateral surplus just topped $20 billion, but it easily meets the other two criteria with a current account surplus of 11 percent of its GDP and intervention of 8 percent of GDP.

I personally think the Treasury should go ahead and name Thailand and give the Bennet Amendment process a test.

There is more than a bit of flexibility in the determination of who counts as a major trading partner. And there is a more intermediate option—the Treasury could indicate that it plans to expand the report’s coverage in October and indicate that if Thailand doesn’t change its policies, it would likely meet all three of the Bennet amendment criteria.

It would be rather disappointing if the Treasury simply sticks to its current list of major trading partners (and leave Thailand out entirely). The changes introduced to a designation under the Bennet amendment were designed to make designation (technically, designation for enhanced analysis) a live option. The actual sanctions are quite mild (arguably too mild) and only come into play after a year of negotiation. And the available sanctions on the Bennet list stop well short of any new tariffs.

In some ways, Thailand is easy. It hasn’t tried to hide its activities in the foreign exchange market and a strict by the books application of the criteria set out in 2015 would lead to the conclusion that Thailand should be named. It has let its currency, the baht, appreciate over the last year (most currencies have strengthened against the dollar) but the scale of both its intervention and its current account surplus stands out.

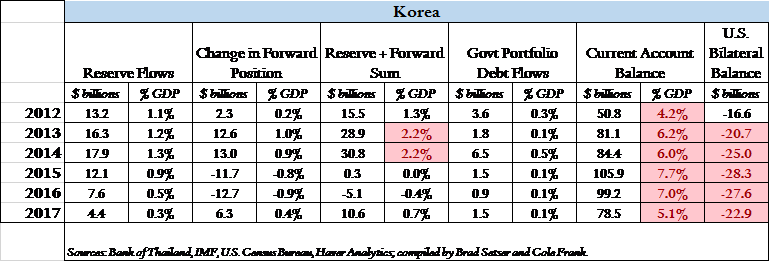

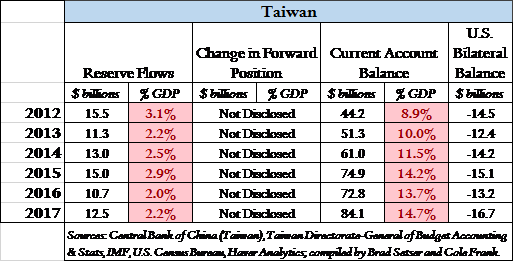

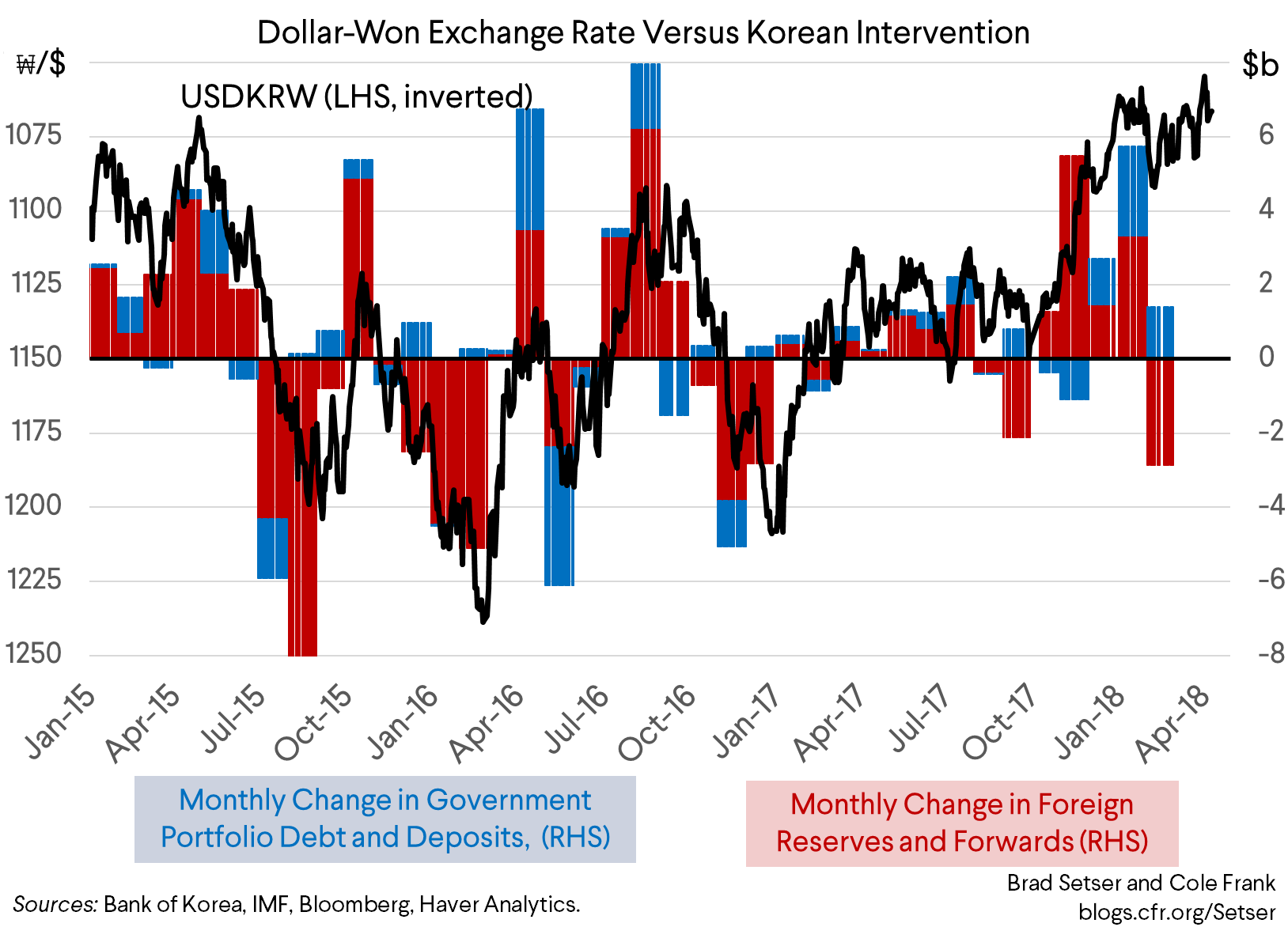

Korea and Taiwan are harder. Both have long been subject to scrutiny in the foreign exchange report. And both have become adept at adopting domestic policies that encourage large capital outflows and thus reduce the need for headline intervention. Korea channels a significant fraction of the buildup of funds in its social security fund (the national pension service) into foreign assets. And Taiwan has allowed its life insurers to buy a ton of foreign assets—loosening limits on foreign exchange exposure in the process (a new note by Citi’s Daniel Sorid and Michelle Yang estimates that the life insurers have added $300 billion to their foreign assets in the last five years, bringing their total foreign portfolio up to $480 billion/65 percent of total assets). As a result of these “structural” outflows from regulated institutions, both Korea or Taiwan have been able to keep their intervention, using the Treasury’s methodology, under the 2 percent of GDP threshold in recent years. Taiwan, though, is close and it has never disclosed its activities in the forward market, so there is a possibility that it actually violates the intervention criteria.*

And this is a case where methodology matters. The Treasury deducts estimated interest income from estimated reserve growth, which helps Taiwan a lot given Taiwan’s enormous stock of reserves. A simple estimate that takes reported reserve flows in the balance of payments and adds in the reported change in the forwards book puts Korea over the threshold in 2013 and 2014 (before the Bennet criteria were articulated) and would put Taiwan just over 2 percent of GDP.**

A by the books application of the Bennet criteria thus would let both Korea and Taiwan off. Treasury could say that neither meets all three criteria and more or less be done with it—perhaps adding that both the won and the new Taiwan dollar appreciated against the U.S. dollar in 2017.

Treasury will of course laud Korea for agreeing to more disclosure in the renegotiated KORUS and ding Taiwan for failing to disclose its forward book or any of the other details that should be disclosed if it voluntarily committed to live up to the IMF’s standard for reserve disclosure. Calling for transparency around intervention is squarely within the Treasury’s comfort zone.

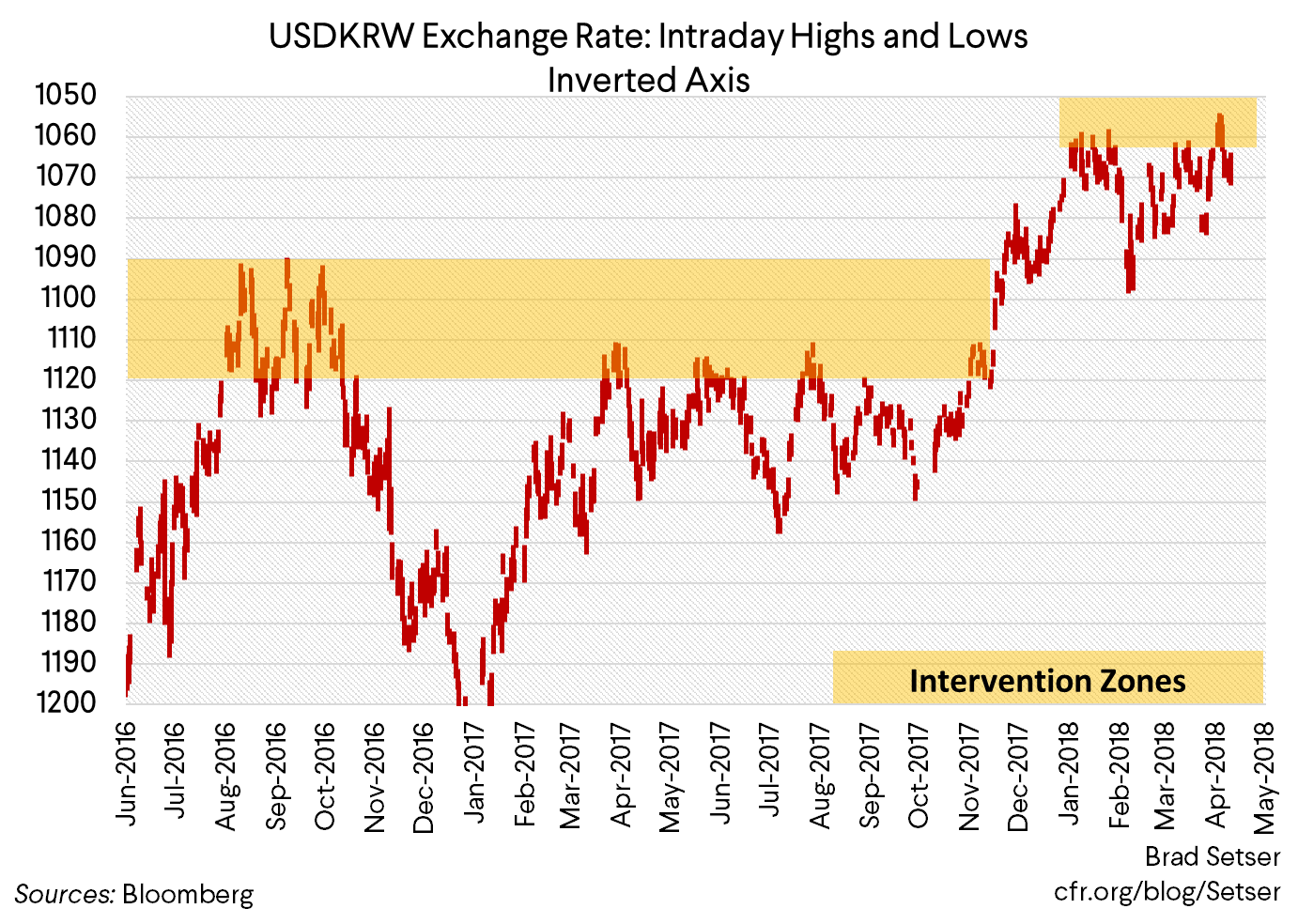

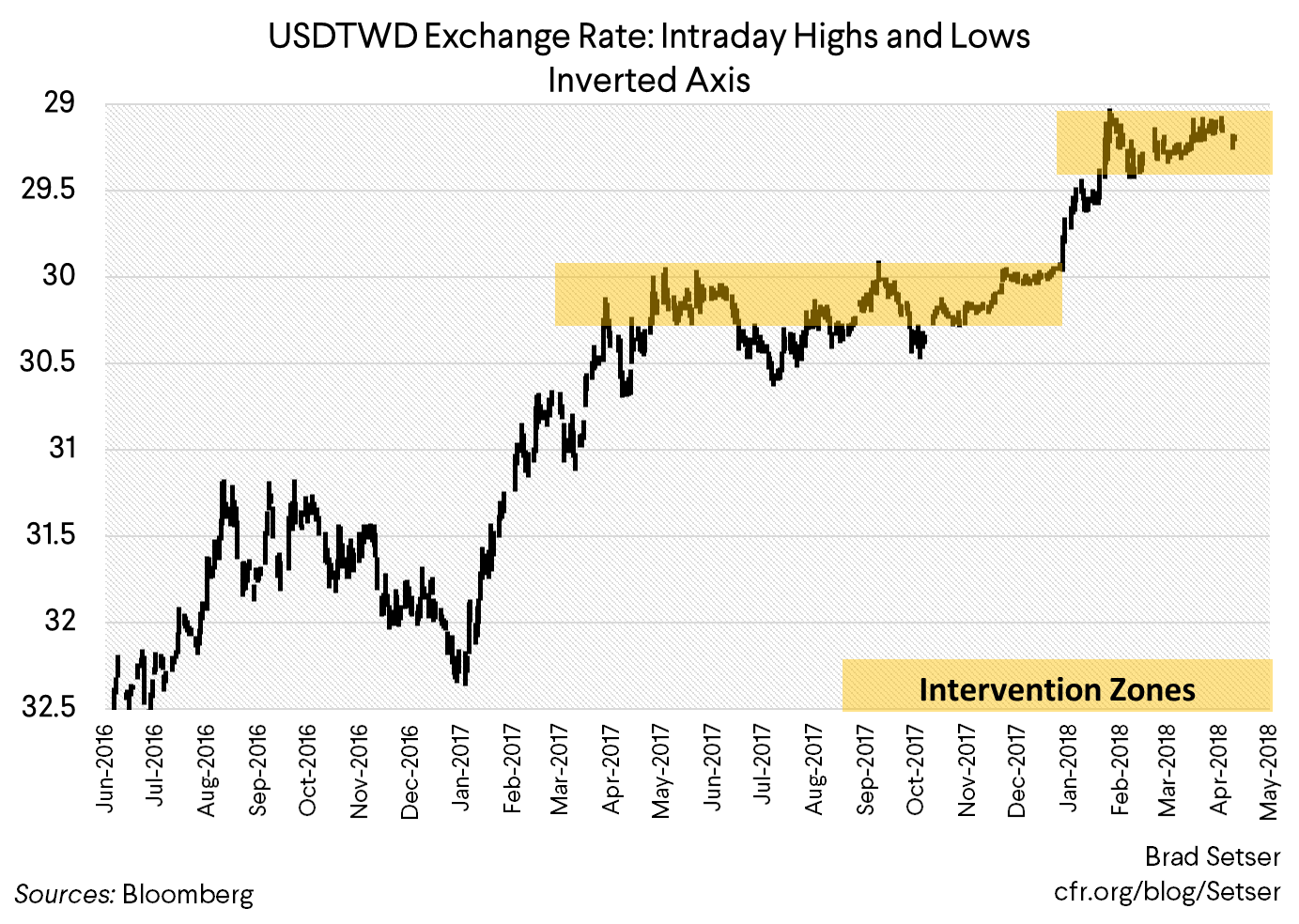

But in this case going strictly by the book would ignore what I think is the real issue. Both Korea and Taiwan are currently intervening to cap the appreciation of their currencies—Korea at 1050 to 1060 won to the U.S. dollar, and Taiwan at around 29 new Taiwan dollars to the U.S. dollar. To be fair, both have shifted the intervention range up a bit in 2018—in early and mid-2017 Korea intervened at around 1100 (it shifted a bit in late 2017), and Taiwan at around 30. But 1050 and 29 are still relatively weak levels for both currencies—given the size of each countries’ surplus** there is ample scope for further appreciation.

I consequently will be watching to see if the Treasury signals that it objects to the level where Korea and Taiwan are intervening even if the amount of intervention falls short of the formal criteria. Korea’s intervention in November, December, and January was actually relatively heavy (the won weakened a bit in February, allowing Korea to sell some of its January purchases, but it looks likely that Korea intervened again to block appreciation through 1050 in late March/early April).

And I am curious if the Treasury will show any sign that it is looking closely at shadow intervention—asking, for example, Korea to disclose the net foreign exchange position (including hedges) of its national pension service, and Taiwan to report not just the central bank’s forward book but also the aggregate foreign exchange position of its regulated insurers. There are also signs that Taiwan’s state banks may have been buying more foreign exchange than in the past. But there I am not holding my breath, I don’t really expect any changes.

Looming in the background is another issue. Without large-scale intervention, foreign demand for Treasuries may be a bit weaker than it has been in the past (see my magnus opus on how the U.S. finances its current account deficit). Deutsche Bank has highlighted this possibility in some of its recent research. They are in my view, more or less right to note that foreign demand for Treasuries historically has been a by-product of intervention, and often, the result of intervention well in excess of the current 2 percent of GDP threshold.

But I am not sure that the Trump Administration is willing to declare that it wants to toss aside the Bennet criteria in order to encourage countries to maintain undervalued currencies so as to raise demand for Treasuries and thus facilitate foreign funding of the fiscal deficit.

*Taiwan though benefits from the bilateral balance criteria, as it exports its chips (semiconductors) to China, and thus the reported bilateral balance understates its “value-added” bilateral surplus. Taiwan’s current account surplus rose in 2017 and is now bigger in dollar terms than Korea’s surplus.

** The Setser/Frank estimates for reserve growth in the tables differ from the Treasury numbers in two ways: Cole Frank and I used the balance of payments data to estimate reserve growth, while the Treasury uses valuation-adjusted change in headline reserves, and I didn’t deduct out estimated interest income. The Treasury believes that only actual purchases in the foreign exchange market should count, and tries to strip out interest income. For countries that already have too many reserves, I think the country should normally sell the interest income received on foreign bonds for domestic currency to cover payments on sterilization instruments and profit remittances back to the Finance Ministry. This matters for a country like Taiwan, which has about 80 percent of GDP in reserve assets. Interest income is likely over a percent of GDP, and will rise over time if U.S. rates continue to increase. I also included for reference changes in the government’s holdings of portfolio debt. These purchases have often appeared in the balance of payments at times when Korea is intervening in the market: they look to be to be a form of shadow intervention.